Author: Will Owens, Galaxy Research Analyst

Compiled by: Hu Tao, ChainCatcher

Hyperliquid's HIP-4 protocol upgrade marks the arrival of the third prediction market model. Among the existing track giants, Polymarket has a native consumer-facing discovery mechanism, while Kalshi has access to a regulated US exchange. Hyperliquid announced the launch of HIP-4 in February of this year, aiming to introduce outcome prediction markets into this "house of all finance," and formally activated the proposal on the mainnet on May 2. It turns out that for hedgers and speculators, prediction markets are one of the most practically useful new financial primitives in recent years. With Hyperliquid's established industry standards in perpetual contract execution and infrastructure, it is now poised to compete for a share of event trading volume.

Hyperliquid's user base is distinctly different from that of Polymarket or Kalshi. The latter two have spent years building products that attract non-crypto users, both featuring polished consumer front-ends that allow users to "browse" prediction markets like shopping on Amazon. In contrast, Hyperliquid serves active crypto-native traders through a terminal front-end. While this results in a niche top-of-funnel user group, its characteristics are: they are traders themselves, the vast majority hold stablecoins, and their wallets are already connected. HIP-4 is precisely tailored for this type of user first.

As of May 25, HIP-4 has expanded from periodic BTC price binary options to "canonical markets" covering real-world off-chain events, published by validators. Currently launched markets include:

-

"Is the BTC price above X at Z time on Y day?" This is a daily recurring binary contract that resets at 2 AM ET and settles based on the BTC mark price on HyperCore at expiration.

-

"What is the BTC price range at Y time on X day?" This is a multi-outcome contract launched within days of the HIP-4 mainnet activation, featuring three ranges (above, between, below) and settling to the same oracle.

-

Fed June Rate Decision (Hike or Cut / Unchanged), settling around June 17.

-

May CPI Year-over-Year Growth (Exactly 4.3% / Below 4.3% / Above 4.3%), settling around June 10 based on official data from the US Bureau of Labor Statistics (BLS).

-

NBA Finals Game 4 (New York Knicks / San Antonio Spurs).

-

2026 NBA Champion (Knicks / Spurs).

-

2026 World Cup Champion (France / Spain / England / Portugal / Brazil / Argentina / Germany etc.).

As a starting point, this product scope is still relatively limited. But the truly intriguing question is: how far can HIP-4 go? How does it compare to Polymarket and Kalshi in terms of infrastructure, fee rates, and distribution channels? And what does its entry mean for this prediction market track where various players are running towards the "trade everything" model from different starting points?

This article provides an in-depth analysis of HIP-4: what it achieves, its comparison with Polymarket and Kalshi, and its far-reaching impact on the overall prediction market landscape.

Summary

-

Mainnet Launch: HIP-4 officially launched on the Hyperliquid mainnet on May 2, 2026. The proposal was announced on February 2, landed on the testnet that week, and was formally delivered three months later. Now, outcome prediction contracts sit alongside perpetual contracts and spot trading under a single margin account in HyperCore (Hyperliquid's native trading engine).

-

Delicate Timing: This launch came just days after Polymarket completed its migration to a new central limit order book (CLOB v2) and a new stablecoin (pUSD). In the same week, Bloomberg reported that Polymarket is seeking US regulatory approval to bring its flagship exchange to the compliant US domestic market.

