Original Author: Santiago Roel Santos

Original Compilation: Luffy, Foresight News

As I write this article, the cryptocurrency market is experiencing a sharp decline. Bitcoin has touched the $60,000 mark, SOL has fallen back to the price level during the FTX bankruptcy asset liquidation, and Ethereum has also dropped to $1,800. I won't dwell on the long-term bearish arguments.

This article aims to explore a more fundamental question: why can't tokens achieve compound growth?

For the past few months, I have held a persistent view: from a fundamental perspective, crypto assets are severely overvalued. Metcalfe's Law cannot support the current valuations, and the divergence between industry application and asset prices may persist for years.

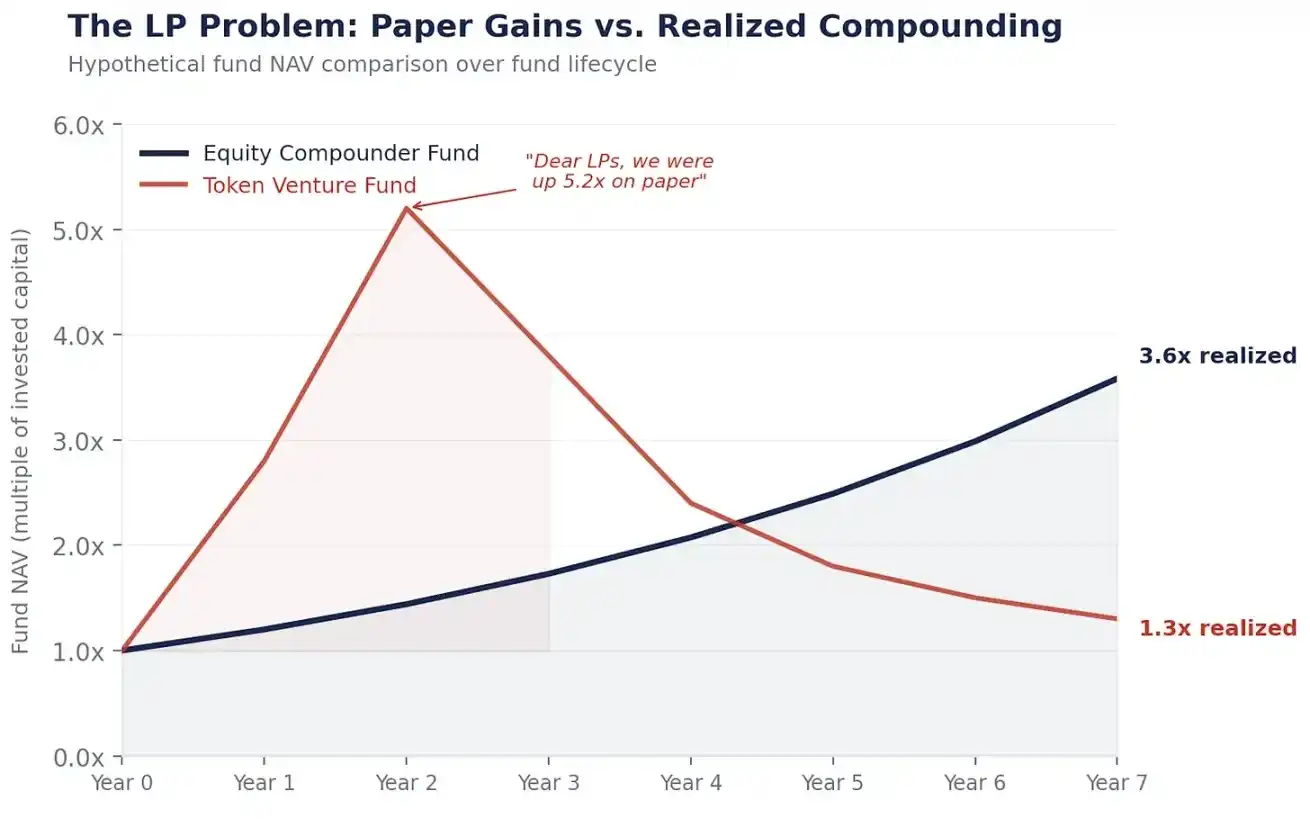

Imagine this scenario: 'Dear liquidity providers, stablecoin trading volume has grown 100-fold, but the returns we bring you are only 1.3 times. Thank you for your trust and patience.'

