Original | Odaily Planet Daily (@OdailyChina)

Author|Azuma(@azuma_eth)

At 17 a.m. Beijing time on July 17th, SpaceX originally planned to conduct the 13th test flight of Starship. However, just as the launch countdown entered the final ignition phase, the automatic launch abort sequence was triggered because some Raptor engines failed to start as expected, forcing the cancellation of this test flight.

Elon Musk stated that to ensure a smooth flight, SpaceX will remove and replace two Raptor engines, hoping to make another launch attempt in a few days, with the most likely launch time being early next week.

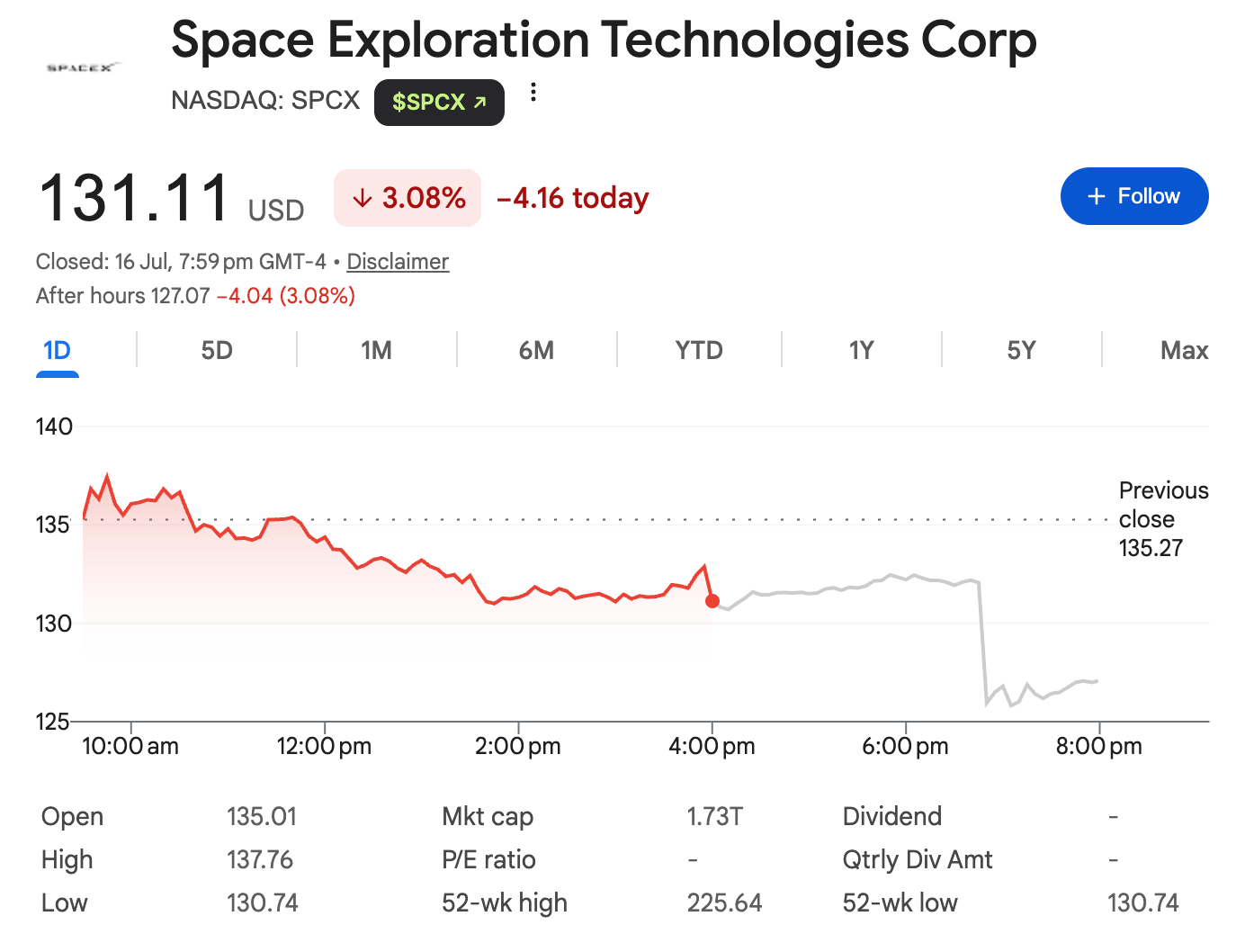

Prior to this test flight, SpaceX's stock price had just fallen below its IPO price, with the maximum decline since listing approaching 40%. As the first Starship test flight after SpaceX's IPO, the market had originally hoped to use it to verify the latest progress of Starship and inject a shot in the arm into the persistently sluggish stock price in recent times. However, the outcome of the launch failure dealt another blow to SpaceX's stock price — SPCX briefly plummeted in after-hours trading, currently reported at $127.07.