-

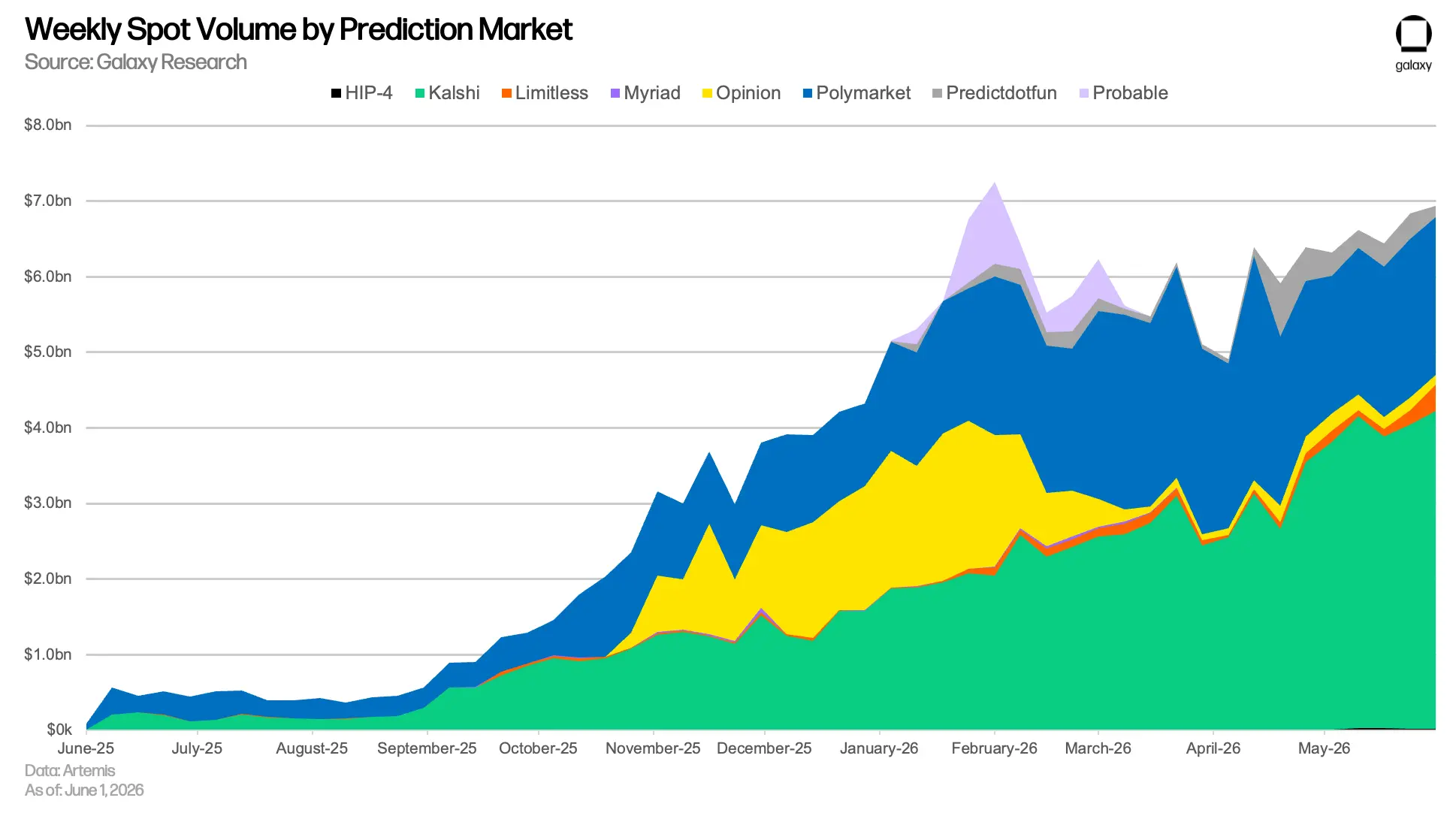

Industry Scale: In April, the historical cumulative trading volume of prediction markets broke through $150 billion. Kalshi set a new all-time high in notional trading volume of $14.81 billion (up 13.3% month-on-month) and, for the first time, surpassed Polymarket comprehensively in notional volume, taker volume, and number of trades. In contrast, Polymarket's trading volume declined to $9.01 billion (down 14.8% month-on-month).

-

Growth Trajectory: Despite the sector experiencing its first month-on-month decline in monthly trading volume after seven consecutive record months, the long-term growth trend remains strong: monthly taker trading volume has grown over 17x in two years. Analysts at Bernstein predict the sector will scale from $51 billion in 2025 to $1 trillion by 2030.

-

Technical Advantage: HIP-4 is embedded directly into HyperCore (Hyperliquid's on-chain CLOB), sharing the same execution layer and unified margin account with perpetual contracts and spot trading. Sub-second finality, throughput of approximately 200,000 orders per second, and cross-margin composability are structural advantages that Polymarket (currently considering migration) and Kalshi (closed centralized infrastructure) cannot replicate without rebuilding their entire products.

-

Initial Results: By day 25 of launch, HIP-4 had captured 20.1% of the combined 24-hour BTC prediction market volume ($2.38 million for HIP-4 vs. $9.46 million for Polymarket).

The Current Prediction Market

Over the past 18 months, prediction markets have been one of the most compelling growth stories in both crypto and the broader fintech space. We've written about them multiple times, as well as about variants like influence markets and decision markets. The combined monthly trading volume of Polymarket and Kalshi was around $2 billion as of September 2025. By April 2026, the combined notional volume of these two platforms reached approximately $24 billion, with historical cumulative total volume surpassing $150 billion for the month. Monthly taker trader volume grew over 17x in less than two years.

In April, Kalshi's leading advantage began to show structural changes.

Kalshi reported April notional volume of $14.81 billion, up 13.3% from its previous record in March, marking a new all-time monthly high. Polymarket's volume fell 14.8% to $9.01 billion. Kalshi's lead expanded from $2.5 billion in March to $5.8 billion in April, the largest monthly gap on record between the two platforms. Kalshi also surpassed Polymarket in taker trader volume ($5.42 billion vs. $1.99 billion) and number of trades (94.4 million vs. 87.4 million), reversing Polymarket's long-standing lead in trade count.

