Author: Yu Shiyi

The parent company of the NYSE, ICE, BlackRock managing $11 trillion in assets, and Apollo, a top global alternative asset manager. Over the past decade, these three institutions have gone from cold to watchful to cautiously participating in on-chain assets, but their involvement was always through investing in company equity, never directly touching Tokens.

But recently, they broke their own rule.

They directly purchased ARC issued by Circle, with a pre-sale total of $222 million at a $3 billion valuation. If they were only optimistic about Circle as a company, logically, they would just need to buy the stock. Choosing ARC indicates they see something beyond just the stock.

On the same day, Circle released its Q1 2026 earnings report. CRCL jumped from 105 to 126 intraday before settling back to 115, with a single-day swing exceeding 20%, later closing around 130. A $30 billion market cap company experiencing such volatility indicates the market hasn't quite figured out: How should Circle be valued?

I haven't written about this project for a long time. Today, I will share my thoughts on some significant and crucial questions.

This is article 21 of the "AI Investment Map" series. Full text is 8000 words. It is recommended to forward or bookmark before reading. Recommending to set this account as a "Starred Account".

I. Two Faces in the Earnings Report

The data in the earnings report is clear, but the ambiguity lies in its presentation of two faces.

(I) One Face is All Growth

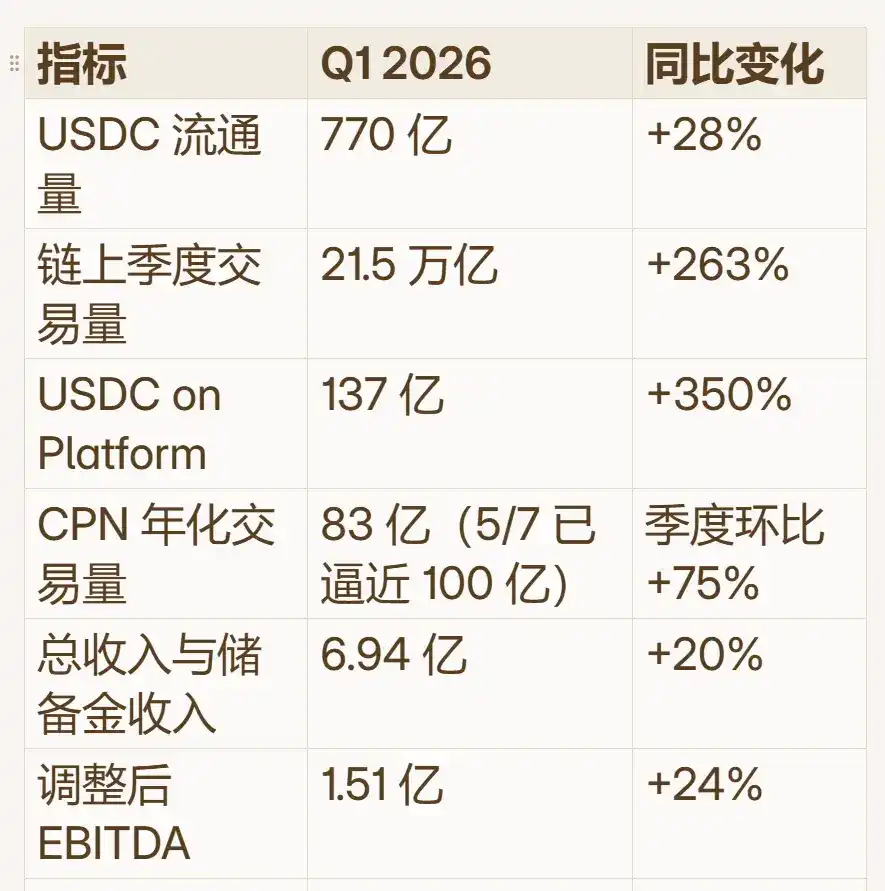

Details as shown in the chart below:

Metric Q1 2026 Year-over-Year Change USDC Circulation 77.0 Billion +28% On-chain Quarterly Transaction Volume 21.5 Trillion +263% USDC on Platform 13.7 Billion +350% CPN Annualized Transaction Volume 8.3 Billion (Approaching 10 Billion as of 5/7) Quarterly Sequential +75% Total Revenue & Reserve Revenue 694 Million +20% Adjusted EBITDA 151 Million +24%

Let's discuss three sets of numbers separately.

