Author: Mesh

Compiled by: Deep Tide TechFlow

Honestly, the development of institutional-grade RWA tokenization over the past six months deserves in-depth attention. The market size is approaching $20 billion. This is not hype; it's real institutional capital being deployed on-chain.

I have been following this space for a while, and the recent pace of development is astonishing. From treasury bonds and private credit to tokenized stocks, these assets are moving to blockchain infrastructure faster than the market expected.

Currently, five protocols have become the foundation of this field: RaylsLabs, OndoFinance, Centrifuge, CantonNetwork, and Polymesh. They are not competing for the same type of clients but are addressing different institutional needs: banks require privacy, asset managers pursue efficiency, and Wall Street firms demand compliance infrastructure.

This is not about who "wins" but about which infrastructure institutions choose and how trillions of dollars in traditional assets migrate through these tools.

An Overlooked Market Approaching the $20 Billion Mark

Three years ago, tokenized RWA was barely a category. Today, on-chain deployed assets for treasury bonds, private credit, and public stocks are nearing $20 billion. This growth is significant compared to the $6–8 billion range at the beginning of 2024.

Honestly, the performance of sub-markets is more interesting than the total size.

According to the market snapshot from rwa.xyz in early January 2026:

-

Treasury bonds and money market funds: approximately $8–9 billion, accounting for 45%–50% of the market

-

Private credit: $2–6 billion (small base but fastest-growing, accounting for 20%–30%)

-

Public stocks: over $400 million (growing rapidly, primarily driven by OndoFinance)

Three Driving Factors Accelerating RWA Adoption:

-

Appeal of Yield Arbitrage: Tokenized treasury products offer 4%–6% returns with 24/7 access, while traditional markets have T+2 settlement cycles. Private credit instruments offer 8%–12% returns. For institutional treasurers managing billions in idle capital, the math is clear.

-

Gradual Improvement in Regulatory Frameworks: The EU's Markets in Crypto-Assets Regulation (MiCA) is now enforced across 27 countries. The SEC's "Project Crypto" is advancing on-chain securities frameworks. Meanwhile, No-Action Letters allow infrastructure providers like DTCC to tokenize assets.

-

Maturation of Custody and Oracle Infrastructure: Chronicle Labs handles over $20 billion in total value locked, and Halborn has completed security audits for major RWA protocols. This infrastructure is mature enough to meet fiduciary standards.

Despite this, the industry still faces significant challenges. The cost of cross-chain transactions is estimated at $1.3 billion annually. Due to higher capital flow costs than arbitrage gains, price spreads for the same asset on different blockchains range from 1% to 3%. The conflict between privacy needs and regulatory transparency requirements remains unresolved.

