Written by: Li Jia

Source: Wall Street News

When cannons roar, gold pours in. Just as the market is hotly debating whether Middle East conflicts will drag down the global economy, the S&P 500 and Nasdaq indices have both hit new record highs. What exactly does war mean for U.S. stocks?

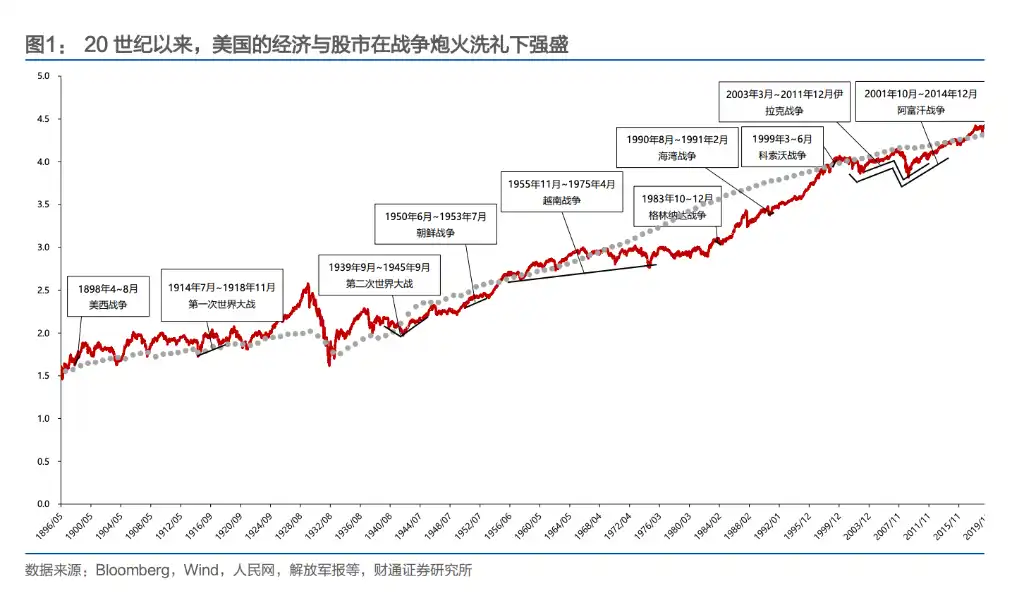

A report from Caitong Securities provides a straightforward answer: War and the long-term bull market in U.S. stocks are not opposites but rather symbiotic. The historical performance of the Dow Jones Industrial Average confirms this—it rose 28% during the Spanish-American War, 26% during the Korean War, and still gained over 80% during the 19-year Vietnam War, while nearly doubling during the Afghanistan War, which spanned the period around the 2008 financial crisis.

Since becoming the world's largest economy at the end of the 19th century, the U.S. has gained substantial benefits from most wars it fought, except for the Vietnam War. From seizing Spanish colonies in the Spanish-American War to profiting handsomely from the two World Wars, and further to the Gulf War and subsequent smaller-scale conflicts centered around oil resources, the U.S. completed its transformation from a 'war participant' to a 'war initiator.'

The reaction path of U.S. stocks amid the sound of gunfire is also clear: During WWII and earlier wars, the market was primarily impacted through sentiment shocks. Starting with the Korean War, this direct effect gradually weakened, and wars increasingly transmitted their impact to the stock market through economic channels like inflation, oil prices, and fiscal deficits.

The Vietnam War was the only war where the U.S. suffered a 'loss,' and it profoundly rewrote its war logic. Since then, almost every conflict initiated by the U.S. has shared three characteristics: short duration, limited geographic scope, and a focus on oil—with all ultimately achieving their objectives.

From 'Taking Advantage of a Fire' to Initiating Trouble: The Three Shifts in American War Strategy

The 1898 Spanish-American War was the first major war actively initiated by the U.S. At that time, domestic monopoly conglomerates urgently needed new markets, investment venues, and sources of raw materials, and Spain's crumbling colonial empire became the ideal target. After the war, the U.S. gained control over Cuba and acquired the Philippine Islands, Guam, and Puerto Rico. The Dow Jones Industrial Average rose 28% during the three-month war, in sync with victories on the main battlefields.