What is the strongest counterargument to all this? 'You're too pessimistic and don't understand the value proposition of tokens; this is a new paradigm.'

I understand the value proposition of tokens all too well, and that is precisely the crux of the problem.

The Compound Interest Engine

Berkshire Hathaway's market capitalization is now about $1.1 trillion. This is not because of Buffett's perfect timing, but because the company has the ability to compound.

Every year, Berkshire reinvests its profits into new businesses, expands profit margins, acquires competitors, thereby increasing the intrinsic value per share, and the stock price follows. This is an inevitable result because the underlying economic engine is continuously growing.

This is the core value of a stock. It represents ownership of a profit-reinvesting engine. Management earns profits, then allocates capital, plans for growth, cuts costs, buys back stock. Every correct decision becomes a building block for the next phase of growth, creating compound interest.

$1 growing at a 15% compound rate for 20 years becomes $16.37; $1 stored at a 0% interest rate for 20 years remains just $1.

Stocks can turn $1 of profit into $16 of value; tokens can only turn $1 of fee revenue into $1 of fee revenue, with no appreciation.

Show Me Your Growth Engine

Consider what happens after a private equity fund acquires a business with $5 million in annual free cash flow:

Year 1: Achieves $5 million free cash flow. Management reinvests it into R&D, building a stablecoin custody channel, paying down debt—three key capital allocation decisions.

Year 2: Each decision yields returns, free cash flow increases to $5.75 million.

Year 3: The gains from earlier continue to compound, supporting the implementation of new decisions, free cash flow reaches $6.6 million.

This is a business compounding at 15%. The increase from $5 million to $6.6 million isn't due to market euphoria, but because every capital allocation decision made by people empowers the next, building layer upon layer. Persist like this for 20 years, and $5 million will eventually become $82 million.

Now consider a crypto protocol with $5 million in annual fee revenue:

Year 1: Earns $5 million in fees, distributed entirely to token stakers. Capital completely exits the system.

Year 2: Might earn $5 million again, provided users are willing to return, then distributed entirely again. Capital exits again.

Year 3: Earnings depend entirely on how many users are still playing at this 'casino'.

There is no compounding because there was no reinvestment in Year 1, hence no growth flywheel by Year 3. Subsidy programs alone are far from sufficient.

Token Design is Inherently Like This

This is not accidental; it's a legal strategy.

Looking back to 2017-2019, the SEC cracked down on all assets that resembled securities. At that time, all lawyers advising crypto protocol teams gave the same advice: never make tokens look like stocks. Don't give token holders a claim on cash flows, don't give them governance rights over the core development entity, don't retain earnings, define them as utility assets, not investment products.

Thus, the entire crypto industry designed tokens to deliberately distinguish them from stocks. No cash flow claims, avoiding the appearance of dividends; no governance rights over the core development entity, avoiding the appearance of shareholder rights; no retained earnings, avoiding the appearance of a corporate treasury; staking rewards are defined as network participation rewards, not investment returns.

This strategy worked. The vast majority of tokens successfully avoided being classified as securities, but simultaneously, they lost all possibility of achieving compound growth.

This asset class was deliberately designed from its inception to be incapable of performing the core action that creates long-term wealth—compounding.

Developers Hold Equity, You Hold the 'Coupon'

Every major crypto protocol corresponds to a for-profit core development entity. These entities develop the software, control the front-end interface, own the brand, and manage enterprise partnership resources. And the token holders? They only get governance voting rights and a variable claim on fee revenue.

This model is ubiquitous in the industry. The core development entity holds the talent, intellectual property, brand, enterprise contracts, and strategic choices; token holders only get a variable 'coupon' tied to network usage and the 'privilege' of voting on proposals that the development entity increasingly ignores.