1. Massive On-chain Transaction Volume

USDC on-chain quarterly transaction volume of 21.5 trillion. The amount of value transferred on-chain by USDC in a single quarter is already close to the annual GDP of the United States.

Comparison with giants:

- Visa's total processed volume for fiscal year 2025 was approximately $17 trillion, over 230 billion transactions, with an average value per transaction around $80.

- SWIFT processed about $150 trillion annually, with around 11 billion messages.

USDC's single-quarter volume of $21.5 trillion exceeds Visa's annual volume, but these are not the same type of flows—Visa's $17 trillion comes from 230 billion small-value consumer transactions piled up; USDC's $21.5 trillion is primarily composed of large, low-frequency on-chain fund transfers, flows between DeFi protocols, market maker repricing, institutional fund allocations, with average values potentially in the thousands to tens of thousands of dollars. The amount is huge, but the number of transactions is not yet in the same world as Visa.

However, the scale of 21.5 trillion and the 263% growth rate roughly indicate that the 77 billion in circulation was moved about 28 times within a quarter. This means it is truly a transactional currency being used on-chain, not just a digital number sitting in a cold wallet.

2. CPN Growth Rate is a Key Variable

In the 21.5 trillion on-chain flow mentioned earlier, Circle currently earns almost nothing. Because USDC is an open protocol, on-chain transfers are free; Circle can only earn reserve interest, not take a cut from the transactions themselves. CPN is a gated payment and settlement network built by Circle. Financial institutions join and use CPN for cross-border payments, and CPN charges a network service fee per transaction, calculated in basis points (covering compliance, routing, settlement infrastructure costs).

Currently, CPN annualized transaction volume has just passed 10 billion, with a penetration rate of less than 0.05% compared to the total on-chain volume. This gap itself represents potential. CPN's quarterly sequential growth of 75%; for a payment network just starting, such acceleration indicates real demand.

If CPN succeeds, Circle will earn money "from the usage of USDC," and this money will have higher retention and better economic quality.

3. Rapid Growth of USDC on Platform

In the chart, there is a category called USDC on Platform, referring to USDC deposited on Circle's own platform. This portion's growth rate surged from 5.7% to 17.2%, nearly a threefold increase. Importantly, like CPN, this portion does not require sharing revenue with Coinbase; it primarily captures reserve interest. The more revenue that flows through Coinbase, the greater Circle's valuation space becomes.

(II) The Other Face is All Constraints

Look at these three data points; this should be the reason for the initial drop after the earnings release:

- GAAP net profit is only 55 million. A company managing 77 billion in reserves only earns 55 million in a quarter.

- Reserve yield is 3.5%, down 66 basis points from the same period last year; interest rates are trending downward.

- Operating expenses are 242 million, a sharp increase of 76% year-over-year, mainly due to rising equity incentive costs post-IPO.

Reserve revenue still accounts for 94% of total revenue, but this 694 million figure is lower than the previous consensus estimate of 715 million. In general: earning less, spending more, thinner profits.

The market is divided into two camps:

One camp believes it's merely an interest machine. A popular saying is "Buying it is worse than buying Coinbase." Interest income is literally taken away by more than half, and contract changes seem distant. Previous articles have explained why the share exists, mainly because when Circle was near collapse, Coinbase acted as a white knight to save it, but also somewhat took advantage, and Circle signed what could be seen as a binding agreement. Moral judgment is meaningless; commercially, once the terms are signed, the initiative to change them later lies with Coinbase.

The other camp believes this is the future on-chain financial infrastructure; one shouldn't focus on reserve interest and sharing, but rather look at CPN, the ARC chain, etc., seeing the embryonic form of a financial operating system.

If seen as an interest machine, 30 billion is overvalued; if seen as a financial operating system, 30 billion at present is also quite reasonable.

However, I believe Circle's valuation must be evaluated multidimensionally because its different business segments have clearly distinct valuation logics. Therefore, this article will establish a three-dimensional valuation framework for reference.

II. The Three-Dimensional Perspective of Circle

The capital market's pricing of a company essentially chooses a frame of reference for it, i.e., comparing it to different business models.

(I) Interest Business: Reference Banks

USDC circulation is its deposits, the US short-term interest rate is its interest spread, and the distribution agreement is its payout cost. Under this frame of reference, if forced to compare to banks, one might assign a P/E ratio of 8-15x. It is sensitive to interest rates and competition. But Circle is actually much better than a bank. Using banks as a comparison gives a sense of a robust safety margin, knowing that at this price, it's already very low. Details will be expanded later.