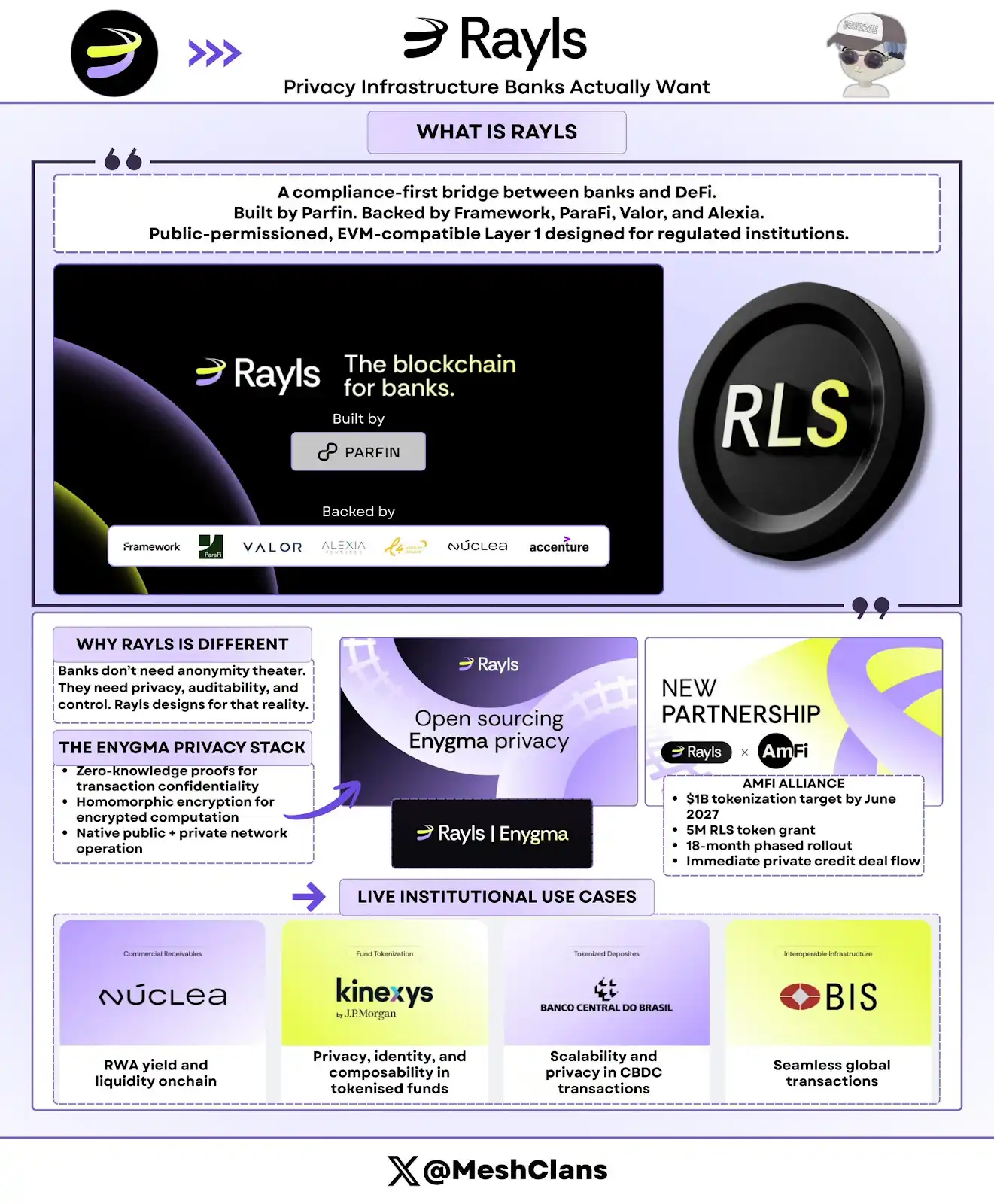

RaylsLabs: The Privacy Infrastructure Banks Truly Need

@RaylsLabs positions itself as a compliance-first bridge connecting banks to decentralized finance (DeFi). Developed by Brazilian fintech company Parfin and backed by Framework Ventures, ParaFi Capital, Valor Capital, and Alexia Ventures, its architecture is a public-permissioned, EVM-compatible L1 blockchain designed for regulated institutions.

I have been following the development of its Enygma privacy tech stack for some time. The key is not the technical specifications but its methodology. Rayls is solving the real problems banks face, not catering to the DeFi community's assumptions about bank needs.

Core Features of the Enygma Privacy Tech Stack:1. Zero-Knowledge Proofs: Ensure transaction confidentiality; 2. Homomorphic Encryption: Supports computations on encrypted data; 3. Native operations across public chains and private institutional networks; 4. Confidential Payments: Supports atomic swaps and embedded "delivery versus payment"; 5. Programmable Compliance: Selective data disclosure to designated auditors

Practical Use Cases:1. Central Bank of Brazil: Used for cross-border CBDC settlement pilots; 2. Núclea: Regulated tokenization of receivables; 3. Multiple undisclosed node clients: Used for privatized delivery versus payment workflows

Latest Developments

On January 8, 2026, Rayls announced the completion of a security audit by Halborn. This provides institutional-grade security certification for its RWA infrastructure, which is particularly important for banks evaluating production deployment.

Additionally, the AmFi alliance plans to achieve $1 billion in tokenized assets on Rayls by June 2027, supported by a reward of 5 million RLS tokens. AmFi is Brazil's largest private credit tokenization platform, bringing immediate transaction flow to Rayls and setting an 18-month milestone. This is one of the largest institutional RWA commitments in any blockchain ecosystem to date.

Target Market and Challenges

Rayls targets banks, central banks, and asset managers requiring institutional-grade privacy. Its public-permissioned model restricts validator participation to licensed financial institutions while ensuring transaction data confidentiality.

However, Rayls faces the challenge of proving its market appeal. Without public TVL data or announced client deployments beyond pilots, the $1 billion AmFi target by mid-2027 is its key test.

