Editor's Note: The current market is not "directionless" but has entered a "no-trade zone" created by the combined impact of AI-driven deflation and geopolitical shocks. The real movement of Bitcoin depends on when the money supply will be forced to expand again.

On one hand, AI is reshaping the labor structure, eroding the income and credit capacity of knowledge workers, transmitting deflationary shocks to the financial system; on the other hand, energy conflicts and geopolitical games are forcing countries to increase fiscal spending, hoard resources, and sustain operations by printing money. Rising interest rates coexist with expanding money supply, leading to sharp divergence in risk assets.

A deeper change lies in the monetary system itself. The restructuring around energy channels and settlement paths has begun to loosen the "dollar-asset" cycle, with gold and the Chinese yuan being passively drawn into trade settlements in peripheral regions. This structural shift has not yet become a mainstream consensus, but its marginal acceleration is already sufficient to influence market expectations.

In such an environment, Bitcoin is no longer an asset driven by a single logic. It faces pressure from deleveraging and liquidity contraction while also benefiting from expectations of monetary expansion and credit rebuilding. Therefore, its price performance appears contradictory but actually reflects the tug-of-war between two systems.

Rather than rushing to bet on a direction, author Arthur Hayes prefers to wait for a signal—when volatility truly spirals out of control and liquidity is forced to be released, the market will re-enter a "tradable" phase. Before that, this is more like a zone where action must be restrained.

This is the starting point of this article: in a world simultaneously experiencing deflation and money printing, the market may be going through a rare "no-trade zone."

Below is the original text:

Because Maelstrom has done almost no trading in the first quarter, some of our brokers occasionally ask me about my views on the market and if they can do anything for us. My usual reply is: "It's a no-trade zone."

Aside from slowly accumulating Hyperliquid, we basically did no trading throughout the entire quarter.

Two factors have combined to create a trading "dead zone," at least for long-only portfolios like ours.

First, the rapid proliferation of agentic AI (what I call "claws"). This technology will destroy the career prospects of ordinary knowledge workers within the "flexible employment" structure of developed Western economies (primarily within the "Pax Americana" system). What follows will be a deflationary financial collapse. I discussed this in detail in my previous article, "This Is Fine."

Second, after that article was published, U.S. President Donald J. Trump, the "Emperor/Head Performer," actively launched a war against Iran to turn it into the latest "Trashcanistan," with the support of his bellicose yet somewhat hapless "backing vocalist," Israeli Prime Minister Benjamin Netanyahu (the "Bedouin Butcher").

The war has been going on for nearly seven weeks, and the only truly important question now is: how will the flow of commodities and goods through the Strait of Hormuz be rearranged?

When discussing war or geopolitics, I always like to preface by saying: I'm just a ski bum, a house music-listening, two-step dancing crypto guy. I know nothing about war and have no insider information on what global leaders will or won't do.

But what I can do is: interpret mainstream propaganda narratives and use my AI tools to perform basic calculations with public data. I try to filter out the noise and focus only on the variables that truly affect my investment portfolio. Fortunately, I don't live in the Levant or the Middle East, so my life and liberty are not directly at risk.

In my relatively simple worldview, there are three scenarios worth considering—strictly speaking four, but the fourth, "nuclear Armageddon," offers no investable opportunities, so there's no need to elaborate.

I will introduce these scenarios one by one and analyze, from a macro perspective, how they might affect the price of Bitcoin.

I don't know the probability of each scenario. But what I really want to figure out is: is there a way to construct a portfolio that, in the best case, can outperform hydrocarbons and their first-order derivatives (like food and fuel prices) in absolute returns; and in the worst case, even if it doesn't outperform energy prices themselves, can at least perform better relative to all major asset classes.

Scenario 1: Back to Normal

In this scenario, the war ends quickly, and the pre-war status quo is largely restored. But a longer-term trend will not change: the process of replacing expensive knowledge workers who "manipulate digital symbols" with cheaper, more efficient AI agents is still accelerating.

The U.S. economy is most vulnerable in this process because about 70% of its GDP comes from consumer spending. Consumers finance their consumerism through bank credit, and these loans constitute assets on bank balance sheets. Once the debt-servicing capacity of ordinary knowledge workers disappears, these banks will be functionally insolvent and can only rely on massive central bank "money printing" to stay afloat.

Scenario 2: Tehran Toll Booth

In this scenario, the U.S. military is either unwilling or unable to prevent Iran from restricting shipping traffic through the Strait of Hormuz.

Iran makes good on its promise: it allows ships from "friendly nations" to pass but requires a $2 million "toll," payable in yuan, cryptocurrency, sanctioned U.S. dollars, or other diplomatic arrangements.

In the worst-case scenario for the financial hegemony of "Pax Americana," countries must find ways to obtain yuan. But since most countries run trade deficits with China, the only realistic path to obtain sufficient yuan is: sell dollar assets (like U.S. Treasuries or U.S. tech stocks) → buy physical gold → then exchange the gold for yuan via the gold markets in Shanghai or Hong Kong.

Among the world's top ten economies by GDP, only Brazil and Russia maintain trade surpluses with China, and they rank only ninth and tenth, respectively. Conversely, "Pax Americana" itself is the economy with the largest global trade deficit, and its operation depends on an equally massive capital account surplus to sustain it.

But when countries start selling dollar assets to obtain yuan, or to cover commodity shortfalls in the spot market at extremely high prices, this capital surplus must mathematically shrink. The highly financialized U.S. economy relies on foreign capital to finance government spending; once foreign capital decreases, this system becomes untenable.

Ultimately, whether bond prices fall (yields rise) or stock prices fall, the government will be forced to "print money" to fill the funding gap.

Scenario 2.5: The Star-Spangled Blockade

A dramatic twist occurred when, after U.S.-Iran negotiations failed to reach a permanent ceasefire agreement, on Sunday, April 12th, Donald J. Trump announced that the U.S. Navy would blockade all ships entering and exiting the strait.

This blockade could evolve into a kind of "pirate toll": ships might be forced to pay fees to both sides, effectively paying "tribute" simultaneously to Iran and the U.S., perhaps even having to "chant Allahu Akbar and Hallelujah" to express loyalty. Alternatively, numerous exemptions might be granted to different countries afterwards, turning the blockade into "Swiss cheese full of holes."

But the core logic remains unchanged: if holding dollars no longer guarantees your assets won't be devastated by "piratical behavior," why hold dollars?

Scenario 3: The Empire Strikes Back

In this scenario, the U.S. Air Force and Navy do their "job": through a punitive long-range strike operation, they destroy the Islamic Revolutionary Guard Corps (IRGC)'s ability to interfere with shipping in the Strait of Hormuz.

The strait reopens, all ships can pass safely without extra fees. With the reassertion of "imperial order," countries no longer need to use currencies other than the dollar in the short term, nor do they need to scramble to buy commodities at high prices in the spot market.

The problem is: ending Iran's control over the strait most likely means the utter destruction of the country itself. In Donald J. Trump's words, "send them back to the Stone Age."

Many Americans raised on the narrative that "Iran is the world's most evil country" will cheer this强硬 stance. But if Iran is destroyed in this manner, it will likely, with its "last breath," make good on its threat—dragging the entire Gulf region's energy and commodity production down into the abyss with it.

At that point, "the spice will not flow" (i.e., global supply chains break down), and global central banks will have no choice but to疯狂印钞疯狂 print money amidst soaring commodity prices to keep the financial system functioning.