This also explains why when Circle acquires a protocol like Axelar, the acquirer buys the equity of the core development entity, not the tokens. Because equity compounds, tokens do not.

Lack of clear regulatory intent has fostered this distorted industry outcome.

What Are You Actually Holding

Set aside all market narratives, ignore price fluctuations, and look at what token holders actually receive.

Staking Ethereum, you get about 3%-4% yield, determined by the network's inflation mechanism and adjusted dynamically based on the staking rate: more stakers, lower yield; fewer stakers, higher yield.

This is essentially a variable-rate coupon tied to the protocol's predetermined mechanism. It's not a stock; it's a bond.

Admittedly, Ethereum's price might rise from $3,000 to $10,000, but the price of a junk bond can also double if the spread narrows—that doesn't turn it into a stock.

The key question is: by what mechanism does your cash flow grow?

Stock cash flow growth: Management reinvests profits, achieving compound growth. Growth magnitude = Return on Capital × Reinvestment Rate. You, as a holder, participate in an expanding economic engine.

Token cash flow: Depends entirely on network usage × fee rate × staking participation. You receive a coupon that fluctuates with block space demand. There is no reinvestment mechanism in the entire system, no engine for compound growth.

Significant price volatility makes people think they hold stocks, but economically, they hold fixed-income products with an attached 60%-80% annualized volatility. This is the worst of both worlds.

The vast majority of tokens, after deducting inflationary dilution, offer a yield of only 1%-3%. No fixed-income investor in the world would accept this risk-reward ratio, but the high volatility always attracts waves of buyers—a true portrayal of the 'greater fool theory'.