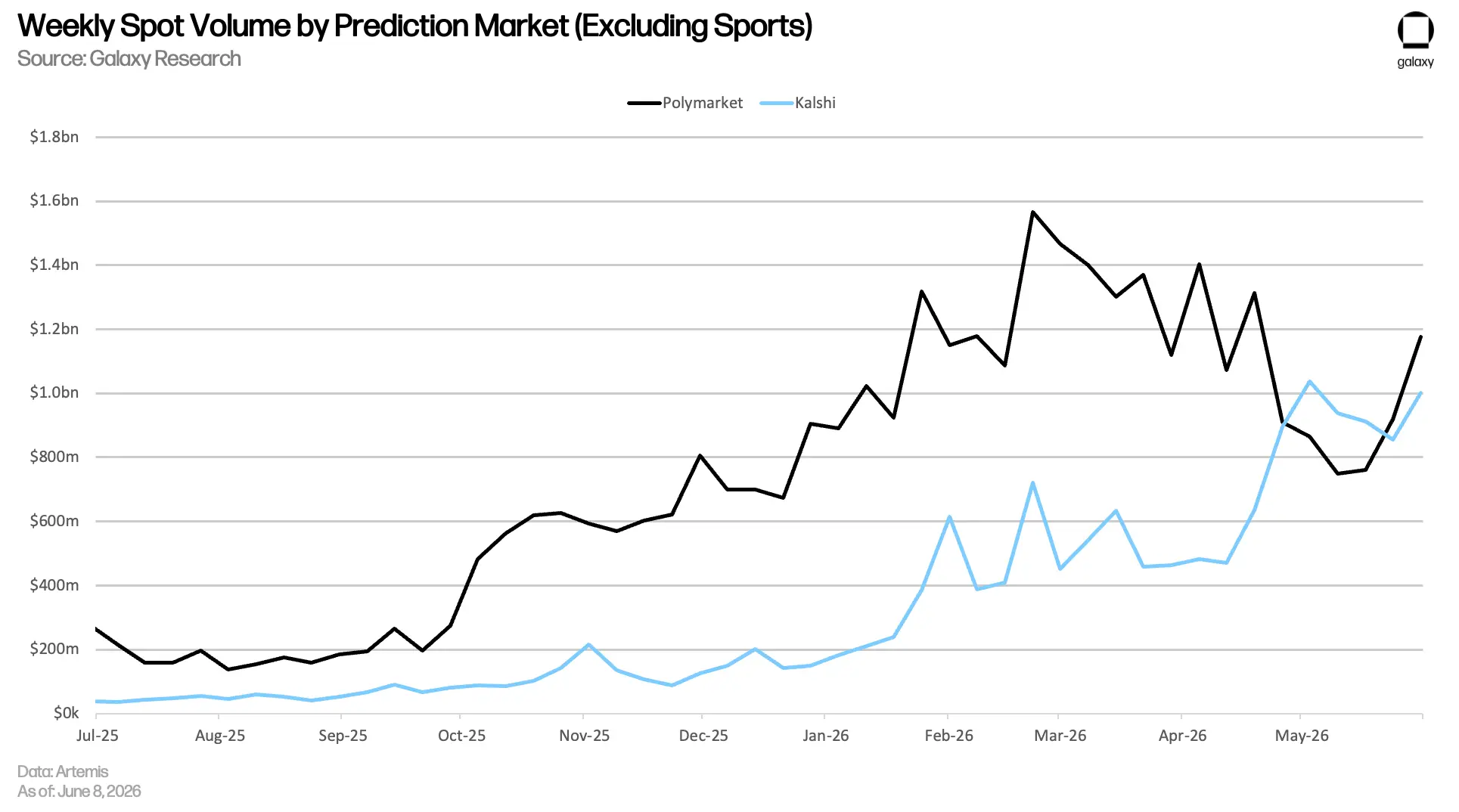

Two structural drivers explain Kalshi's lead. The first is product mix. In late April, sports contracts accounted for 74.3% of Kalshi's weekly volume, with Exotics (the platform's parlay-style combination contracts) pushing that share to around 85%. The US Masters golf tournament alone generated $545 million in notional volume on Kalshi, on par with the platform's Super Bowl single-game total. Kalshi's preparations for the NBA Finals and 2026 FIFA World Cup are well-established. That said, sports markets skew more speculative, lacking the "information signal" value generated by geopolitical or tech markets, despite some commercial hedging use cases. The second driver is regulatory clarity. Kalshi's status as a CFTC-regulated Designated Contract Market (DCM) has brought it distribution partnerships and a faster path to US retail access than Polymarket.

Polymarket's category mix is more diverse (as of late April: sports 46%, politics 27%, crypto 22%), which is structurally an advantage during periods of political volatility or major crypto cycles, but a disadvantage during periods lacking political catalysts and dense with sports events. April was the latter. Polymarket's active user count also declined, from about 733,000 in March to 646,000 in April.

Nonetheless, Polymarket's economics remain strong. Polymarket collected $47.7 million in fees in April. Its user base also remains significantly larger than Kalshi's implied retail base. Polymarket has the deepest non-sports markets in the category, an official partnership with MLB announced in March, and a $2 billion strategic investment from ICE, the parent company of the New York Stock Exchange. The platform already operates a limited, US-compliant product through an acquired CFTC-licensed exchange and is working to bring its flagship exchange onshore (more details below). It also just completed a major infrastructure upgrade (CLOB v2 and migration from USDC.e to its new internal collateral token pUSD) four days before HIP-4's launch on April 28.

April also marked the first sector-wide month-on-month decline in monthly trading volume after seven consecutive record months. Whether this is a calendar effect (April had no Super Bowl, no March Madness, no NFL playoffs) or the first real demand ceiling will be revealed as we observe May's performance.

As of May 1, sector open interest was $1.11 billion, with Kalshi at $630.7 million and Polymarket at $449.9 million (combined representing about 98% of the total share). Limitless, predict.fun, and Opinion each held less than $150 million.

Every major platform is moving from different starting points towards the same "trade everything from one account" model.

What's interesting here is the strategic convergence beneath the volume numbers. Both Kalshi and Polymarket are reportedly building perpetual contracts. Hyperliquid has already built outcome markets via HIP-4. Every major venue is moving from different starting points towards the same "trade everything from one account" model.