If you are in certain "fragile countries," your local currency might experience hyperinflation against the dollar or ruble. The U.S. and Russia would remain the only major energy producers with the capacity to adjust supply, filling the void left by a burning Middle East.

What could follow is: famine, and widespread social unrest.

Therefore, even if your Bitcoin might be worth "an infinite amount" of some worthless fiat currency on paper, if you cannot leave high-risk areas in time, your own survival situation will still face serious threats.

Scenario Charts

Before analyzing Bitcoin's performance under different scenarios in detail, let's quickly go over some "chart material" to support the above with more直观的数据 visual data.

Back to Normal

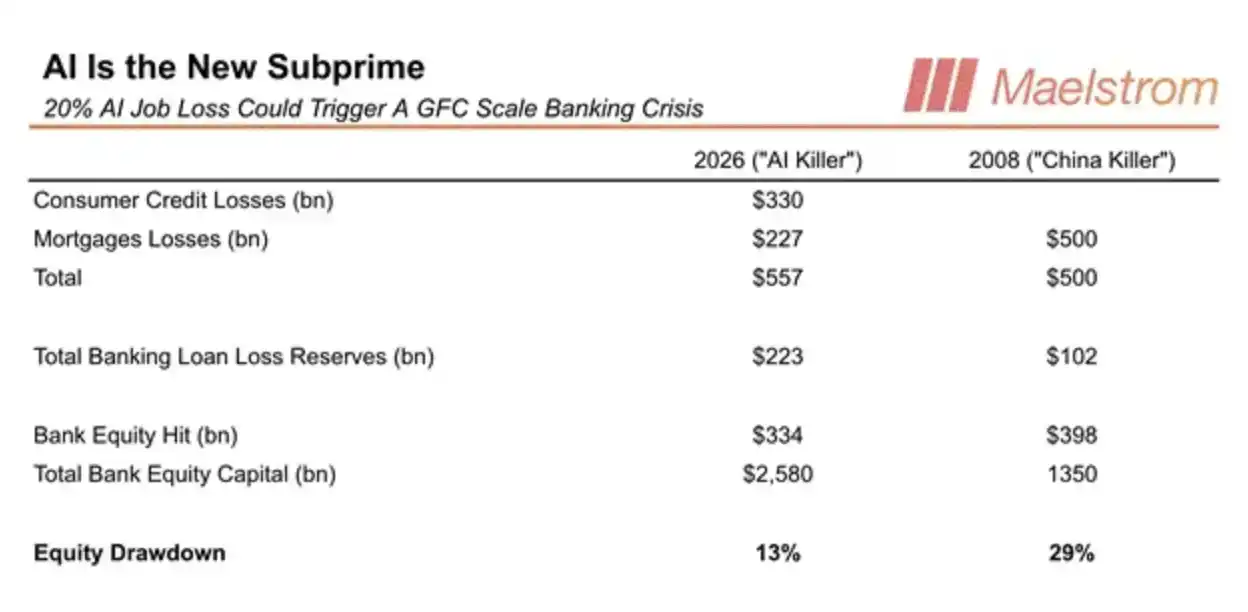

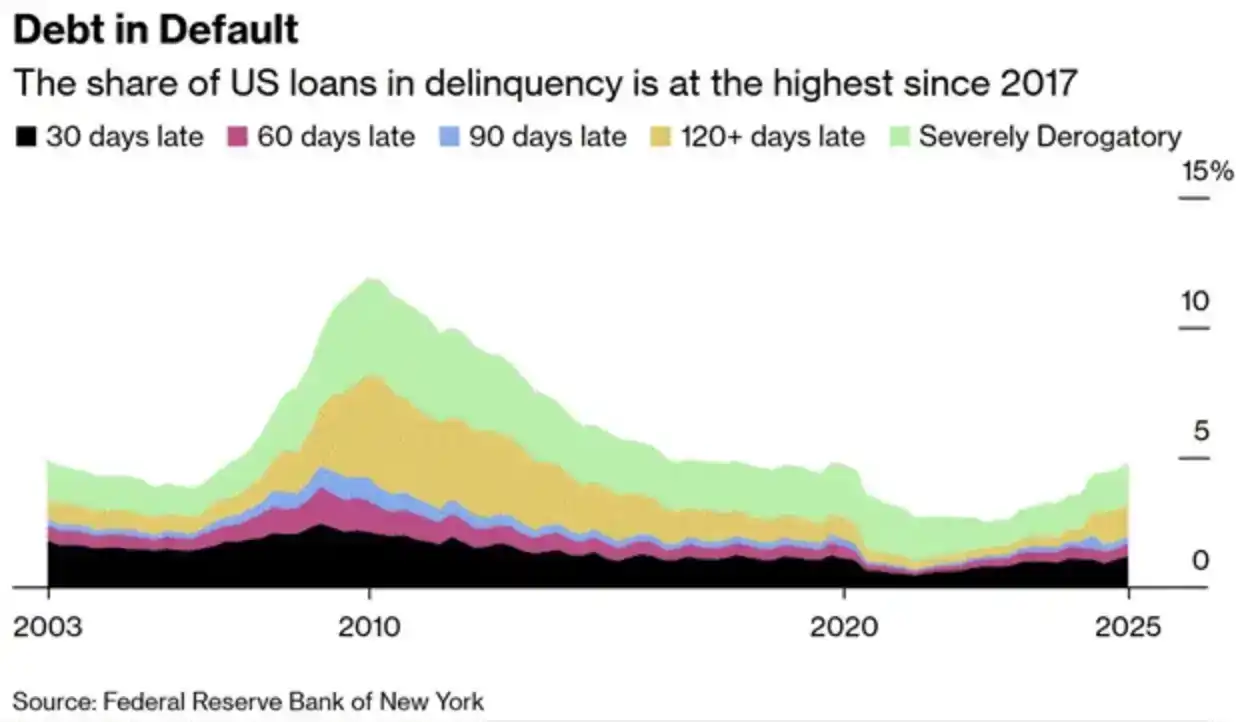

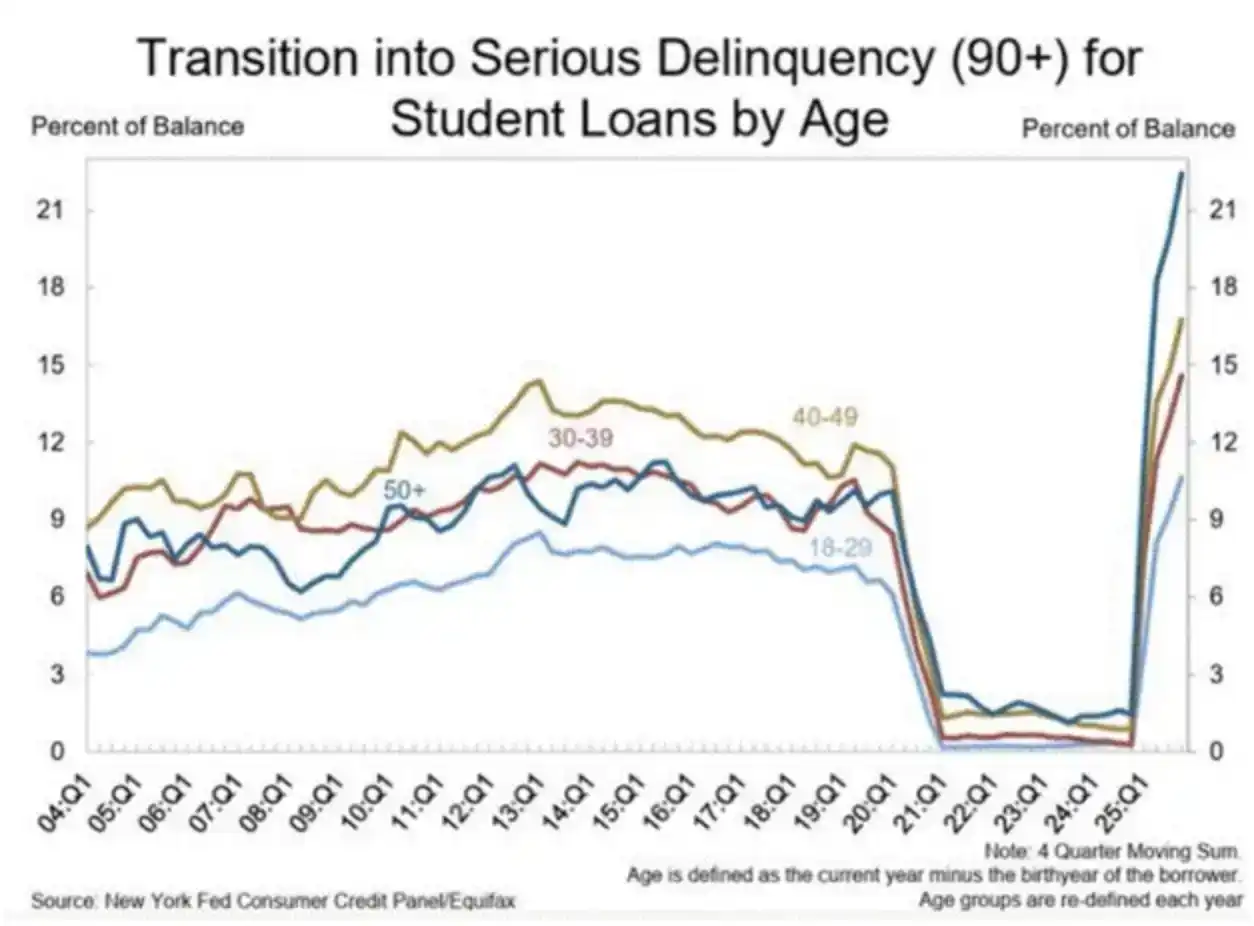

Since I have already discussed this scenario in some detail in my article "This Is Fine," I will directly reuse some of the charts and data tables provided there.

Overall, the deflationary collapse triggered by agentic AI is as severe as the 2008 Global Financial Crisis.

Currently, consumer credit default rates are already rising, and the real massive wave of知识工作者 layoffs hasn't even officially begun yet.

Tehran Toll Booth

In essence, if this scenario holds, it means the end of the "petrodollar system" and the rise of a new global reserve currency (or a basket of currencies).

