This article is from:Bankless

Compiled by|Odaily Planet Daily (@OdailyChina); Translator|Azuma (@azuma_eth)

On July 7th, Strategy disclosed that the company sold 3,588 BTC between June 29th and July 5th, worth approximately $216 million.

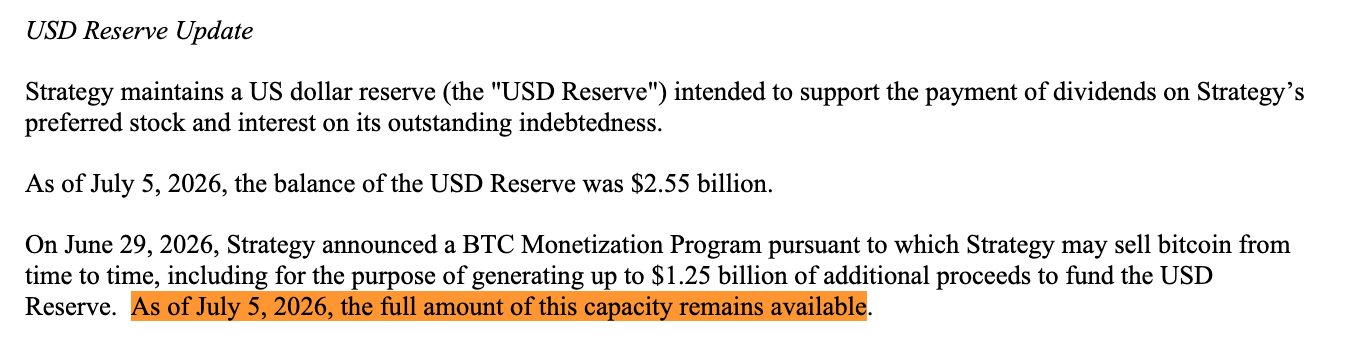

These funds were used to pay STR C dividends and replenish the USD Reserve previously used for dividend payments. Despite completing this sale, Strategy stated that its full $1.25 billion reserve-building capacity remains intact.

- Odaily Note: In the "self-help plan" announced last week, Strategy had indicated it authorized the company to sell BTC to build a USD reserve of up to $1.25 billion.

In other words, the $216 million worth of BTC sold to replenish the reserve is not counted against the previously disclosed reserve-building capacity.

Strictly speaking, there is a technical distinction: one is "replenishing," and the other is "building." However, in practice, both types of sales ultimately flow into the same reserve pool for the same purpose, just categorized for different uses.

From another perspective, the previously disclosed "BTC Monetization Program" never limited Strategy to selling only $1.25 billion worth of Bitcoin in total; it only capped one specific funding pool — the sale of BTC to "build" the USD reserve.

The plan also permits Strategy to sell BTC for other purposes, which is exactly what we are seeing now.

Three Funding Pools

On June 29th, after weeks of pressure on MSTR and STR C, Strategy launched the aforementioned BTC "Monetization Program" as part of its broader "Digital Credit Capital Framework."

This plan allows Strategy to sell Bitcoin and actually mentions three primary uses:

- First, to Build the reserve: Sell up to $1.25 billion worth of BTC to establish a USD Reserve.

- Second, to Cover the preferreds: Sell BTC to cover Strategy's fixed dividend and interest obligations on its preferred shares and debt. If management deems it "more advantageous to sell BTC than issue common stock," they may also sell BTC to replenish reserve funds previously used to cover these obligations.

