Table of Contents:

1.Cosmos: The Current Version of ICS Will Struggle in 2023

2.Cosmos: Mesh Security Will Lead To Validator Centralization

3.Celestia: Data Availability Sampling Will Revolutionize the Development of Blockchains

4.Key infrastructure Will Be Built to Address the Bottleneck of Liquidity Fragmentation in 2023

5.The Most Important Problem to Solve in 2023: Exclusive Orderflow

Cosmos: The Current Version of ICS Will Struggle in 2023

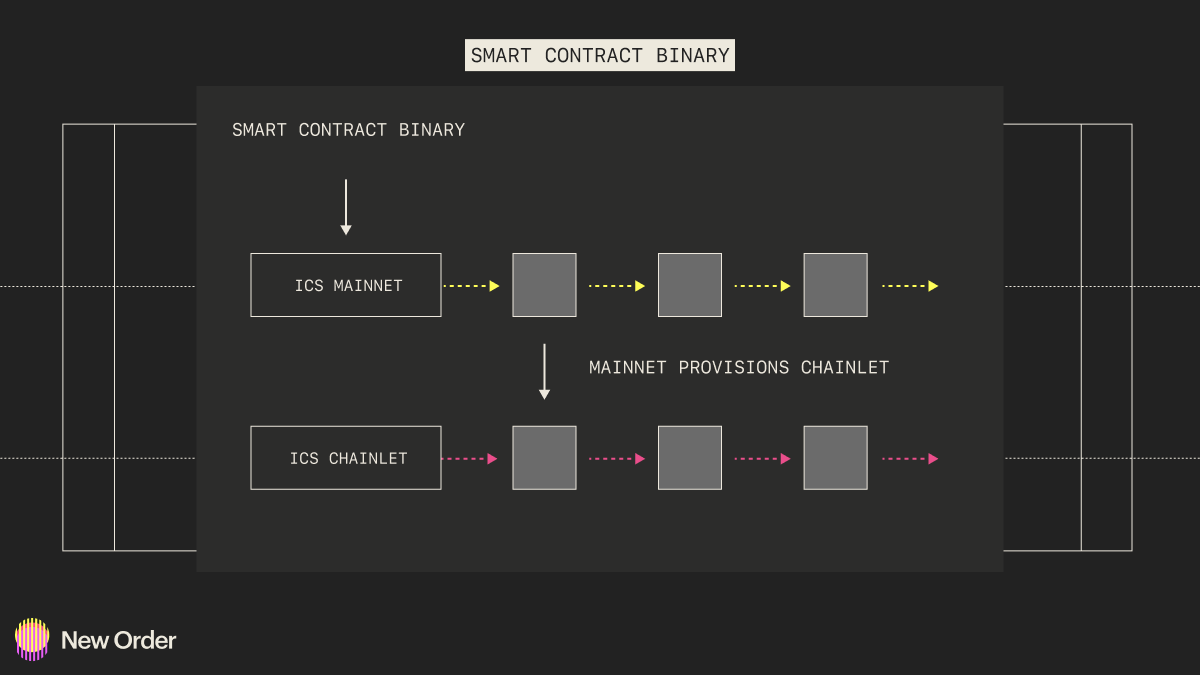

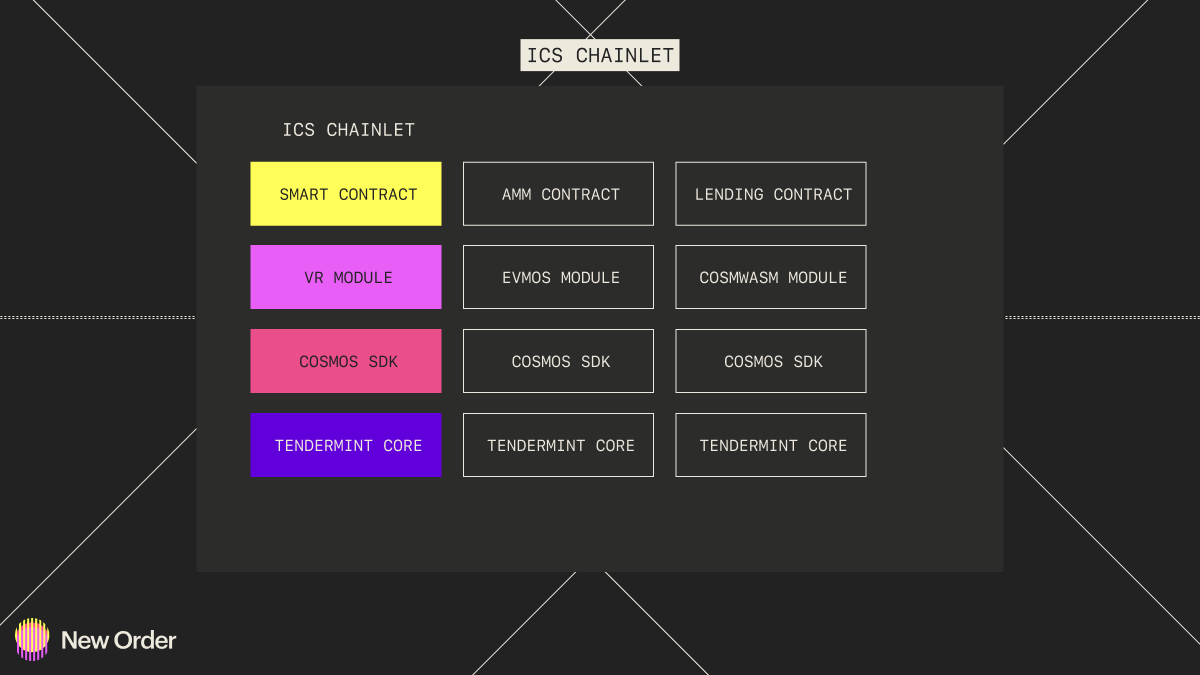

Interchain Security's (ICS) popularity and implementations won't see a market fit in its current state, but will do so through more customized and marketable solutions like Saga. This is because simply getting a validator set isn't enough for smaller teams like indie game studios and projects that can’t afford a Golang developer with CosmosSDK experience (something that is in big demand these days, as the popularity of app-chains grow). With a customizable app-chain solution that provides all the building blocks such as agnostic VM choice, validator sets, and easy setup, ICS is going to see real adoption, something that it deserves. It's great tech, after all.