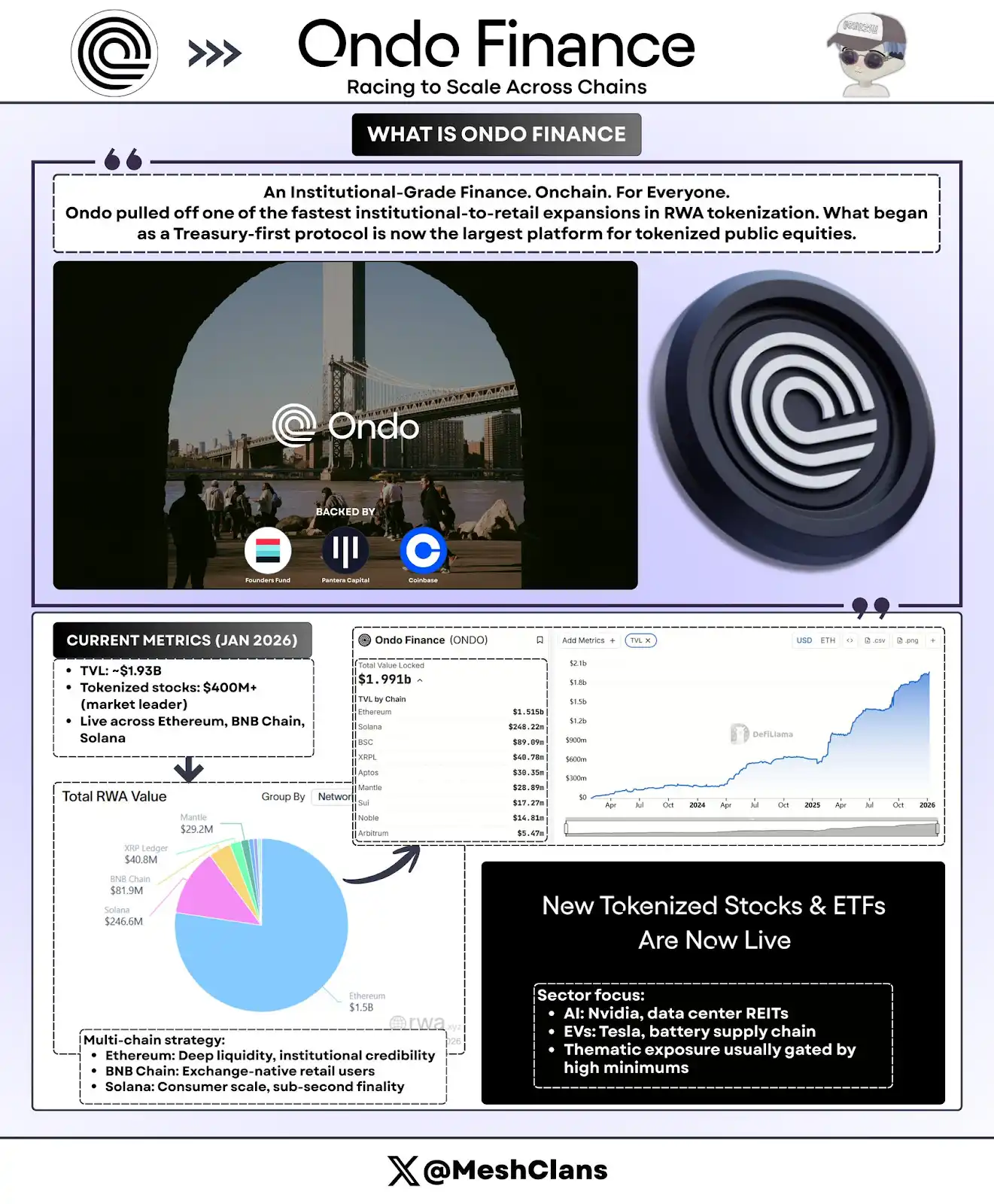

OndoFinance: The Race for Cross-Chain Expansion

Ondo has achieved the fastest expansion from institutions to retail in the RWA tokenization space. Starting as a protocol focused on treasury bonds, it is now the largest platform for tokenized public stocks.

Latest Data as of January 2026:

-

TVL: $1.93 billion

-

Tokenized Stocks: Over $400 million, accounting for 53% market share

-

USDY Holdings on Solana: Approximately $176 million

I personally tested the USDY product on Solana, and the user experience was seamless: combining institutional-grade treasury bonds with DeFi convenience is the key.