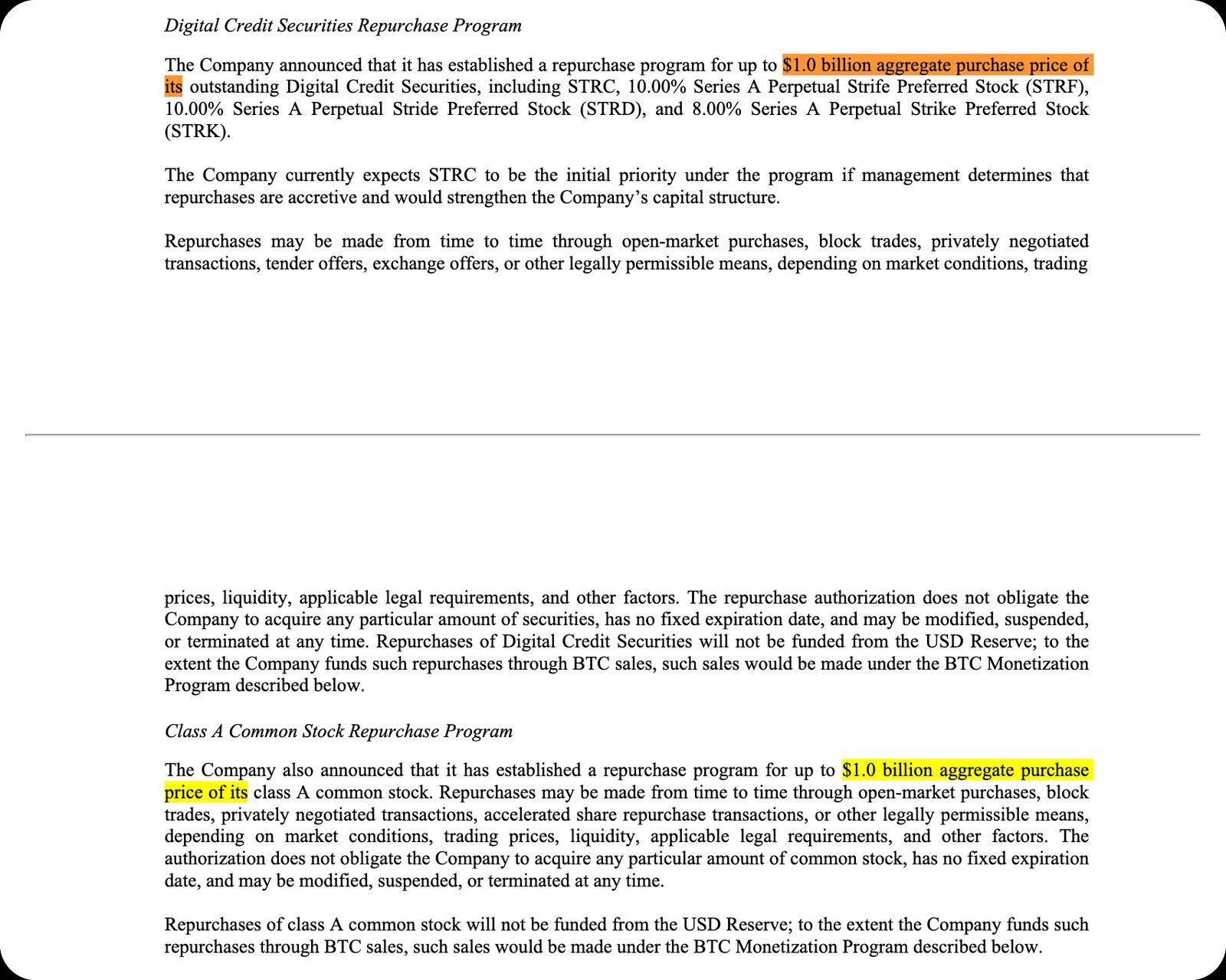

- Third, to Fund buybacks: Sell BTC to repurchase up to $1 billion worth of preferred shares and up to $1 billion worth of MSTR common stock. Additionally, proceeds from BTC sales may also cover related taxes, fees, and other expenses.

At the time, the entire market discussion focused on the $1.25 billion cap for the first funding pool, but the reality is far more complex.

Looking solely at the third pool, it adds an additional $2 billion in potential sales. Therefore, even calculating only the parts with explicit caps, Strategy's currently designed BTC sale plan already exceeds $3 billion. This does not include the funding pool for paying dividends, interest, and replenishing the reserve — for which there is no disclosed cap.

