Original Author: Sanqing, Foresight News

On May 26, Kelp DAO transferred the final batch of 20,373.72 rsETH to the LayerZero OFT Adapter, while Aave simultaneously announced that rsETH and all affected markets had returned to normal. In 37 days, the full replenishment of 116,500 rsETH was completed.

However, this only means rsETH is once again backed 1:1; it does not mean Aave's books are cleared. The 30,766 ETH frozen by the Arbitrum Security Council is still stuck in the U.S. District Court for the Southern District of New York, with ownership undecided. The TVL lost by Aave hasn't returned along with rsETH.

The Bill Extends Beyond the TVL Column

According to DefiLlama data, Aave's TVL was $26.396 billion on April 18, the day of the incident; on May 25, it was $14.181 billion. The amount that hasn't returned after a month exceeds $12 billion.

The more difficult part lies ahead. The U.S. District Court for the Southern District of New York will hold a hearing on June 5 regarding the ownership of the 30,766 ETH frozen by the Arbitrum Security Council. Both Aave LLC and Gerstein Harrow had submitted supplemental briefs by May 22. The judge previously modified the restraining notice on May 8 to allow fund transfers, but the substantive ruling is still pending confirmation on June 5.

Gerstein Harrow represents families of North Korean terrorism victims, holding an unexecuted judgment of $877 million. Regardless of the outcome, this lawsuit consumes Aave's brand.

This time, DeFi United was able to form because multiple parties were willing to provide backing: Stani Kulechov contributed 5,000 ETH from his own pocket, Consensys and Joseph Lubin committed up to 30,000 ETH, the Aave treasury allocated up to 25,000 ETH, plus a credit line of up to 30,000 ETH provided by Mantle and support from multiple parties like Lido and Ether.fi.

The scale of community mobilization was unprecedented, but Aave exhausted this one-time-only card. If another upstream contamination event occurs, assembling a similar list may not be possible again.

For example, after the incident, Sun Yuchen moved approximately $174 million (including 65,854 ETH and some stablecoins) from Aave to Spark, with cumulative deposits in Spark exceeding $1.3 billion. Whales voted with their feet, and funds have already migrated.

The Openness of V4 is Being Slowed Down by Governance

Aave has more than just V4 as a countermeasure card, but V4 is the most crucial one.

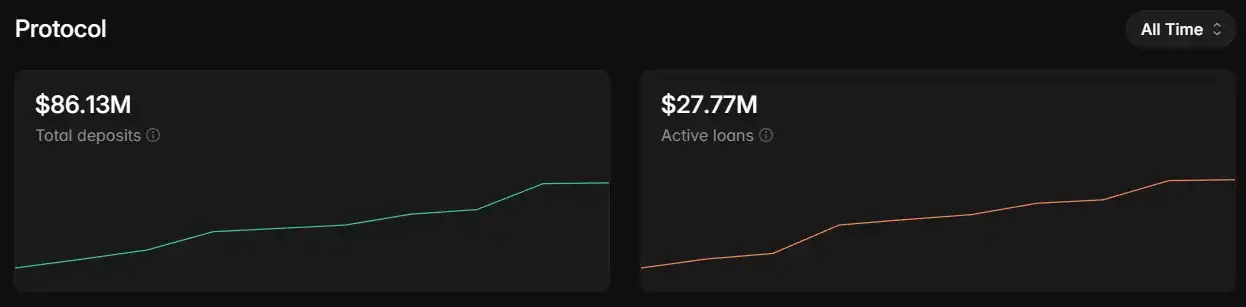

V4 was already launched on the Ethereum mainnet on March 30, with a Hub-and-Spoke architecture and three initial Liquidity Hubs. Aave Labs promised "security-first growth," with deposit limits gradually increasing. Deposits surpassed $10 million on April 8, crossed $50 million on May 9, and total deposits reached $86.13 million on May 26, with active borrowing positions at $27.77 million.

This pacing was a responsible design choice before rsETH; after rsETH, it became a stress test. Aave was handling a $200 million bad debt on V3 while slowly expanding limits on V4.

More challenging is that V4 also faces internal friction from its own governance layer. In February 2026, Aave Labs submitted a strategic proposal bundling product revenue, service provider incentives, the V4 growth engine, and brand/legal custody, requesting representatives to vote on four different risk dimensions at once.

Marc Zeller, founder of the Aave Chan Initiative, publicly questioned whether it was appropriate to bundle such a massive funding request with strategic approval. This governance dispute continued to ferment around the V4 launch, with each delay allowing competitors to eat away a bit more market share.

V4's advantage is the openness of the Spoke design—anyone can build a Spoke, and those meeting conditions can connect to a Liquidity Hub as a credit line. This is also why Babylon Labs chose to connect its Trustless Bitcoin Vaults to V4 rather than others. But the speed at which this openness materializes depends on whether the governance layer can keep up with the pace.

More Than Just V4: Aave is Fighting Three Battles

Aave V3 remains the cash cow. With annualized revenue exceeding $100 million, and $14.1 billion TVL primarily on V3. The "Aave will win" proposal positions V3 as in a "stable maintenance" phase, with Stani publicly committing to no forced migration and no deadline.

V4 and V3 will run in parallel for at least 24 to 36 months, with V4 being an additive complement layer, taking on heterogeneous scenarios that V3 cannot accommodate. Horizon is an independent, permissioned V3 fork specifically designed for institutional RWA.