This thesis is further solidified by the fact that the Cosmos Hub's community recently voted no to the Atom 2.0 Vision. Interchain Security is definitely going to see some use within the Hub, and might get a few chains on boarded - if they can get it through governance. The Cosmos Hub has quite a few hardliners that have been pushing it to stay as free of state and bloat as possible. This might make it difficult to pass certain proposals. We saw this issue with large with the large Atom 2.0 proposal failing to pass. This is another reason why ICS might not be able to fully flourish on the Hub itself. Regardless, the fact that teams still have to do most of the initial work (apart from the validator setup) means that it is out of reach for the vast majority of applications and protocols. Most of these teams don’t have the funds to pay over $300K a year for a blockchain engineer with Golang (CosmosSDK) experience. This means that they’re highly likely to pick a solution which provides a customisable and out of the box solution, which requires no actual developer work on the blockchain side. This is why solutions such as the one-click developer deployment of app-chains are going to be extremely important if we want to see the Interchain ecosystem grow beyond what it is now.

Cosmos: Mesh Security Will Lead To Validator Centralization

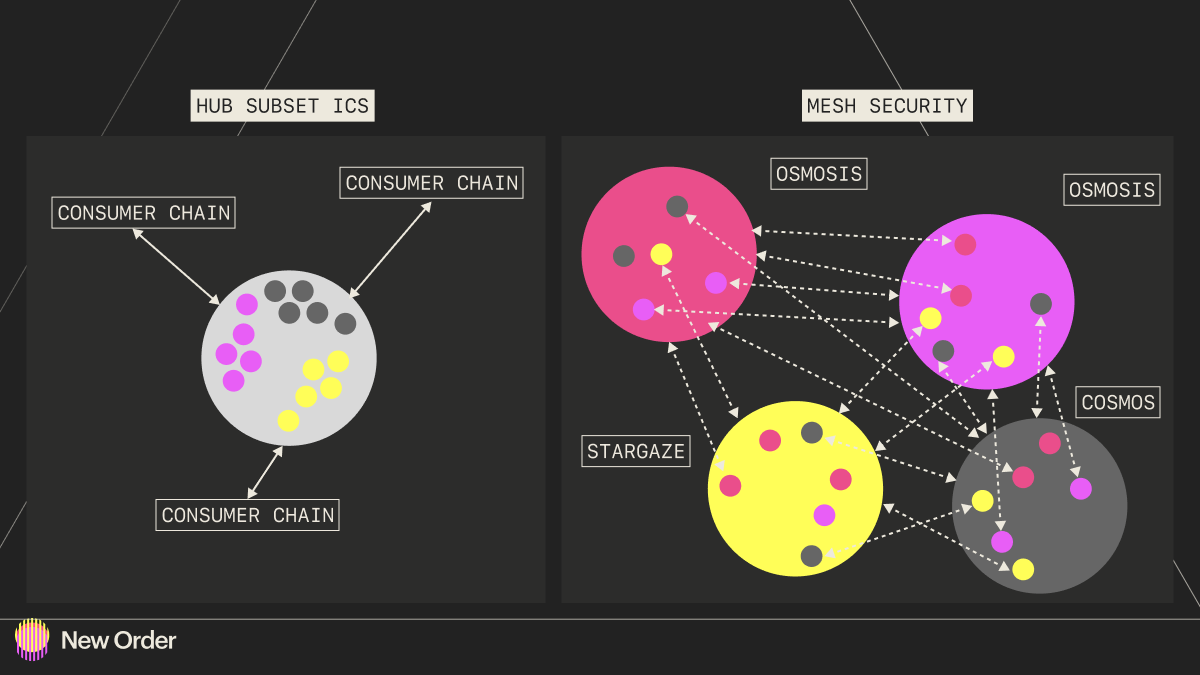

Mesh Security is going to increase power within certain validator cliques, leading to centralization and collusion. While the NATO example given by Sunny in his speech around Mesh Security makes sense, it doesn't take into account that the “nation states” of the Interchain community aren’t particularly nationalistic and tend to support chains across the Cosmos tech stack. This means that while some of these chains are incredibly popular, some are less so, and if mesh security were to become the go-to security measure, it will severely centralize the power into a certain few validators (some of which already have incredible amounts of power).

We should rather look at methods for furthering decentralization among validators, such that it is not the few that have power, but rather the many. Mesh Security is an answer to ICS in theory. It aims to solve some of the issues that ICS might bring to the table. Let’s quickly explain what mesh security is, what it does well, and where it might fall short. The primary issue with the way ICS is supposed to work with the Cosmos Hub is the fact that by being opt-in by nature, it makes it so subsets of validators validate various chains. In this case, you’re not deriving security from Cosmos, but rather from a subset of validators, which might be less secure and fall prey to malicious actions in case of increasing centralization. Regardless, if it is not the entirety of the stake that protects the consumer chain, it falls short.

Going back to our previous thesis, it clearly shows that an ICS Hub should be built for the specific purpose of ICS, not for a Hub to make a pivot that the majority don’t agree with — such as with the Cosmos Hub. Now for Mesh Security, you allow delegators on provider chains (such as the Hub) to delegate to validators in the consumer chain's own validator set, which offsets some of the subset problems. However, what you get now is increasingly fragmented security spread across several chains, of which some staking providers (validators) might become increasingly entangled and grow their power base.