(II) Payment & Settlement: Reference VISA, etc.

USDC is its settlement asset, CPN is its settlement network, and the take rate is its revenue. Under this frame of reference, for example, Visa and Mastercard valuations are around 24-30x forward P/E, enjoying the compound growth of global payment volumes.

(III) ARC Network: Reference Infrastructure

Arc is its execution layer, ARC is the coordination asset, and USDC is the gas currency. Under this frame, there is no standard valuation. One can roughly reference the Ethereum network's value, the network effect premium of Visa's early IPO, or consider it more as option pricing. The official whitepaper was released on May 11th, containing many crucial details we will discuss later.

These three dimensions correspond to different valuation systems and play different roles in our actual investment practice, as understood in the table below.

Dimension Corresponding Business Valuation Logic Role in Market Cap 1st Dimension Reserve Interest Income Interest-Sensitive Net Profit Multiple Determines the Floor 2nd Dimension Other Revenue & CPN Platform-Type Revenue Multiple Determines the Turning Point 3rd Dimension Arc Network & ARC Token Ecosystem Option Value Determines the Future

Let's break them down one by one.

III. First Dimension: Reserve Interest and Sharing

Circle's most well-known revenue method is simple: users hold USDC, backed by real US dollar reserves. Circle invests these dollars in US short-term Treasuries and repo agreements, earning the Treasury yield. In Q1 2026, this business brought in 653 million in reserve revenue, annualized at approximately 2.6 billion.

Average USDC circulation was 75.2 billion, implying a reserve yield of 3.47%. This is the "floor" of Circle's valuation. No matter how Arc and CPN evolve, as long as USDC is circulating, this business is certain.

Determining the appropriate P/E or valuation multiple for this business is subjective. Simply put, comparing it to banks undervalues it, while comparing it to SaaS overvalues it. The reference content below allows for a rough estimation. A vague correctness is better than precise error.

(I) Circle is Not a Bank, Nor is it SaaS

Circle does not have a traditional banking charter (though it's applying for an OCC national trust bank charter). It does not make loans, does not bear credit risk, has no duration mismatch, and does not need to meet capital adequacy ratios. Its asset side consists solely of US Treasuries, repos, and money market funds, with near-zero "credit risk."

This makes it much cleaner than banks.

On the point of whether it's a bank, I think the valuation consideration is simple: The worst-case scenario is to compare it to a bank, giving it a 10x P/E. But in reality, compared to banks, Circle's business model, even just for "earning interest," is far superior.

Banking is a tough business. You take depositors' money and lend it out, bearing the risk of principal loss. For instance, as a bank president, you lend money to Xu Jiayin (Evergrande), lend money to NIO, all in hot sectors, but the money can't be recovered soon—and this tough business doesn't earn much because, despite taking huge risks, you only earn a small interest spread.

Circle earns nearly all the interest with virtually no risk to principal.

However, Circle's model also shouldn't be priced like SaaS (Software-as-a-Service), which often receives high valuations due to stickiness, sustainability, high certainty, and pricing power. In contrast, Circle's reserve yield is not priced by Circle but by the Federal Reserve. Moreover, a significant portion of USDC "users" are not Circle's direct customers—they use USDC indirectly through Coinbase, DeFi protocols, third-party wallets, the Base chain, etc.

Circle owns the USDC network but does not always own the end-customer relationship.

It shouldn't be priced like SaaS, but is it worse than SaaS? Opinions vary. From my personal perspective, I believe Circle's business model is one of the best ever: this is the first time in history private entities have partially captured "seigniorage."

A monkey comes to a tree, stands upright, enabling its transformation from monkey to human.

(II) The Competitive Moat of Stablecoins

Reserve interest revenue is so lucrative, can't competitors beat it by offering rebates or interest? For ordinary financial products, this logic holds. But stablecoins are not ordinary financial products.

When you send someone USDC, the recipient is usually willing to accept it—because wallets support it, exchanges support it, on-chain protocols support it, liquidity is good, conversion is convenient, and trust is high. But if you send someone a new stablecoin, the recipient first needs to check if their wallet supports it, where to exchange it, if it might depeg, if there's liquidity.

These frictions are USDC's moat.

