Original | Odaily Planet Daily (@OdailyChina)

Author | Ethan(@ethanzhang_web3)

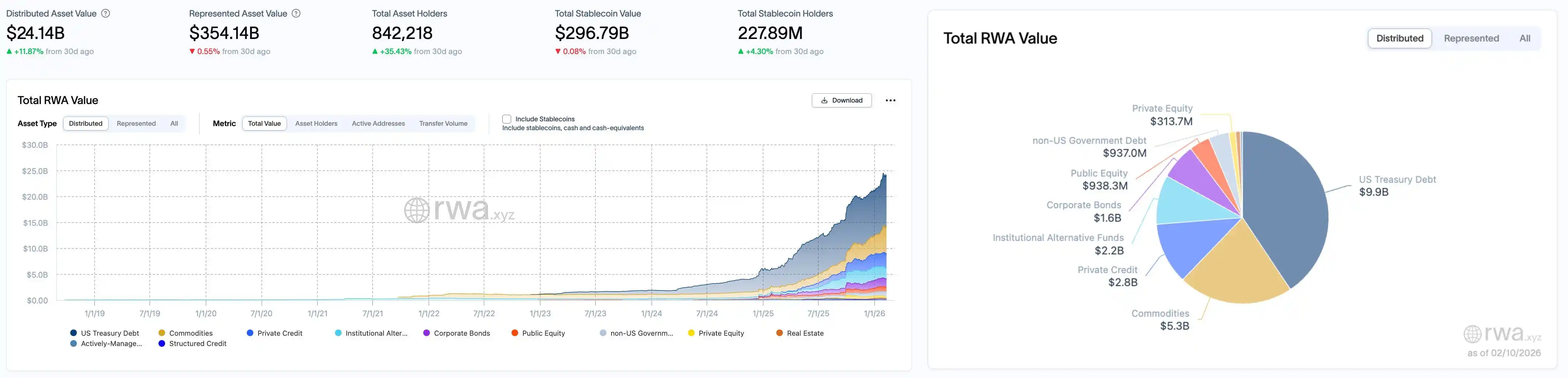

RWA Sector Market Performance

According to rwa.xyz data panel, as of February 10, 2026, the total on-chain value of RWA (Distributed Asset Value) continued to rise, increasing from $23.96 billion on February 3 to $24.14 billion, a weekly increase of approximately $180 million, a rise of about 0.75%. Although the on-chain asset scale did not continue the rapid expansion pace of the previous week, the overall trend remained steadily upward. The Representative Asset Value rebounded this week from $199.42 billion to $354.14 billion, a weekly increase of about $154.72 billion, essentially recovering from the previous temporary decline caused by statistical adjustments.

User-side performance remained strong, with the total number of asset holders increasing from 830,500 to 842,200, a weekly addition of about 11,700 people, an increase of approximately 1.41%. The stablecoin market experienced a slight correction, with the total market capitalization dropping from $310.15 billion to $296.79 billion, a decrease of about $13.36 billion, a drop of about 4.3%; however, the number of stablecoin holders continued to increase, rising from 224.73 million to 227.89 million, an addition of about 3.16 million people.

In terms of asset structure, U.S. Treasury bonds continued to be the core anchor of on-chain RWA, with the scale slightly increasing from $9.6 billion to $9.9 billion, a weekly increase of about $300 million, returning to the historical high range. Commodity assets grew further from $4.8 billion to $5.3 billion, a weekly increase of about $500 million, making it one of the sectors contributing the most to the total volume this week. Private credit continued its moderate expansion, increasing from $2.7 billion to $2.8 billion. Institutional alternative funds saw a slight decline, dropping from $2.3 billion to $2.2 billion.

In the risk asset sector, the scale of corporate bonds and non-U.S. government debt remained largely unchanged, staying around $1.6 billion and $937 million respectively. The public equity sector grew this week from $932.5 million to $938.3 million, showing a recovery trend; while private equity declined further, dropping from $322.1 million to $313.7 million, reflecting the market's continued cautious attitude towards assets with weaker liquidity and longer cycles.

