Original Author / Tiago Souza, Mario Stefanidis

Compiled by / Odaily Planet Daily Golem(@web 3_golem)

Editor's Note: On February 13th, Coinbase released its Q4 and full-year 2025 financial report.The reportshowed that although Coinbase had a strong full-year performance with trading volume and market share doubling, and platform assets and USDC balances both hitting record highs, it recorded a net loss of $667 million in Q4 2025, with a loss per share of $2.49, and total revenue of $1.78 billion, falling far short of analysts' expectations.

Consequently, several Wall Street investment banks, including JPMorgan and Canaccord,loweredtheir target price for Coinbase stock. However, by the close of US markets on February 14th, COIN still surged by 16.46%, seemingly unaffected by the Q4 earnings miss, proving that the market remains optimistic about Coinbase's various business developments in 2026 in the short term.

But analysts at Artemis believe that in this field, timing is crucial. While Coinbase's market prospects are promising in the long run, its current returns are insufficient to compensate for the risks in the short term. Coinbase remains highly cyclical. Given the continued pressure on brokerage fundamentals and the lagging impact of the current market downturn, the market's general expectations for Coinbase in 2026 are still too high. Therefore, it is not advisable to buy its stock now.

The analysts systematically elaborated on the composition of Coinbase's business revenue, its current advantages, and future challenges. Odaily Planet Daily has compiled and translated the key analysis points below for investors' reference.

Conclusion First: Not Recommended to Invest in Coinbase Now

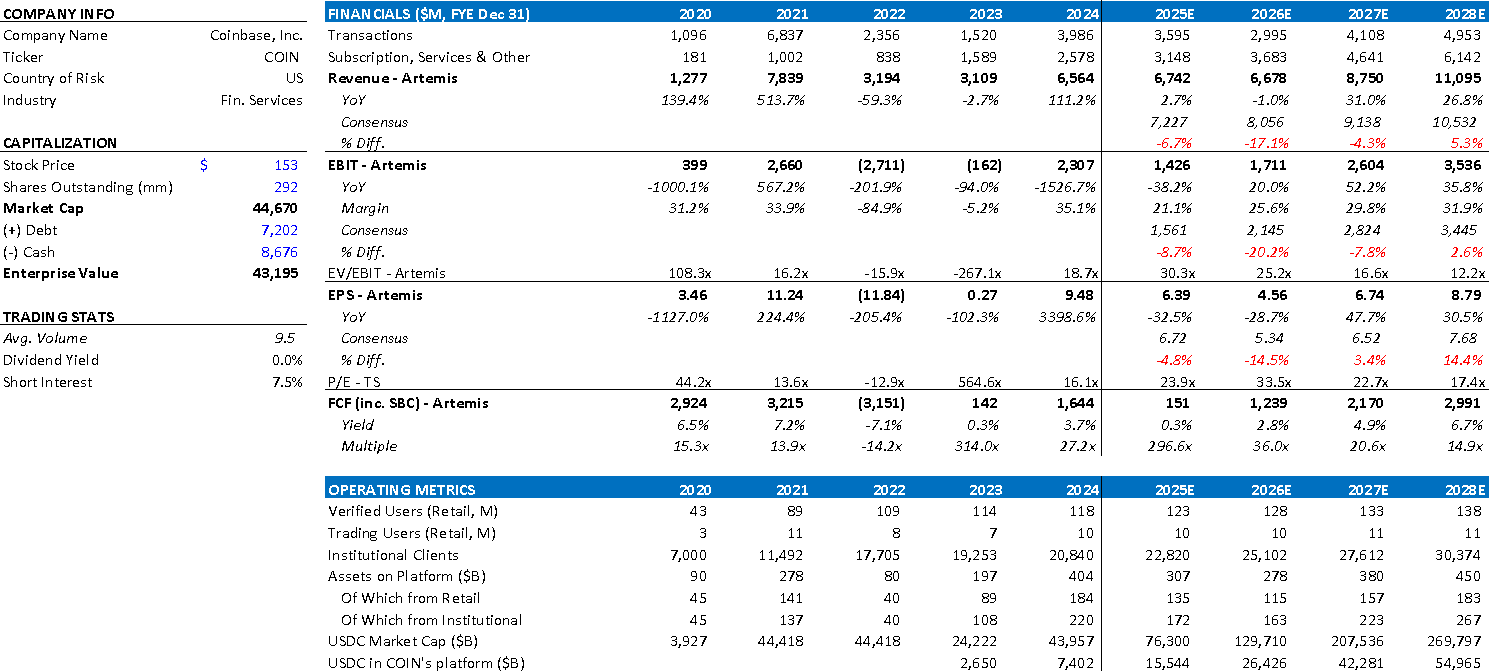

Coinbase's Core Financial Data Over the Years

We currently do not recommend investing in Coinbase because we believe its current returns are insufficient to compensate for the risks. Although Coinbase still holds an absolute leading position in the US market, with a strong institutional client base, a favorable regulatory status, and solid domestic competitive advantages, the timing of investor entry is paramount.

Looking back at previous cryptocurrency sell-offs, earnings estimate downgrades and P/E multiple compression often persist for some time after the initial price correction, as declining account asset sizes and weak trading activity lag behind financial performance. We expect a similar pattern in the current cycle.

Given the continued pressure on Coinbase's brokerage business fundamentals and the high likelihood of earnings falling short of expectations for fiscal years 2025 and 2026, significant downside risks remain. Although Coinbase's long-term franchise value persists, short-term volatility and the potential for earnings misses lead us to conclude: at this stage of the cycle, the expected return is insufficient to compensate for the risk.