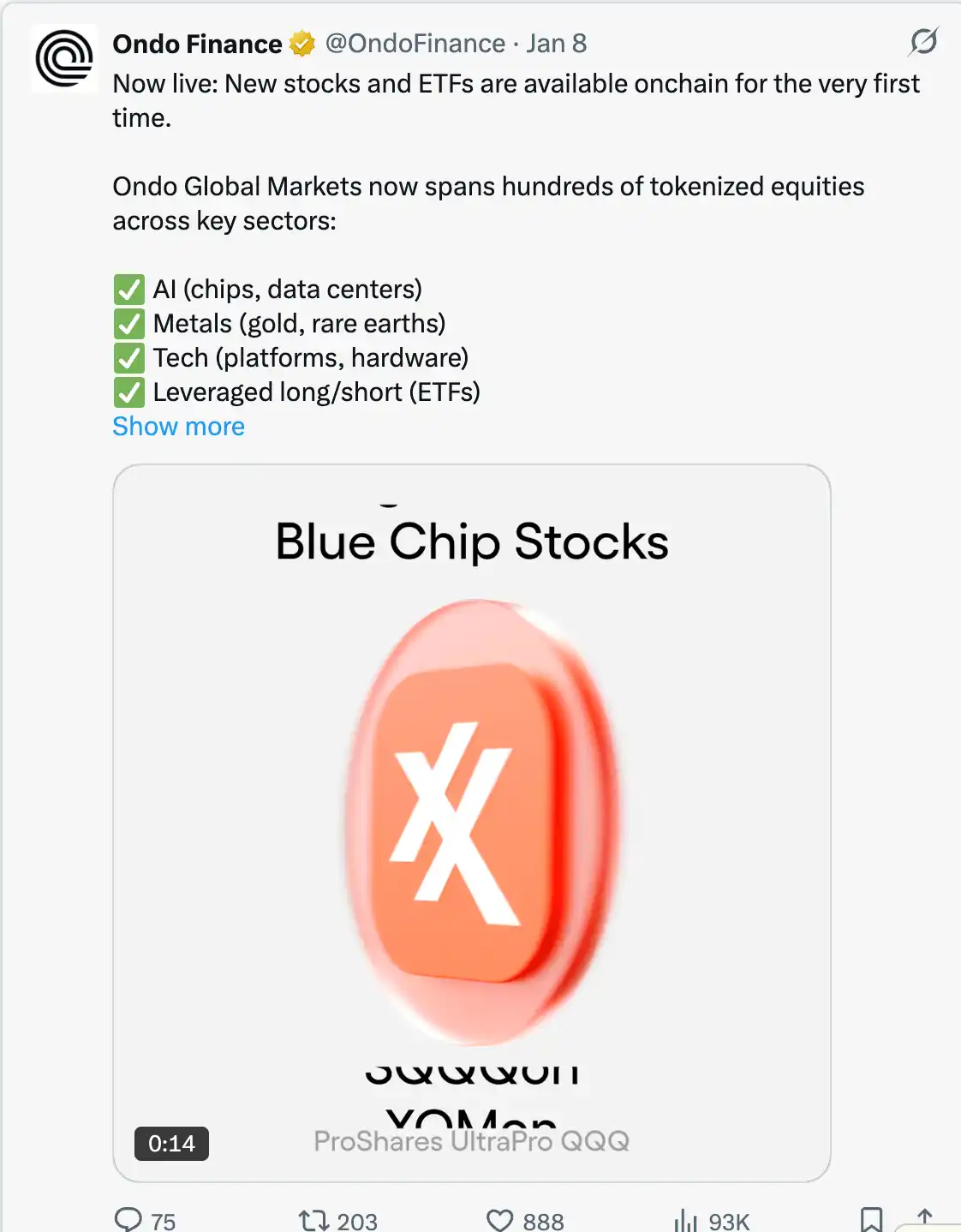

Latest Developments

On January 8, 2026, Ondo launched 98 new tokenized assets in one go, covering stocks and ETFs in areas like artificial intelligence (AI), electric vehicles (EV), and thematic investing. This is not a small-scale test but a rapid push.

Ondo plans to launch tokenized U.S. stocks and ETFs on Solana in Q1 2026, its most aggressive attempt to enter retail-friendly infrastructure. According to the product roadmap, the goal is to list over 1,000 tokenized assets as expansion progresses.

Industry Focus:

-

AI Sector: Nvidia, data center REITs (Real Estate Investment Trusts)

-

EV Sector: Tesla, lithium battery manufacturers

-

Thematic Investing: Niche sectors traditionally limited by high minimum investment thresholds

Multi-Chain Deployment Strategy:

- Ethereum: DeFi liquidity and institutional legitimacy

-

BNB Chain: Coverage of exchange-native users

-

Solana: Supports mass consumer use with sub-second transaction finality

Honestly, Ondo's TVL reaching $1.93 billion while its token price declined is the most important signal: protocol growth takes precedence over speculation. This growth is primarily driven by institutional treasury bonds and DeFi protocols' demand for idle stablecoin yields. The TVL growth during the market consolidation in Q4 2025 indicates real demand, not just chasing market trends.

By establishing custodian-broker relationships, completing Halborn security audits, and launching products on three major blockchains within six months, Ondo has taken a lead that competitors struggle to match. For example, its competitor Backed Finance has a tokenized asset size of only about $162 million.

However, Ondo still faces challenges:

-

Price Volatility During Non-Trading Hours: Although tokens can be transferred anytime, pricing still references exchange operating hours, which can create arbitrage spreads during U.S. night trading hours.

-

Compliance Restrictions: Securities laws require strict KYC and accreditation checks, limiting the "permissionless" narrative.

