Author: KarenZ, Foresight News

Not all chains can support institutions.

Over the past few years, the market has been discussing "when institutions will truly come on-chain." But the question truly worth asking is not whether institutions will enter the on-chain world, but whether existing chains have the capability to handle serious business when services like bonds, repos, fund shares, collateral management, and cross-institutional settlements begin to migrate.

Canton's goal is not to compete for the most bustling general-purpose chain traffic. It targets a narrower, and more difficult task: to become the coordination layer for institutional financial workflows. Institutions can continue running their own applications, ledgers, and permission systems, while connecting to a shared synchronization infrastructure when it comes to transactions, collateral, and settlement.

In other words, Canton is not vying for the traffic gateway, but for a more foundational position: enabling large financial institutions to collaborate within the same network when they truly need to move core processes on-chain.

This pragmatic positioning is inseparable from its founding team, which deeply understands traditional financial market structures. Canton was initially promoted by Digital Asset, whose core team has long operated at the intersection of traditional finance, market structure, enterprise systems, and cryptographic engineering.

Co-founder and CEO Yuval Rooz previously worked at Citadel and DRW, familiar with institutional trading and market structure; Eric Saraniecki also comes from DRW with long-term involvement in liquidity business and co-founded Cumberland Mining. Another co-founder, Shaul Kfir, has a strong background in cryptography and distributed systems and is one of the co-authors of libsnark (a zkSNARK library). The management also includes members with extensive experience in market infrastructure at institutions like JPMorgan Chase.

Those long embedded in institutionalized financial markets know that institutions won't migrate core operations merely because a chain has higher throughput or more assets. They first need assurance that the new infrastructure can handle data boundaries, permission management, and settlement responsibilities. More persuasively, this assessment has now garnered a collective response from various types of financial market participants.

Rare Alliance of Financial Giants: The Strategic Consensus Behind $8 Billion

The latest funding round clarifies Canton's strategic stance.

On June 11, Digital Asset, the developer of Canton, announced the completion of a $355 million funding round led by a16z crypto. Participants span both traditional and on-chain finance, including the Abu Dhabi Investment Authority (through a wholly-owned subsidiary), Apollo Funds, BNP Paribas, Broadridge, Citadel Securities, CME Ventures, Coinbase Ventures, HSBC, Polychain, S&P Global, SBI Group, and other key institutions.

The most notable aspect of this list is not just the number of institutions, but the diversity and complexity of their roles: sovereign capital, asset managers, global banks, market infrastructure firms, market makers, trading platforms, rating agencies, and crypto-native capital. Their concerns are not identical, yet they all see common value in Canton.

More crucially, this is not a funding round centered around token expectations. Digital Asset CEO Yuval Rooz told The Block, "Many supporters in this round are new investors in Canton, receiving equity, not token allocations, with many institutions also being potential users of Canton."

According to Foresight News' summary, including previous funding, Digital Asset's cumulative funding has been pushed to approximately $805 million.

In June 2025, Digital Asset raised $135 million co-led by DRW Venture Capital and Tradeweb Markets, with participation from Citadel Securities, DTCC, Circle Ventures, etc.; in December of the same year, Digital Asset completed another $50 million funding round with participation from BNP Paribas, Nasdaq, S&P Global, etc.

Within just a year, Digital Asset has garnered support from various core financial participants, indicating that Canton's appeal is not merely a technical narrative but is entering the strategic budgets and business planning of financial institutions.

This is by no means an ordinary list of investors; it is a "Wall Street All-Star Network" spanning global market infrastructure, top investment banks, custody and clearing institutions, market makers, rating agencies, and leading stablecoin firms.

These institutions do not naturally align: they have their own interests, with some businesses even in direct competition. Yet, they can converge around Canton. Core players in the financial industry are reaching a strategic consensus, jointly betting on this underlying coordination layer that may one day move the entire global financial collaboration framework on-chain.

Deconstructing Canton: The Complete Operating Conditions Institutions Need to Go On-Chain

The traditional financial system is not lacking in electronic networks; what's missing is a common foundation that allows multiple institutions to collaborate seamlessly within the same network while retaining their respective data sovereignty, permission boundaries, and compliance responsibilities.