If this is to be implemented it needs clear UX that shows exactly what is being validated by who, how much stake they hold, and much more. Mesh Security has the chance to fragment and distribute more than need be. It is also entangling, which could have catastrophic consequences if done incorrectly. However, at this point the correlation between validators is extremely large across chains, as seen below with the Juno/Osmosis example. So from that perspective, mesh security seems like a natural extension of what is already happening. The question is, should we really be glorifying that?

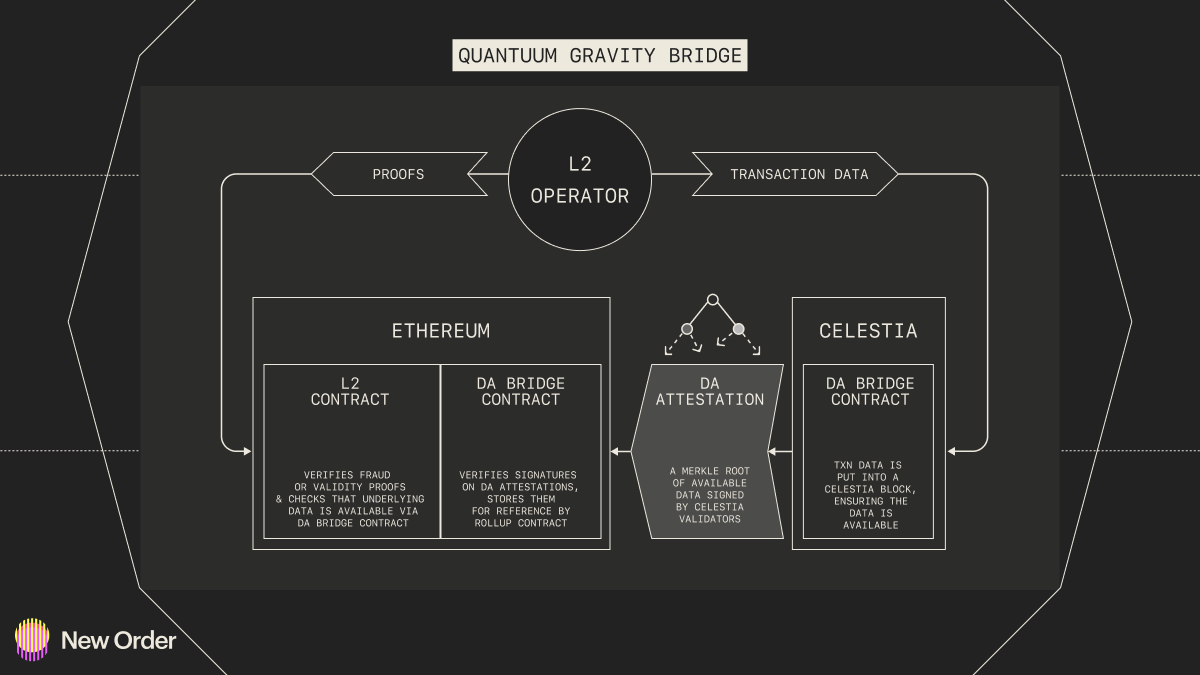

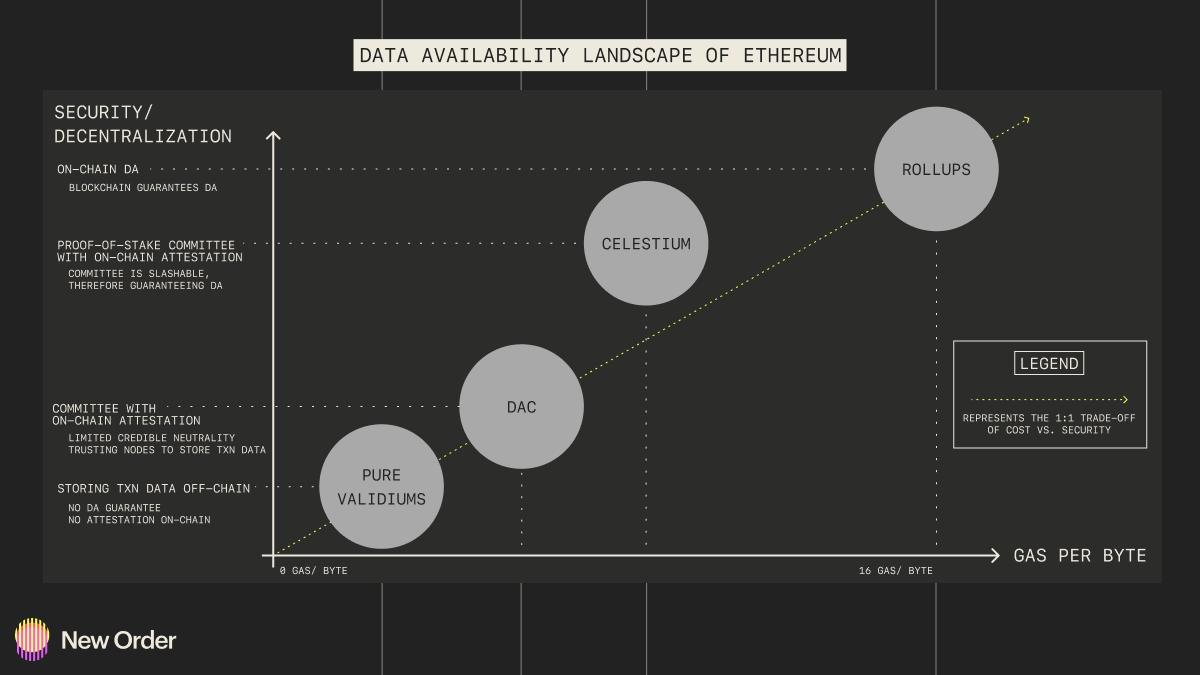

Celestia: Data Availability Sampling Will Revolutionize the Development of Blockchains

