Written by: Jeff Park

Compiled by: Chopper, Foresight News

In the financial world, every generation invents a new tool to package its worst instincts into something that appears prudent.

The 1980s had junk bonds, cloaked in the guise of 'democratizing capital'; the 1990s had emerging market debt, packaged as a noble cause to help developing countries integrate into the global economy; the 2000s had structured credit, so complexly layered that even its designers couldn't understand it before it collapsed.

These 'innovations' share a common thread: they created artificial solutions (like liquidity transformation) for real problems (like insufficient growth), ultimately leading to disaster due to excess.

Private credit is the latest chapter in this story, and perhaps the most insidious one. Unlike its predecessors, it is designed from the outset to make the清算 (liquidation) before a risk explosion completely invisible. By the time it's discovered, the consequences are irreversible.

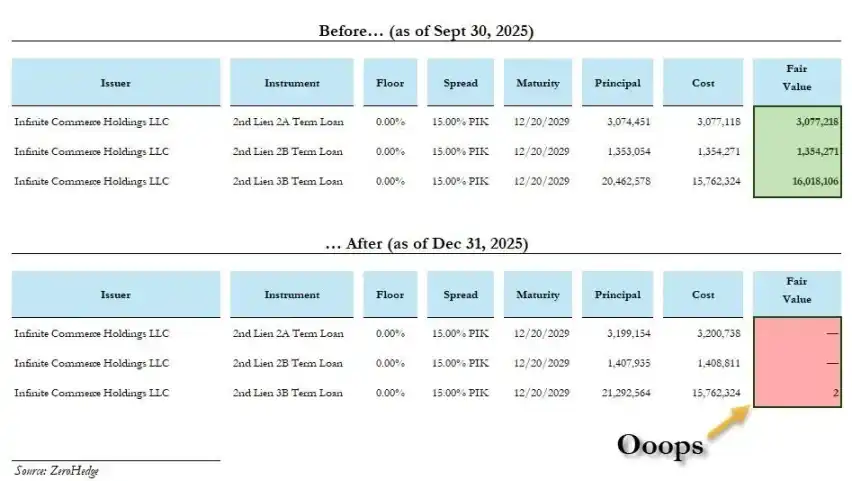

Recently, BlackRock directly wrote down the face value of two private credit loans from 100% to 0 in one go, one of them in less than a month. This doesn't look like a technical error in valuation methods; it looks more like a confession of flawed incentives.

How did we get here?

The Crisis Isn't the Root Cause; Concealing the Truth Created It

The mainstream industry narrative goes like this: After the 2008 financial crisis, banks, constrained by Basel III, became afraid to lend. Non-bank institutions stepped in to fill the void, serving small and medium-sized enterprises. This was the market's inevitable choice.

The more truthful situation is that the post-2008 regulatory framework did not truly eliminate risk. Instead, it actively fostered a shadow system that bears the same underlying risks but evades the regulations originally designed to constrain them.

The private credit market has ballooned from $46 billion in 2000 to about $2 trillion today. This money didn't appear out of thin air, nor did it accidentally flow into pension funds and insurance companies. It was precisely channeled to institutions with large capital bases, long lock-up periods, and a willingness to accept opaque valuations.

Its structure is identical to that which precipitated the 2008 financial crisis, with one significant difference. When the subprime mortgage market collapsed in 2008, losses were concentrated in reckless borrowing households and the banks that lent to them. If private credit crashes, the losses have no boundaries; the money comes from life insurance policyholders and pension beneficiaries—ordinary people.

The socialization of losses that outraged the public in 2008 at least had a preceding period of private gains. With private credit: profits go into the pockets of fund managers, losses are socialized and flow to the retirement accounts of teachers, nurses, civil servants—people who never agreed to bear this risk.