Canton's goal is not to make finance adapt to a chain, but to first make a chain adapt to the operating logic of finance. If many chains answer "how assets flow," Canton cares more about whether transactions can be executed, confirmed, and settled under real financial rules. This starting point is crucial because it determines that all subsequent technical and ecosystem paths of Canton are developed around "institutions going on-chain." Canton's technical architecture is precisely designed to replicate and upgrade these complex, layered financial operating conditions on-chain:

Canton's first layer of differentiation is that it does not take "replicating all data to all nodes" as the default premise. Instead, it adopts a segmented architecture with sub-transaction-level data visibility management. Different participants do not see the complete plaintext of the same transaction but rather the part of the transaction view relevant to their own rights and obligations. Officially summarized as sub-transaction privacy, in terms more suited to institutional language, it is essentially a native selective disclosure mechanism. Its significance is not just "more confidential," but that collaboration is built upon precise authorization: who should see what, and who should not, is defined from the outset of system design.

The second layer of differentiation is Daml smart contracts and native permission controls. The reason many so-called "on-chain finance" projects remain stuck in outer-layer applications is not due to a lack of contract expressiveness, but because the truly complex rules remain off-chain. Real-world financial transactions are not just asset transfers; they include who has signing authority, observation rights, who can execute actions only after certain conditions are met, who can grant temporary authorization, and who must participate in confirmation. The value of Daml lies in encoding these business rules, originally scattered across contracts, processes, regulations, and backend systems, directly into contract logic. Thus, compliance and governance are no longer post-execution reviews but part of the execution process; permission management no longer relies on organizational patchwork but can become part of the application logic itself.

Going one layer deeper is where Canton truly creates a gap. Many chains can complete asset transfers but may not handle the issues institutions care about most: whether assets are effectively locked, whether cash and securities can be exchanged simultaneously, and whether cross-application and cross-institutional processes can be established in the same state. For financial markets, risks often don't occur at the matching moment but in the time gap before and after settlement. Especially in scenarios like repos, collateral transfers, delivery-versus-payment (DvP), and multi-party collaboration, if transaction parties see inconsistent states, or if the Asset Leg and Cash Leg cannot complete synchronously, the result is not just delay, but settlement failures, additional capital usage, and higher counterparty risk.

What Canton provides here is a full set of layered capabilities. Committed Settlement first addresses the issue of "whether assets can be truly controlled for this transaction." According to Digital Asset, it is essentially a method that uses Daml to quickly establish control accounts or "memo pledges" on a distributed ledger. Think of it as first locking the assets intended for settlement under specific transaction conditions, preventing their arbitrary use before delivery is complete. This step handles deliverability, turning verbal delivery commitments into verifiable asset control states within the system.

Building on this, atomic settlement addresses whether "securities and funds can complete simultaneously," aligning more closely with the core requirement of delivery-versus-payment (DvP) in traditional finance. It aims to prevent the time-gap risk where securities have been transferred but cash hasn't arrived, or cash has been paid but assets haven't been delivered. For institutions, this isn't a technical detail; it's a matter of credit exposure and capital efficiency. What Canton attempts is to compress the Asset Leg and Cash Leg as much as possible into the same indivisible, verifiable settlement action, making delivery and payment logically simultaneous.

If the first two address the locking and settlement logic within a single transaction, then the Global Synchronizer addresses how this logic remains synchronously valid across different applications, participants, and subnets. Because Canton is not about cramming all business into a single ledger, but a network composed of multiple applications and subnets. The role of the Global Synchronizer is to provide underlying coordination capabilities for this cross-application, cross-network synchronization, enabling atomic transactions and composite workflows to be valid across a broader scope while preserving their respective data visibility controls and governance boundaries.

However, a public infrastructure layer capable of coordinating transactions needs to answer another question: when validation, synchronization, and cross-application settlements occur continuously, who bears the costs, and who gets rewarded for providing services?

Infrastructure Economics: How to Understand the Core Functions of Canton Coin?

Canton Coin (CC) is precisely the institutionalized answer to this question. From an infrastructure economics perspective, CC serves as the economic anchor for its native coordination network, establishing a sustainable payment and incentive mechanism for the Global Synchronizer.

Canton targets asset transfers, trading, and settlement between financial institutions, requiring parties to run validation nodes, maintain synchronization infrastructure, and applications/users to continuously bring real transaction activity. CC is the economic medium connecting these participants.