Trend Analysis (Compared to Last Week)

Overall, the total RWA market volume increased steadily this week, but structural rotations persisted. The on-chain distributed asset value continued to rise, and the number of users and stablecoin holders grew simultaneously, indicating that real participation is still strengthening. Structurally, commodities and private credit remain the core directions for absorbing incremental funds. U.S. Treasuries regained allocation after a brief correction, while private equity and some institutional assets continued to face pressure. Market risk preference remains in a range of gentle increase but still rational.

Market keywords: steady expansion, structural rotation, commodities continue to lead gains.

Key Event Review

White House to Hold Another Stablecoin Yield Discussion Meeting Today

Crypto journalist Eleanor Terrett posted on X that insiders revealed the next round of consultations between the White House and cryptocurrency institutions on the issue of stablecoin yields is scheduled for next Tuesday. This meeting will still involve banking staff, but this time, in addition to the banks' own representatives, representatives from various industry associations will also attend.

The specific attendance list will be disclosed later.

Beijing Business Daily: Hong Kong Stablecoin License Review Nears End, Industry Warns of Mainland Regulatory Policy Differences

Beijing Business Daily published an article pointing out that Hong Kong maintains a稳健 (steady/robust) attitude towards stablecoin license issuance, and related review and research work is nearing completion. The industry believes this is a choice combining global stablecoin market risks and the reality of Hong Kong's financial development. However, investors should be clear about the regulatory policy differences between mainland China and Hong Kong regarding stablecoins. It is recommended that investors stay away from various unlicensed stablecoin products domestically and internationally. Furthermore, cross-border participation in Hong Kong's licensed stablecoin-related businesses must comply with mainland foreign exchange, cross-border transaction regulations, and other relevant regulatory provisions,警惕 (be vigilant against) market hype leading to irrational investment risks and avoid blindly participating in related trading activities.

People's Bank of China and Seven Other Departments Issue Notice on Further Preventing and Disposing of Risks Related to Virtual Currency, etc.

The People's Bank of China and seven other departments issued a notice on further preventing and disposing of risks related to virtual currency, etc., which states: Virtual currency-related business activities are illegal financial activities. Virtual currency-related business activities conducted within China, including exchange business between legal tender and virtual currency, exchange business between virtual currencies, acting as a central counterparty to buy and sell virtual currency, providing information intermediary and pricing services for virtual currency trading, token issuance financing, and trading of virtual currency-related financial products,涉嫌 (are suspected of) illegal issuance of token tickets, unauthorized public issuance of securities, illegal operation of securities and futures businesses, illegal fundraising, and other illegal financial activities. All such activities are strictly prohibited and resolutely banned according to law. Overseas units and individuals must not provide virtual currency-related services to entities within China in any illegal form. Stablecoins pegged to legal tender, in their circulation and use,变相履行 (perform in a disguised form) some functions of legal tender. Without approval from relevant departments according to laws and regulations, any domestic or overseas unit or individual must not issue stablecoins pegged to the Renminbi overseas. Without approval from relevant departments according to laws and regulations, domestic entities and their controlled overseas entities must not issue virtual currency overseas.

White House Advisor and Former House Financial Services Committee Chairman: Crypto Market Structure Bill Could Pass Before End of May

White House Advisor Patrick Witt and former House Financial Services Committee Chairman Patrick McHenry stated during an interview with CoinDesk Live at the Ondo Summit that a comprehensive crypto market structure bill could pass within months. Patrick McHenry predicted the bill could be sent to the President for signing before May 25. Patrick Witt said that after the passage of the Genius Act, Trump has prioritized this legislation. The White House is currently mediating core disagreements such as stablecoin yields. Consensus has been reached on aspects like prohibiting false宣传 (promotion/propaganda), but disputes remain over whether centralized exchanges should be allowed to pay yields on idle stablecoins. Patrick McHenry emphasized that DeFi is the core of the market structure legislation, and its decentralized nature is the source of cryptocurrency efficiency and transparency. The drafting team has now entered the stage of specific legal text negotiations, and the Senate may take action before the Easter recess in April.