HIP-4 Mechanics

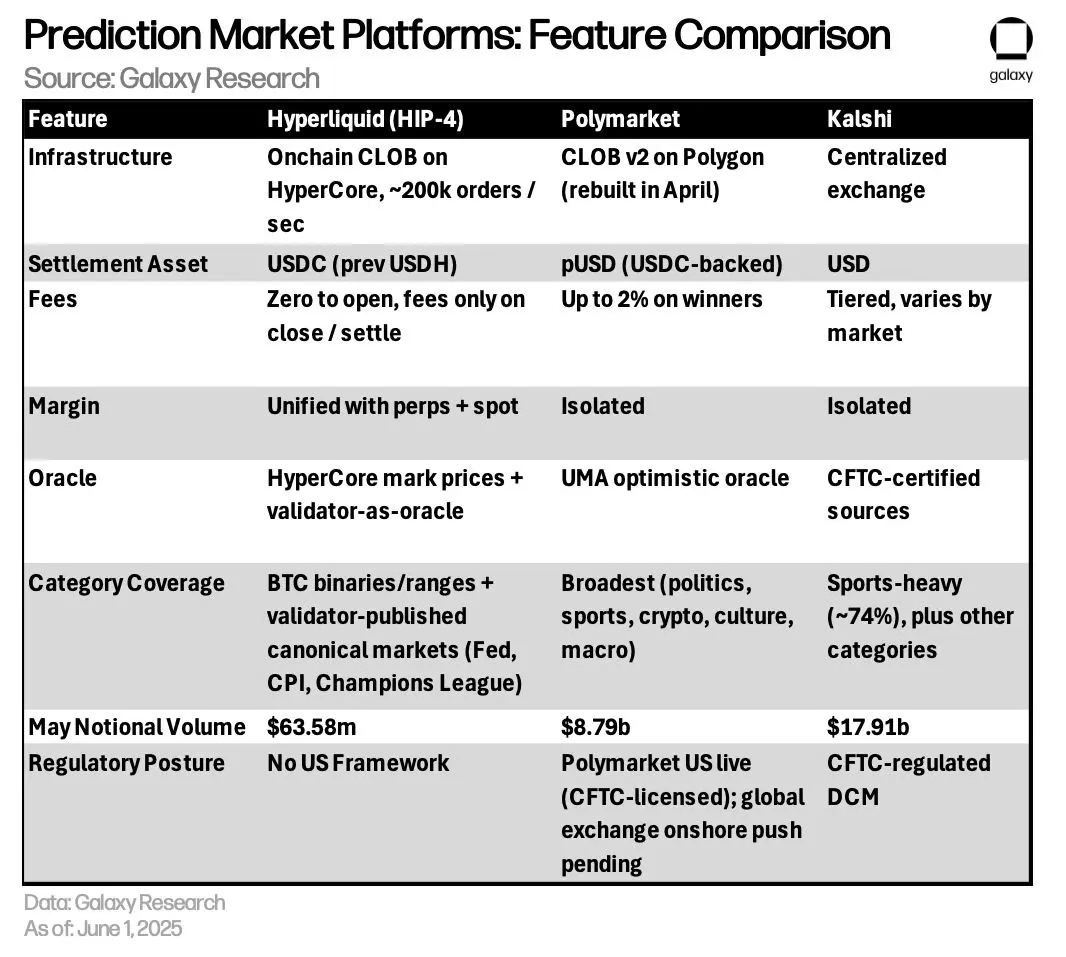

HIP-4 adds outcome markets to HyperCore (Hyperliquid's on-chain trading engine). These are fully collateralized binary instruments that settle to 0 or 1 at expiration based on whether a discrete real-world event occurs. The mechanics are simple and familiar to prediction market traders: buy "Yes" at price P. If the event occurs, the contract settles to 1, and you profit (1 – P). Buying "No" is the opposite. Maximum loss is always your entry cost. No leverage, no liquidation. Under the Coinbase/Circle AQAv2 arrangement, USDC is becoming the consistent quote asset across Hyperliquid's markets; canonical HIP-4 outcome markets settle in USDC, and USDH issued by Native Markets is being phased out.

To deploy a market, a builder must stake 1 million HYPE, then define the event title, resolution time, oracle source, and optionally a dispute window. The 1 million HYPE stake is per builder deploying markets. Canonical markets are published directly by the validator set, requiring no builder stake, with deployment and settlement managed by on-chain validator votes.

A one-time, ~15-minute single-price clearing auction opens the market and clears at the price that maximizes matched volume. This is followed by continuous limit/market order trading, with prices constrained between 0.001 and 0.999 until expiration. At settlement, the oracle posts 0 or 1, and USDC is automatically paid out. The P&L card looks similar to a perpetual trade, except the title is the market question instead of an asset ticker, and your position size is expressed as a number between 0 and 1 instead of a levered notional amount. If the outcome is challenged, the dispute window delays final settlement.

A notable technical detail: each outcome market has two tokens ("Yes" and "No"), but their order books are merged to share liquidity. An order to buy "Yes" at price P is equivalent to an order to sell "No" at price 1-P. Under the merged book, price-time priority generalizes to price-side-time priority. This means at the same merged price level, resting sell orders fill before resting buy dual orders. For advanced users, balances can be manually split and merged between primary and secondary sides. These are mostly abstracted at the API level, but this is the mechanism that allows HIP-4 markets to quote tight spreads with relatively thin nominal liquidity.

HIP-4 charges zero fees on opening positions. Fees are only levied when closing, burning, or settling. (In practice, during this initial testing phase, all outcome market fees are zero.) For traders, predicting the future on Hyperliquid is significantly cheaper economically than on Polymarket and Kalshi, which charge materially higher fees on winning positions. This fee design also plugs directly into Hyperliquid's tiered fee structure (outcome market volume counts toward protocol-wide tier calculations), meaning active prediction market traders become eligible for lower fees on their perpetual contracts through the same unified account.

The first live contract covered a recurring daily BTC price threshold event resetting at 2 AM ET. The market is essentially "Is BTC above X at Y time on Z day? Yes or No." Within days of the mainnet launch, Hyperliquid added multi-outcome markets, starting with a recurring BTC price range contract that settles daily to three buckets (upside, downside, within range). Planned expansion categories include politics, sports, macro data releases, crypto, and entertainment.

On May 25, the canonical market set expanded to include off-chain events. Hyperliquid validators now directly publish markets using automated news feed software running as part of the chain operation, with on-chain validator votes managing deployment and settlement. The first off-chain markets are the June Fed rate decision (change or unchanged, settling around June 17), May CPI YoY (three-bucket multi-outcome around 4.3%, settling around June 10 per BLS data), and the UEFA Champions League football champion (Paris Saint-Germain or Arsenal). Settlement remains closed-loop inside Hyperliquid L1: no external oracles, no UMA-style optimistic dispute layer (arguably Polymarket's Achilles' heel), just validator votes based on predefined rules and automated feeds.