The most direct function of CC is to pay for network usage costs. Before submitting transactions on the Global Synchronizer, validation nodes need to convert CC into non-transferable traffic credits, consumed for the network resources required by transactions. Costs may also rise with larger transaction sizes, more complex computations, or higher network demand. For application providers and institutional users, CC thus resembles an infrastructure fee: using the network's synchronization, settlement, and asset transfer capabilities incurs corresponding costs.

Simultaneously, CC is also an incentive tool to maintain infrastructure operation. Validation nodes, Super Validators, application providers, and participants contributing network utility can receive rewards based on their contributions. Officially, CC has no pre-mine or VC allocations; tokens in circulation come from actual network contributions. This means CC's issuance logic attempts to distribute rewards to participants providing validation, synchronization, application services, and driving real transaction activity.

Another key design of CC is its burn-and-mint mechanism: fees generated from users utilizing the public infrastructure are burned, while newly minted CC are gradually created based on the utility provided by participants. This mechanism attempts to create a dynamic balance between infrastructure supply and real usage demand, linking token economics to network adoption.

Canton's uniqueness also lies in the fact that CC serves a financial network emphasizing privacy and interoperability. CC balances and transfer information are not, by default, publicly visible like many public chain assets, but fee payments and reward distributions can provide a window into the network's economic activity. Therefore, understanding CC's core requires viewing it as Canton's financial infrastructure's unit of account, incentive, and governance tool: it bears network operating costs and helps the public synchronization layer continuously obtain construction and maintenance resources.

Of course, the viability of this mechanism depends not only on design completeness but also on whether the network already generates real usage: Are enough institutions connected? Is there already scaled asset and transaction flow?