Overview of Coinbase's Business Revenue Composition

Coinbase is a centralized cryptocurrency platform whose primary source of revenue is its brokerage business, providing digital asset trading intermediary services for retail and institutional clients. The platform matches client trades with liquidity providers, uses public blockchains to record and settle asset ownership, and integrates with the traditional banking system for fiat deposits and withdrawals.

Despite the competitive and cyclical nature of the trading market, Coinbase is actively expanding its business beyond a pure trading economy model towards broader crypto financial infrastructure and has embedded multiple initiatives directly into its core application. These initiatives include:

- Coinbase One, a subscription product offering zero-fee trading and enhanced services, aimed at boosting recurring revenue and customer retention;

- Prediction markets (in partnership with Kalshi), expanding Coinbase's derivatives and event-driven trading capabilities;

- Tokenized stocks, allowing users to access traditional financial assets via blockchain.

In addition to existing businesses like institutional custody and prime brokerage services, staking and on-chain yield, stablecoin distribution and payments, and derivatives, Coinbase is also building application and settlement infrastructure through its open-source, permissionless Ethereum Layer-2 network, Base.

These initiatives aim to enhance customer engagement and retention, especially at the institutional level, diversify revenue towards more recurring and infrastructure-related income, and transform Coinbase from a trading-oriented broker into a platform and gateway connecting traditional finance with on-chain markets.

Trading Revenue

56% of Total Revenue | 6-Year CAGR 36% | Market Size: $270 Billion (2024)

Trading revenue is the core brokerage business of Coinbase, where the company holds approximately a 14% market share. Revenue comes from transaction fees and spreads charged on platform trading volume.

Trading volume is primarily driven by total platform assets, which are approximately $516 billion, with retail contributing 42% and institutional clients 58%. While institutional clients contribute most asset growth, retail clients remain the primary source of profitability due to significantly higher trading spreads.

- Retail Spread: ~154 basis points

- Institutional Client Spread: ~6 basis points

Institutional clients trade through Coinbase Prime, a suite of standalone products offering advanced execution algorithms, smart order routing, and over-the-counter (OTC) block trading services. These clients require more sophisticated infrastructure but yield lower revenue per dollar, highlighting the importance of retail participation for Coinbase's overall margin profile.

Subscription and Services Revenue

44% of Total Revenue | 6-Year CAGR 232%

This segment aggregates Coinbase's non-trading revenue sources, reflecting the company's strategic shift towards a recurring, infrastructure-driven profit model. It includes the following parts:

- Stablecoins (30% of Revenue)

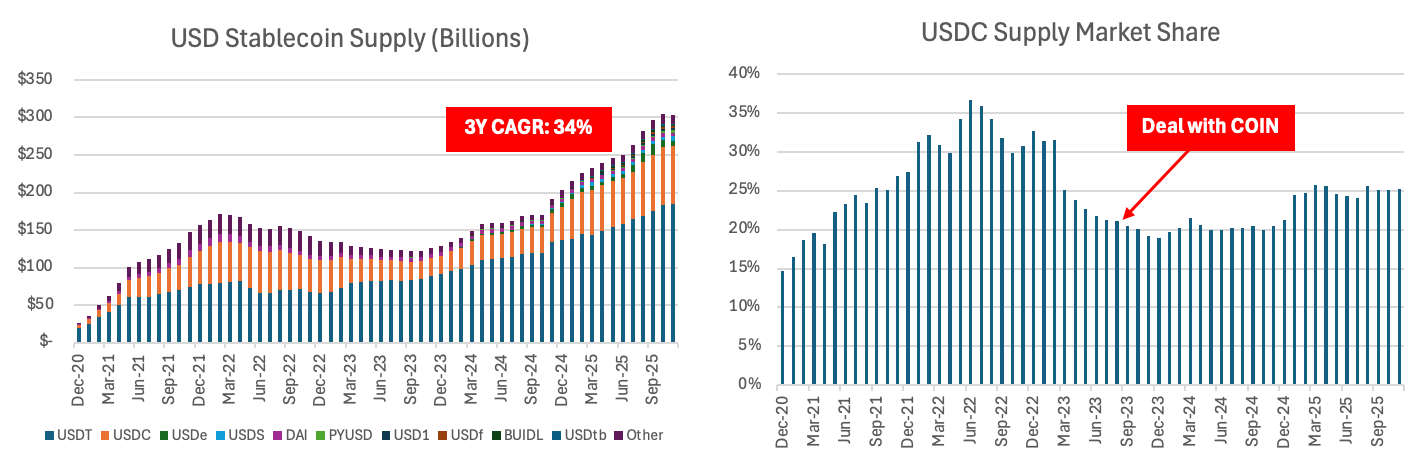

Stablecoin revenue is primarily influenced by USDC adoption and the federal funds rate. Coinbase earns interest income from USDC reserves through a revenue-sharing agreement with the issuer, Circle.

Under the August 2023 agreement, Coinbase receives all interest income generated from USDC on its platform, while interest from USDC held off-platform is split 50/50 between Coinbase and Circle.

This structure makes USDC Coinbase's most significant non-trading revenue source, creating a scalable but interest-rate-sensitive revenue stream that helps reduce the company's reliance on volatile trading volumes (trading revenue still accounted for 86% of total revenue in 2020).

Notably, the majority of the economic value from the Circle partnership accrues to Coinbase, reflecting Coinbase's control over distribution and user access. Data shows that USDC's market share stabilized after a period of decline following Circle's distribution agreement with Coinbase, before beginning to recover, underscoring the central role large, trusted platforms play in stablecoin adoption and reinforcing the strategic value of Coinbase's distribution advantage.

- Staking Services (10% of Revenue)

Customers stake crypto assets through Coinbase, and the company earns a commission from the staking rewards. In proof-of-stake (PoS) networks like Ethereum and Solana, staking involves locking up assets to support network validation. Validators earn rewards akin to yield, which Coinbase facilitates, taking a cut as a service fee.

