Original | Odaily Planet Daily (@OdailyChina)

Author | Ding Dang (@XiaMiPP)

2025 is a year of substantial breakthroughs at the institutional level for the cryptocurrency market, and a year of gradual departure from wild growth and convergence towards the mainstream financial system. In terms of scale, the total global crypto asset market capitalization has reached $3.2 trillion, while stablecoin trading volume has exceeded $50 trillion—a figure far surpassing traditional payment giants like Visa and PayPal. Behind these numbers lies the support of two core legislative advancements.

First, stablecoin-related legislation has been formally enacted. The bill clarifies the issuing entities, reserve requirements, and regulatory mechanisms, providing a clear legal status for "on-chain dollars." This not only reduces policy uncertainty for stablecoin businesses but also directly stimulates investment and financing activity in stablecoin, payment, and settlement-related sectors. Second, the cryptocurrency market structure bill is steadily progressing, incorporating crypto assets into a classified regulatory framework to avoid a "one-size-fits-all" approach, providing project teams and investors with a predictable compliance path.

The combination of these two legislative advancements will, to some extent, reshape the primary market's assessment of risk and return.

However, in contrast to the improved institutional environment, the secondary market in 2025 did not respond with strong performance. Bitcoin prices fluctuated sharply, and altcoins performed weakly. Against this backdrop, the primary market did not exhibit the widespread frenzy seen in the previous bull market but instead showed a cautiously active态势, with明显的 changes in financing节奏 and preferences.