When World War I broke out, the U.S. initially remained neutral. During the market closure in July 1914, investors realized America would become the biggest beneficiary of the European conflict—its homeland, far from the battlefield, could continue production and export arms to Europe. By 1917, American banks, including J.P. Morgan, had provided $10 billion in loans to the British and French governments for purchasing weapons. Although the index fell nearly 10% after the official entry into the war in April 1917, the industrial index had already risen approximately 107% from its low in 1914 to March 1917.

World War II was the crucial conflict that established the U.S. as a global hegemon. At the outbreak in September 1939, U.S. stocks initially fell due to suppressed corporate earnings expectations from the 'excess profits tax'—Congress imposed a tiered tax of up to 95% on profits exceeding $5,000, severely dampening the numerator in the Dividend Discount Model (DDM). It wasn't until the Battle of the Coral Sea and the Battle of Midway in May 1942 turned the tide of war that investors keenly sensed the war's direction, leading U.S. stocks to bottom out and rebound ahead of time. The industrial index rose 82% in the latter half of the war, the transportation index rose 127%, and the utilities index surged 203%.

The Korean War was the first war the U.S. 'did not win.' Although military demand stimulated the post-WWII sluggish economy, the U.S. military failed to achieve its stated objectives. Nonetheless, the Dow Jones Industrial Average still rose 26% throughout the entire period, with the transportation index soaring 86%.

The Vietnam War became a watershed; it was the only war where the U.S. was defeated and gained no benefits.

The U.S. defense budget skyrocketed from $49.6 billion in 1961 to $81.9 billion in 1968 (43.3% of the federal budget), the fiscal deficit ballooned from $3.7 billion to $25 billion, and inflation rose from 1.5% to 4.7%. The U.S. share of the world's total GDP fell from 34% to less than 30%. Post-war, U.S. war strategy shifted completely: it abandoned large-scale ground wars in favor of short-duration, low-casualty, air-strike-centric 'proxy-style' conflicts.

Subsequent wars—the Gulf War, Kosovo War, Afghanistan War, and Iraq War—were all without exception initiated by the U.S., leveraging local conflicts or black swan events. The war zones were mainly concentrated in the Middle East and the Balkans, with the core objectives revolving around oil resource control and military demand.

The Transmission of War to the Stock Market Has Changed: From Sentiment-Driven to Economy-Driven

During WWII and earlier, war events often directly impacted investor sentiment. During the Spanish-American War, victories at the Battle of Manila Bay and the Battle of Santiago de Cuba each drove the index up by about 10% within ten days. In contrast, news of the U.S. entering the two World Wars often triggered panic selling.

But starting with the Korean War, this direct impact gradually faded. From November 1950 to February 1951, despite successive retreats by UN and U.S. forces, the U.S. stock market continued to rise—the reason being that the post-WWII stagnant economy restarted during the Korean War: U.S. real GDP grew about 8.7% in 1950 and remained above 8% in 1951. The fiscal expansion brought by the war, in turn, became a catalyst for economic recovery.

This shift became even more pronounced during the Vietnam War. The Battle of Ia Drang in November 1965 (the first large-scale battle for U.S. troops in Vietnam) did not cause a significant market shock; the 'Tet Offensive' launched by North Vietnam in early 1968 also failed to stop U.S. stocks from reaching new highs. What truly drove the market was instead the Federal Reserve tightening credit conditions in 1966 in response to Vietnam War expenditures, along with the two economic recessions of 1969-1970 and 1973-1975. War sentiment had given way to macroeconomic policy and corporate earnings.