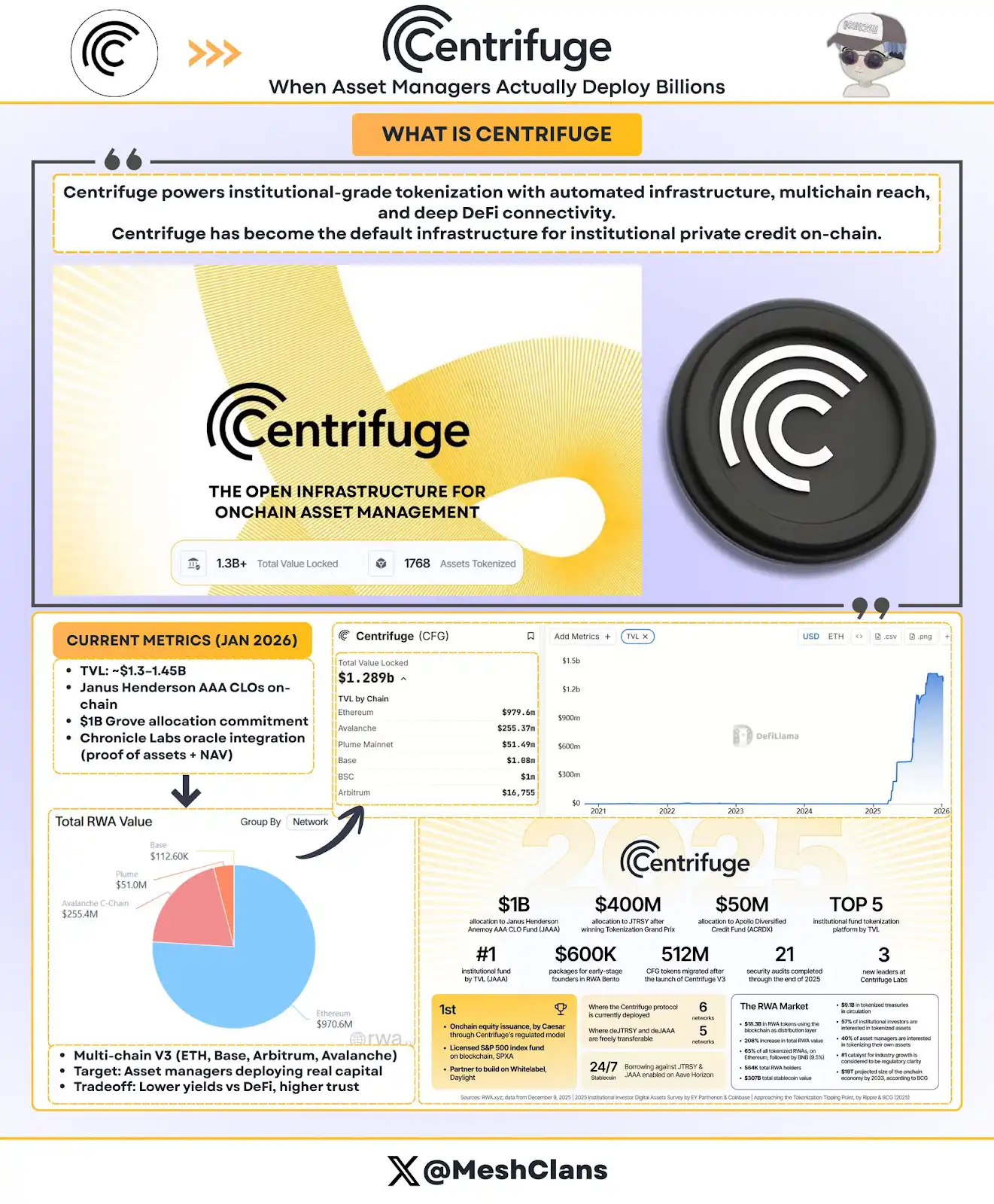

Centrifuge: How Asset Managers Truly Deploy Billions

Centrifuge has become the infrastructure standard for institutional-grade private credit tokenization. As of December 2025, the protocol's TVL surged to $1.3–1.45 billion, driven by actual deployed institutional capital.

Major Institutional Deployment Cases

-

Janus Henderson Partnership (global asset manager with $373 billion AUM)

-

Anemoy AAA CLO Fund: Fully on-chain AAA-rated collateralized loan obligation (CLO)

-

Uses the same portfolio management team as its $21.4 billion AAA CLO ETF

-

Announced expansion plans in July 2025 to add $250 million on Avalanche

-

Grove Capital Allocation (institutional credit protocol for the Sky ecosystem)

-

Committed allocation strategy of $1 billion

-

Initial launch capital of $50 million

-

Project founding team from Deloitte, Citigroup, BlockTower Capital, and Hildene Capital Management

-

Chronicle Labs Oracle (announced January 8, 2026)

-

Proof-of-Assets Framework: Provides cryptographically verified holding data

-

Supports transparent Net Asset Value (NAV) calculation, custody verification, and compliance reporting

-

Provides dashboard access for limited partners and auditors

I have been following the oracle problem in blockchain, and Chronicle Labs' approach is the first to meet institutional needs: providing verifiable data without sacrificing on-chain efficiency. The January 8 announcement included a video demo showing the solution is already in practical use, not a future promise.

Centrifuge's Unique Operating Model:

Unlike competitors who simply wrap off-chain products, Centrifuge tokenizes credit strategies at the issuance stage. Its process is as follows:

-

Issuers design and manage funds through a single transparent workflow;

-

Institutional investors allocate stablecoins for investment;

-

Funds flow to borrowers after credit approval;

-

Repayments are proportionally distributed to token holders via smart contracts;

-

AAA assets offer an annualized yield (APY) of 3.3%–4.6%, with full transparency.

Multi-chain V3 architecture supports networks: Ethereum; Base, Arbitrum, Celo, Avalanche

The key is that asset managers need to prove that on-chain credit can support deployments of tens of billions, and Centrifuge has achieved this. The Janus Henderson partnership alone provides tens of billions in capacity.

Additionally, Centrifuge's leadership in industry standards (e.g., co-founding the Tokenized Asset Coalition and Real-World Asset Summit) further solidifies its position as infrastructure, not just a single product.

Although the $1.45 billion TVL proves institutional investment demand, the targeted 3.8% APY pales compared to historically higher-risk, higher-return opportunities in DeFi. Attracting DeFi-native liquidity providers beyond Sky ecosystem allocations is Centrifuge's next challenge.