The core competitiveness of a stablecoin is not "whose interest rate is higher," but "when money flows from A to B, will B accept it without friction, and be able to use it conveniently everywhere?" Security, redeemability, liquidity, wallet and exchange support, enterprise acceptance, regulatory compliance, on-chain integration—all these ultimately form the moat.

I previously wrote an article on why PayPal, with so many users and issuing subsidies, couldn't surpass Circle with its stablecoin, still stuck at 30 billion after so long? Because users on its platform move in when interest is offered and move out when it's not, and when making payments, they don't care what's backing it. Also, examples like USDC-1, relying on subsidies to grow, ultimately plateaued at a 40 billion market cap.

New stablecoins relying on subsidies all face the same fate: when subsidies stop, growth hits zero. The time window for new challengers is narrowing.

(III) The Inevitable Rate Cuts

Q1 reserve yield was 3.5%, down 66 basis points from 4.16% a year ago. The reason is no surprise: US short-term rates have been declining over the past 12 months following Fed rate cuts.

Declining interest rates mean less revenue for the same USDC volume, that's certain. But there's another variable: the larger USDC becomes, the more money Circle manages; the higher the interest rates, the more each unit of money earns. The product of the two determines real profitability.

In the earnings report, USDC circulation grew 39% year-over-year, so reserve revenue still grew 17%. Although the incremental gain was halved by falling rates, if USDC growth continues, the rate cut factor is observable and somewhat controllable.

Therefore, Circle is not purely the "central bank of on-chain dollars," because it only captures part of the "seigniorage," and central banks don't rely on US short-term rates for income; Circle does.

Circle is more like a good sailboat: it goes fast when the wind is strong, but the wind wasn't invented by the captain.

(IV) Coinbase Revenue Share

1. Three-Tier Share

Circle's total revenue in Q1 was 694 million. Looking just at the reserve portion, the Net Reserve Margin retention rate is only 38%, a large chunk taken by Coinbase's share and other costs. For every 1 dollar of interest Circle's "interest-earning machine" makes, only 38 cents is its own.

Specifically, Coinbase's share is taken in three tiers, in order:

First, issuer retention. Circle first takes a certain number of basis points on USDC circulation as issuer retention. The prospectus disclosed a rate range from low double digits to high single digits (roughly 0.05%-0.15%), decreasing as circulation increases. Based on the current 77 billion circulation, this amount is roughly in the tens of millions of dollars annually. Not huge, but it's money Circle takes before any sharing begins.

Second, platform split. For portions on the Coinbase platform, it all goes to Coinbase; for portions on Circle's own products (Circle Mint, Gateway, Wallets), it goes to Circle.

Third, residual distribution. For USDC in third-party scenarios—DeFi, other exchanges, third-party wallets—generating reserve revenue, Coinbase also takes 50%.

Overall, this is a massive and ongoing expense. The revenue-sharing agreement was signed in August 2023, with an initial term of three years, expiring in August 2026. If both parties fulfill their obligations and no modifications are reached, it automatically renews for another three years. Coinbase recently stated this is a permanent, non-terminable contract. Legally speaking, to change the contract in the future, either Coinbase fails to meet its obligations under the agreement, or new regulations give Circle leverage to renegotiate. In short, this portion is currently in a "status quo for now" position. The next six months will be a critical window: renegotiation period approaches, and how the "CLARITY Act" lands will determine how and what the two parties negotiate.

2. Revenue Share Isn't Necessarily Bad

This sharing also has returns. Coinbase is not just the "blood-sucking" party taking a share; it is also USDC's most important distribution network, bringing liquidity, user entry points, trading scenarios, Base ecosystem, institutional reach, and brand endorsement.

Without Coinbase's channels, USDC couldn't have grown from zero to 77 billion in circulation. Coinbase eats USDC's economics but also helps USDC scale.

Newcomers to the stock market might find this sharing repulsive, psychologically hard to accept. But in reality, scaling a business typically can't rely on "eating alone." This is common in business models: Taking Visa and Mastercard as familiar examples, for every dollar of revenue, Visa only earns about 10%, while banks take the lion's share (around 85%), and various POS and network parties take a bit more.

So, Visa and Mastercard get shared much more heavily than Circle, yet it doesn't stop them from becoming multi-hundred-billion-dollar companies.