A natural reaction to HIP-4 is to compare it to HIP-3 (Hyperliquid's framework for builders to deploy perpetual contracts). Both involve builders staking HYPE to deploy markets on HyperCore. Both share the same matching engine and order types. But the two primitives differ structurally in ways that matter for what each can trade.

HIP-3 perpetuals use continuous oracles with ~1% price deviation limits per update; this design works for continuous levered trading on assets with continuous price discovery. This works for equities, FX, commodities, and crypto, precisely the categories that trade.xyz and other HIP-3 deployers have already built. But it doesn't work for discrete events.

A perpetual can't cleanly express questions like "Does the Fed cut rates?" or "Does Trump win Oregon?". The payoff isn't continuous, the oracle isn't, and there's no funding rate to converge the contract to the correct answer.

HIP-4 uses fixed-range settlement, no funding rates, and no liquidation engine. These contracts are limited to their entry premium and rely on a single oracle post rather than a streaming price feed. This is why HIP-4 must exist as a separate proposal, not a subfeature of HIP-3.

Perhaps the most powerful part of HIP-4 is what it allows traders to do with the rest of their Hyperliquid account. Unified margin unlocks several specific use cases that any standalone prediction market platform cannot match without a full product rebuild.

First is discrete event hedging for a perpetual book. A trader holding an ETH perpetual long ahead of a Fed meeting historically had two choices: reduce size or accept the binary risk exposure. HIP-4 introduces a third: buy the "Yes" or "No" contract on the event itself in the same margin account. The outcome position partially offsets the directional risk of the perpetual without closing the position. For example, holding a $10,000 ETH-PERP long ahead of a Fed decision can be paired with a $1,000 "No" contract on "Fed cuts rates." If the Fed holds and ETH falls, the outcome position pays out (1 – P) and offsets some of the perpetual loss. If the Fed cuts and ETH rallies, the trader loses the outcome position's premium but keeps the perpetual upside. The hedge sits in the same margin account and settles in the same collateral.

Second is market maker hedging for discontinuous risk. A delta-neutral perpetual market maker faces tail risk from one-time events (regulatory announcements, protocol upgrades, sudden macro decisions) that streaming perpetual hedges can't cleanly express. A market maker quoting ETH or BTC perpetuals ahead of a CPI release can use HIP-4 contracts to hedge the discontinuous part of the risk without moving funds to a separate platform or running a parallel options book. This is a real improvement in risk management for professional liquidity providers on Hyperliquid.

For a user already trading perpetuals and spot on Hyperliquid through the same account, the cost of entry into prediction markets is essentially zero.

How Does HIP-4 Compare?

HIP-4, Polymarket, and Kalshi are now competing for the same end state: a venue where users can express views on any event from a single account. But they start from different products, different infrastructure, and different regulatory postures. The table below lists the structural differences. The following subsections elaborate on the dimensions where the gaps matter most.

User Experience & Discovery

Polymarket and Kalshi have spent years building consumer-facing front-ends, and both work. They just serve different audiences and generate market depth in different ways. Kalshi's depth comes from programmatic, vertical-specific market generation. An NBA basketball game on Kalshi doesn't spawn just one market. Instead, it spawns markets covering player prop bets, spreads, and combination contracts.

Multiply that across every major sports league, daily weather and economic data releases, and macro data release cycles, and Kalshi's active contract count runs into the hundreds of thousands. The result is massive depth within a limited set of CFTC-permitted verticals. The app is sports-first (sports, including Exotics, currently drive ~85% of weekly volume), and its onboarding flow is the cleanest in the category. Deposit dollars, no crypto wallet needed, no cross-chain bridges, fully regulated (provided the user doesn't mind KYC). Kalshi is live on the Robinhood and Coinbase apps, putting prediction markets in front of tens of millions of retail traders who never thought to download a dedicated app. This combination of programmatic depth, regulated onboarding, and embedded distribution is what drove it past Polymarket in April volume.

Polymarket is the opposite. Its depth is in breadth. Operating outside US commodity trading rules, Polymarket can list long-tail markets Kalshi legally cannot touch: hyper-specific foreign elections, foreign policy events, court rulings, Twitter spats, crypto protocol upgrades, etc. Its category mix is the broadest in the industry: politics ~27% of weekly volume, sports 46%, crypto 22%, with culture and macro filling the rest. Its front-end is built on a browsing experience, with curated categories, "trending" markets, a social layer for users discussing active markets (comment sections), and an onboarding flow that walks users through their first trade. The result is 646,000 monthly active users in April and the deepest non-sports liquidity in the category.

These are different products serving different users. If you want to intraday trade NBA player props or tiny moves in Fed Funds futures, Kalshi has the programmatic depth. If you want to take a position on the UK general election or a celebrity court ruling, Polymarket is currently the only option. Both work. Neither will lose its respective audience to the other in the near term. It will be interesting to see which one can tap institutional flows. Prediction markets as an institutional hedging tool are perhaps the most lucrative market for platforms, and Kalshi seems best positioned to do that.

HIP-4 has none of this. Outcome markets are tucked into Hyperliquid's trading terminal alongside perpetuals and spot. There's no "browse markets" view, no trending feed, no social layer, no distribution partnerships with retail brokers, no programmatic market generation across sports or macro. To be fair, HIP-4 just launched. Discovery runs through builder front-ends like Outcomexyz and Stratium, early projects whose footprints remain small.

This is a real near-term gap.