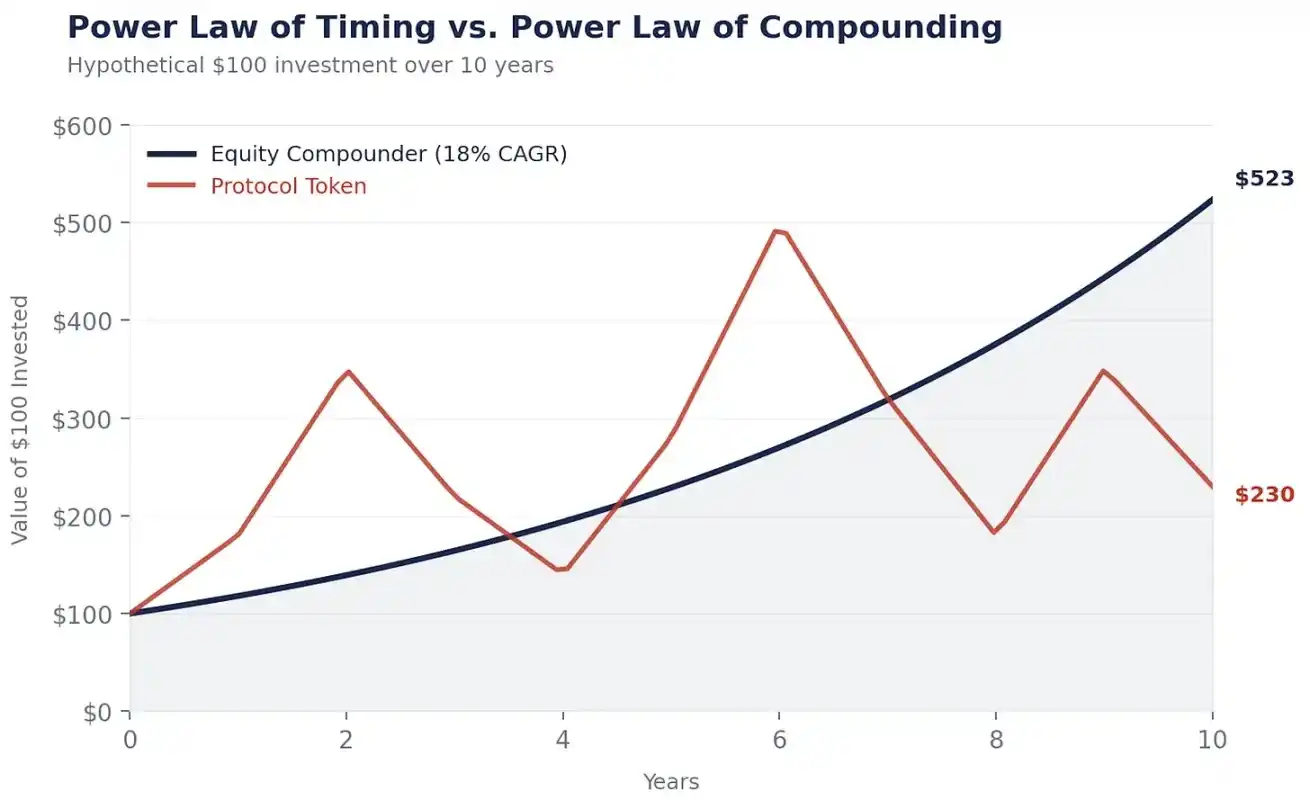

Power Law of Timing, Not Power Law of Compounding

This is why tokens cannot achieve value accumulation and compound growth. The market is gradually realizing this. It is not stupid; it is shifting towards crypto-related stocks. First, digital asset treasuries, then increasingly, capital flows into enterprises that use crypto technology to reduce costs, increase revenue, and achieve compound growth.

Wealth creation in crypto follows the power law of timing: those who make huge profits buy early and sell at the right time. My own portfolio follows this pattern. Crypto assets are called 'liquid venture capital' for a reason.

Wealth creation in stocks follows the power law of compounding: Buffett didn't make money on Coca-Cola by timing the purchase, but by buying and holding for 35 years, letting compounding work.

In crypto, time is your enemy: hold too long, and profits evaporate. High inflation mechanisms, low float, high fully diluted valuation (FDV) design, coupled with insufficient demand and excess block space, are key reasons. Super-liquid assets are rare exceptions.

In stocks, time is your ally: the longer you hold a compounding asset, the more remarkable the gains.

The crypto market rewards traders; the stock market rewards holders. And in reality, far more people get rich by holding stocks than by trading.

I have to repeatedly check these numbers because every liquidity provider asks: 'Why not just buy Ethereum?'

Pull up the chart of a compounding stock—Danaher, Constellation Software, Berkshire—and compare it to Ethereum's chart: the compounding stock's curve climbs steadily up and to the right because its underlying economic engine grows stronger every year; Ethereum's price surges and crashes, cycles repeatedly, and the ultimate cumulative profit depends entirely on your entry and exit timing.

Perhaps the final returns might be similar, but holding stocks lets you sleep soundly at night, holding tokens requires you to be a prophet who can predict the market. 'Time in the market beats timing the market'—everyone knows it, but the hard part is actually holding long-term. Stocks make long-term holding easier: cash flow supports the stock price, dividends give you patience, buybacks compound while you hold. The crypto market makes long-term holding extremely difficult: fee revenue dries up, market narratives change, you have nothing to rely on, no price floor, no stable coupon, only belief.

I'd rather be a holder than a prophet.

Investment Strategy

If tokens cannot compound, and compounding is the core way to create wealth, then the conclusion is self-evident.

The internet created trillions of dollars in value. Where did that value ultimately flow? Not to protocols like TCP/IP, HTTP, SMTP. They are public goods, immensely valuable, but bring no return to investors at the protocol level.

The value ultimately flowed to enterprises like Amazon, Google, Meta, Apple. They built businesses on top of the protocols and achieved compound growth.

The crypto industry is repeating this history.

Stablecoins are gradually becoming the TCP/IP of money—highly practical, high adoption rate—but whether the protocols themselves can capture value commensurate with this is unknown. USDT is backed by a company with equity, not just a protocol—a crucial hint.

The true compounding entities are the enterprises that integrate stablecoin infrastructure into their operations, reduce payment friction, optimize working capital, cut foreign exchange costs. A CFO who saves $3 million annually by switching cross-border payments to stablecoin channels can reinvest that $3 million into sales, product development, or debt repayment, and that $3 million will continue to compound. The protocol that facilitated the transaction only earned a fee—no compounding.