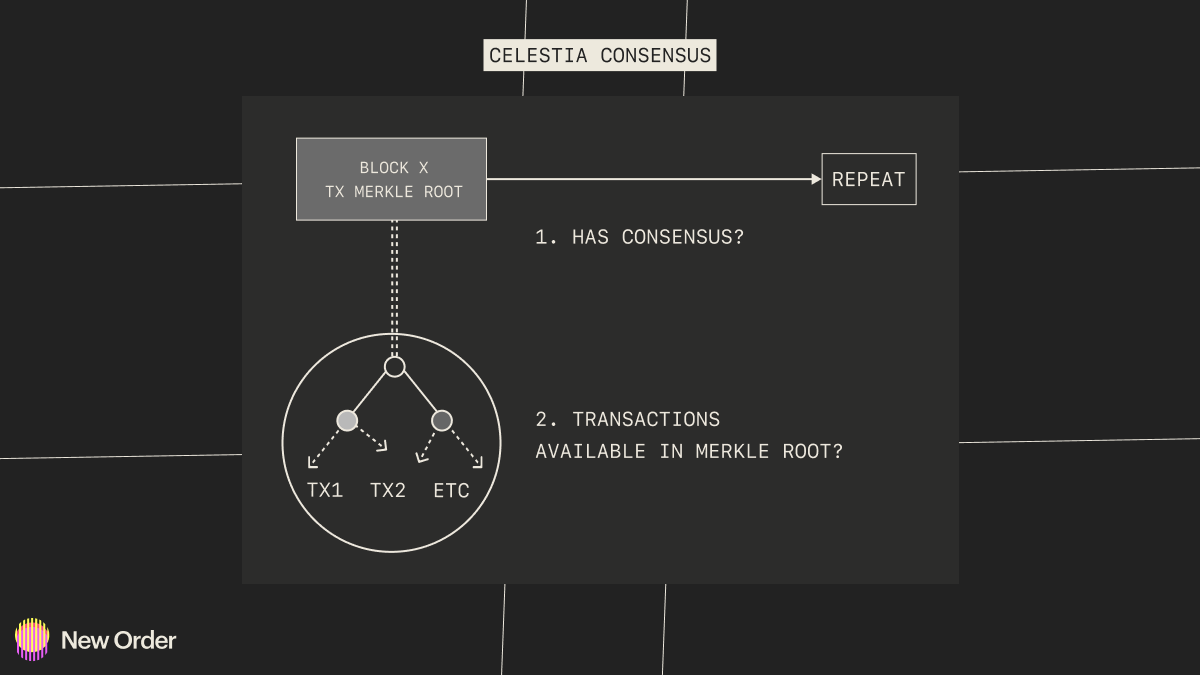

Data Availability Sampling (DAS) is set to become the biggest innovation for building out multiple aspects of blockchains. DAS enables you to increase decentralization (node count) without losing throughput. For example, block verification in Celestia works quite differently from other current blockchains since blocks can be verified in sub-linear time. This means that throughput increases with a sub-linear growth in cost, compared to linear growth in cost. This is possible since Celestia’s light clients do not verify transactions, they only check that each block has consensus and that the block data is available to the network.

By optimizing a part of the network (with Data Availability and Consensus, in Celestia’s case) or just one of them, we can allow other networks and layers to specialize in what they deem most important. This means that we overall get a much more specialized and focused blockchain ecosystem with various layers and nodes that are great at their specific task. This means that throughput, data availability, and much more won’t be much of a problem for much longer. By focusing on what makes layers other than execution best, we can allow for execution to become more efficient. As others have said before us, execution is now the bottleneck - so how will you increase it? There are various layer 2 teams working on exactly that, and it’s going to be very interesting to see what happens in the next year or two for execution layers in particular.

Now for some bold predictions for Celestia - We expect a thriving ecosystem on top of Celestia with Total Value Locked that would put the ecosystem in the top 10 of ecosystem TVL. We also expect to see some Celestiums (Ethereum for everything but DA, DA on Celestia rollups) see significant traction pre-danksharding for Ethereum.

After all, Ethereum must realize a modular future for decentralization to be upheld while simultaneously increasing throughput.

Something else we would like to note is that we also expect to see DAS and Erasure Encoding getting usage beyond just data availability sampling for DA in Ethereum and Celestia. For example, another use case is clearly described in an excellent paper by Joachim Neu from Stanford on the ability to use DAS for Information Dispersal with Provable Retrievability for Rollups. This is a storage and communication efficient protocol using linear erasure-correcting codes and homomorphic vector commitments. It also requires no modification to on-chain contracts and can even provide some privacy assumptions against storage nodes. This is a fascinating application that only scratches the surface of what these technologies are capable of.