Key revenue drivers for this segment include crypto asset prices and overall blockchain activity.

- Other Services (4% of Revenue)

This category includes several monetization initiatives launched post-IPO that are currently scaling:

- Coinbase One, a subscription service offering lower trading fees, enhanced rewards, and priority customer support;

- Base, Coinbase's L2 blockchain, enabling developers to build applications and services on-chain;

- Payments, including a prepaid debit card launched in partnership with Visa, allowing customers to spend fiat and earn crypto rewards. Transactions settle in fiat, but the user experience resembles native crypto payments.

Bull and Bear Debates Around Core Coinbase Issues

Can Coinbase significantly reduce its cyclicality, or will its stock remain a leveraged proxy for cryptocurrency (primarily Bitcoin) prices?

Historically, COIN's stock price has been highly correlated with Bitcoin and broader cryptocurrency prices, reflecting its earnings being driven by spot trading volumes.

- Bull Case: Management's moves into subscriptions, stablecoins, derivatives, custody, and Base will diversify revenue and reduce cyclicality over time.

- Bear Case: Despite these initiatives, spot trading still dominates its economics, meaning declines in Bitcoin and major crypto prices will impact its stock price.

Falling crypto assets directly lead to decreased trading volume, margins, and earnings.

Can stablecoins significantly improve the company's profit profile?

- Bull Case: USDC-related revenue is a scalable, high-margin business tied to on-chain payments, treasury use, and tokenized cash, providing a partial hedge against trading volatility.

- Bear Case: Stablecoin revenue is highly sensitive to interest rates, asset mix, and competitive dynamics, meaning rate cuts or changes in custody balances could significantly impact earnings. If stablecoin profits prove cyclical rather than structural, the perceived downside protection in Coinbase's earnings model weakens.

How will regulatory changes over the next 12-24 months impact the company's profit profile?

- Bull Case: Clearer rules will facilitate institutional participation and cement Coinbase's position as the most compliant platform in the US, making it the default gateway to crypto markets.

- Bear Case: Regulation could also attract traditional brokers and financial institutions into crypto, accelerating fee compression and intensifying competition, especially in the retail market. Greater legitimacy might expand trading volumes but could come at the cost of long-term pricing power.