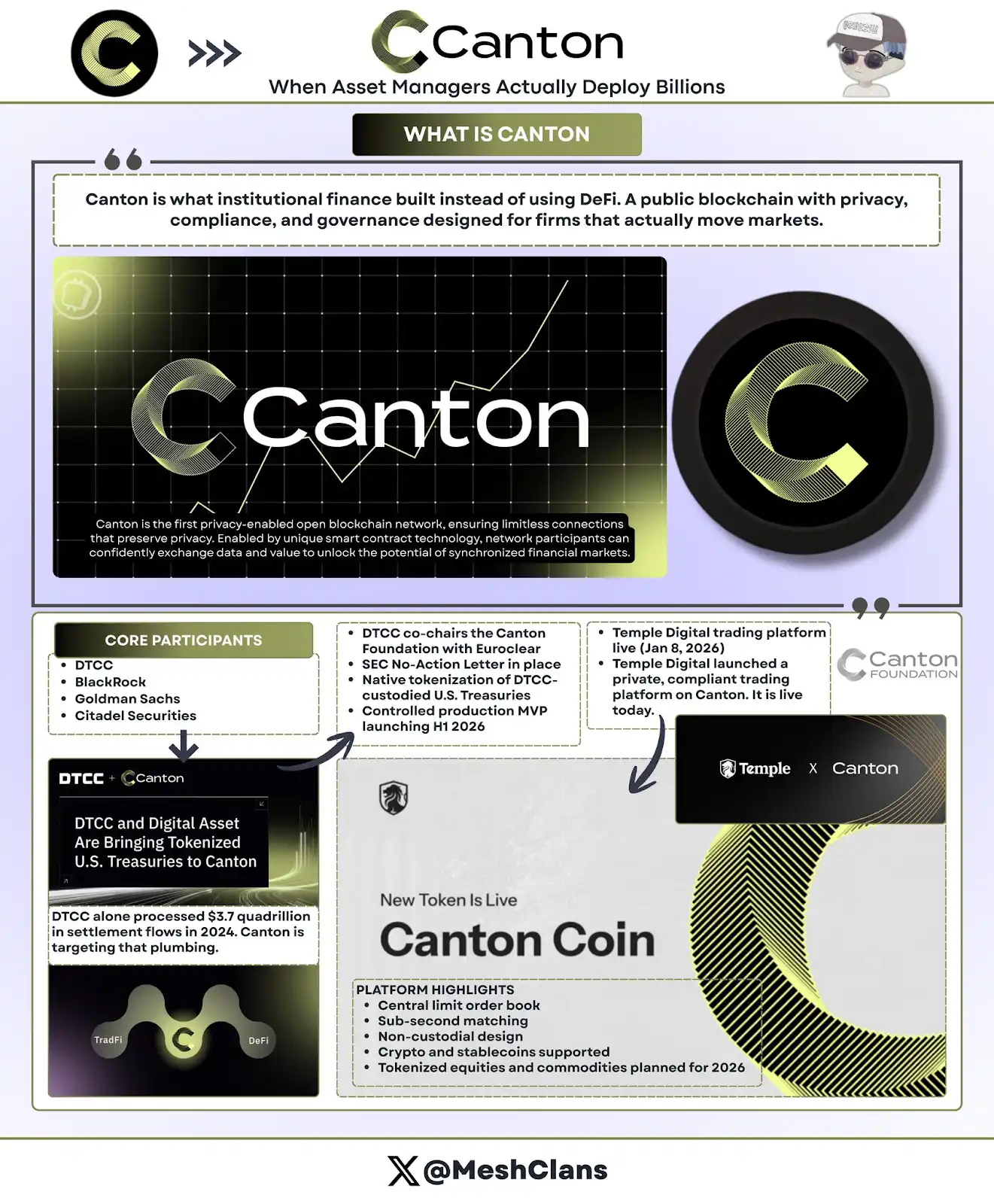

CantonNetwork: Wall Street's Blockchain Infrastructure

Canton is the institutional blockchain's response to DeFi's permissionless ethos: a privacy-preserving public network backed by top Wall Street firms.

Participating Institutions: DTCC (Depository Trust & Clearing Corporation), BlackRock, Goldman Sachs, Citadel Securities.

Canton aims to target the $370 trillion in annual settlement volume handled by DTCC in 2024. Yes, that number is correct.

DTCC Partnership (December 2025)

The partnership with DTCC is crucial. This is not just a pilot but a core commitment to building U.S. securities settlement infrastructure. With SEC No-Action Letter approval, this allows partial tokenization of U.S. treasuries custodied by DTCC natively on Canton, with a controlled production MVP (Minimum Viable Product) planned for H1 2026.

Key Details:

-

DTCC and Euroclear serve as co-chairs of the Canton Foundation;

-

Not just participants but leaders in governance;

-

Initial focus on treasury bonds (lowest credit risk, high liquidity, clear regulation);

- Potential expansion to corporate bonds, stocks, and structured products post-MVP.

Initially, I was skeptical of permissioned blockchains. But the DTCC partnership changed my mind. Not because of technical superiority, but because this is infrastructure traditional finance will actually adopt.

Temple Digital Platform Launch (January 8, 2026): Canton's institutional value proposition was further clarified with the launch of the private trading platform by Temple Digital Group on January 8, 2026.

Canton offers a central limit order book with sub-second matching speeds and a non-custodial architecture. Currently supports cryptocurrency and stablecoin trading, with plans to add tokenized stocks and commodities in 2026.

Ecosystem Partners:1. Franklin Templeton manages an $828 million money market fund; 2. JPMorgan enables delivery versus payment settlement via JPM Coin.

Canton's Privacy Architecture: Canton's privacy features are at the smart contract level, implemented using Daml (Digital Asset Modeling Language):

-

Contracts explicitly define which parties can see which data;

-

Regulators have access to full audit trails;

-

Counterparties can view transaction details;

-

Competitors and the public see no transaction information;

-

State updates propagate atomically across the network.

For institutions accustomed to Bloomberg Terminals and dark pools for confidential trading, Canton's architecture makes sense: offering blockchain efficiency without exposing trading strategies. After all, Wall Street will never put proprietary trading activity on a transparent public ledger. Canton's 300+ participating institutions demonstrate its appeal. However, much of the reported volume may be simulated pilot activity rather than actual production flow. The current limitation is development speed: the MVP planned for H1 2026 reflects multi-quarter planning cycles. In contrast, DeFi protocols often launch new products in weeks.