Every app we download from a mobile app store or every in-app purchase we make gets a 15-30% cut taken by Apple and Google. For instance, Apple in China originally took 30% from most apps, reduced to 25% in 2026. It doesn't stop the emergence of mobile app giants.

3. Growth Beyond Sharing

For Circle, rather than debating when it can share less with partners, the focus should be: Can areas outside Coinbase's share grow vigorously?

The data already shows signs. The proportion of USDC on Platform is rising. The daily weighted average share increased from 5.7% a year ago to 17.2%. This means the portion Circle keeps for itself is accelerating. Q1 retention rate increased 1.5 percentage points year-over-year and 1.3 percentage points sequentially, already reflecting this trend.

Other Revenue, CPN, Managed Payments, Agent Wallets, Agent Marketplace, Arc fee capture in the current revenue structure will become sources exempt from sharing for Circle.

(V) Regulation Might Actually Protect Circle

Currently, two relevant bills are long-term protections and positives for Circle.

1. The "GENIUS Act" Has Been Enacted. Signed into law in July 2025, it's the first federal framework targeting payment stablecoins in the US. Section 4(a)(11) explicitly prohibits: Stablecoin issuers shall not pay any form of interest or earnings to stablecoin holders (whether in cash, tokens, or other consideration), as long as such payment is based on holding, using, or retaining the stablecoin itself. The effective date is January 18, 2027.

The current issue is that everyone is indirectly paying interest. For example, Circle, through its partnership with Coinbase, lets Coinbase pay it; USDC-1 uses similar logic, paying through Binance.

Thus, the second bill aims to ban this indirect payment.

2. The "CLARITY Act" Is Still Under Negotiation. It's a broader digital asset market structure bill. The core unresolved issue it addresses is that the GENIUS Act did not explicitly prohibit "affiliates or third parties" from paying interest-like rewards to holders.

The 20% single-day drop in CRCL on March 24th was the market interpreting an early draft of the CLARITY Act as intending to extend the ban thoroughly to affiliates and third parties. However, looking at the bill's evolution, the outcome might be much milder than the initial panic. It's expected to be announced soon.

Another parallel regulatory line is also progressing. The GENIUS Act only prohibits issuers from directly paying interest to holders. However, the OCC's proposed rule in February goes further: If an issuer shares reserve earnings with an affiliate, and the affiliate then transfers "rewards" to holders, the OCC presumes you violated the rule, and you must prove your innocence. This is exactly what Coinbase is currently doing. But since this rule is still in the proposed stage, the final rule is expected mid-2026, and the GENIUS Act overall takes effect no later than January 2027. If implemented, Coinbase's rewards will also have to adjust.

However, the CLARITY Act legislation and OCC rule have different legal authority. Currently, the CLARITY Act is also discussing this interest payment issue, so once the CLARITY Act defines it clearly, the OCC will likely follow suit.

Interestingly, Circle and Coinbase previously held different stances on the relevant bills:

- Circle's CEO and policy head publicly praised the OCC's rule. Because if Coinbase can no longer pass on the share to users, the share percentage Circle pays Coinbase might have room for negotiation in the future. Coinbase's biggest selling point for attracting users to hold USDC would be weakened.

- Coinbase publicly opposed it, submitting objections to the OCC, arguing such rules harm consumers.

3. Impact on Circle's Reserve Business

The outcome isn't finalized, but the direction can be preliminarily inferred: Passive holding earning interest will be compressed, regardless of method—it's just a matter of how much space is compressed.

Personally, I speculate this path won't be completely blocked as banks might wish. Previously, I wrote three points about the nature of compliant dollar stablecoins:

Stablecoins are the second growth curve for the US dollar and US Treasuries.

It's a top-tier business model that, for the first time in history, allows sharing part of seigniorage.

The US government is the greatest driving force behind compliant stablecoins.

Starting from these three points, I have considerable confidence that regulations won't reverse course at the institutional level. Additionally, it's worth noting these two bills are among the few jointly advanced by both US political parties; even if the administration changes later, the direction will likely remain.

The essence of stablecoin growth is ultimately aligned with maximizing the US dollar's interests.

However, regardless of how the regulations land, stricter or looser. It's good for maintaining Circle's moat. If stricter, competitors cannot rely on spending money to grab market share (though currently, spending hasn't worked anyway). Competition returns to harder-to-replicate factors—security, compliance, redemption network, wallet coverage, enterprise integration, on-chain integration, liquidity depth.