A test flight failure is nothing new for SpaceX, but judging from the secondary market's reaction this time, investors are clearly reevaluating a question: After going public, can SpaceX still afford the luxury of "unlimited trial and error"?

Test Flight Failures Are Not New, But Times Have Changed

If we turn the clock back a few years, almost every Starship test flight failure was seen as part of the engineering progress. While discussions in the community about Elon Musk "blowing up rockets" were mainly in a teasing tone, there was also a degree of respect within them.

For SpaceX, the company has always adhered to the Silicon Valley-style R&D philosophy — build fast, test fast, fail fast, and iterate fast. Compared to completing all verification on the ground, SpaceX prefers to send rockets into the sky as soon as possible, obtain data through real flights, and continuously optimize the design. Because of this, in over ten previous Starship test flights, various unexpected events, from in-flight disintegration, booster recovery failures to orbital verification setbacks, have almost run through the entire development history. However, these setbacks have not hindered Starship's continuous forward evolution.

In the era of the primary market, this R&D model also received general recognition from investors. Whether institutional shareholders or employee shareholders, they valued more whether the R&D pace was continuously advancing and whether technological barriers were accumulating, rather than whether a particular test flight succeeded or failed. For them, a failure meant acquiring a new batch of flight data, meant getting one step closer to final commercialization, and essentially still belonged to part of the R&D cost.

But after the IPO, the way the capital market views Starship has begun to change. For secondary market investors, Starship is no longer just an R&D project; it has become an important variable affecting the company's valuation. A test flight setback not only means needing to replace engines and rearrange the launch window but may also imply a delay in commercial deployment timelines, a slowdown in revenue realization, and a readjustment of future cash flow forecasts. In the past, engineers saw data accumulated from a test; now, Wall Street sees whether growth expectations can be met on schedule.

This change does not mean the capital market demands SpaceX "must succeed, must not fail," but rather that every failure will be incorporated into the valuation system for recalculation. Especially against the backdrop of the company already being public and the market assigning a high growth premium, any event potentially affecting the Starship commercialization timeline is more likely to trigger stock price volatility than before.

The IPO: Both Motivation and Constraint

A month ago, SpaceX just completed the largest IPO in human history.

For any capital-intensive, high-investment technology company, the greatest significance of entering the capital market is precisely to obtain more stable and lower-cost financing capabilities. For SpaceX, which is still in a phase of rapid expansion, whether it's continuously building the Starlink constellation, advancing Starship R&D, or laying out a larger commercial space network in the future, it all implies massive capital expenditures. The financing channels brought by the IPO can undoubtedly provide more ample "fuel" for these long-term plans.

But the capital market never provides anything for free. As more and more public investors become shareholders, what SpaceX needs to face is no longer just pure engineering problems, but the capital market's ongoing scrutiny of growth, profit, and the pace of realization.

In the past, Musk could tell investors: "Failure is also part of R&D."

Now, every delay, every launch abort, every test flight incident may quickly be reflected in the stock price, and further affect the company's financing capability, market sentiment, and may even indirectly squeeze management's decision-making space. The capital market inherently pursues certainty, while the greatest characteristic of aerospace R&D is precisely uncertainty. There always exists a difficult-to-eliminate tension between the two.

For SpaceX, going public means both gaining more abundant funds and bearing heavier pressure on its shoulders.

Next Week's Relaunch Is Crucial

Fortunately, this test flight was not a failure after the rocket lifted off (at least it didn't explode), but an active termination of the launch during the ignition phase, making problem localization relatively clear. According to Musk's latest statement, SpaceX will attempt another launch early next week.

For SpaceX's engineers, this might just be another ordinary launch postponement; but for the newly public SpaceX, this relaunch carries significance far beyond mere technical verification.

If the relaunch goes smoothly, market concerns about the Starship R&D pace are expected to ease, and the recently pressured stock price may experience an emotional recovery; conversely, if another unexpected event occurs, SPCX may test even deeper lows.