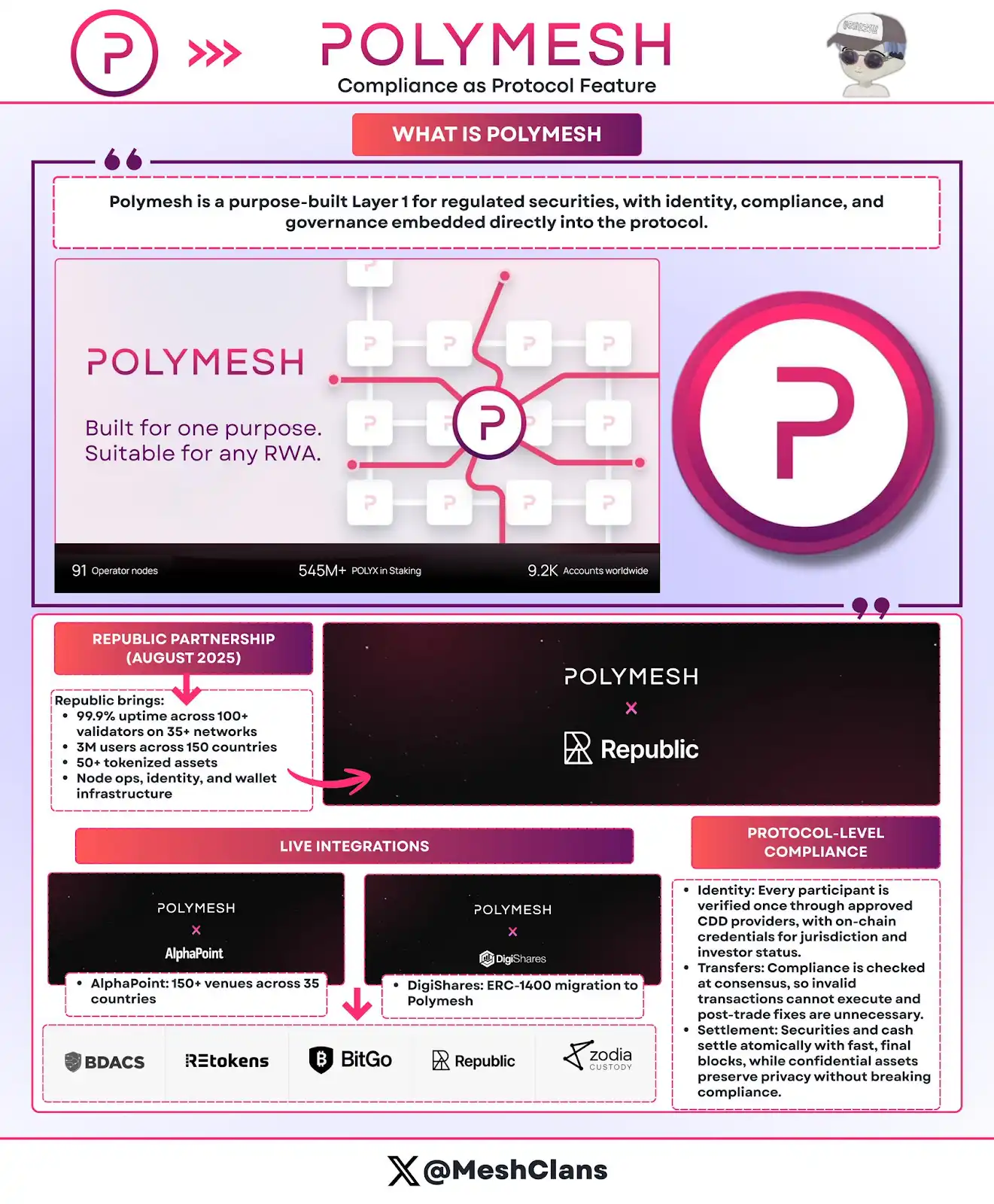

Polymesh: The Securities Network Built for Compliance

Polymesh stands out with protocol-level compliance rather than smart contract complexity. As a blockchain designed for regulated securities, Polymesh validates compliance at the consensus level,无需 relying on custom code.

Core Features

-

Protocol-Level Identity Verification: KYC via permitted Customer Due Diligence providers;

-

Embedded Transfer Rules: Non-compliant transactions fail directly at consensus;

-

Atomic Delivery vs. Payment: Settles trades with finality in under 6 seconds.

Production-Level Integrations

-

Republic (August 2025): For private securities issuance;

-

AlphaPoint: Covers 150+ trading venues across 35 countries;

-

Target Sectors: Regulated funds, real estate, corporate equity, etc.

Advantages: No need for custom smart contract audits; Protocol automatically adapts to regulatory changes; Non-compliant transfers cannot be executed.

Challenges & Future: Polymesh currently operates as a standalone chain, isolating it from DeFi liquidity. To address this, an Ethereum Bridge is planned for Q2 2026. Whether it delivers on time remains to be seen. Honestly, I underestimated the potential of this "compliance-native" architecture. For security token issuers frustrated with ERC-1400 complexity, Polymesh's approach is appealing: embedding compliance directly into the protocol, not relying on smart contracts.

How Do These Protocols Divide the Market?

These five protocols are not in direct competition because they solve different problems:

Privacy Solutions:

-

Canton: Based on Daml smart contracts, focused on Wall Street counterparty relationships;

-

Rayls: Uses ZKPs, offers bank-grade mathematical privacy;

-

Polymesh: Protocol-level identity verification, offers one-stop compliance solutions.