The question is whether the builder ecosystem can fill this gap fast enough to matter. Hyperliquid's framework explicitly invites third parties to deploy markets and build front-ends on top of HIP-4, precisely how perpetuals expanded on the platform via HIP-3 (trade.xyz alone now accounts for most of HIP-3 open interest). If a comparable builder ecosystem emerges for outcome markets on Hyperliquid, the discovery gap could shrink faster than expected. If it doesn't, HIP-4 may remain a niche product inside active trader accounts.

Infrastructure

HyperCore is the strongest part of the HIP-4 proposition and the dimension with the largest gap to Polymarket and Kalshi. Hyperliquid's execution layer is an on-chain CLOB with sub-second finality, throughput of ~200k orders per second, and a unified margin engine that handles billions in daily perpetual volume. HIP-4 plugs into that infrastructure without modification. Outcome markets share the same matching engine, same order types, same wallet, and same collateral as perpetuals and spot.

Currently, Polymarket is running a brand-new rebuilt central limit order book on infrastructure not designed for it.

Polymarket runs on Polygon, an Ethereum L2 blockchain. The CLOB v2 launched on April 28 is a complete rebuild of the matching engine and migration to pUSD as the internal collateral token, a meaningful upgrade. But Polymarket's chain dependency remains structural. The platform's VP of Engineering, Josh Stevens, has publicly acknowledged that reaching the performance levels needed for active trading would mean migrating to a dedicated chain. Whatever Polymarket does next on infrastructure will require multiple quarters of engineering work and likely some form of chain migration. For now, Polymarket is running a brand-new rebuilt CLOB on infrastructure not designed for it.

Kalshi runs on centralized exchange infrastructure. It's fast, stable, regulated, and closed. Kalshi cannot natively combine with on-chain products, cannot offer cross-margin with crypto positions, and cannot let users self-custodial collateral. The trade-off is frictionless dollar onboarding and regulatory clarity. For institutions that need a CFTC-regulated counterparty, Kalshi's infrastructure is the feature.

The ranking across the three: HyperCore is the most flexible execution layer in the category, Polymarket is mid-transition, and Kalshi is designed as a closed system. But infrastructure alone doesn't win volume. It must be paired with markets, users, and discovery. That's the part HIP-4 still needs to prove.

Oracle Scope

At the May 2 mainnet launch, HIP-4 was limited to HyperCore's price feeds. The only markets it could parse were variations of "What is BTC's price at time T?". The initial two markets, the daily binary and the multi-outcome range contracts, were both BTC price events. The May 25 expansion changed this. Hyperliquid validators now directly publish off-chain canonical markets, running automated news feed software as part of regular chain operation, with deployment and settlement via on-chain validator votes. Parsing remains closed-loop inside Hyperliquid L1. No UMA-style optimistic dispute layer, no Chainlink or Pyth integration.

This is a third path not previously seen in the category and worth calling out explicitly. Polymarket has UMA's optimistic oracle, which parses arbitrary real-world events through a staking and challenge mechanism. It's permissionless and universal, which is why Polymarket can list markets on-demand on any tweet, foreign election, court ruling, or protocol upgrade. Kalshi has CFTC-certified resolution sources, each contract going through a filing process that approves the market and the resolution method. The oracle layer is slower and more rigid than UMA's but highly defensible in a regulatory sense.

Hyperliquid's validators-as-oracle model is curated, not permissionless, meaning it can't match UMA's long-tail coverage. The validator set must actively choose, which filters for quality but limits throughput. But it's demonstrably faster and more flexible than Kalshi's filing process and runs without dependency on a third-party parsing layer. The model works well for high-signal events with clear outcomes, less well for long-tail markets where standards are disputed or the event itself is ambiguous.

What's worth watching over the next 6-12 months is what Phase Two (permissionless builder deployment, akin to HIP-3) will look like. The canonical market question is now answered (validators handle them directly), but the permissionless layer remains open.

Regulatory Posture

The three platforms occupy three different regulatory positions, and the asymmetry matters more than my table captures.

Kalshi is a CFTC-regulated Designated Contract Market (DCM) with frictionless US retail access. That status is precisely what unlocked the Robinhood and Coinbase distribution partnerships. But Kalshi's sports contracts face legal challenges from states claiming jurisdiction over such wagers. Massachusetts has issued a ban. Wisconsin has filed a lawsuit. VC firm a16z (also a Kalshi backer) wrote to the CFTC in April supporting federal preemption, a notable industry intervention, but the issue isn't settled. If federal preemption holds, Kalshi keeps its largest growth category. If not, the sports business that drove 85% of Kalshi's April volume gets carved up state-by-state.

Polymarket is seeking a full return to the US market. It already has a domestic foothold: following last year's acquisition of a CFTC-licensed exchange (QCEX), Polymarket launched a limited, US-compliant product. But that version is like a popcorn stand next to the flagship store overseas, with a tiny fraction of the markets, liquidity, and category breadth. The real prize is bringing the flagship store itself onshore. In the same week HIP-4 launched, Polymarket was reportedly seeking CFTC approval to do just that. If approved, Polymarket would gain nationwide retail access it has struggled to reach for years, putting its deepest markets and broadest category coverage in front of US traders for the first time, rather than the simplified product it currently runs domestically.

HIP-4 inherits Hyperliquid's broader regulatory exposure, the same legal gray area the rest of crypto-native DeFi inhabits. CME Group and ICE, parent of the New York Stock Exchange, have reportedly urged US regulators to scrutinize Hyperliquid. Per news reports, the two exchanges told the CFTC and lawmakers that Hyperliquid's decentralized environment poses risks of manipulation and sanctions evasion, particularly focusing on 24/7 commodity and crude oil contracts running under HIP-3, categories long dominated by CME and ICE.