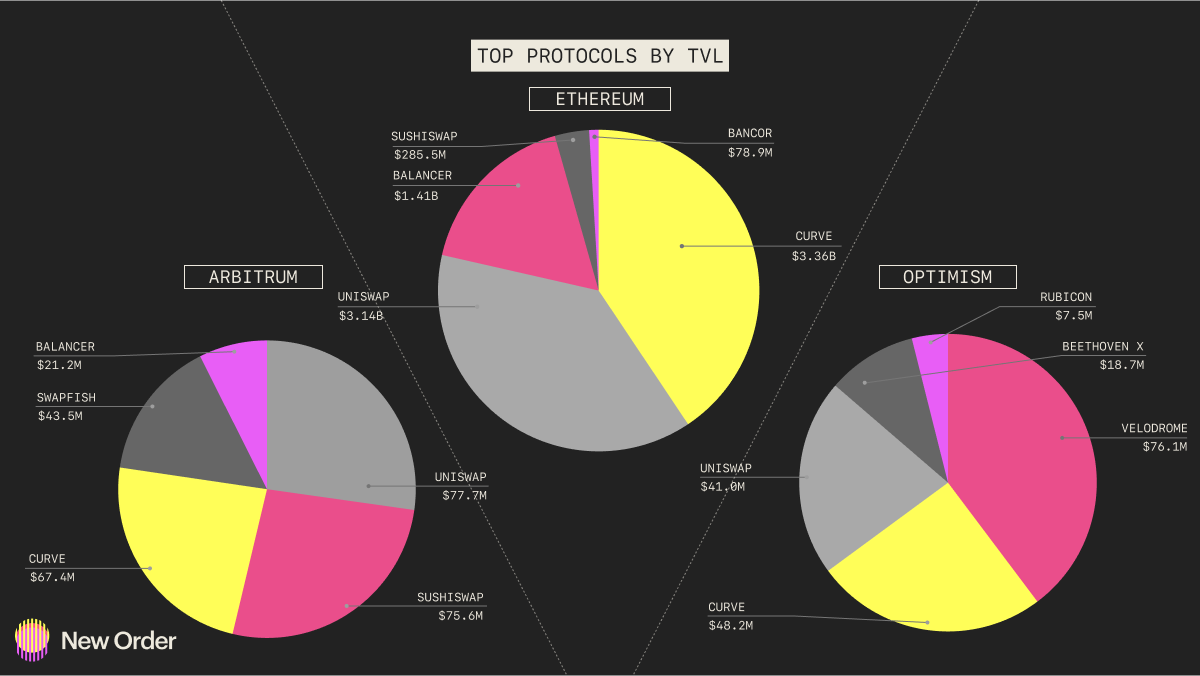

Key infrastructure Will Be Built to Address the Bottleneck of Liquidity Fragmentation in 2023

Fragmentation of liquidity - both interchain and cross chain - creates apparent price discrepancies that result in unfavorable environments for both liquidity providers and traders. Liquidity providers struggle to correctly predict favorable trading venues with the highest volumes and lowest fees to maximize capital utilization and revenue. While traders suffer from high slippage resulting in materially worse trade pricing and user experience.

Introduction of concentrated liquidity provision and stableswaps are driving the market towards specialization, though a large portion of emerging token markets are unable to find a consistent edge dispersing among various xyk bonding curves. Such token markets rely on trading aggregators to efficiently route their trading order to the best execution environment while navigating the fragmented liquidity on trading venues.

To analyze pathways to consolidation, we should break down the grand issue of fragmentation into layers. Such layers include the following: Application, Middleware, and Infrastructure.

Applications are decentralized exchanges with accompanying bonding curves that serve as the bottom most level in the trading hierarchy. Examples of such protocols include Curve, Uniswap, SusiSwap etc.

Middleware layers serve as chain-specific DEX aggregators and Liquidity optimizers. The most prominent examples are 1inch as an aggregator, and concentrated/ single sided liquidity provisioning as optimizers. This layer introduces chain specific efficiency optimization, but does not solve fragmentation of capital within a chain and cross-chain.

On the other hand, trading infrastructure includes liquidity direction engines and communication protocols that allow for efficient cross chain asset and message transfers. Examples for this top most layer include Layer 0, Polymer, Socket etc. The infrastructure layer tackles fragmentation directly by providing a toolkit for cross chain liquidity direction. This allows liquidity providers to allocate capital based on prediction models around capital utilization, slippage, and fees incurred. Such infrastructure allows for liquidity to be allocated to environments that are experiencing the largest trading volume, hence maximizing capital utilization for liquidity providers and minimizing price impact for traders.

Consolidation of liquidity is largely believed to be bound by bonding curve innovation, where liquidity providers are seeking the highest capital utilization with the lowest exposure to impermanent loss. We argue that the primary bottleneck is liquidity infrastructure, trumping application and middleware layer constraints. Solutions for mending fragmented liquidity, enabled by advanced infrastructure, will see unprecedented growth in 2023. Two overarching approaches will be standard in achieving liquidity unification.

Asynchronous cross-chain communication: enhanced cross-chain messaging solutions that afford native composability for dissimilar execution environments, e.g., chain-agnostic IBC

Shared liquidity layers: liquidity hubs that allocate liquidity to various marketplaces (satellites) on different chains and applications based on predictive volume demand (ex. SLAMM cross-chain liquidity model)