Currently, the IRGC remains quite flexible regarding payment methods. But if its control over the Strait of Hormuz is truly consolidated, why would it continue to accept dollar payments, given the U.S.'s continued restrictions on its ability to use dollars?

Ultimately, I believe it will no longer accept dollar settlements. The yuan and gold will likely become the two core settlement assets in sovereign trade.

If a country must first exchange gold for yuan, then use yuan to pay the toll, just to get its goods shipped, what reason is there to continue holding dollars as reserves?

Considering most major economies run trade deficits with China, the only realistic path to obtain yuan is: sell dollar assets → buy gold → then exchange gold for yuan.

In such a system, what countries will need to reserve in the future is gold, not dollar assets like U.S. Treasuries or stocks.

To illustrate the expanding use of the yuan in trade settlement, I want to引用一些图表引用 some charts shared by Luke Gromen. These charts show the process of a "quasi yuan-gold standard system" quietly taking shape.

Step 1: Sell dollar assets (like U.S. Treasuries), switch to buying gold

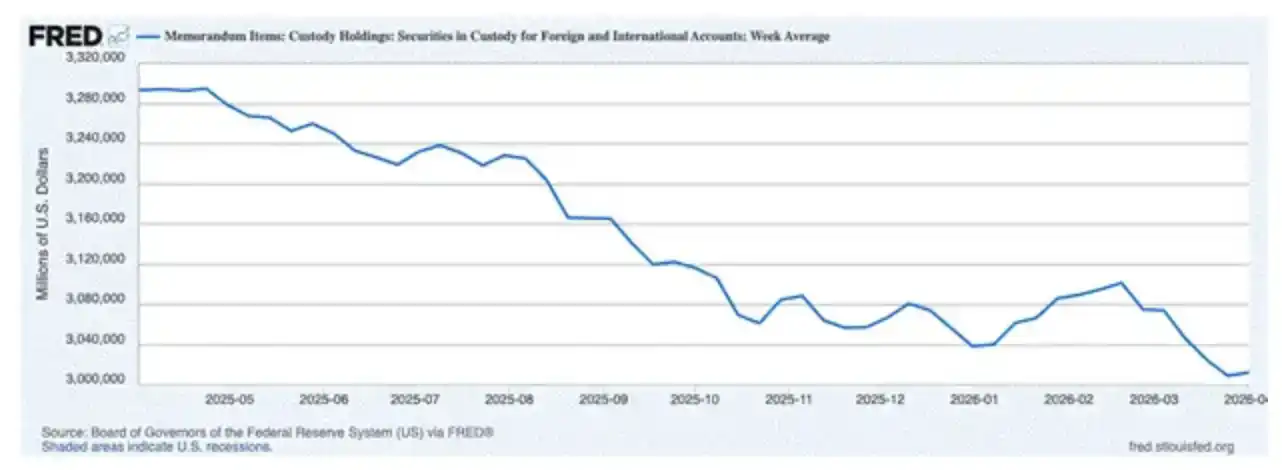

Since the war began, on a net basis, the value of securities held in custody at the Fed for foreign official and international accounts has decreased by $63 billion. I use this data as a "directional indicator" to gauge changes in foreign holdings of U.S. Treasuries and other dollar assets (like stocks).

So, where did the money from these dollar asset sales go?