Furthermore, looking at the two bills currently, they essentially lock out any chance for USDT to make a comeback, because Circle's compliance advantages and infrastructure are all Tether's weaknesses.

IV. Second Dimension: New Hope in Three New Businesses

Reserve revenue is "money from interest rates," money from the government, money that gets shared. In contrast, Other Revenue is money Circle earns from its own products and platform capabilities, money that doesn't need to be shared.

Q1 2026 Other Revenue was 42 million, doubling from 21 million a year ago. The company's FY2026 full-year guidance is to earn 150-170 million, nearly 100% annual growth. The absolute value is still small, only 6% of total revenue, but the significance of this line far exceeds its current size.

(I) "Other Revenue" Has a High Ceiling

According to the prospectus, Other Revenue comprises three segments:

- Transaction Services (processing stablecoin payments, payments to sellers/suppliers/end-users, ledger management, auxiliary digital asset transactions)

- Integration Services (implementation services for integrating stablecoins into public blockchains)

- Other Services (USYC management-related fees, stablecoin redemption fees, cross-chain transfer fees, developer services, etc.)

These three segments are revenue generated by Circle's own products and platform capabilities, no longer needing to be shared, only requiring deduction of associated costs like compliance. It differs from reserve revenue in several key aspects:

First, it's not interest-rate dependent. Reserve revenue is closely tied to interest rate levels, while Other Revenue growth is almost entirely driven by products and customers. This business can grow even during a rate-cutting cycle, providing Circle with counter-cyclical profit quality.

Second, it has a higher ceiling. Reserves are an interest-based business. While currently the revenue pillar, interest rates have an upper limit. Payment networks, enterprise services, AI agent payments—these are markets with open ceilings. Visa's market cap of around 590 billion is the result of payment network compounding effects.

Third, it's closer to a service fee. This part resembles SaaS-type revenue, with purer characteristics, more sustainable growth, and a higher ceiling.

For such high-growth services, P/E valuation isn't typically used. Maotai, Apple, Pinduoduo can use P/E fine—looking at how much money the company has, yearly profit, market cap, and a rough number emerges. But for Circle in this area, Price-to-Sales (P/S) can be used. Based on FY2026 guidance of 1.5-1.7 billion, at 10-20x P/S, it corresponds to roughly 1.5-3.4 billion in valuation.

It's still small now, but it's the seed for a change in valuation logic.

(II) CPN: Large Transaction Volume ≠ Large Revenue

CPN is the Circle Payments Network, the company's global payment network. Its narrative is challenging SWIFT, enabling 24×7 on-chain dollar clearing.

Q1 data: Annualized transaction volume 8.3 billion (based on the last 30 days of March annualized), quarterly sequential growth 17%. As of May 7th, nearing 10 billion, quarterly sequential growth 75%. Participating financial institutions 136, quarterly sequential growth 36%. In April, Managed Payments product launched, packaging the entire infrastructure for traditional banks and payment service providers.

8.3 billion sounds significant. But for payment networks, you can't just look at transaction volume. Corporate payments, cross-border settlements, institutional fund flows often have large single amounts but potentially very low take rates. What truly matters for a payment network is: Transaction Volume × Take Rate = Revenue.

Annualized Transaction Volume 5 bps Revenue 10 bps Revenue 20 bps Revenue 8.3 Billion (Current) 4.2 Million 8.3 Million 16.6 Million 50 Billion 25 Million 50 Million 100 Million 100 Billion 50 Million 100 Million 200 Million 500 Billion 250 Million 500 Million 1 Billion 1 Trillion 500 Million 1 Billion 2 Billion

At a 5-20 basis point take rate range—common for payment networks, with cross-border payments on the higher end, pure on-chain settlement on the lower end—CPN's current annualized transaction volume contributes revenue roughly between 4 million and 17 million.

At the current scale, CPN is not yet a profit mainstay.

But it is a key validation metric for Circle's platformization. If CPN reaches a trillion dollars in annualized transaction volume within three years, a 10 bps take rate corresponds to 1 billion in revenue; if it reaches ten trillion dollars, it corresponds to 5-20 billion in revenue. That's when CPN can truly change Circle's valuation structure. Of course, we still need to see what the eventual take rate will be. It's still early.

Based on the near 10 billion annualized volume as of May 7th and 75% quarterly growth, it's not unlikely for CPN to reach 20-30 billion within a year. At that point, the market would have reason to redefine it from a "narrative project" to an "early-stage monetizing payment network."