Centralized Exchange Challenges and Coinbase's Unique Advantages

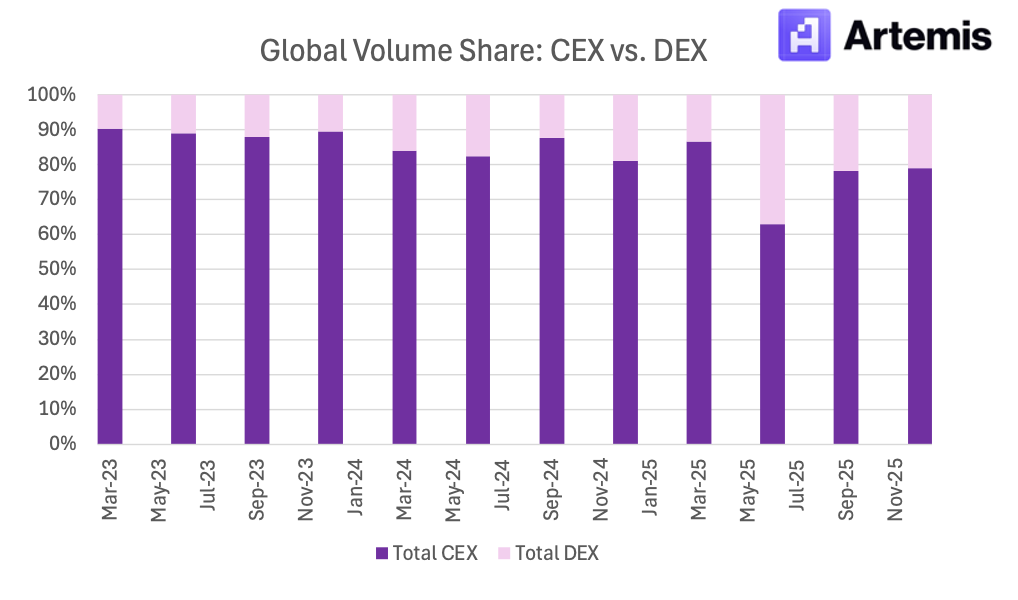

The Rise of DEXs in the Global Trading Market

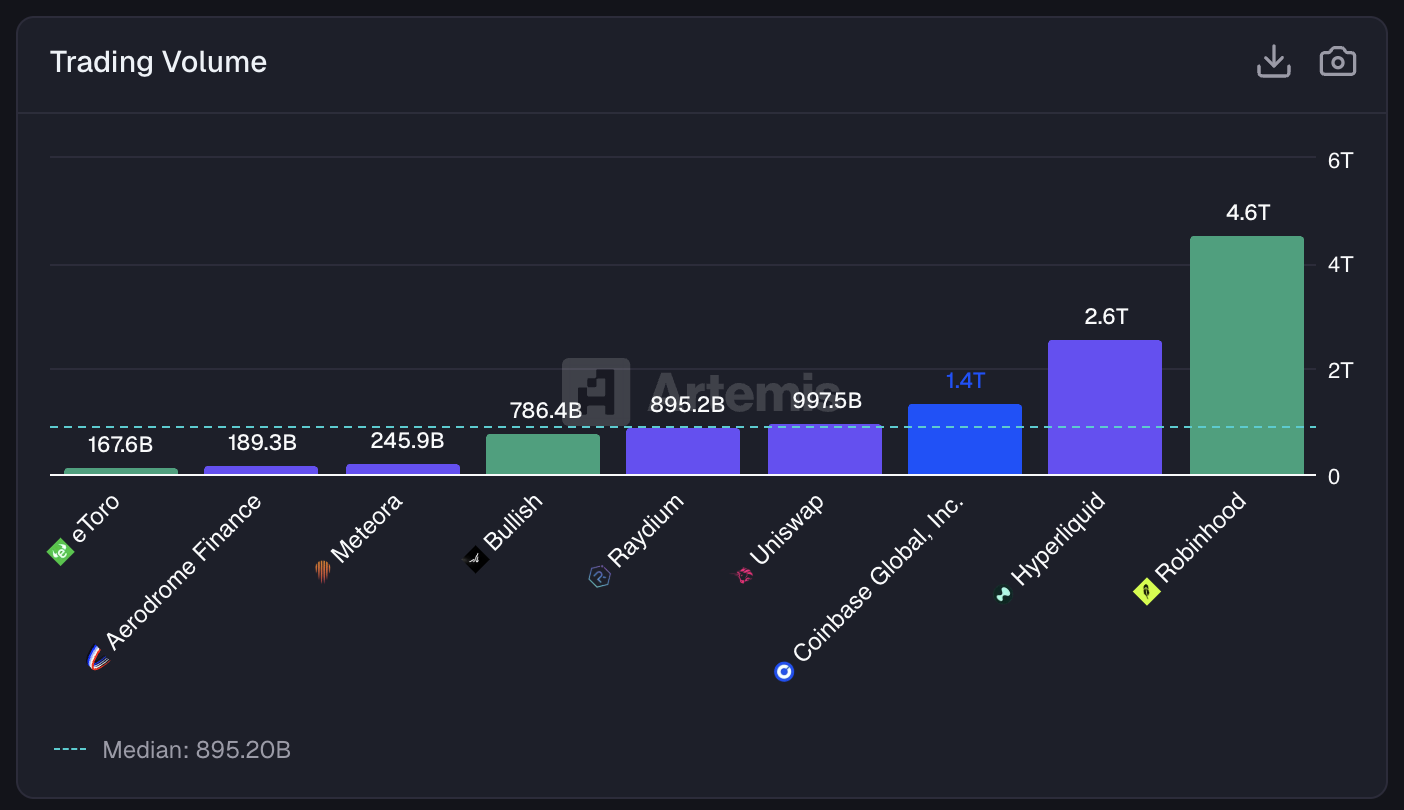

Globally, the total addressable market (TAM) for both centralized exchanges (CEXs) and decentralized exchanges (DEXs) is the same underlying pool of capital: cryptocurrency trading activity encompassing spot, derivatives, and on-chain asset exchanges, with annual nominal volumes currently in the trillions of dollars.

For spot trading alone, industry data shows global CEX spot volume exceeded $18 trillion in 2024, while derivatives volume is significantly larger. In the US, the spot TAM is smaller but still substantial, with USD-denominated spot volume estimated at around $1.5 trillion annually, reflecting the US's importance in fiat liquidity and price discovery. Historically, centralized exchanges (CEXs) have captured the majority of this market due to their deep liquidity, easy fiat on-ramps, and more user-friendly experience, especially for retail and institutional participants.

However, over time, the share of decentralized exchanges (DEXs) in global trading volume has steadily grown, from low single digits a few years ago to over twenty percent today. This shift is more pronounced outside the US, where DEX usage benefits from permissionless access, while US market share remains noticeably lower, constrained by fiat dependency and regulatory friction.

The underlying drivers are structural: L2 networks have reduced transaction costs, improved execution quality and liquidity depth, and the rapid development of the on-chain ecosystem, where functions like trading, lending, and yield generation are increasingly performed natively.

Simultaneously, increased regulatory and compliance burdens have limited product flexibility for CEXs in multiple jurisdictions, while DEXs remain globally accessible by design. Additionally, it's worth noting that in the US, increased regulatory and compliance burdens similarly limit product flexibility for CEXs in multiple jurisdictions, while DEXs are accessible globally without permission.

Therefore, although CEXs still dominate absolute trading volume and institutional flow, especially in the US, DEXs are capturing an increasingly larger share of the global trading market size (TAM), reflecting a gradual but persistent reallocation of trading activity.