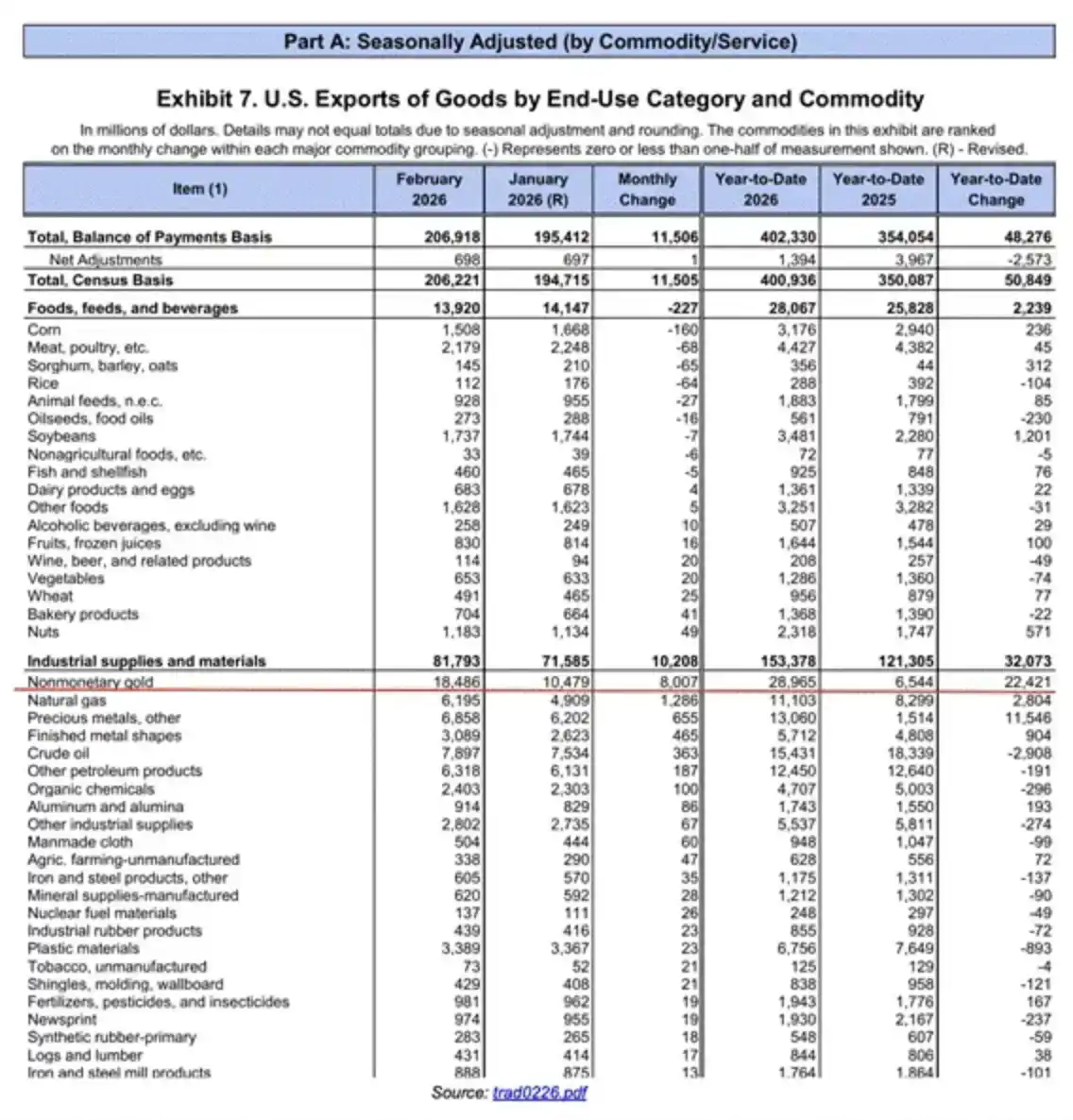

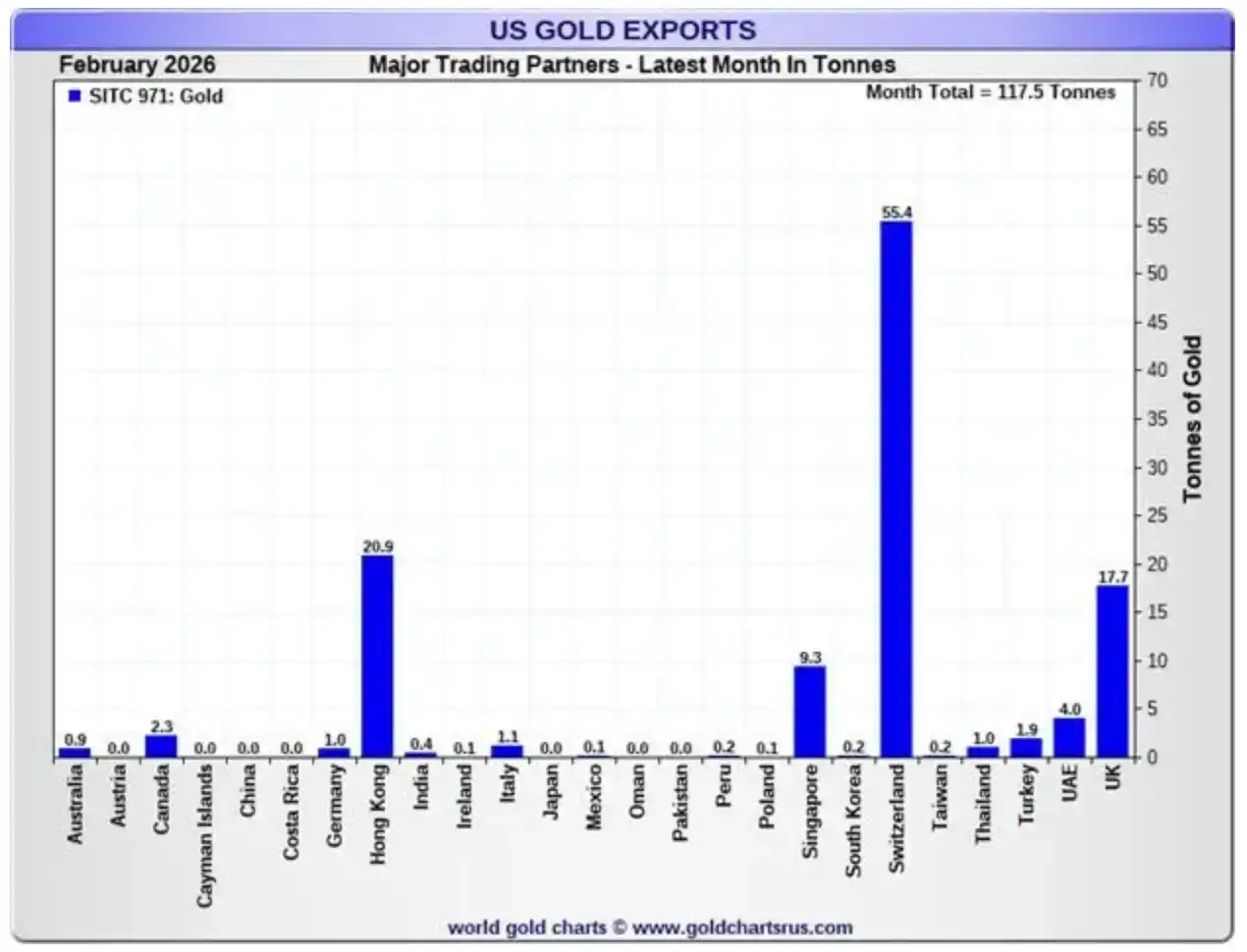

Nonmonetary gold has been the largest U.S. export commodity for four of the past five months, up 342% year-over-year.

In other words, this money did not stay in the U.S.; it was used to buy gold, which was then shipped out of the U.S. The narrative of "U.S. manufacturing回流" seems quite ironic in the face of reality—what's actually leaving the U.S. is a "barbarous relic" (gold). For supporters期待高薪制造业岗位期待 high-paying manufacturing jobs returning, this is another unmet expectation. Another presidential cycle passes, and the blue-collar class still hasn't truly benefited.