Building vs. Replenishing

This is where it gets truly subtle.

The purpose of the USD Reserve is to pay these preferred share dividends and debt interest obligations. Under the current policy framework, it cannot be used for stock buybacks.

As of June 28th, Strategy's USD Reserve stood at $2.55 billion, sufficient to cover the company's annual obligations of approximately $1.76 billion for debt and preferred shares, providing about 17 months of coverage. The board has set a minimum requirement to maintain 12 months of coverage unless board-approved reductions occur.

This is why the distinction between "building" and "replenishing" the reserve is noteworthy.

- Selling BTC before paying dividends to add cash to the reserve: This is defined as "building."

- Using the reserve to pay dividends, then selling BTC to refill the reserve: This is defined as "replenishing."

The plan treats these as different categories, but they essentially accomplish the same thing — converting BTC into cash to cover preferred share dividends and interest payments.

These details were already disclosed in the documents, but the recent sale made this categorical distinction more apparent. Strategy sold $216 million worth of BTC, using the funds to pay dividends and replenish the reserve, while simultaneously announcing that its $1.25 billion reserve-building capacity remains intact.

Now, the market needs to start understanding Strategy's "proprietary language": "Building" and "replenishing" are essentially accounting classifications, but they determine whether Strategy's BTC sales count against the "public cap" the market sees.

From Hoarding to Active Capital Management

In the June 29th announcement, Michael Saylor stated that this framework reflects Strategy's need for "liquidity, discipline, and active capital management."

Strategy CEO Phong Le was more direct: "Strategy is shifting from a one-way capital issuance model to an active capital management model."

As Matt Walsh and Jeff Dorman from Castle Island explained in a podcast last week, Strategy has essentially evolved into an actively managed hedge fund.

The past Strategy narrative was simple: sell MSTR stock → buy Bitcoin → provide investors with leveraged BTC exposure. But the logic has now changed.

Today, Strategy is buying and selling different components within its own capital structure to manage the pressures between common stock (MSTR), preferred shares, the USD Reserve, and Bitcoin assets (BTC).

This dynamic also introduces new conflicts of interest. Walsh and Dorman pointed out:

- Selling common stock can support preferred share dividends but depress MSTR's premium relative to its underlying BTC holdings.

- Selling Bitcoin can extend the cash runway but further erode the core "never sell" narrative.

- Supporting the preferred share system can maintain market confidence but depletes cash reserves.

- Cutting preferred share dividends can protect liquidity but may cause preferred share prices to crash.

The so-called "reserve loophole" is an embodiment of this shift. Bitcoin is no longer just an asset for Strategy to accumulate; it is becoming a balance-sheet lever used to keep the preferred share system operational.

What We Will Ultimately See

Now, investors must assess Saylor's ability to operate this "machine" — each adjustment to one lever in the capital structure helps one part while potentially threatening another.

This is the most significant takeaway following the July 6th filing disclosure. Strategy is not out of options. It likely has more room to maneuver than what is apparent on the surface.

Don't continue to mistakenly believe that the $1.25 billion cap represents the total ceiling for Strategy's Bitcoin sales.

Today, Strategy has become an institution that the market must relearn to understand. Now, every proprietary term matters more:

- Build

- Replenish

- Issue

- Repurchase

- Defend

Just as Fed watchers parse every punctuation mark in policy statements, the market must also deconstruct every term Strategy uses to gauge what it implies for future BTC sales.

By rolling out this plan, Strategy has secured greater flexibility for itself, but the underlying contradictions persist. This is no longer a simple "leveraged Bitcoin play." It has now become a bet on active capital management prowess.

Can Strategy consistently manage to "sell BTC," "replenish reserves," "issue securities," "repurchase stock," and "maintain the capital structure" without any one action undermining the others?

Personally, I wouldn't want to bet on it.