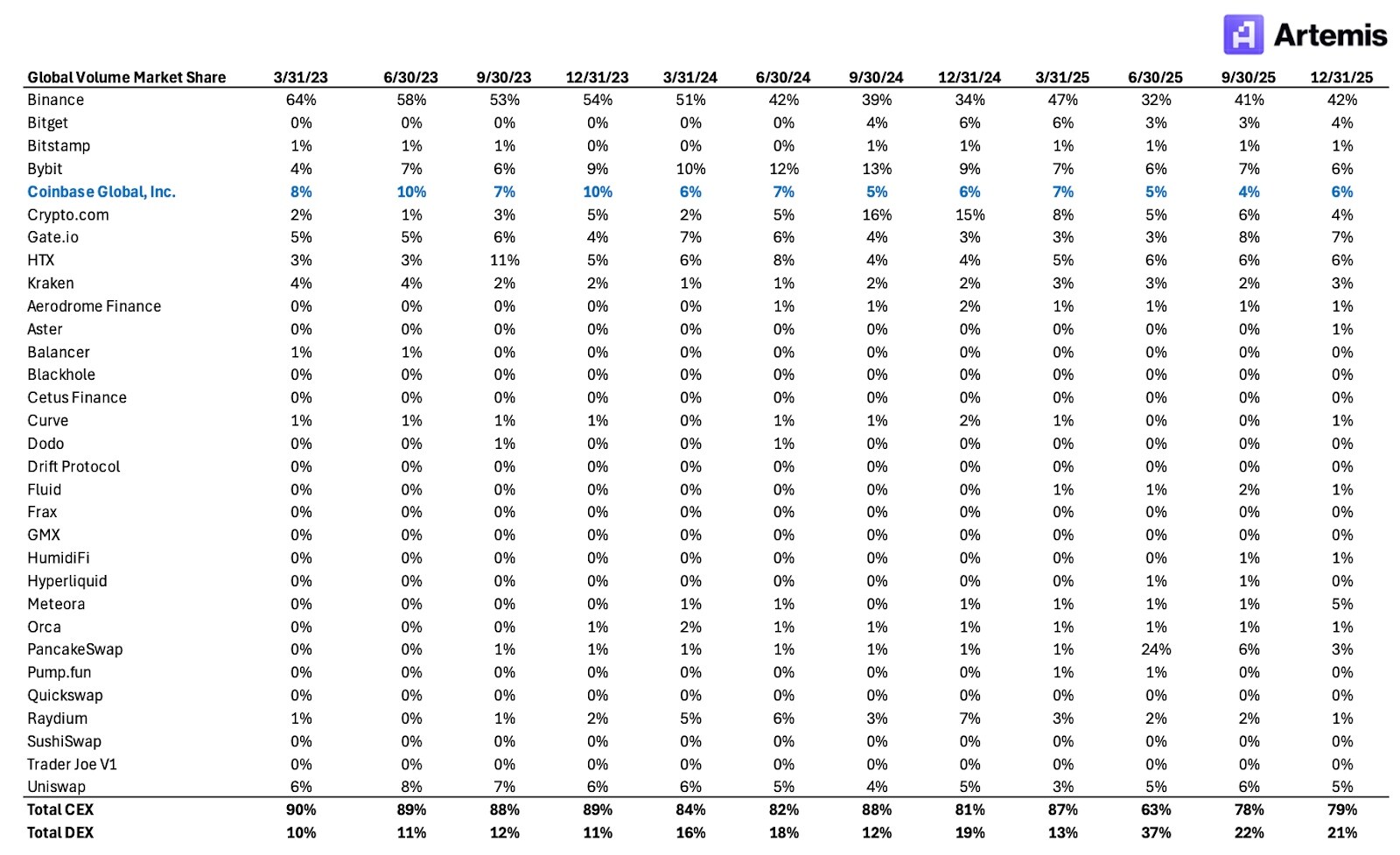

Coinbase's Advantages in the US Market

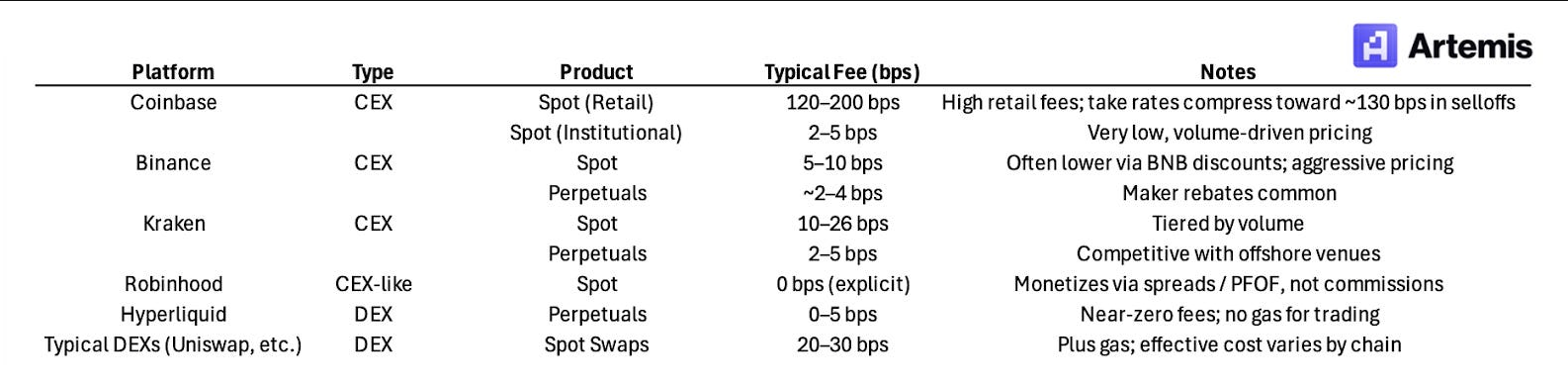

In the global cryptocurrency market, trading fees vary significantly across platforms, reflecting differences in regulatory regimes, cost structures, and competitive intensity. In this context, Coinbase has historically charged fees significantly higher than most global peers, primarily due to its US-centric operational model.

Operating fully within the US regulatory framework implies higher costs (covering compliance and custody standards, reporting, capital requirements, etc.), but it also provides users with a level of legal clarity and security that offshore platforms cannot match. For US retail users, especially during periods of strong market growth, this trade-off has justified paying for convenience, trust, and regulatory certainty.

Fee Rates Charged by Different Exchanges

In the US, Coinbase holds a unique position as the largest and longest-standing regulated cryptocurrency exchange, particularly in USD-denominated spot trading.

Coinbase captures approximately 40% to 50% of US spot cryptocurrency trading volume, with its share even higher during periods of market stress when counterparties prioritize balance sheet safety and regulatory clarity. Coinbase's core customer base includes US retail users who value ease of use and reliable fiat on-ramps, as well as institutional clients (including asset managers, ETFs, corporations, and market makers) who value convenience and regulatory certainty.

This two-sided franchise model is bolstered by deep banking relationships, integrated custody services, and a long history of engagement with US regulators.

But the competitive landscape in the US differs markedly from global markets. Coinbase's main competitors include Robinhood (which competes aggressively on price in the retail market but offers a narrower range of crypto products), Kraken (which attracts more active traders with lower fees), and Binance.US (whose scale and product breadth remain limited compared to its global parent).