Each of the three layers is capturing different increments. V4 captures new scenarios that V3's risk architecture cannot accommodate, with an added task after rsETH: giving funds that have migrated to Morpho and Spark a reason to return to Aave. Horizon captures traditional finance RWA flows, completely separate from V3 and V4 pools.

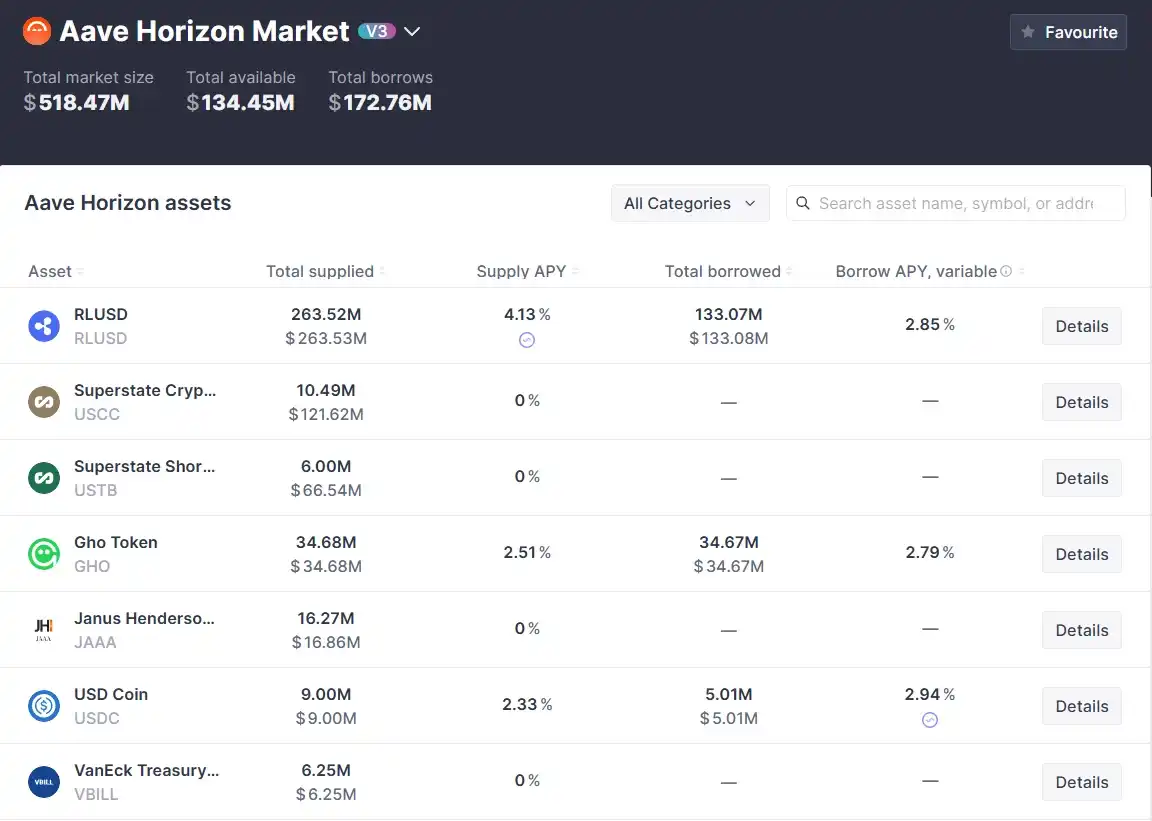

Horizon Market officially launched in August 2025, a permissioned V3 instance deployed by Aave, allowing institutions to use tokenized government bonds, corporate bonds, and money market funds as collateral to borrow stablecoins like USDC, GHO, and RLUSD.

As of May 26, it has accumulated over $500 million in net deposits, aiming to surpass $1 billion by the end of 2026, with partners including BlackRock, Franklin Templeton, Circle, Ripple, and VanEck.

This route diverges from Morpho's vault management model. Morpho uses third-party institutions like Steakhouse and Gauntlet to curate vaults, capturing lending flows from retail institutions like Coinbase. Aave uses Horizon to directly connect with traditional finance asset managers for RWA.

The two paths target different institutional customer profiles. Morpho serves fintech companies that use on-chain lending as a tool, while Aave serves asset managers that treat the chain as an issuance venue.

The fund migration after the rsETH event primarily affected the first type of client. The migration cost is higher and the reaction slower for the second type. The compliance framework, KYC processes, and asset access audits Aave has accumulated on Horizon are not easily replicable by Morpho in the short term after the event.

This is the only incremental line for Aave not directly impacted by the rsETH event, but its growth depends on the pace at which traditional finance integrates with DeFi.

No Second DeFi United

Aave remains the largest protocol in the lending market, with $14.1 billion TVL still nearly double that of Morpho. The deployment depth accumulated over years is unmatched in the short term.

But the bill left by rsETH isn't on the balance sheet; it's in the column for institutions' default preference for lending protocols. Spark's TVL grew from $3.727 billion to $5.3 billion in a month; Morpho slowly climbed back to pre-incident levels after hitting bottom on April 21. These numbers won't automatically reverse and flow back just because Aave's markets have recovered.

The speed at which V4 delivers on heterogeneous scenarios, plus the progress of Horizon on institutional RWA, will determine whether Aave can recapture the lost market share. But the former is stuck in governance friction, and the latter depends on traditional finance's own integration pace. And for both these things, Aave can only wait.

DeFi United is not a permanent institution; it was a one-time mobilization.