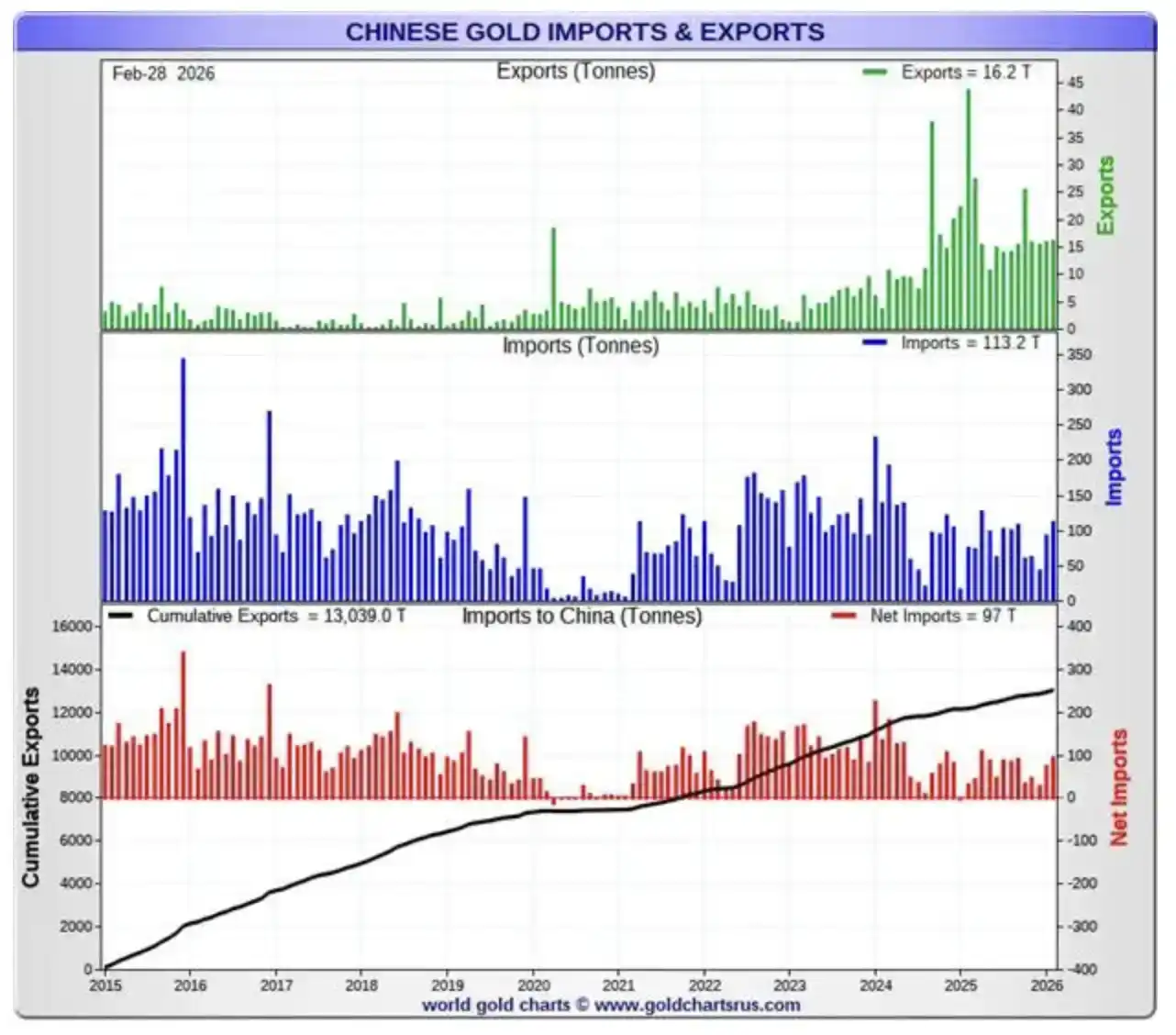

Step 2: Sell gold for yuan

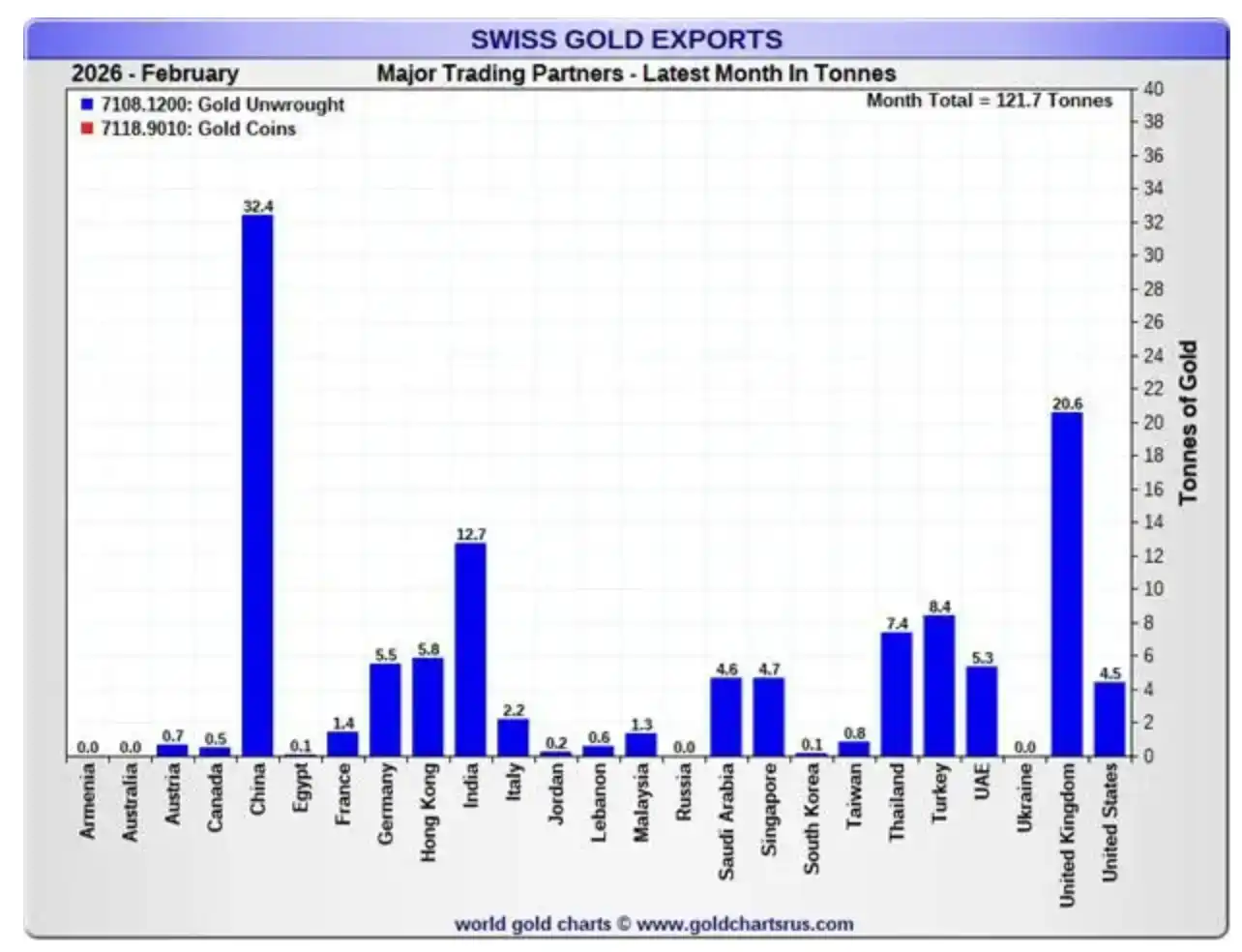

Swiss refineries receive gold from the U.S. and recast it into bars that meet Chinese delivery standards.