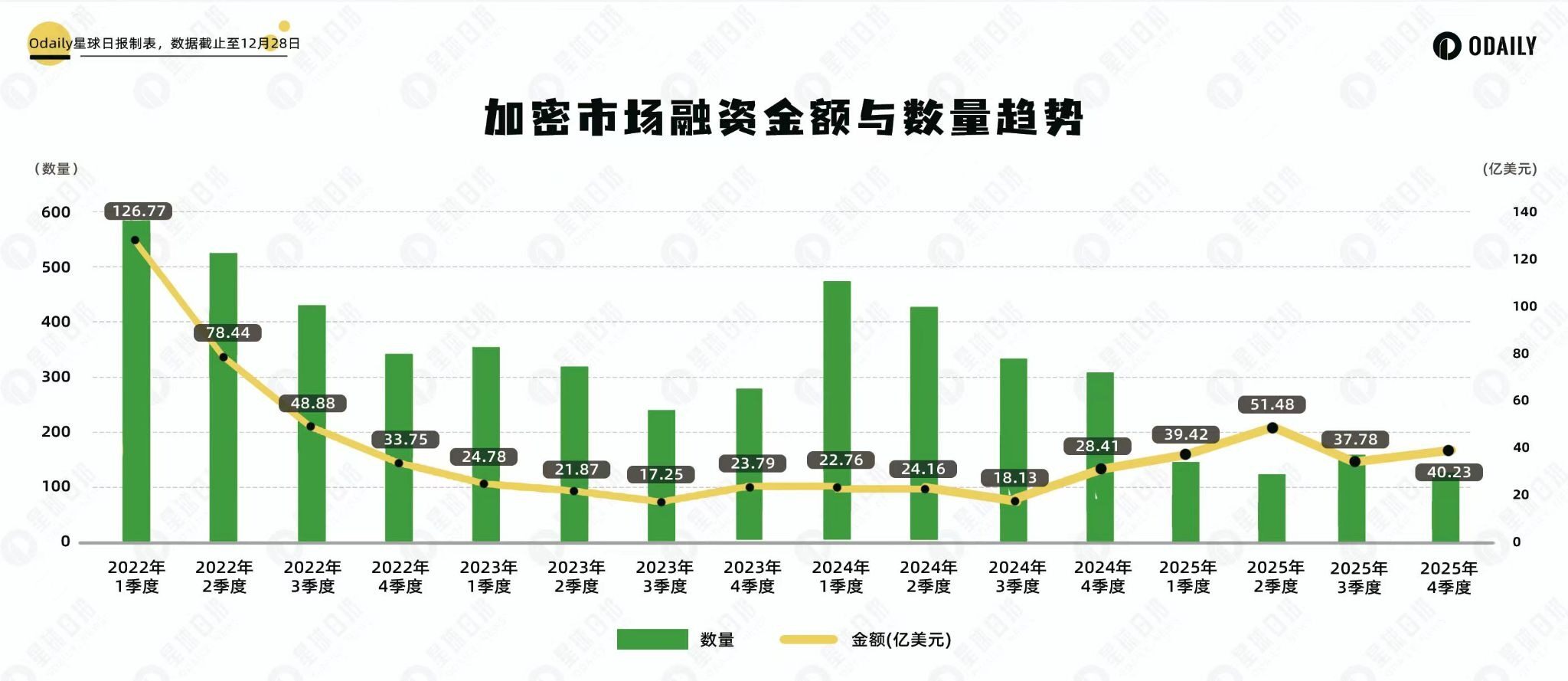

Four-Year "Cycle" Review: Two Instances of Divergence in Financing Count and Amount

Reviewing the trends in crypto financing over the past four years, the evolution of the relationship between the primary market and secondary market performance becomes clear.

Early 2022 still benefited from the residual heat of the bull market, with both the number of financing events and the amounts raised remaining high; subsequently, as Bitcoin entered a downward cycle, financing activity gradually萎缩. Between 2022 and 2023, investment and financing activities were highly correlated with price movements, remaining overall低迷 under bear market pressure.

2024 became a significant turning point, marking the first divergence between the amount raised and the number of deals.

This year, with the restart of the Bitcoin halving narrative, the number of financing events明显回暖, but the amount raised remained consistently克制. Quarterly financing规模 hovered in the range of $1.8 billion to $2.8 billion, even similar to levels during the bear market. The main reason was that during this period, the crypto market行情 was dominated by Bitcoin and the Meme sector, which stood in stark contrast to the performance of the previous cycle. In the previous cycle, VC-backed projects were often the core of market hotspots, whereas in 2024, VC projects overall performed低迷, struggling to substantially impact the market, which to some extent also抑制了大额融资的出现.

Entering 2025, the divergence phenomenon reappeared, but this time the direction reversed.

The number of financings saw a significant decline, but the amount raised began to回升. Quarterly financing规模 returned to the range of $3.7 billion to $5.1 billion. This means that the average financing size increased significantly; investors are actively reducing the number of investments and instead concentrating their bets on a few projects deemed to have certainty and scalability.