(III) AI Agent Toolstack: Awaiting an Entry Point for "AI Economic Activity"

Another underrated release in the Q1 earnings was the AI Agent Toolstack.

It includes command-line tools (Circle CLI), Agent Wallets, Agent Marketplace, and Nanopayments. Nanopayments support minimum transaction amounts of 0.000001, i.e., one-millionth of a dollar.

The existence of such payment granularity indicates it's not for humans but for AI agents. If AI agents calling each other's APIs, purchasing services from each other, and settling among themselves truly become mainstream in the next decade, then "machine-to-machine stablecoin payments" will be a brand new market. Stablecoins are naturally suited for this scenario: on-chain, low fees, programmable, 24×7, cross-border.

The AI Agent Toolstack currently has no quantifiable revenue contribution; it's pure optionality. But it complements Arc. Arc is the settlement layer; the AI Agent Toolstack is the application layer entry point. Viewed together, the logic becomes complete.

V. Third Dimension: Arc & ARC—Making Stablecoins Grow an Operating System

The ARC token pre-sale raised 222 million at a 3 billion fully diluted valuation (FDV). This was the other major event released on May 11th, concurrent with the earnings report. I believe its informational value is no less than the earnings report itself.

Circle defines Arc as the "Economic Operating System (Economic OS) for the internet." It sounds abstract, but if you break down the stack, the logic is clear:

- USDC is the currency layer

- CPN is the payment network layer

- Arc is the settlement and execution layer

- ARC is the governance and coordination asset

- The AI Agent Toolstack is the application layer entry point for AI economic activity

If USDC is on-chain dollars, then Arc is the highway that makes these on-chain dollars move. USDC is the money, Arc is the road, and ARC is the coordination mechanism for this road.

(I) What Arc Aims to Do

Arc is an EVM-compatible Layer 1 chain. Several core design choices point to one goal: making stablecoins the default foundation for institutional-grade finance.

The chain's positioning differs significantly from current L1s.

- Ethereum prioritizes decentralization, institutional friendliness second.

- Solana prioritizes performance, institutional services supplementary.

- Arc prioritizes institutions, compliance, stablecoin settlement first, with decentralization as a gradual goal.

On this chain, USDC serves as the native gas (fee) currency, meaning institutional clients don't need to hold volatile tokens like ETH or SOL to pay fees; sub-second finality means transaction confirmation speed supports real-time settlement; optional privacy design meets financial institutions' requirements for transaction detail confidentiality; post-quantum signature schemes mean underlying security won't be compromised even with mature quantum computing.

Arc's economic mechanism: Denominated in stablecoins, but protocol fees are ultimately converted to ARC at the protocol layer. The converted ARC is partly distributed to validators and stakers (network characteristic, requiring staking for decentralization) and partly burned, offsetting programmatic inflation. This "usage → conversion → partial burn" mechanism resembles Ethereum's EIP-1559, meaning more network activity creates greater deflationary pressure on ARC.

The public testnet launched in October 2025. As of May 5th, it processed over 244 million transactions. Already over 100 institutions are participating, including BlackRock, Visa, Goldman Sachs, State Street, Deutsche Bank, AWS, Anthropic.

Mainnet Beta is expected in the second half of 2026.

2. ARC's Prestigious Investor List</p

Investor list: a16z crypto (led 75 million), Apollo, BlackRock, ARK Invest, Bullish, General Catalyst, Haun Ventures, Intercontinental Exchange (NYSE parent), IDG Capital, Janus Henderson, Marshall Wace, SBI Group, Standard Chartered Ventures.

On this lengthy list, ICE is the parent of the NYSE, BlackRock manages 11 trillion in assets, Apollo is a top global alternative asset manager. This array of traditional asset management giants, global exchange operators, and Asian capital simultaneously appearing in the same public chain token pre-sale is an unprecedented configuration in the industry.

If these institutions were only optimistic about Circle the company, they could just buy CRCL stock in the secondary market. Choosing ARC indicates they see value in the Arc network itself.