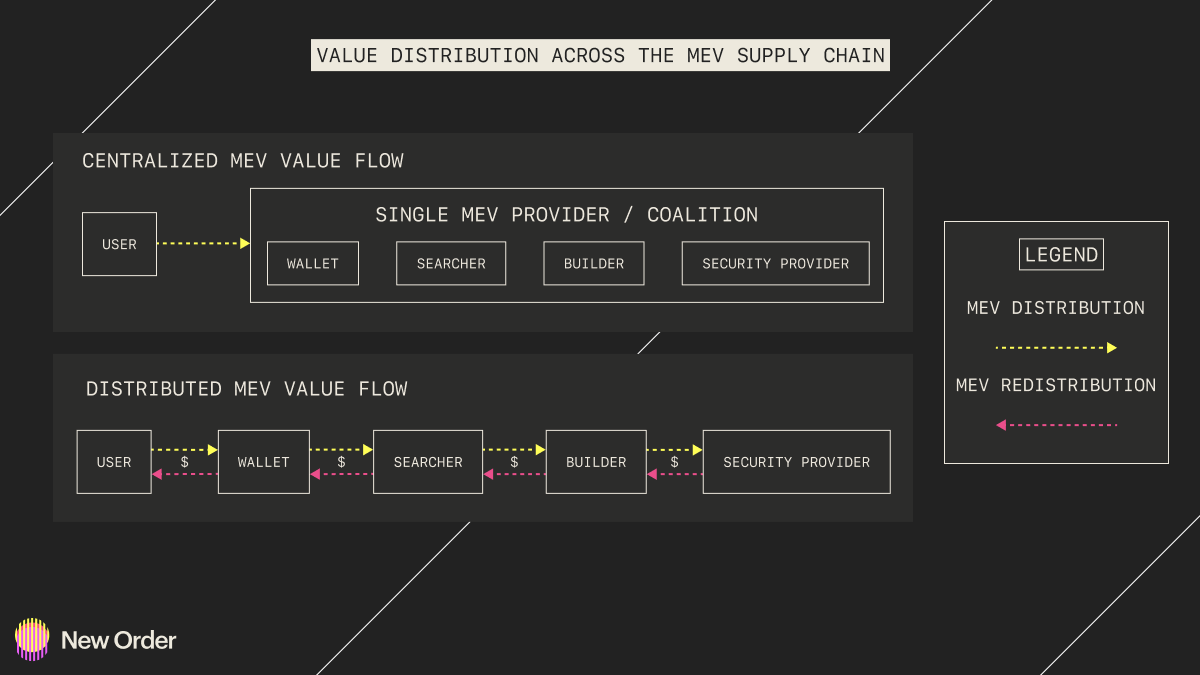

The Most Important Problem to Solve in 2023: Exclusive Orderflow

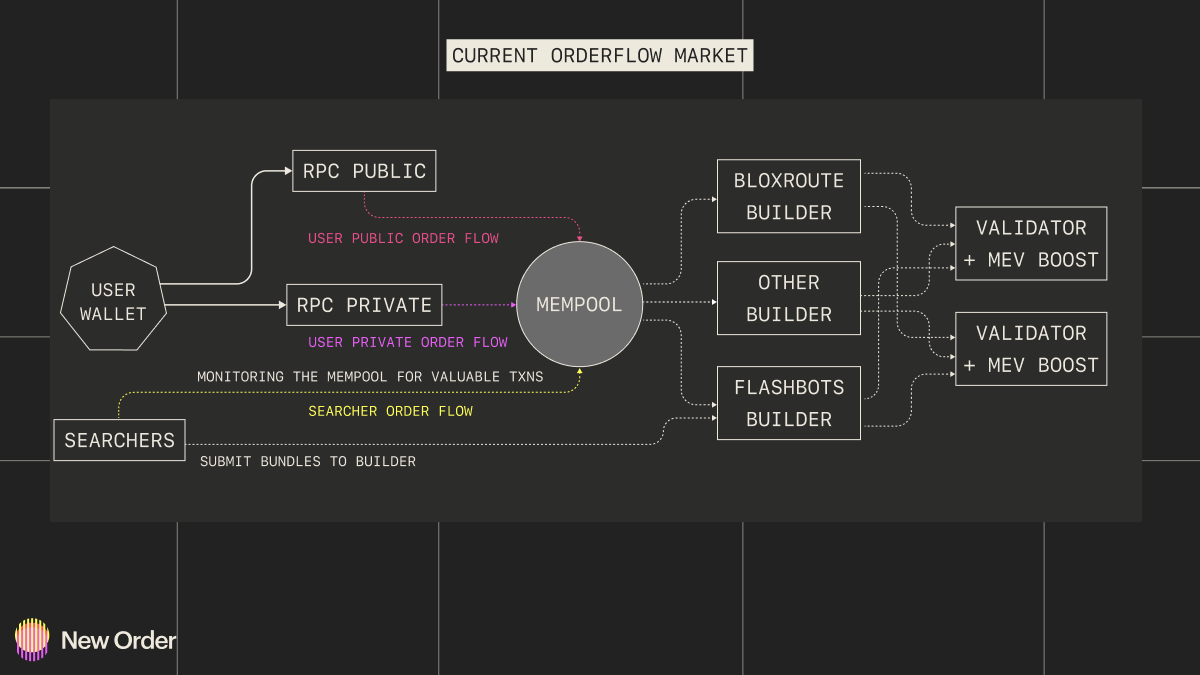

The block builder's primary goal is to extract the maximum amount of value from a collection of “orders,” or orderflow. They ultimately have the incentive to receive as much private orderflow as possible. This is known as the exclusive orderflow (EOF) problem. It is detrimental to blockchain networks because a builder who receives order flow exclusivity, i.e., toxic order flow, gains an outsized advantage over their counterparts and creates a point of centralization on the network which can lead to market manipulation and transaction censoring. Additionally, this value, known as MEV, that is extracted from EOF remains entirely with the extracting parties (builders/searchers) without redistributing rewards to some of the other participating parties (validators/users). This situation will likely result in a small group of colluding builders eliminating all other competitors and gaining control over the orderflow throughout the entire blockchain stack. While there are numerous working solutions to prevent EOF from damaging the network, none are currently fully operational. This threat is truly existential when it comes to the long-term prospects of any blockchain network.

The MEV supply chain comprises a collection of actors (see image above) that play a role in executing transactions. However, these actors often do not act in good faith and extract mercenary value from the $1B+ pool of capital that is up for grabs. Specifically, mercenary value extraction is when value extraction is not equitably distributed among parties that helped facilitate the transaction in the first place. This usually occurs when there are collusive agreements between block builders and relays or proposers, but it can also happen directly between a relay and proposer as outlined here. Yet, the mercenary MEV problem stems from exclusive order flow to various centralized, collusive actors who act only in their interest.