On-chain analyst ZachXBT pointed out that the NYSE reportedly took issue with Hyperliquid but not Polymarket, despite ICE's $2 billion investment in the latter. ICE's stake may give it a direct interest in slowing Hyperliquid's expansion into prediction markets via HIP-4, not just its push into commodities via HIP-3. Critics read the lobbying as an attempt to stifle a fast-growing competitor, especially as both incumbents face their own CFTC and DOJ scrutiny over timely oil trades. Hyperliquid called the manipulation claims "unfounded concerns," arguing public blockchains expose manipulation rather than facilitate it. HYPE token price declined the day of the Bloomberg report.

The broader regulatory picture is also shifting. The Senate Banking Committee passed the CLARITY Act on a bipartisan 15–9 vote on May 14, moving the bill to the full Senate floor. The legislation would create a federal framework classifying most digital assets as commodities under CFTC jurisdiction, formally extending CFTC authority over derivatives to include crypto spot markets. The bill also includes provisions shielding non-custodial software developers from money transmitter laws (see CLARITY Act Sec. 604, the "Blockchain Regulatory Certainty Act" or "BRCA"). While that safe harbor is designed for developer prosecutions of the Tornado Cash and Samourai mold (programmers who write and release open-source software but exercise no ongoing control), and Hyperliquid is a different fact pattern (an actively operated trading venue that happens to settle on-chain), nonetheless, if its developers are determined to be "non-controlling" in the context of Sec. 604, it could be beneficial for Hyperliquid. But the key point is that Hyperliquid would need to navigate Title III of the CLARITY Act, particularly the Sec. 301 framework dealing with securities law and Bank Secrecy Act obligations.

That includes exemptions for decentralized finance trading book applications, but Sec. 301(a)(2)(A) clause removes those exemptions if the protocol is determined not to be a decentralized trading protocol. If Hyperliquid fails to qualify for the exemption and the regulators implementing the Act determine it is not a decentralized trading protocol, then Hyperliquid would need to assume BSA obligations under Sec. 301(b)(d)(D).

During the May 14 Senate Banking Committee markup, there were several amendments to the latest text of the CLARITY Act, not included in the latest publicly available version, reportedly some relating to the BRCA. Further, negotiations over the CLARITY Act's language are ongoing, with issues related to illicit finance and the BRCA among the top items not yet resolved. So all of this could change between the time I write this and the bill's final passage into law.

Beyond BRCA and BSA-related issues, Hyperliquid hopes CFTC's emerging acceptance of perpetuals will include on-chain perpetuals. That hasn't happened yet, and it's unclear if it will, but Hyperliquid founder Jeff Yan spent a week in Washington in mid-May meeting with lawmakers alongside the Hyperliquid Policy Center.

All of this to say: there remain many regulatory questions around whether Hyperliquid could replicate its offshore dominance in the US.

Summary of this section's four dimensions: Polymarket leads on oracle scope and consumer UX, Kalshi leads on regulated US distribution and sports, and HIP-4 leads on infrastructure and unified margin, with its regulatory path potentially opening up. None of the three dominates across all four. What happens as each platform expands into the others' territory will be the category's story over the next 12–18 months.

Risks

HIP-4 launched 25 days ago into a competitive category, and the arguments for why it might not develop into a meaningful product are concrete. The following risks are most likely to determine whether HIP-4 expands beyond a niche feature inside a trader terminal.

Canonical Market Breadth

The remaining limit is breadth, not category coverage. Both HIP-4 and Polymarket curate market launches, so it's not a curated vs. open distinction. The difference is what each parsing layer can support. UMA's optimistic oracle can parse arbitrary real-world events, so Polymarket's curation is a product choice, not a technical ceiling; it can list nearly infinite long-tail markets on-demand as needed.

HIP-4's validators-as-oracle model can only parse what the validator set can adjudicate cleanly, so its curation is partly enforced by the parsing model. The validator set must actively choose to publish each market, an arrangement that, as noted, filters for quality but limits throughput. Long-tail markets (specific foreign elections, court rulings, any event with social controversy) require a Phase Two permissionless deployment with broader oracle integrations, which hasn't launched yet. Until Phase Two arrives, HIP-4's market directory will remain constrained by what validators can parse, limiting the number of markets even as category coverage expands.

Discovery Gap

Hyperliquid is a trading terminal, not necessarily a consumer product. Outcome markets have no native browse layer or social component. The bet is that builder front-ends can fill this gap the way trade.xyz expanded HIP-3. If they don't, HIP-4 will remain a feature for active Hyperliquid traders, never reaching the audience sizes Polymarket and Kalshi have built. Discovery is also the only risk Hyperliquid can't solve on its own. It relies on third parties choosing to build. In Hyperliquid's favor, it's one of the most attractive places to build in crypto.

Validator Centralization

Hyperliquid runs on 24 (soon 27) validators, and the chain's history includes the JELLY delisting event of March 2025, where the team froze a market mid-trade. This precedent is well-known to crypto-native users and is the version of "trust" Hyperliquid operates under. For prediction markets that settle to binary outcomes and where dispute resolution is critical, this is a real execution risk. The May 25 expansion makes this risk more concrete in principle: canonical market resolution now relies on explicit validator votes, not external oracle posts.

In practice, the validator curation model is preemptively avoiding this risk. The initial canonical markets (Fed move/unchanged, CPI bucketed around a fixed number, binary Champions League final) are all designed with clear resolution outcomes tied to a single authoritative source. Harder cases (post-release macro data revisions, contested sports results, ambiguous Fed statement language) are the kind of markets the validator set has an incentive not to publish. The closed-loop design eliminates third-party oracle dispute risk but centralizes resolution power in the validator set, and early market selection suggests Hyperliquid understands this trade-off.