3. Value for Circle Shareholders

Total ARC supply is 10 billion tokens. The allocation structure is:

- Circle holds 25% (2.5 billion tokens)

- Ecosystem participants 60% (6 billion tokens)

- Long-term reserves 15% (1.5 billion tokens)

At the 3 billion fully diluted valuation, Circle's holding has a nominal value of 750 million. Important points to note here:

First, value is not cash. ARC tokens currently have no public trading market, the mainnet is not live, pre-sale investors are locked for at least 1 year (post-PoS transition), possibly extending to 4 years. Circle's own 2.5 billion tokens have a similar unlock path. This nominal value won't convert to short-term profits—and it's reasonable to expect that Circle the company will not sell this portion, likely participating in network governance and earning network revenue through staking.

Second, value will be distributed among multiple parties. The ARC whitepaper disclaimer states: ARC does not represent equity, debt, dividend rights, revenue-sharing rights, liquidation rights, ownership interests in any person, nor any claim to Circle's revenue, profits, or assets. This statement is extremely important for CRCL shareholders. Legally, there is no direct claim relationship between ARC token value and CRCL shareholder rights. If the Arc network scales, value will be distributed among CRCL shareholders (via Circle's 25% holding), ARC token holders, validators, stakers, ecosystem developers, early investors. CRCL shareholders are only one beneficiary.

Therefore, for valuing this Arc network component, a slight discount considering the above two points is necessary, combined with future contributions to the network. Its holding can be considered as a non-directly-monetizable asset in valuation, looking at both the short-term market cap reached during network hype and, more importantly, the value captured based on the network's real development.

The market typically assigns a much higher valuation ceiling to infrastructure providers like ARC than to "interest-earning" businesses.

VI. What Today's 30 Billion Is Betting On

Now, combining the three dimensions, we can perform a simple SOTP (Sum-of-the-Parts) valuation.

Based on current annualized figures (Q1 data × 4):

First Dimension Reserve Business. Valuation formula: Annualized Reserve Revenue × Post-distribution Retention Rate × After-tax Coefficient × Reasonable P/E Multiple.

Annualized reserve revenue 2.612 billion. Based on a Net Reserve Margin retention rate of 38%, post-distribution retention is 993 million. Deducting taxes, management expenses, etc., roughly estimated at 600 million. At 10-15x P/E, valuation corresponds to 6-9 billion.

This business segment's valuation floor is relatively solid, but the ceiling is limited—because it's sensitive to interest rates and the distribution agreement.

Second Dimension Other Revenue. FY26 guidance midpoint 160 million. At 10-20x P/S (common range for early-stage high-growth platform businesses), corresponds to 1.6-3.2 billion.

CPN current annualized transaction volume 8.3 billion, nearing 10 billion as of May, but not yet at a scale contributing substantial profit. Temporarily excluded here, but can be considered a plus in mental calculation.

Third Dimension Arc Network & ARC Token. Circle holds 25% of ARC, nominal value 750 million. Valuation here varies per person. Some think it's not sellable, the chain has little on it yet, requiring a significant discount; others think when it actually launches, it'll be worth more than now, deserving a higher valuation. I won't elaborate in detail here; you can determine your own acceptable range.

Summing the three dimensions, under current annualized figures, it's roughly 10-15 billion. This value seems low, but note it's a figure without considering dreams, FOMO, narratives, or tokenomics, seeking some clear safety margin. The greatest significance of this value is to give us a sense of the "bottom."

CRCL's current market cap is around 30 billion. The difference is the market pricing for 3-5 year forward growth, roughly assuming a compound growth rate of 27%, USDC scale reaching 200 billion, interest stabilizing at 3%, Other Revenue rising to 35%, etc., then priced at a slightly higher P/E.

However, I've always believed that "holding a calculator" can only be used to determine if something is cheap. Investment is absolutely not about calculating back and forth. Ultimately, it comes down to the business model.

If the business model is right, being a little expensive or cheap doesn't matter much in the long run; if the business model is wrong, even your cheapest calculation will still lead to losses.

Duan Yongping bought Apple and then it fell 50%, ultimately not stopping him from becoming "Duan God," essentially because he understood "Apple's business model."

In a recent dialogue between Duan Yongping and Wang Shi, Tian Pujun asked Duan: What do you think was the biggest gain (from having a meal with Buffett)?

Duan Yongping said: My biggest gain was when I asked him, what's the most important thing you look at in a company? He said the business model. That left a deep impression on me because we look at everything in a company. I asked, what's the first thing you look at? He said the business model. If the business model isn't right, I don't look further. He has a filter. He calls it the right person and the right price. For me, I don't even mention the right price.