Expansion Strategies:

-

Ondo: Manages $1.93 billion across three chains, prioritizing liquidity speed over depth;

-

Centrifuge: Focuses on the $1.3–1.45 billion institutional credit market, depth over speed.

Target Markets:

-

Banks/CBDCs → Rayls

-

Retail/DeFi → Ondo

-

Asset Managers → Centrifuge

-

Wall Street → Canton

-

Security Tokens → Polymesh

In my view, this market segmentation is more important than people realize. Institutions won't choose the "best blockchain" but the infrastructure that solves their specific compliance, operational, and competitive needs.

Unresolved Issues

Inter-Chain Liquidity Fragmentation: The cost of cross-chain fragmentation is high, estimated at $1.3–1.5 billion annually. Due to high bridging costs, price spreads of 1%–3% exist for the same asset on different blockchains. If this persists until 2030, annual costs could exceed $75 billion. This is one of my biggest concerns. Even if you build the most advanced tokenization infrastructure, efficiency gains vanish if liquidity is scattered across incompatible chains.

Privacy vs. Transparency矛盾: Institutions need transaction confidentiality, while regulators demand auditability. In multi-party scenarios (e.g., issuers, investors, rating agencies, regulators, auditors), each party needs different levels of visibility. No perfect solution exists yet.

Regulatory Fragmentation: The EU has MiCA across 27 countries; the U.S. requires case-by-case No-Action Letters, taking months; cross-border fund flows face jurisdictional conflicts.

Oracle Risk: Tokenized assets rely on off-chain data. If data providers are compromised, on-chain asset performance may reflect incorrect reality. While Chronicle's Proof-of-Assets framework offers a solution, risks remain.

The Path to Trillions: Key Catalysts for 2026

Catalysts to Watch in 2026:

Ondo's Solana Launch (Q1 2026): Tests whether retail-scale distribution can create sustainable liquidity; Success metric: Over 100,000 holders, proving real demand.

Canton's DTCC MVP (H1 2026): Validates blockchain feasibility for U.S. treasury settlement; If successful: Could shift trillions in flow to on-chain infrastructure.

U.S. CLARITY Act Passage: Provides clear regulatory framework; Enables currently hesitant institutional investors to deploy capital.

Centrifuge's Grove Deployment: $1 billion allocation to be completed in 2026; Tests actual capital运作 of institutional credit tokenization; If executed smoothly without credit events, boosts asset manager confidence.

Market Predictions

-

2030 Target: Tokenized assets reach $2–4 trillion;

-

Growth Required: 50–100x from current $19.7 billion;

-

Assumptions: Regulatory stability, cross-chain interoperability readiness, no major institutional failures.

Growth Predictions by Industry:

-

Private Credit: Grows from current $2–6 billion to $150–200 billion (small base, highest growth rate);

-

Tokenized Treasuries: Potential $5 trillion+ if money market funds migrate on-chain;

-

Real Estate: Projected $3–4 trillion (depends on property registry systems adopting blockchain-compatible title records).

$100 Billion Milestone:

-

Expected Timeframe: 2027–2028;

-

Expected Distribution: Institutional Credit: $30–40 billion; Treasuries: $30–40 billion; Tokenized Stocks: $20–30 billion; Real Estate/Commodities: $10–20 billion.

This requires 5x growth from current levels. Though aggressive, given institutional momentum in Q4 2025 and upcoming regulatory clarity, it's not out of reach.

Why Are These Five Protocols Critical?

The institutional RWA landscape in early 2026 shows an unexpected trend: no single winner because there is no single market.

Honestly, this is how infrastructure should develop.

Each Protocol Solves Different Problems:

-

Rayls → Banking Privacy;

-

Ondo → Tokenized Stock Distribution;

-

Centrifuge → Asset Manager On-Chain Deployment;

-

Canton → Wall Street Infrastructure Migration;

-

Polymesh → Simplified Securities Compliance.

Market growth from $8.5 billion in early 2024 to $19.7 billion indicates demand has moved beyond speculation.

Core Needs of Institutional Players:

-

Treasurers: Yield and operational efficiency;

-

Asset Managers: Lower distribution costs, broader investor base;

-

Banks: Compliance-ready infrastructure.

The Next 18 Months Are Critical

-

Ondo's Solana Launch → Tests retail market scalability;

-

Canton's DTCC MVP → Tests institutional-grade settlement;

-

Centrifuge's Grove Deployment → Tests credit tokenization with real capital;

-

Rayls' $1 Billion AmFi Target → Tests privacy infrastructure adoption.

Execution over architecture, results over blueprints. That's the key now.

Traditional finance is embarking on a long-term journey of on-chain migration. These five protocols provide the infrastructure institutional capital needs: privacy layers, compliance frameworks, and settlement infrastructure. Their success will determine whether tokenization evolves as an efficiency improvement to existing structures or a new system replacing traditional financial intermediaries.

The infrastructure choices institutions make in 2026 will define the industry landscape for the next decade.

2026 Key Milestones

-

Q1: Ondo's Solana Launch (98+ stocks);

-

H1: Canton's DTCC MVP (Treasury tokenization on Wall Street infrastructure);

-

Ongoing: Centrifuge's Grove $1 billion deployment; Rayls' AmFi ecosystem building.

Trillions in assets are coming. NFA.