Regulatory Exposure

Hyperliquid, like the rest of the category, operates in the same DeFi gray area. The CLARITY Act offers a plausible path to legality in the US, but it isn't law yet. Until then, HIP-4 inherits Hyperliquid's current status as an offshore, unregulated venue, and the CME/ICE lobbying efforts indicate this risk is real, not theoretical. Regulatory action against Hyperliquid, or a final CLARITY Act that excludes on-chain derivatives or simply fails to resolve its legal status, would severely limit HIP-4's addressable market. The outlook for the next 12–24 months is brighter than six months ago, but the near-term reality hasn't changed.

Convergence Pressure

This risk became non-hypothetical on May 29, when the CFTC approved Kalshi's Bitcoin perpetual contract (BTCPERP), which Kalshi promptly moved to launch. Kalshi had telegraphed the move since April, but approval turned the plan into a realistic competitive threat. This is the first CFTC-regulated perpetual in US history, and the framing is clear: a regulated, onshore alternative to the offshore platforms that dominate perpetual markets, with Hyperliquid squarely in the crosshairs. The "trade everything" pressure is now clearly reciprocal. HIP-4 is Hyperliquid moving into prediction markets; Kalshi launching a perpetual directly attacks Hyperliquid's strongest, most entrenched product.

Two things temper this threat in the near term. First, Kalshi's approval is currently limited to BTC, with the CFTC reviewing additional contracts case-by-case, so this is a single regulated perpetual, not the full multi-asset book Hyperliquid runs. Second, the CFTC currently has only one sitting commissioner, Chairman Michael Selig, a Trump appointee who has advocated bringing perpetuals onshore, making the regulatory posture supportive but also thin and potentially fragile. Polymarket is also reportedly seeking to launch its own perpetual product.

But the direction of travel is now clear. A CFTC-regulated competitor offering onshore perpetuals attacks precisely the institutional hedging flows, the most lucrative prize in the category, and it has something Hyperliquid can't yet offer: US regulatory status. If Kalshi expands beyond BTC before HIP-4 launches permissionless markets and broad category coverage, the convergence race tilts toward the incumbent that can run a full tech stack under US regulation first. Over the next 12 months, the landscape may depend more on who can credibly run a full tech stack than who can best build outcome markets, and Kalshi has fired the first shot.

So What?

The prediction market category is in the midst of a structural shift most coverage misses. The story isn't Kalshi vs. Polymarket, nor HIP-4 vs. either incumbent. The story is convergence. Every major venue is moving towards the same end state: a single account, a single margin engine, all markets in one place. Hyperliquid built outcome markets on a perpetual platform. Kalshi and Polymarket are building perpetuals on prediction market platforms.

The race to trade everything is now the defining competitive dynamic of the category, and the prize is the most lucrative customer segment in crypto-adjacent finance: institutions that need to hedge and speculate across asset classes, events, and time horizons in one place.

Each platform starts from a different moat. Polymarket has consumer distribution and the most flexible oracle layer. Kalshi has US regulatory access and the clearest sports product. Hyperliquid has crypto's best execution infrastructure and a unified margin engine competitors can't match without rebuilding their tech stacks from scratch.

The question is which moat is hardest to copy. In a sense, both Polymarket and Kalshi are trying to build what Hyperliquid already has. CLOB v2 is Polymarket trying to build HyperCore on Polygon. Polymarket reportedly seeking its own chain is Polymarket trying to build an execution layer equivalent to HyperCore.

Kalshi is a different case. It already runs a high-performance regulated exchange, and its May 29 perpetual approval proves it can ship. What's hard for Kalshi to copy isn't the perpetual itself, but the composability around it: cross-margin between perpetuals, spot, and outcome contracts in a single self-custodied account. Kalshi's closed, centralized design is the source of its regulatory clarity but also what prevents that unified, composable account from emerging. Kalshi can match Hyperliquid product-by-product; what it can't easily match is the integrated tech stack.

Hyperliquid, by contrast, needs to expand category coverage and attract a consumer discovery layer. HIP-3 has already shown the platform can attract builders to its primitives. Building markets and discovery on top of an execution layer is easier than re-building the execution layer itself, and the unified, composable account is what Hyperliquid has already built. This asymmetry favors Hyperliquid, though the advantage is narrower against Kalshi than against Polymarket.

The story isn't Kalshi vs. Polymarket, nor HIP-4 vs. either incumbent. The story is convergence.

We are long-term bullish on HIP-4 for two reasons:

First, the regulatory framework for HIP-4 is changing faster than most reporting suggests. The CLARITY Act passed the Senate Banking Committee on May 14. Jeff Yan and the Hyperliquid Policy Center are actively engaging in the process in Washington. Six months ago, offshore DeFi exposure looked permanent. Now, there's a credible path to US regulatory clarity, and Hyperliquid is positioning to seize it.

Second, HIP-4 is moving faster than expected. By day 25, the protocol had captured 20% of combined 24-hour BTC prediction market volume, and the canonical market set published by validators already included the Fed, CPI, and sports events. The validators-as-oracle model is a credible third path between UMA's universal parsing flexibility and Kalshi's CFTC-certified rigidity. Phase Two permissionless deployment remains the long-term unlock for arbitrary builder markets, but near-term category gaps have closed faster than the initial launch implied.

Hyperliquid spent two years becoming the standard for on-chain perpetuals. It did it by building infrastructure first, attracting builders second, and letting the consumer layer assemble on top. HIP-4 is applying the same playbook to a new product surface. The platform that wins this race will be the one whose execution layer is hardest to copy, whose builder ecosystem ships fastest, and whose regulatory path opens widest.

On all three counts, the case for Hyperliquid is stronger than current market positioning implies.