Caixin: Foreign Debt RWA to be Regulated by NDRC, Equity and Asset Securitization RWA to be Regulated by CSRC

Caixin Web published an article "Chinese Government Allows Domestic Assets to Issue RWA Overseas, Regulatory Framework Announced", which pointed out: The issuance of RWA (Real World Asset tokenization) by Chinese domestic assets overseas will no longer be a grey area. Regulatory authorities believe that foreign debt RWA, equity RWA, and asset securitization RWA should be regulated according to the principle of "same business, same risk, same rules", referring to the traditional financing businesses corresponding to these three situations for依法依规 (law-based and regulation-based) supervision. Therefore, foreign debt RWA will be regulated by the National Development and Reform Commission (NDRC); equity RWA and asset securitization RWA will be regulated by the China Securities Regulatory Commission (CSRC). Like traditional overseas financing businesses, overseas RWA also involves the repatriation of funds raised overseas to China, which will be regulated by the State Administration of Foreign Exchange (SAFE). Other forms of RWA will be regulated by the CSRC in conjunction with relevant departments according to their职责分工 (division of responsibilities).

In short, foreign debt RWA, equity RWA, asset securitization RWA, and other forms of RWA. The first three correspond to traditional overseas financing businesses where corporate foreign debt requires审核登记 (examination and registration) by the NDRC, stock issuance requires "exchange review, CSRC registration", and asset securitization requires exchange review. All other situations besides these three are categorized as the fourth type.

Tether Invests $150 Million in Gold.com, Boosting Tokenized Gold Distribution

Stablecoin issuer Tether announced a $150 million investment to acquire approximately a 12% minority stake in Gold.com to expand the distribution channels for its gold-pegged token XAUT. The two parties plan to integrate XAUT into Gold.com's infrastructure and explore using USDT and its newly launched US-compliant stablecoin USAT to purchase physical gold. Driven by rising gold prices, the tokenized gold market size has exceeded $5 billion, with XAUT accounting for over 60% of it. Additionally, Tether announced an investment in Anchorage Digital to support the compliant推进 (advancement) of USAT in the United States. (CoinDesk)

Pharos Network Launches Over $10 Million RealFi Incubation Program with Hack VC Participation

Pharos Network announced the launch of a builder incubation program called "Native to Pharos" with a fund size of over $10 million. The program aims to accelerate innovation in its on-chain financial ecosystem, focusing on the intersection of real-world assets (RWA), DeFi, and blockchain infrastructure.

This incubation program is supported by partners including Hack VC, Draper Dragon, Lightspeed Faction, and Centrifuge. Participating projects will receive technical guidance, strategic advice for product launch and scaling, and support from networks of investors and ecosystem partners. Pharos Network is a RealFi Layer 1 blockchain developed by former Ant Group executives and engineers. The program is now open for applications, and the first recruitment event will be launched in Hong Kong.

Startale and Japanese Financial Giant SBI Holdings Plan to Launch Strium, a Layer 1 Blockchain Focused on RWA and Tokenized Securities

Startale Group and Japanese financial giant SBI Holdings publicly announced Strium Network (Strium), a Layer 1 platform focused on trading tokenized securities and real-world assets (RWA). As the core product of their joint venture, Strium aims to build the trading layer infrastructure for Asia's on-chain securities market, supporting 24/7 spot and derivatives trading to address the limitations of traditional markets in issuance and custody.

Currently, the platform's proof-of-concept (PoC) is ready, focusing on verifying its settlement efficiency and interoperability with traditional financial systems and blockchain networks. Strium plans to launch a testnet this year and leverage the customer base of the SBI Holdings ecosystem to promote the on-chain development of institutional-grade capital markets.

ETHZilla Launches RWA Token for Aircraft Engine Cash Flow

Nasdaq-listed company ETHZilla (ETHZ) announced it will launch Eurus Aero Token I this week, splitting the monthly cash flow generated from leasing aircraft engines through tokenization to provide investors with on-chain yield exposure.

The token is issued by subsidiary ETHZilla Aerospace, with the related assets being two commercial aircraft engines leased to a "leading U.S. airline". Token holders will receive monthly cash flow distributions from basic rents and usage fees generated by the underlying assets through ERC-20 tokens.

ETHZilla is supported by Peter Thiel's Founders Fund. The company was previously known for its Ethereum reserve strategy but has gradually shifted towards real-world asset (RWA) tokenization since last year. Previously, the company completed a trial tokenizing assets comprising 95 housing loans.