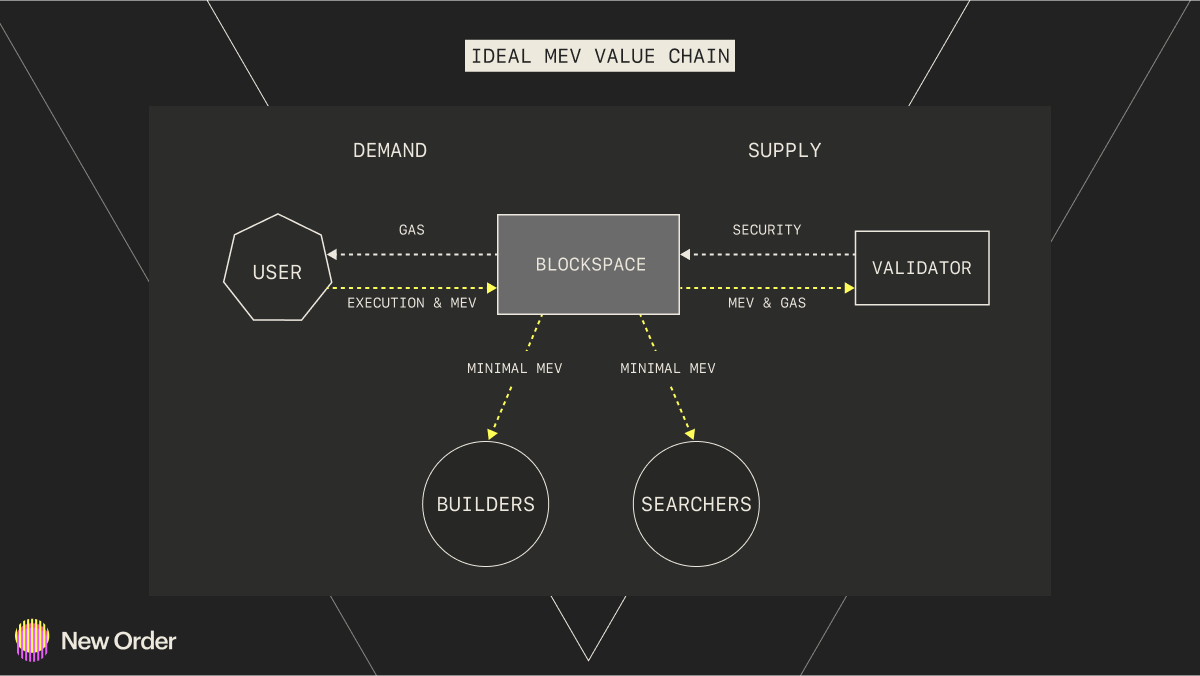

The users and the validators are the two most important parties in the entire chain, so they should be compensated fairly. Users represent the sole source of block demand, and should be rewarded with fair execution and a MEV rebate for the amount of blockspace their transaction(s) use. Similarly, the validators are the source of block security; without them, there would be no block supply. They should be rewarded with market priced gas payments and a majority portion of the MEV. Thus, value extraction from block space should primarily accrue to the edges instead of the middle parties (Builders and Searchers).

The best solution to EOF is to create an optimal blockchain-based financial economy that decentralizes all components of the MEV supply chain and aligns the actor’s incentives toward extracting and redistributing MEV. To this extent, the fundamental question is how to prevent malicious actors from exploiting the system for their gain while maintaining the most critical network properties: security, fairness, and efficiency.

There have been efforts to address some aspects of the problem, but none have completely resolved it. For instance, Flashbots and Bloxroute are off-chain searcher-builder marketplaces that aim to minimize harmful MEV. While they provide some benefits, they also contribute to the risk of centralization, which is a more significant concern. The routers and builders of Flashbots and Bloxroute create a point of centralization that, if exploited, would have meaningful consequences for all actors in the value chain. Additionally, it creates opportunities for cartelization, as sole entities can hold multiple roles across the value chain and create a system of oligopolistic competition.

Despite these challenges, there are several approaches that projects are using to address the EOF problem. In general, there are three primary ways: transaction fee auctions, fair ordering, and randomness. Transaction fee auctions enable builders to bid on transactions, and the highest bidder will receive the fees as a reward. Fair ordering employs a priority-based transaction ordering system that ranks transactions based on specific criteria, such as the size, time, or sender's reputation of the transaction. Finally, on-chain randomness makes it difficult to predict the outcome of transactions, which helps reduce the profitability of front-running and enhances the overall security of the network. The most effective solution is likely a combination of these factors, but it is not possible to determine this until all working solutions are fully operational.

While there have been some positive developments, more focus on the issue is needed. Flashbots, a leading block builder in the industry, open-sourced their builder to promote competition, which has had some success as its market share declined from 75% to 25%. However, more measures are necessary to prevent collusion. One potential solution is a mechanism that decentralizes sequencers, validators, and builders to prevent vertical integration. Two projects, in particular, stand out from the rest: Flashbots SUAVE and DFlow.