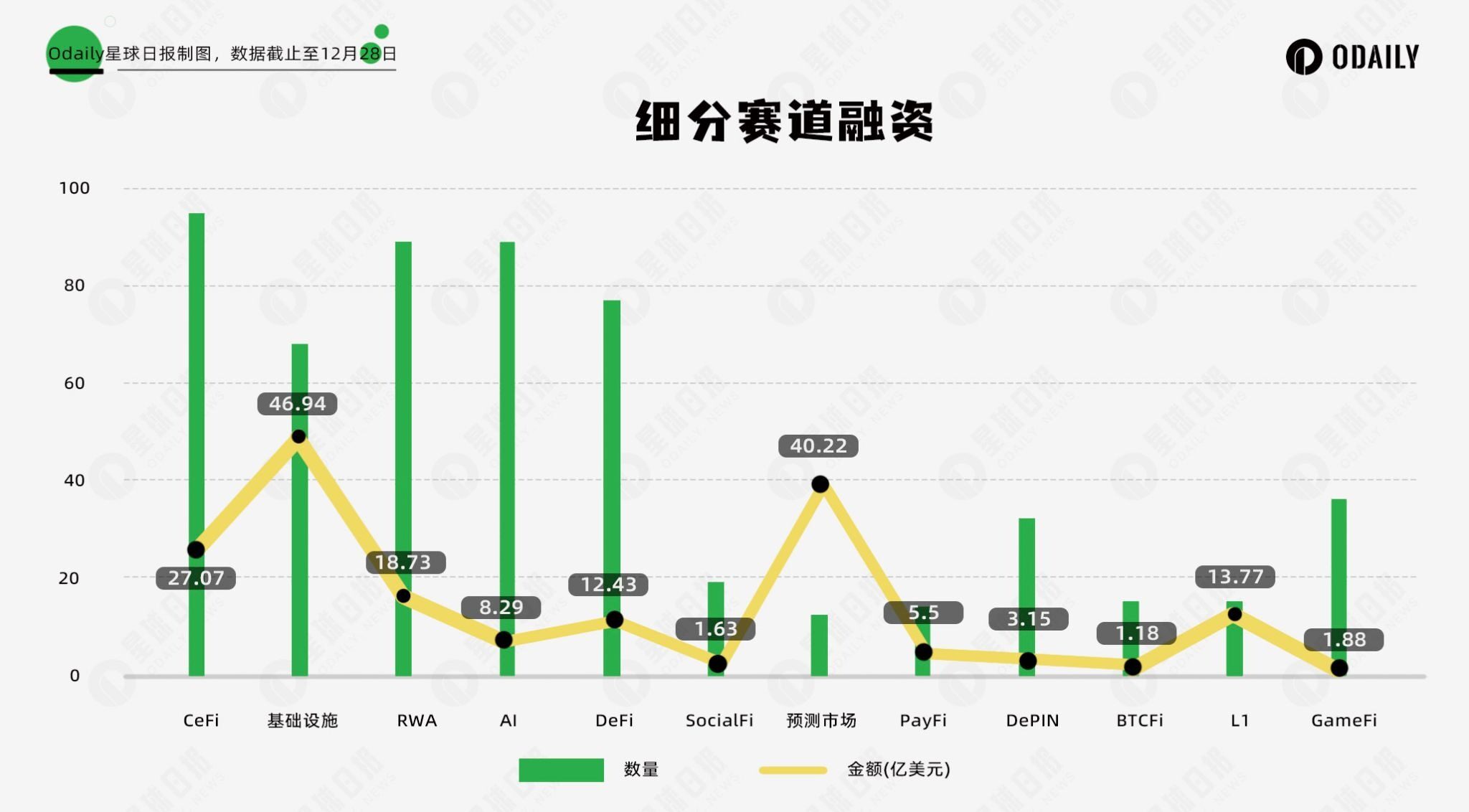

12 Sectors, $178.9 Billion: Structural Changes in the Primary Market

According to incomplete statistics from Odaily Planet Daily, the total primary market investment and financing in 2025 reached $178.9 billion, with a total of 569 financing events. To more accurately depict changes in financing preferences, we have categorized all disclosed financing projects (the actual close time is often earlier than the announcement) into 12 sectors based on business type, target audience, and business model dimensions. These include: CeFi, Infrastructure, RWA, AI, DeFi, SocialFi, Prediction Markets, PayFi, DePIN, BTCFi, L1, and GameFi.

Looking at the financing situation in细分 sectors:

- CeFi and Infrastructure ranked at the top in terms of both financing amount and number of deals. Underlying capabilities such as trading, custody, clearing, security, and cross-chain remain key areas for continuous capital investment. The market consensus on "infrastructure first" has not wavered.

- DeFi projects continue to maintain high activity levels. The market still has high demand for innovation in new DeFi protocols, especially as the success of Hyperliquid directly demonstrated to the market that decentralized exchanges can also effectively handle large-scale capital inflows. Perp DEX has become a new financing hotspot.

- AI and RWA have become new narrative pillars. The former aligns with the main theme of the global tech cycle, while the latter directly benefits from the institutional红利 of tokenizing traditional financial assets. Both paths share a common characteristic: their growth logic no longer relies entirely on the crypto-native market but extends into the broader tech and traditional financial systems.

- The real dark horse is the Prediction Market sector. Although the number of projects in this sector is not particularly突出 compared to others, the amount raised jumped to become the second-largest sector,仅次于 infrastructure. This indicates that capital is being高度集中地押注 on a few leading projects.

- In contrast, once-hot sectors like DePIN and GameFi, while still seeing many projects emerge, have experienced a sharp decline in financing appeal, as capital shifts towards areas with greater certainty and economies of scale.

Overall, the primary market is shifting from "casting a wide net" to "intensive cultivation."