Unlike offshore platforms, these competitors operate under similar regulatory constraints, limiting fee arbitrage and product differentiation. Therefore, competition in the US focuses less on who offers the lowest global fees and more on trust, compliance, and USD liquidity. Coinbase's regulatory credibility, institutional penetration, and dominant USD on-ramp position solidify its leadership in the US crypto market, even as competitive pressures intensify at the margins.

Three Arguments for Expecting Suboptimal Future Performance for Coinbase

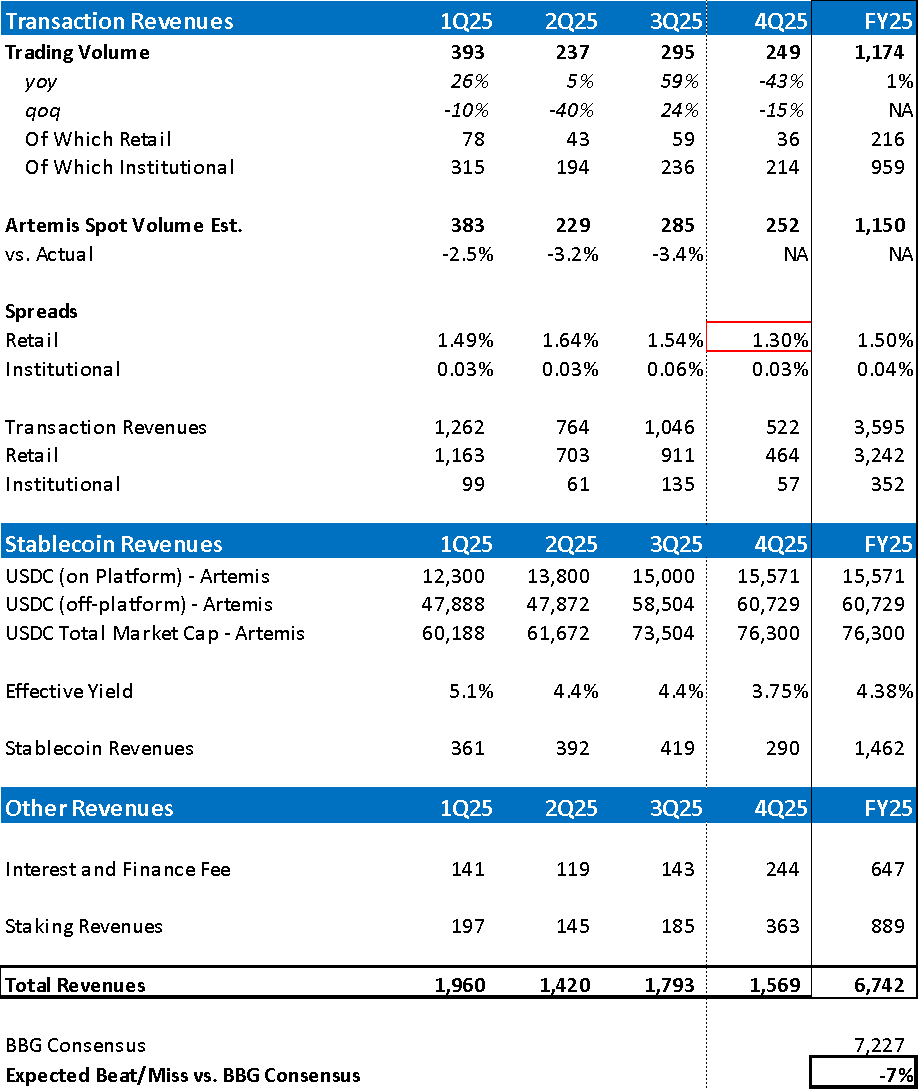

Argument 1: Coinbase's brokerage business is expected to face pressure in Q4 2025, potentially leading to FY2025 revenue being about 7% below market expectations

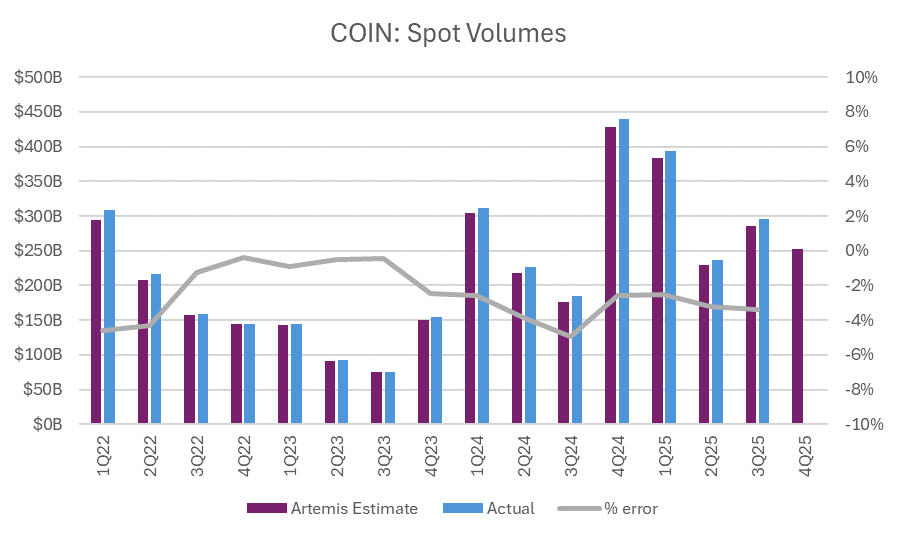

Although Coinbase is expanding into other services on its platform, its earnings remain highly dependent on two main business segments: brokerage and stablecoin-related revenue. This anticipated performance decline stems primarily from continued pressure on the brokerage business in Q4 2025. We estimate this using the Artemis terminal to track Coinbase's spot trading volume, which historically has an average error margin of about 2.5% for quarter-end volume estimates.