The key step here is: Switzerland is the core hub of global gold refining, capable of reprocessing bars of different specifications into high-purity standardized products that meet the demands of the Asian market (especially China) (Discovery Alert). In other words, gold流出美国 flowing out of the U.S. does not go directly to China; it goes through Switzerland, this "transshipment and standard conversion center," for形态重构 reshaping.

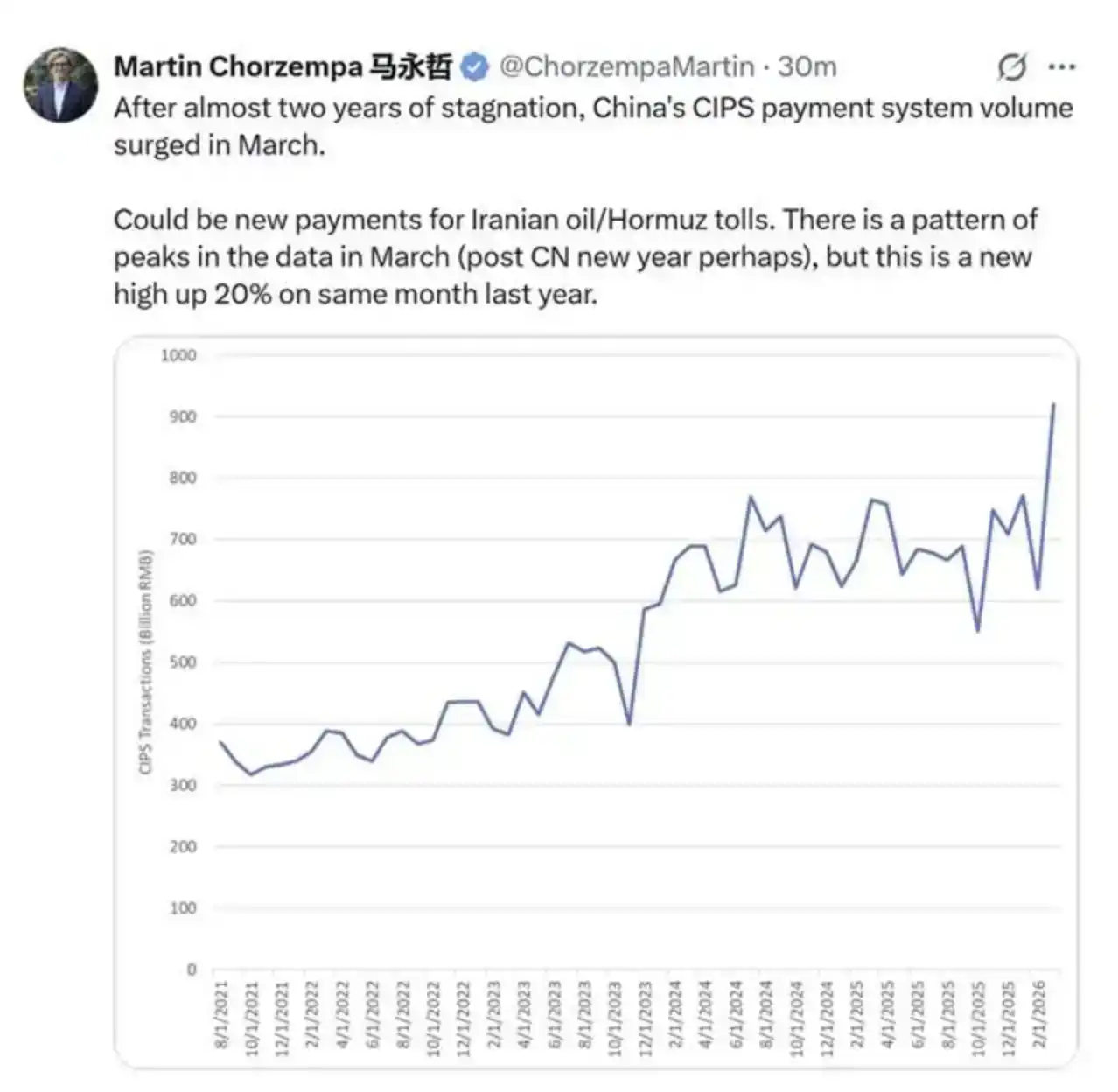

Step 3: Pay the "Tehran toll"

"Buffalo Bill" Besant was dead serious when he said that: "Either stick the dollar on yourself, or face another round of sanctions."

Due to sanctions imposed by the U.S. nearly fifteen years ago, Iran cannot use the SWIFT payment messaging system. To get yuan to the IRGC, one must rely on China's currency settlement system, the China International Payment System (CIPS). As you can see, transaction volumes on this system have noticeably increased since the war broke out.

This series of charts shows a capital flow chain: dollar assets are sold, switched to gold, and ultimately the gold is exchanged for yuan to make payments to Tehran or other suppliers. The key is not that the dollar is currently still the dominant currency in trade, but that—markets are forward-looking. More important than the fact that the current scale of yuan usage is still lower than the dollar's is its accelerating growth in global trade. For investors, avoiding dollar assets before the market consensus forms is a way to protect portfolios.

Historically, the pound sterling was nominally the global reserve currency until the 1944 Bretton Woods Agreement, but in reality, as the U.S. economy became the world's most productive economy in the early 20th century, the dollar had already replaced the pound as the de facto reserve currency.

By 2026, the U.S. runs trade deficits with the world's most productive economies (China, Japan, Korea, Germany, Taiwan, etc.), and most countries also run trade deficits with China.

Let me emphasize this logic again: if you must pay those "Stone Age" Middle Eastern forces in yuan to get your goods, what's the point of storing your assets in dollars?