As the blockchain industry accelerates the onboarding of traditional assets, RWA is seen as one of the fastest-growing sectors. Ark Invest estimates that the tokenized asset scale could reach $11 trillion by 2030, while the current market size is approximately $22 billion.

Vitalik: Algorithmic Stablecoins are the True DeFi

Vitalik Buterin posted on platform X, stating that algorithmic stablecoins belong to the true DeFi. He believes that if there were high-quality algorithmic stablecoins with ETH as the underlying asset, even if the vast majority of liquidity is supported by CDP holders of negative algorithmic dollars, the ability to transfer counterparty risk to market makers is an important characteristic. Even if algorithmic stablecoins are backed by RWA, if they can ensure sufficient collateral through over-collateralization and diversification in case of a single RWA failure, it would be an effective improvement in risk characteristics for holders. He pointed out that the industry should develop in these directions and gradually move away from using the US dollar as the unit of account,转向 (shifting towards) a more通用 (universal/general) diversified index. Furthermore, the current operation of depositing USDC into Aave does not fall into the above categories.

Kyle Samani Responds Intensively to Community Concerns: No Return to Multicoin, Ethereum Has No Advantage in RWA

After announcing his departure from Multicoin Capital, Kyle Samani responded intensively to community concerns on platform X. Dragonfly managing partner Haseeb said his departure was like Jordan leaving the Bulls, to which Kyle Samani responded, "Won't be returning to the Bulls,"暗示 (implying/hinting) he would not return to Multicoin Capital. He also stated he would support Solana's rapid development and said that besides stablecoins, Ethereum has no obvious advantage in RWA;相反 (on the contrary), Solana has already achieved significant leads in payments, applications, and DePIN.

Hot Project Dynamics

Ondo Finance (ONDO)

One-sentence introduction:

Ondo Finance is a decentralized finance protocol focused on structured financial products and the tokenization of real-world assets. Its goal is to provide users with fixed-income products, such as tokenized U.S. Treasury bonds or other financial instruments, through blockchain technology. Ondo Finance allows users to invest in low-risk, highly liquid assets while maintaining decentralized transparency and security. Its token, ONDO, is used for protocol governance and incentive mechanisms. The platform also supports cross-chain operations to expand its application within the DeFi ecosystem.

Latest developments:

February 7: Bloomberg senior ETF analyst Eric Balchunas stated on platform X that 21Shares is applying to launch an Ondo ETF.

February 3: Ondo Finance stated in an official website post that Ondo Global Markets has confidentially submitted a registration statement to the U.S. Securities and Exchange Commission (SEC). Once effective, this filing will provide global investors with issuer-level信息披露 (information disclosure) that meets SEC standards.

MSX (STONKS)

One-sentence introduction:

MSX is a community-driven DeFi platform focused on tokenizing U.S. stocks and other RWAs for on-chain trading. Through a partnership with Fidelity, the platform achieves 1:1 physical custody and token issuance. Users can use stablecoins like USDC, USDT, USD1 to mint stock tokens like AAPL.M, MSFT.M, and trade them 24/7 on the Base blockchain. All trading, minting, and redemption processes are executed by smart contracts, ensuring transparency, security, and auditability. MyStonks is committed to bridging the gap between TradFi and DeFi, providing users with a high-liquidity, low-barrier entry to on-chain U.S. stock investment, building the "Nasdaq of the crypto world".

Developments:

Previously, Maiton MSX announced that starting immediately, it would change the fee collection model for RWA spot trading. After the adjustment, this section changed from the original "two-way fee" to a "one-way fee". The specific execution standard is that the buy side will maintain a 0.3% handling fee, while the sell side handling fee is reduced to 0. This means that when users complete a full trading cycle of "buy + sell", the comprehensive transaction cost will be substantially reduced by 50%. This fee policy is now effective across the entire MSX platform, covering all listed RWA spot trading pairs.

Additionally, Maiton MSX published a 2025 review article "Anchored in the Era Window, Co-building a New On-Chain U.S. Stock Ecosystem", reviewing the phased achievements of this year.

Related Links

《RWA Weekly Report Series》

《Does Kyle Samani's Exit Have Hidden Reasons?》

《Web3 Lawyer Interpretation: New Regulations from 8 Departments Landed, RWA Regulatory Path Officially Clarified》