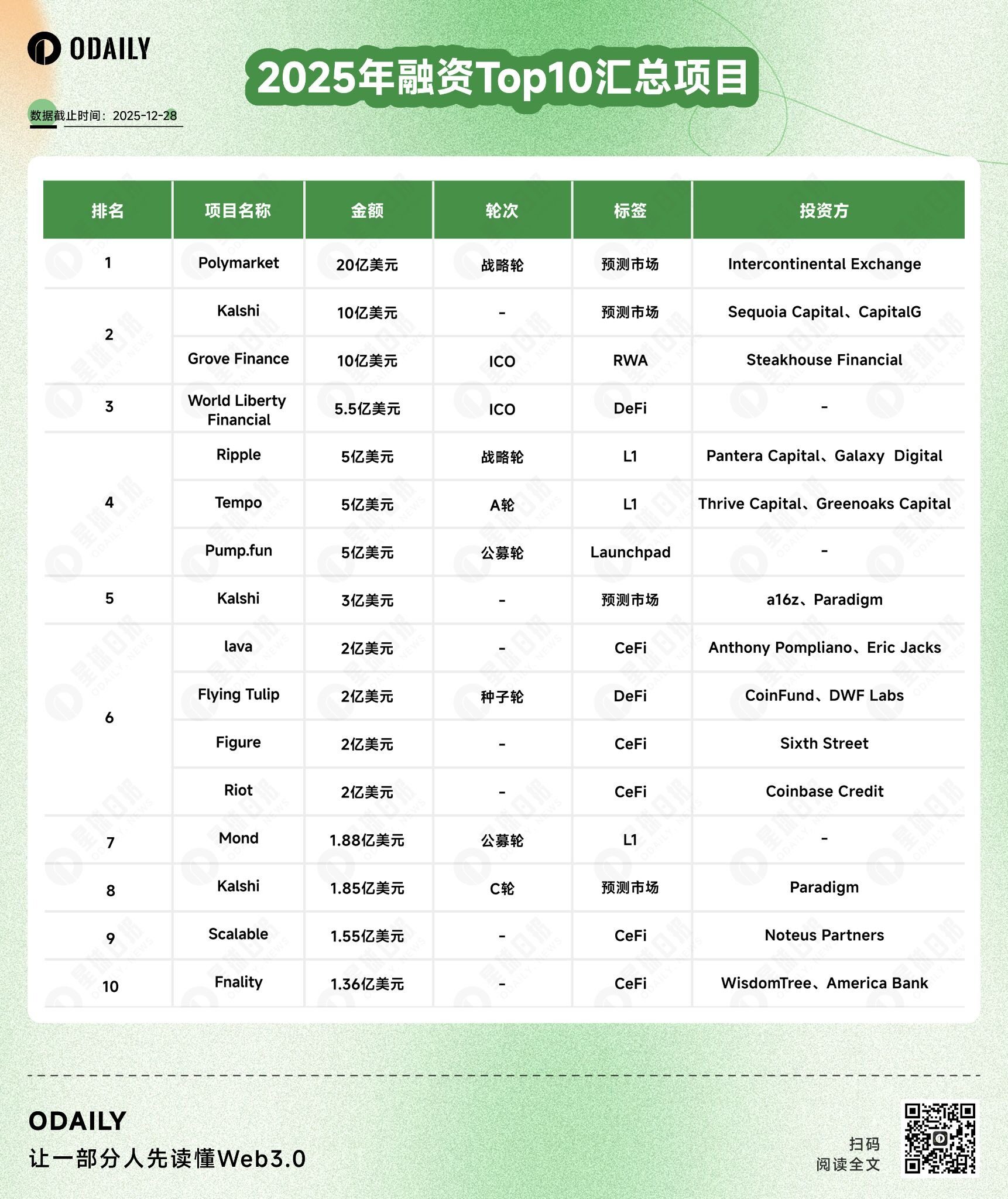

Polymarket: Consensus Changes Behind the Top Financing of 2025

From the list of Top 10 financing amounts in 2025, it can be seen that Polymarket and Kalshi almost constitute the entire narrative of 2025 financing.

Among them, Polymarket has completed nearly $2.5 billion in multiple rounds of financing, with investors including知名加密风投 funds like Polychain, Dragonfly, and Coinbase; Kalshi began to gain momentum in 2025, completing approximately $1.5 billion in financing, supported by Paradigm, a16z, and Coinbase. Unlike Polymarket, Kalshi emphasizes compliance with federal regulation. However, what they share is that prediction markets are being viewed as a financial form with real demand and have now become the most vibrant and positively trending sector.

In the L1 sector, capital preferences similarly persist. On the list, besides the established public chain Ripple, others like Tempo and Mond are new-generation projects. Among them, Mond has already issued tokens, while Tempo has not. This reflects investors' continued investment in underlying infrastructure, with high-performance L1s still seen as the long-term cornerstone for ecosystem expansion.

Conclusion

Overall, the primary market in 2025 did not cool down but is undergoing active convergence and restructuring.

Capital is still flowing, but it is no longer chasing quantity; instead, it is being allocated集中 around certainty, compliance, and scalability potential. This change does not necessarily mean fewer opportunities but may instead signal that the crypto market is entering a more rational and mature stage.