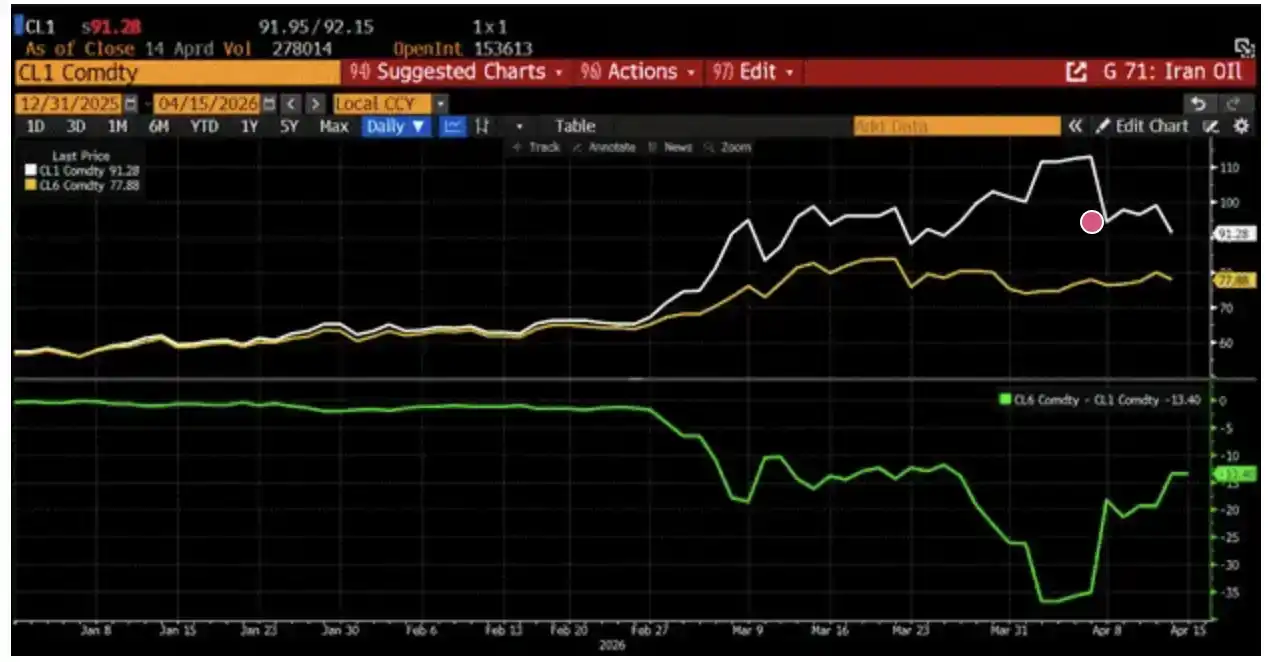

To judge whether the strait is "clear" or "blocked," look at the chart above, or make a similar chart yourself using any charting tool.

The top chart shows the WTI crude oil futures prices for May 2026 (CL1, white line) versus October 2026 (CL6, gold line). I chose WTI because this benchmark is closer to U.S. consumer gasoline prices. For Donald J. Trump, he only has motivation to substantially cool the situation if oil prices put明显压力明显 pressure on voters before the November midterm elections.

The bottom chart shows the spread between these two contracts (back month minus front month); the curve is currently in "backwardation." Since the back month price is rising less than the front month, the market is essentially betting that oil flow through the strait will increase significantly.

If this judgment holds, then as the front-month price falls, the spread will widen. But if the opposite happens—the back-month price rises and the spread narrows—it means the global economy is facing a severe shock.

So, rather than focusing on the war of words between Trump and the IRGC, keep an eye on this chart.

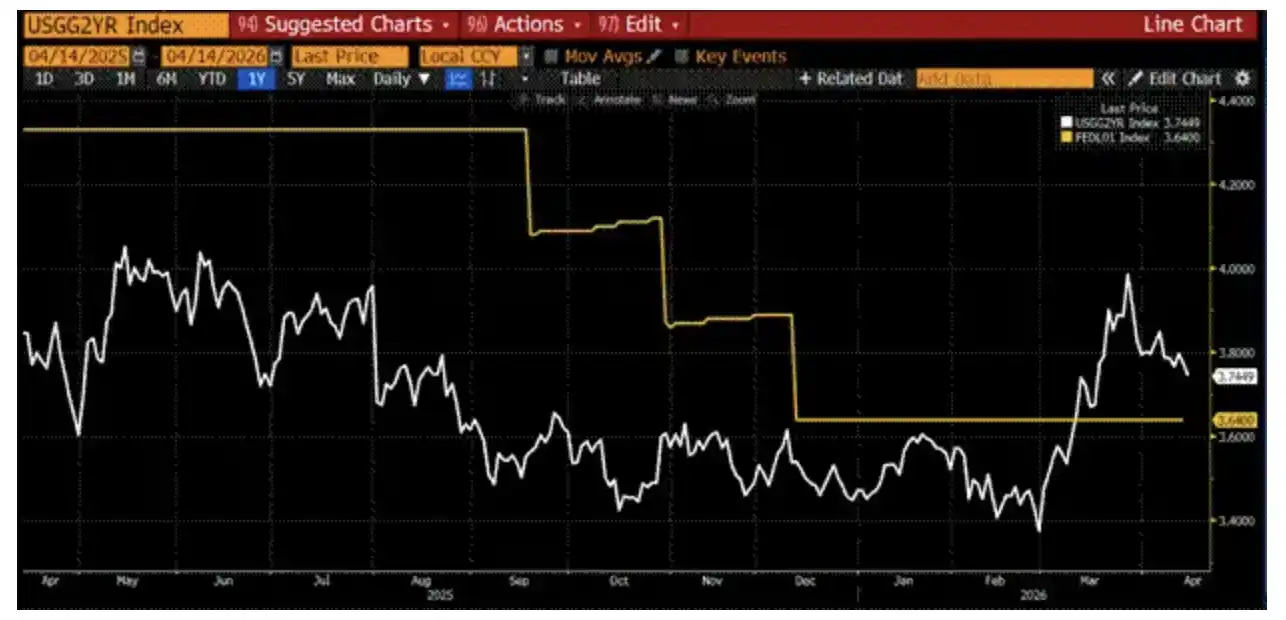

Quantity versus Price of Money

The 2-year U.S. Treasury yield (white line) spiked rapidly after the war began, far above the effective federal funds rate (yellow line). This indicated the market believed the Fed would hike rates to counter rising energy inflation.

Now, it's time to choose sides: when pricing Bitcoin, do you think the "quantity of money" or the "price of money" is more important? I believe Bitcoin's price is determined by the quantity of money, not its price. Bitcoin has no cash flow, so the discount rate derived from central bank policy rates does not apply to the valuation of this "internet magic money." But since Bitcoin's supply is fixed, its value denominated in fiat currency depends on the total amount of fiat.

The reason we need to form a judgment on this is that we might enter a new macro state: major central banks, including the Fed, might hike interest rates while simultaneously printing money (whether directly or through indirect credit expansion in the banking system). As war pushes up food and energy prices, governments that can往往往往 often subsidize key input costs in the economy, otherwise social unrest or even famine could erupt. But to prevent inflation from spreading to all goods and services, central banks must suppress demand through rate hikes, especially压制那些对信贷敏感的经济活动压制 credit-sensitive economic activities. Any entity that relies on borrowing to spend will reduce支出支出 spending when credit costs rise.

If central banks only did this, then my judgment on Bitcoin would be simple: in an environment where people cut spending on everything except food and energy, Bitcoin's price would fall. But the reality is that both allies and adversaries of "Pax Americana" must increase defense spending and hoard key commodities. Do you want your country to be like Australia, which is almost 100% dependent on China for refined energy imports? When the war started, China suspended exports, and Australia's库存库存 inventory lasted less than a month. They had to ask Singapore for help and buy jet fuel at extremely high prices, otherwise the country would grind to a halt.

To avoid becoming a "Trashcanistan," countries need to manufacture weapons (especially nuclear weapons) and hoard commodities, which will lead to a sharp rise in government borrowing. If domestic private investors cannot or will not buy these "bad" government bonds, then the central bank or the banking system will print money to buy them, thereby expanding the fiat money supply.

This combination of "rising interest rates (higher price of money) + expanding money supply (higher quantity of money)" will cause divergence among risk assets: assets priced based on discounted cash flows will fall, while assets with fixed or near-fixed supply (like Bitcoin and gold) will rise, because the banking system needs to expand credit to support government war and resource hoarding spending.

Before continuing to read my judgment on Bitcoin's trend under different scenarios, please keep this in mind: you must judge whether the "quantity of money" or the "price of money" is more important, otherwise you will not understand the seemingly contradictory price performance among different risk assets.