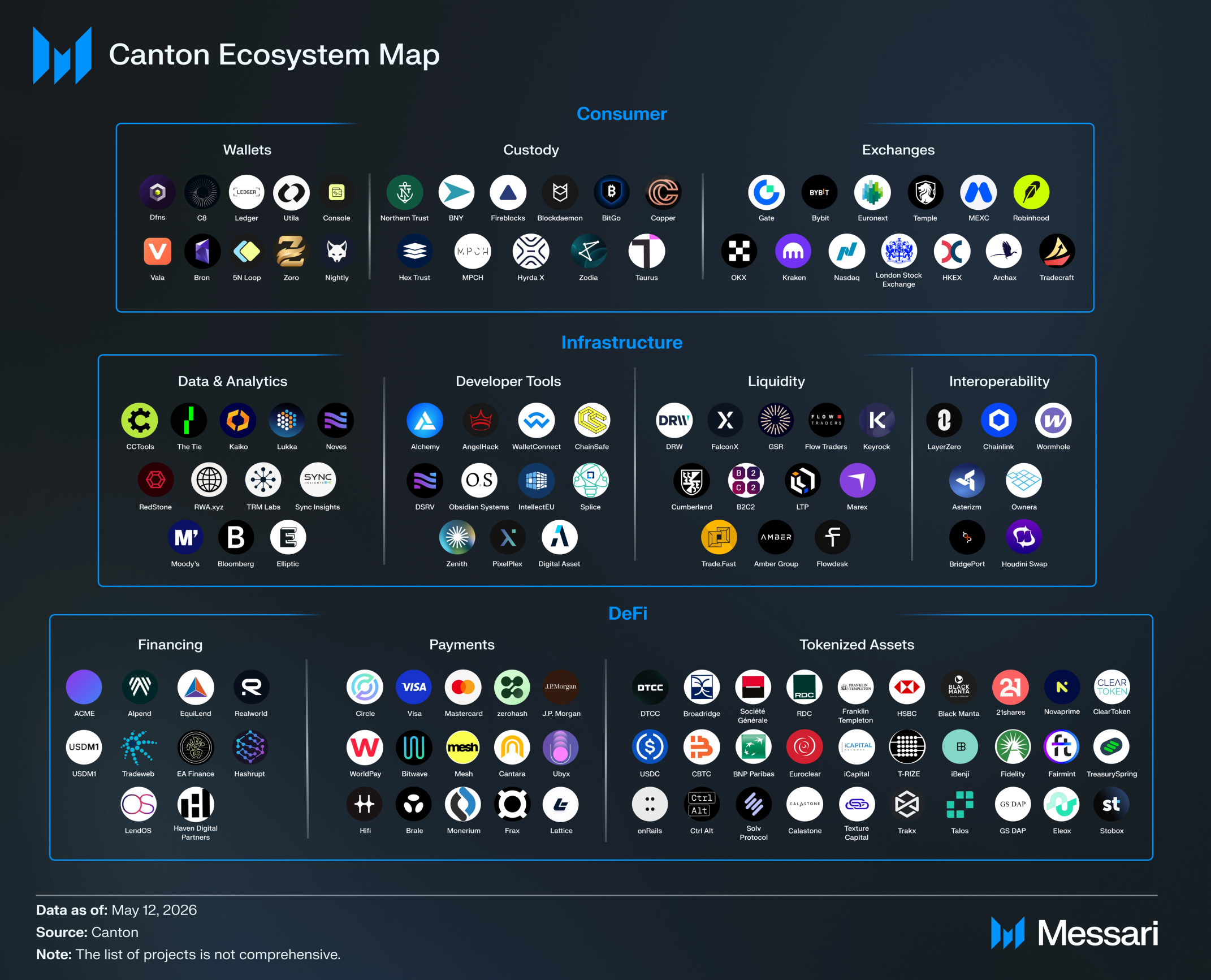

Ecosystem Landscape: Network Effects in Real Data

To understand Canton's network effects, data is the best microscope. In terms of the Canton ecosystem, from market infrastructure like DTCC and Tradeweb to Global Systemically Important Banks (G-SIBs) like Goldman Sachs and JPMorgan Chase, and further to Visa, Moody's, and Franklin Templeton, this matrix spanning multiple roles and interlocking connections means Canton is forming not isolated pilot projects, but a fully-linked assembly of institutions. The Canton Ecosystem website shows 297 current partners.

Source: Messari (statistics as of May 12, 2026)

Simultaneously, network-level activity and real business traffic are moving from "proof-of-concept" to full-scale takeoff. According to The Tie data, the Canton network currently has 762 active validators. Additionally, data disclosed by Canton in November 2025 showed it processes over 15 million transaction flows monthly using Canton Coin, handling over $6 trillion in tokenized assets and more than $350 billion in daily US Treasury repo transactions.

This hard data proves Canton is forming a collaborative foundation layer that multiple key market roles can jointly rely upon.

The next question is: As this track scales up, how will it change asset utilization efficiency and mobility? And how will this transmit to the broader on-chain world?

Laying the Institutional Track: What Changes for On-Chain Liquidity?

Canton first addresses the long-standing liquidity friction within institutional workflows: where assets are custodied, whether they can be quickly mobilized when needed; how many layers of confirmation, reconciliation, and permission approvals collateral must undergo before entering another financing transaction; whether securities delivery and fund payment can complete synchronously within the same process.

This impact will more likely transmit to the broader on-chain financial markets indirectly. Canton first improves internal institutional asset mobilization, collateral financing, and settlement efficiency, enabling more bonds, fund shares, and deposit instruments to operate on-chain. They may not directly enter open protocols but will push infrastructure like custody, stablecoins, compliance interfaces, and cross-network settlement to mature faster.

As the on-chain scale of institutional assets expands, market makers, asset issuers, and financial service providers will have greater incentive to build channels connecting different markets. Subsequently, some capital and demand may flow to more open on-chain scenarios through compliant stablecoins, tokenized cash, yield-generating products, or composable collateral forms.

This remains a long-term process, constrained collectively by regulatory boundaries, institutional risk appetite, asset transferability, cross-chain security, market depth, and compliance interface maturity. Therefore, Canton's impact on public DeFi or broader on-chain markets should not be understood as directly injecting liquidity, but more as expanding the pool of institutional assets that can be brought on-chain and providing more mature infrastructure conditions for future market connections.

Conclusion

The construction logic of most chains is "solve openness first, build order later"; the acceptance sequence of traditional financial institutions is precisely the opposite—they must first see solid order before accepting greater openness.

The importance of Canton lies precisely in its decision to avoid competing in the red ocean of open public chains and instead first provide a "foundation of order" where the world's most serious, coordination-intensive core financial activities can be securely placed and interoperate across institutions.

What it truly competes for is the most irreplaceable layer—the financial infrastructure coordination layer—in the coming era of institutions going on-chain.