Current data indicates a slowdown in trading activity this quarter, with Q4 2025 trading volume around $249 billion. We anticipate a decline in retail take rates, consistent with patterns observed during previous crypto sell-offs, where retail take rates fell to around 130 basis points due to reduced volatility and increased competition. Institutional take rates, already structurally low, are expected to remain below 5 basis points, aligning with patterns from historical downturns.

Argument 2: Headwinds for the brokerage business are expected to persist into 2026, but the downward pressure will be less severe than during the 2022/2023 crypto winter due to portfolio structure changes; EPS for 2026 is expected to be 14% below consensus

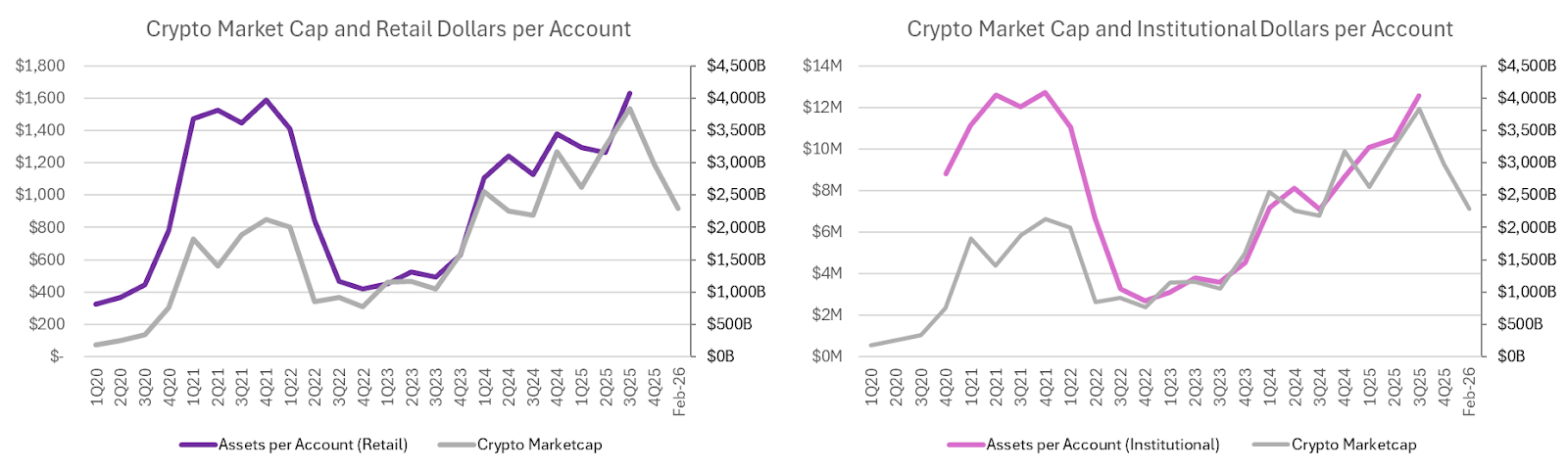

We expect earnings pressure to continue in 2026, primarily driven by the cryptocurrency sell-off that began in 2025 and extended into early 2026. A core variable in the brokerage revenue model is assets per account (the average dollar value held by clients), which has historically been highly correlated with total cryptocurrency market capitalization (~0.8 for retail accounts, ~0.6 for institutional accounts). This dynamic is particularly important given retail clients' higher sensitivity to market swings and typically higher fee rates.

As of February 2026, the total cryptocurrency market cap is down approximately 20% from the end of 2025, following a 22% decline in Q4 2025, indicating continued pressure on client asset balances. In our base case forecast, we model a compression in retail assets per account of nearly 10% for 2026, and institutional account balances also compressing nearly 10%.

We assume a recovery pattern consistent with previous cycles in 2027, with market cap rebounding to 2024 levels, followed by sustained growth of around 15% annually thereafter, leading to outperformance relative to consensus expectations in later years.

On the stablecoin front, we continue to model strong growth, anticipating ~40% growth in 2026, supported by USDC market cap growth of ~70% versus 2025, albeit slowing from the ~110% growth seen from 2024 to 2025. This growth partially offsets brokerage weakness.

However, overall, we project total revenue to decline by approximately 1% in 2026, implying revenue ~17% below consensus, with EPS declining ~15%, as operating leverage amplifies the impact of weak trading fundamentals.

Argument 3: Regulatory progress in 2026 is structurally positive but too slow to offset near-term earnings pressure

We expect regulatory clarity in the US crypto market to improve in 2026, potentially through partial market structure legislation, reducing legal uncertainty and strengthening the position of compliant incumbents like Coinbase. In principle, clearer rules could be a significant catalyst for broader crypto adoption, especially among institutional investors, unlocking new pools of capital and expanding the TAM.

Members of the SEC's crypto working group have previously indicated that "regulators are expected to issue guidance clarifying the line between securities and non-securities in the crypto space, provide potential innovation exemptions for tokenized securities and new on-chain market structure pilot programs, and expand the use of no-action letters to indicate that certain activities are not enforcement priorities."

However, the legislative process remains slow, and the pace of implementation suggests that any substantial adoption benefits will materialize gradually over time rather than immediately. In the near term, Coinbase's financial performance remains primarily driven by crypto prices, retail trading volumes, and take rates—factors currently under pressure amid a prolonged adjustment phase. Institutional adoption, while supported by regulatory progress, tends to be gradual and carries structurally lower trading margins.

Furthermore, regulatory optimism is already largely priced into market sentiment following ETF approvals and recent policy signals. Therefore, while regulatory improvement does represent a long-term structural positive, its slow pace renders these benefits insufficient to offset near-term earnings headwinds, creating downside risk to consensus expectations for 2026 and 2027.