Worse, the industry, not content with just harvesting institutions, is now targeting retail investors. Since 2025, private credit ETFs have become hugely popular, but the problem is even more severe: illiquid assets don't become liquid by being put into an ETF. It merely transfers the bomb of 'redemption runs hitting but assets being unsellable' from professional institutions to the brokerage accounts of ordinary investors.

This is the reality unfolding.

Asset Allocators Who Hate Bitcoin Expose Everything

Over the past few years, I've been recommending Bitcoin to institutions everywhere and discovered a startling pattern: those who reject Bitcoin are often fervent enthusiasts of private credit. This isn't just two different viewpoints on a topic; it's the same mentality.

Their objections to Bitcoin sound 'prudent': too volatile, drawdowns are inexplicable, no cash flow so it can't be valued.

But the subtext is: Bitcoin's price is too honest. Real-time, public, visible to all. If it makes a mistake, it's wrong, and it can't be hidden.

Private credit is the exact opposite:

- Valuation changes are extremely slow, 'smoothed' quarterly by fund managers

- There is no liquid market to puncture the lies

- Lock-up periods are long enough for the decision-makers to get promoted, change jobs, or retire

The so-called 'proprietary deal flow' is just an excuse for a lack of effective pricing competition.

A true fiduciary seeks the truth. These allocators seek to avoid facing the truth. This isn't risk management; it's the opposite of risk management, yet it's cloaked in professionalism, completely disregarding the beneficiaries' interests.

The AI Boom Turns It Into a Systemic Risk

Morgan Stanley estimates that from 2025 to 2028, global data centers will require $2.9 trillion in capital expenditure, with about $800 billion of that to be solved by private credit. This has turned private credit from a lending market into the key infrastructure for the most important technological transformation of the coming decades.

A typical case: In October 2025, Meta and Blue Owl completed a $27 billion data center financing deal, the largest private credit transaction in history. The money came from PIMCO, BlackRock, and ultimately from pensions and insurance companies.

The cruelty of this cycle: the retirement savings of ordinary workers are used to fund automation and AI, which in turn replaces the very jobs of those workers. Private credit distorts the cost of capital and suppresses the value of labor. Now, nearly $50 billion in private credit floods into the AI sector every quarter.

The financialization of AI infrastructure and the displacement of the workforce that funds it form a closed loop: the left hand cuts the right hand.

Liquidity Transformation is Theft of Time

I'm not saying credit itself is sinful, nor that all private credit firms are bad. Credit has always been a game of probabilities; bad debts and mismatches exist in every era.

The key difference is: who truly bears the loss?

- If a bank makes a bad loan, it's on their balance sheet, regulated, faces bank runs and equity wipeouts—there is real money at risk;

- Private credit managers earn performance fees, incentives that 'encourage you to place bets,' not incentives that 'encourage you to win responsibly.'

By the time the loan goes to zero, the manager has already made enough money.

Every financial engineering endeavor ultimately points to one question: who bears the costs nobody wants?

The 'brilliance' of private credit is how 'elegantly' it answers this question:

Profits flow upward and backward: to the older, already retired beneficiaries of long-term capital

Costs flow downward and forward: suppressing wages, freezing hiring, delaying investment, distorting the entire economy's cost of capital

Private credit is the theft of time.

This is the age-old liquidity transformation in finance, just stripped of its disguise.

They bear risks they shouldn't have to bear, through tools they cannot choose, at prices they cannot foresee.

Lock-up periods ensure they cannot exit. The lack of public valuation ensures they cannot protest. And the quarterly valuation smoothing mechanism ensures that when the final bill comes, those responsible are long gone.

It doesn't look like plunder; it looks like 'steady returns.' The two are almost indistinguishable until the moment of collapse. While this story is age-old, the novelty lies in its sheer scale, its profound lack of transparency, and the astounding success of an asset class built on this illusion of safety, which has managed to convince the world's most cautious capital managers.

There is no asset class in the world that can be valued at 100% for three consecutive months and then written down to zero overnight.

If this isn't theft, then I don't know what is.