Back to Normal

After the situation returns to the pre-war state, Bitcoin might see a反弹反弹 bounce. But the deflationary shock triggered by AI agents continues to build. Before the Fed provides sufficient liquidity to the banking system to fill the balance sheet gaps caused by consumer credit defaults, Bitcoin is unlikely to see substantial上涨上涨 gains. This doesn't mean it can't briefly spike to $80,000-$90,000, but for me, without a clear signal of liquidity release from the Fed, putting new fiat into the market is too risky. Since I am already纯多头纯 long-only, seeing net worth rise would feel good, but the current risk-reward ratio is not enough for me to push my position to the extreme.

I cannot judge how long it will take for the banking system to truly collapse. But almost every week, I see news like:某些公司某些 companies laying off large numbers of knowledge workers due to AI efficiency gains, and consumer credit default rates continuing to rise.

Here's an example. I recently spoke with an entrepreneur running a crypto gaming company, an old hand in the industry. We talked about AI's impact on business. He is a computer engineer by background and during the 2025 Christmas period tried developing projects with the latest Claude model. He was quickly stunned by its efficiency—it could produce shippable code in极短时间极短 time. Months later, he gathered his team for an offline discussion and demanded they build an AI programming workflow running 24/7, even automating code reviews. The result was tested code ready to use every morning. One employee, assisted by AI, completed a development plan originally scheduled for six months in four days.

After this, he decided to immediately adjust the company's processes. About 50% of the company's employees will be laid off in the coming weeks.

In the age of AI agents, average engineers will become redundant, while top engineers' productivity will increase 10 to 100-fold. As models strengthen their capabilities in various niches, a large number of mid-level knowledge workers will face the risk of unemployment.

The problem is, even with unemployment insurance, the maximum annualized subsidy in U.S. states is about $28,000, while according to the BLS and St. Louis Fed, the median annual salary for knowledge workers is about $85,000 to $90,000. The gap is huge, and the result can only be masses of people starting to default on bank consumer credit.

This is a fatal blow to the current "fictional" fiat fractional reserve banking system.

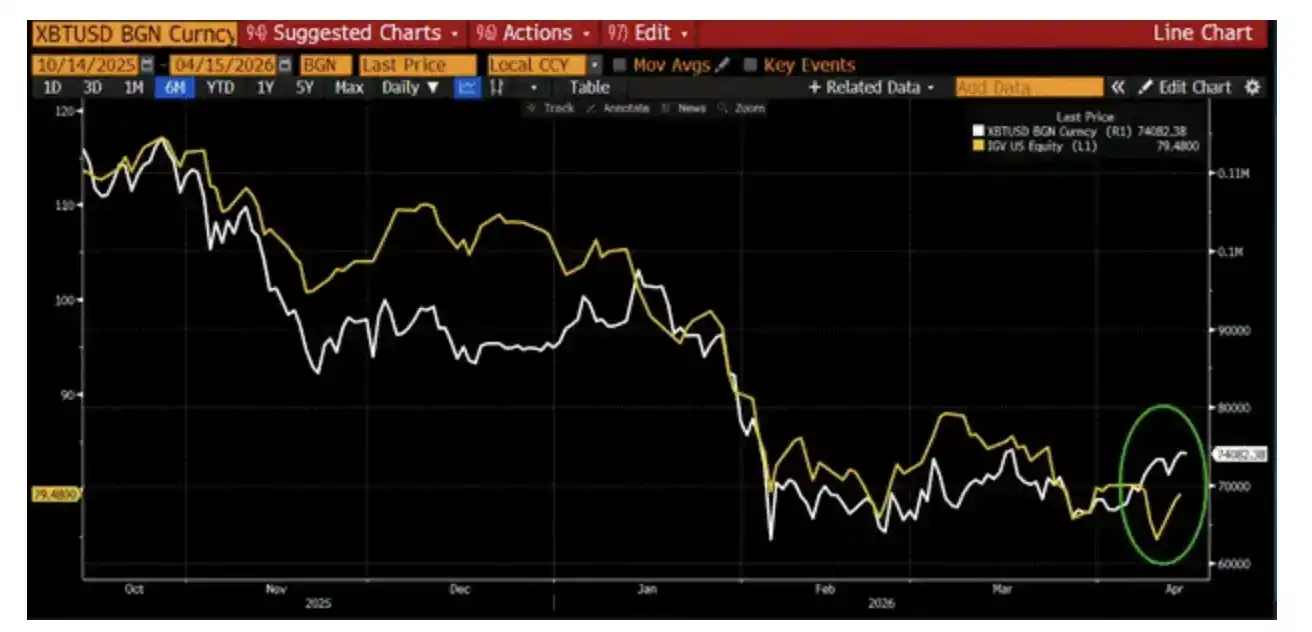

In summary, after a ceasefire, U.S. SaaS software stocks resumed their unilateral decline, while Bitcoin stabilized and bounced. This temporary decoupling of correlation is encouraging, but in my view, it is too early to conclude that Bitcoin has already "seen through" the knowledge worker deflation caused by AI and is poised for a massive rally.

Tehran Toll Booth

As countries sell dollar assets to obtain yuan and pay the "toll," U.S. bond and stock prices will come under pressure and fall. This process might be gradual, as payment options other than yuan still exist. But given the high leverage embedded in the entire system, even a small shock can trigger a chain reaction—selling begets more selling, volatility rises, market liquidity freezes. At that point, monetary authorities will have to step in and "print money" to stabilize the situation.

A key indicator to watch is the MOVE Index (U.S. bond market volatility index). Once this index rises above 130, it often signals that some form of monetary easing is imminent.

As volatility rises and U.S. large-cap tech stocks fall, Bitcoin will also struggle to rally有力有力 strongly. When investors de-risk due to increased market volatility and falling asset prices, they often sell Bitcoin to meet margin requirements. Bitcoin will only truly rise when the situation deteriorates to a point where a bailout is widely expected.

Wait until Besant, or whoever is Fed Chair at the time, presses the "money printer" (Brrrr button). Trying to position提前提前 beforehand doesn't offer a favorable risk-reward ratio. I hope Bitcoin can hold $60,000 during a systemic financial shock in traditional markets. If it tests and holds this level for a second time, I would be inclined to gradually increase risk exposure.

The Star-Spangled Blockade & The Empire Strikes Back

If back-month crude oil futures prices rise rapidly and catch up to the spot or front-month price, the global economy will be shocked. At some point, demand contraction will hit the U.S. bond and stock markets. Similar to the previous scenario, the initial reaction is still a decline in Bitcoin. And when the highly leveraged Western financial system begins to collapse, the money printer will start again.

If the最终局势最终 situation evolves into: lifting the blockade through punitive bombing of Iran, while Iran retaliates by destroying the entire Persian Gulf's energy production capacity, this could even lead to the collapse of the Iranian state. In this case, the Bitcoin rally driven by "money printing" might be short-lived, as it would significantly increase the risk of World War III.

Portfolio Construction

As an unleveraged, long-only investor, Maelstrom can rely on time and compound interest to work naturally. Bitcoin's slight outperformance relative to IGV (U.S. software SaaS ETF) over the past few days is a positive signal, making me start to re-examine my previously bearish judgment based on "AI-induced knowledge worker deflation."

At this stage, the only assets I am willing to increase exposure to are gold and $HYPE (Hyperliquid's governance token). HIP-4 will launch in a few weeks, and I expect it to capture a considerable market share from Polymarket and Kalshi in the prediction market赛道赛道 space.

Other than that, the only thing I can do every day is pray that Satoshi can "influence" the minds of global political elites to choose acid instead of dropping bombs.