Valuation Forecasts Under Different Scenarios

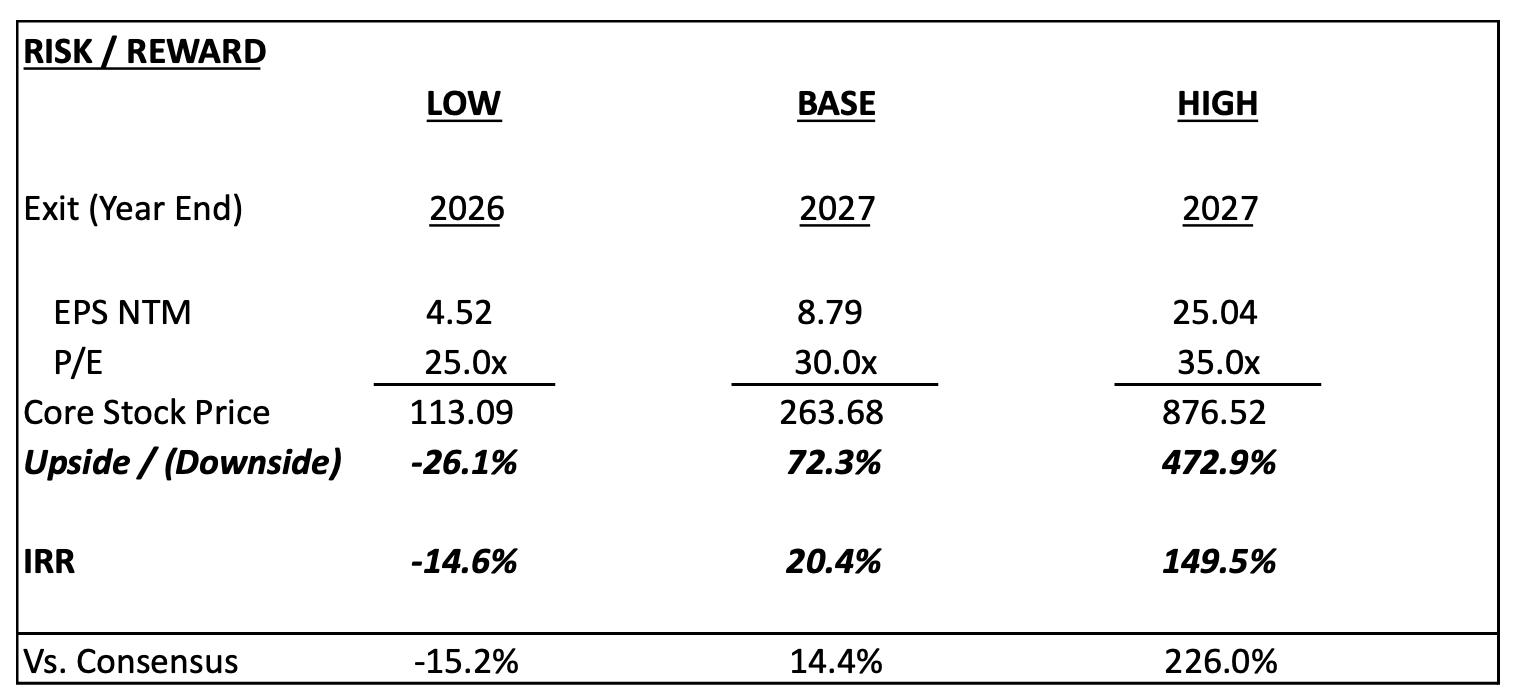

Low Valuation Scenario

We assume a prolonged downturn comparable to the 2022-2023 cycle, modeling a ~50% decline in assets per account for 2026 and flat growth in 2027, reflecting sustained weakness in user engagement and asset balances. We assume USDC growth slows to ~25% annually, as on-chain activity and risk appetite remain subdued.

In this scenario, pressure on Coinbase's brokerage business persists, operating leverage remains constrained, and visibility into earnings sustainability diminishes. Consequently, we apply a more conservative 25x NTM P/E multiple as an exit multiple at the end of 2026, appropriate for Coinbase valued as a highly cyclical brokerage. This scenario implies a negative IRR of approximately 15%, highlighting the downside risk if the adjustment proves deeper and longer than expected.

Base Case Scenario

We assume a more moderate adjustment, with retail assets per account declining nearly 10% in 2026 and institutional client assets declining nearly 10%, followed by a recovery to 2024 levels in 2027 as crypto market cap rebounds.

For stablecoins, we model ~40% annualized growth, with stronger growth in 2026 and 2027 (~70% and ~60% respectively), reflecting continued USDC adoption. Growing stablecoin revenue partially offsets brokerage weakness and gradually improves the overall revenue mix.

We apply a 30x NTM P/E multiple as an exit multiple at the end of 2027, implying an attractive ~20% IRR over three years. However, we acknowledge path dependency is crucial: although the model's final returns are compelling, the anticipated earnings miss in 2026 and potential future volatility make the risk-adjusted trajectory less attractive.

Optimistic Scenario

We assume an initial adjustment similar to the base case, with retail assets per account declining nearly 10% in 2026 and institutional client assets declining ~14%, followed by a stronger rebound starting in 2027. Under this scenario, assets per account grow ~80% in 2027 and 2028, broadly in line with the recovery seen in 2023-2024, followed by sustained growth in the high single digits thereafter.

For stablecoins, we project USDC market cap growing at a ~56% CAGR through 2030, with ~80% growth in 2026 and ~50% in 2027, reflecting accelerated USDC adoption and expanding on-chain utility.

Under these assumptions, Coinbase's revenue mix becomes significantly less cyclical, supporting higher operating leverage and justifying a 35x expected P/E (NTM P/E) valuation by the end of 2027, implying an IRR of approximately 226% over three years.