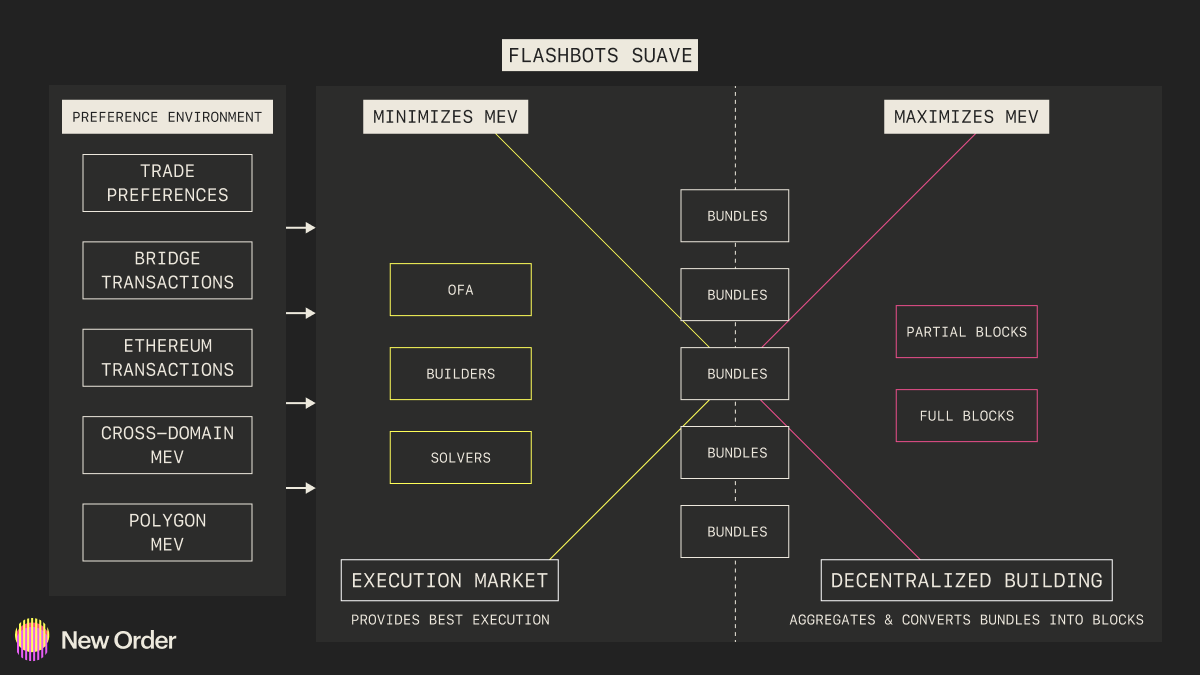

Flashbots SUAVE is an app chain that can serve as a plug-and-play mempool and decentralized block builder for any blockchain. The team has identified EOF and cross-domain MEV as the primary risk factors for centralization in the MEV supply chain. SUAVE aims to address this issue by developing three components: Universal Preference Environment (a chain and mempool aggregator), an Optimal Execution Environment (a network of executors who compete to provide the best transaction execution), and a decentralized block building network. With SUAVE, users’ transactions are private and accessible to all participating block builders, and users are entitled to any MEV they generate. Futhermore, to neutralize the impact of cross-domain MEV, block builders across different chains can integrate in an open and permissionless way. The combination of these components aims to address the entire exclusive orderflow (EOF) and centralization problem.

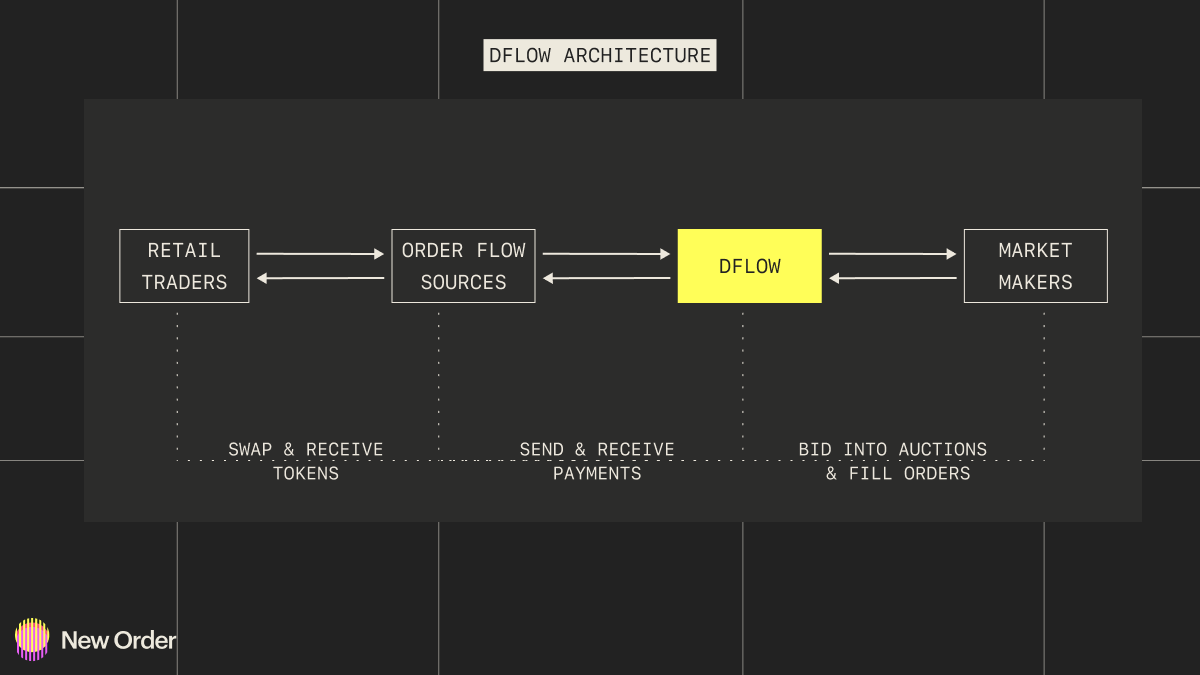

As the name suggests, DFlow is building a decentralized payment-for-order-flow (PFOF) marketplace. Specifically, the project is a Cosmos application-specific blockchain that facilitates decentralized first-price sealed-bid auctions that run in parallel and sequentially. Like SUAVE, DFlow is blockchain-agnostic, meaning that any application, regardless of the blockchain it is on, can sell its order flow, and DFlow will facilitate the PFOF auction.

Other potential solutions or contributing factors to the EOF problem include encrypted mempools (e.g., Shutter), side pools (e.g., EIP-4337), and app-specific mempools via Batch Auctions (e.g., CoW Protocol).

It is probable that a few players will eventually dominate the builder market due to the high upfront cost and technical requirements needed to be profitable in this industry. Vitalik agrees with this idea and has emphasized the need to carefully consider the levels of decentralization in block production that are realistically achievable. In 2023, the need for decentralization in critical areas of block production will become even more evident as the exclusive orderflow problem continues to result in centralized actors colluding and gaining control over a significant amount of value in the network. Collaboration among a wider range of participants working on various approaches will be crucial in identifying the most pressing issues and finding effective solutions. Without a robust decentralized value chain, the consequences could be catastrophic.