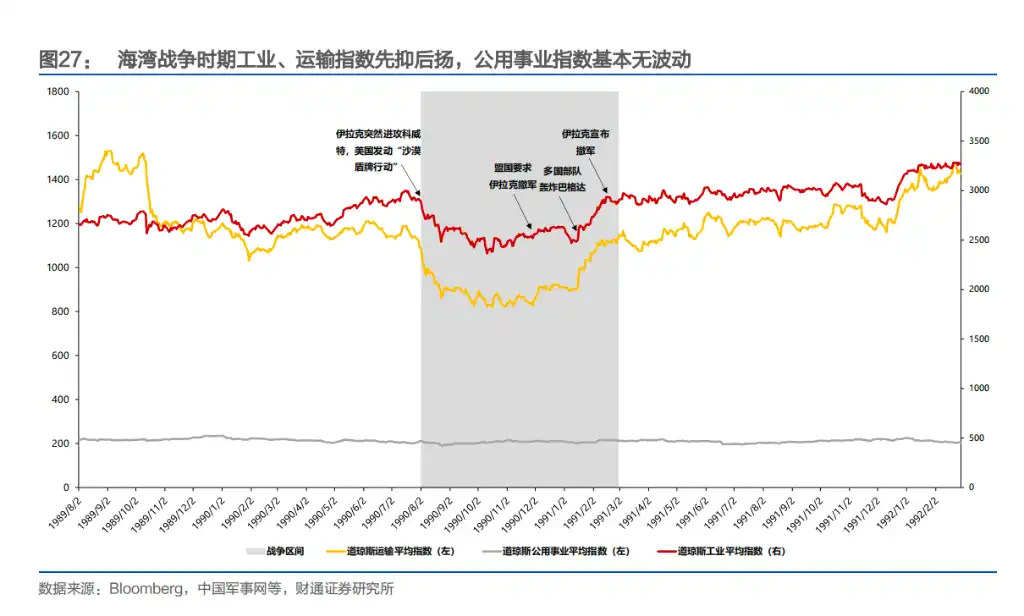

The Gulf War provides the clearest case of 'economic transmission.' After Iraq's invasion of Kuwait in August 1990, oil prices surged, and the market anticipated a U.S. economic recession, pushing S&P 500 valuations to a bottom. When coalition forces bombed Baghdad in January 1991, oil prices fell back to pre-war levels, and the stock market rebounded in sync. During the war, the Dow and crude oil prices moved almost perfectly inversely—the market was trading the trade-off between inflation and growth.

The 2001 Afghanistan War and the 2003 Iraq War further validated this pattern. The most symbolic moment was perhaps the killing of Osama bin Laden in May 2011—arguably the most breakthrough moment in the Afghanistan War. The next day, the Dow fell a mere 0.02%, and the S&P 500 declined 0.18%. The market almost completely ignored the news.

In summary, the reaction of U.S. stocks to war has undergone a clear evolution path: shifting from 'sentiment dominance' to 'economic transmission.' Early wars directly shook the market through news of victories and defeats, but since the Korean War, the stock market has increasingly focused on real economic variables like fiscal expansion, inflation expectations, oil price volatility, and monetary policy.

War itself is no longer the reason for rises or falls; how war affects growth and costs is what the market truly prices.

Which Industry Profits from War? The Answer is Changing

During WWII, coal was the lifeblood of war. Bituminous coal's share rose from 43.8% pre-war to 48.9%, and the industry cumulatively rose 415%.

During the Korean War, oil took over as the new protagonist. Crude oil extraction and refining took the top two spots for gains, with profits climbing continuously from mid-1950 to the first half of 1952. During the Vietnam War, the collapse of the Bretton Woods system forced the U.S. dollar to depreciate, and OPEC was allowed to raise prices to compensate for losses. The oil extraction industry exploded during the dollar crisis from late 1970 to early 1973, surging a staggering 1378% throughout the war.

The Kosovo War continued this pattern, with raw materials and energy industries performing best.

The Gulf War is the only exception—the transmission path shifted to the indirect mode of 'oil price → economic expectations,' making consumer staples and health industries advantageous in the short term, while energy, raw materials, industrials, and other heavy-asset sectors performed the worst.

A notable trend is: As the U.S. economy's size has expanded, the defense industry has transformed from a growth engine into a fundamental part of the economy. The marginal contribution of any single war to the overall economy has been declining, and the driving force for the stock market has increasingly shifted to macroeconomic variables like inflation, interest rates, and fiscal deficits.