The 'Fat Protocol' thesis argued that crypto protocols would capture more value than the application layer. But seven years on, public chains occupy about 90% of the total crypto market cap, yet their share of fees has plummeted from 60% to 12%; the application layer contributes about 73% of fees but has less than 10% of the valuation. Markets are always efficient; this data says it all.

The market still clings to the 'Fat Protocol' narrative, but the next chapter of crypto will be written by crypto-enabled stocks: enterprises that have users, generate cash flow, and whose management can use crypto technology to optimize the business and achieve higher compound growth rates will outperform tokens.

Portfolios of companies like Robinhood, Klarna, NuBank, Stripe, Revolut, Western Union, Visa, Blackrock will certainly outperform a basket of tokens.

These companies have a real price support: cash flow, assets, customers. Tokens do not. When token valuations are pumped to outrageous multiples based on future revenue, the severity of their decline is predictable.

Be long-term bullish on crypto technology, cautious in selecting tokens, and heavily invest in the stocks of enterprises that can leverage crypto infrastructure to amplify advantages and achieve growth through compounding.

The Frustrating Reality

All attempts to solve the token compounding problem inadvertently confirm my point.

DAOs that try to perform actual capital allocation—like MakerDAO buying treasuries, setting up subDAOs, appointing specialized teams—are slowly recreating corporate governance models. The more a protocol tries to compound, the more it must resemble a corporation.

Digital asset treasuries and tokenized stock wrapper tools also don't solve this. They just create a second claim on the same cash flow, competing with the underlying token. Such tools don't make the protocol better at compounding; they merely redistribute yield from token holders who don't hold the tool to those who do.

Token burns are not stock buybacks. Ethereum's burn mechanism is like a thermostat set to a fixed temperature, unchanging; Apple's stock buybacks are flexible decisions made by management based on market conditions. Smart capital allocation, the ability to adjust strategy according to the market, is the core of compounding. Rigid rules don't create compound interest; flexible decisions do.

And regulation? This is actually the most worth discussing part. The root cause why tokens cannot compound today is that protocols cannot operate as enterprises: they cannot incorporate, cannot retain earnings, cannot make legally binding promises to token holders. The GENIUS Act proves that the US Congress can integrate tokens into the financial system without stifling development. When we have a framework that permits protocols to operate using the capital allocation tools of enterprises, that will be the biggest catalyst in crypto history, far exceeding the impact of the Bitcoin spot ETF.

Until then, smart capital will continue flowing to stocks, and the compounding gap between tokens and stocks will widen every year.

This Is Not Bearish on Blockchain

I want to be clear: Blockchain is an economic system with limitless potential; it will undoubtedly become the underlying infrastructure for digital payments and agentic commerce. My company, Inversion, is developing a blockchain precisely because we deeply believe this.

The problem is not the technology itself, but the economic model of tokens. Current blockchain networks transfer value; they do not accumulate and reinvest it for compounding. But this will eventually change: regulation will improve, governance will mature, some protocol will find a way to retain and reinvest value like a good enterprise. When that day comes, tokens will be stocks in everything but name, and the compounding engine will officially start.

I am not bearish on that future, I just have my own estimate of its arrival time.

Someday, blockchain networks will achieve compound value growth. Until then, I will choose to buy enterprises that use crypto technology to achieve faster compound growth.

I might be wrong on timing. The crypto industry is an adaptive system, and that is one of its most precious traits. But I don't need to be perfectly precise; I just need to be right on the major direction: compounding assets will ultimately outperform other assets in the long run.

And this is the charm of compounding. As Munger said: 'The amazing thing is that people like us, by simply trying to not be stupid rather than trying to be very intelligent, have obtained such a huge long-term advantage.'

Crypto technology drastically reduces the cost of infrastructure, and wealth will ultimately flow to those who leverage this low-cost infrastructure to achieve compound growth.