Author: Prathik Desai

Original Title: Circle Draws an Arc, Can it address the rate-cut problem?

Compiled and Edited by: BitpushNews

The year is 2026. When we make video calls with people around the world, the delay is at most a second or two, with marginal costs close to zero. However, when it comes to transferring funds between institutions, countries, or systems, we still face deadlines, exorbitant fees, and reliance on settlement windows that close on weekends.

Cryptocurrency promised to solve this problem with stablecoins, which have been around for over a decade. Yet, despite the significant, quantifiable savings stablecoins can bring, businesses and commercial institutions have not fully embraced them for fund transfers.

We have discussed this issue before, and how the inherent privacy concerns in public blockchains become a barrier here. We also listed privacy infrastructure as the number one cryptocurrency theme to watch in 2026.

Stablecoin issuer Circle has seized this opportunity with its Layer 1 blockchain, Arc, to address the industry's demand for privacy and stablecoin infrastructure.

In this in-depth analysis, I will explain why Circle is building an L1 blockchain now, what its biggest challenges are, and how this move could change the stablecoin ecosystem.

The story begins......

Why Launch an L1 Blockchain Now?

Currently, the stablecoin issuance business is entirely driven by interest income and heavily reliant on distribution channels. This has become clearer since the company went public last June, through the public reports of the USDC issuer.

I mentioned last year:

> In the third quarter, although the circulation of USDC increased by more than 100% year-over-year, reserve income only grew by 66%, reaching $711 million. The rest was offset by the Federal Reserve's interest rate cuts. The average yield dropped by 96 basis points, resulting in a $122 million reduction in Circle's reserve income.

> For every $1 of reserve income Circle earned in Q3, it spent over 60 cents on distribution and transaction costs, including wallet integrations, exchange listings, incentive programs, and revenue sharing.

The U.S. Federal Reserve has begun cutting interest rates. In December 2025, it lowered the effective rate by 25 basis points to 3.50%–3.75%. The central bank also announced the cessation of quantitative tightening effective December 1st.

Recently, the U.S. economy has also been signaling to policymakers that it's time to soften their stance in response to disappointing data.

The U.S. Institute for Supply Management's Manufacturing Purchasing Managers' Index (PMI) for December 2025 was 47.9 (a reading below 50 indicates contraction), marking the 10th consecutive month of contraction. The December employment report will be released later today, but data from the past few months has been lackluster.

When you put all this together, it explains why Circle is desperately pivoting to a new business model.

The issuer wants to reduce its reliance on falling short-to-mid-term interest rates while building a second engine that can rely on broader, more diversified distribution.

The Arc Transformation

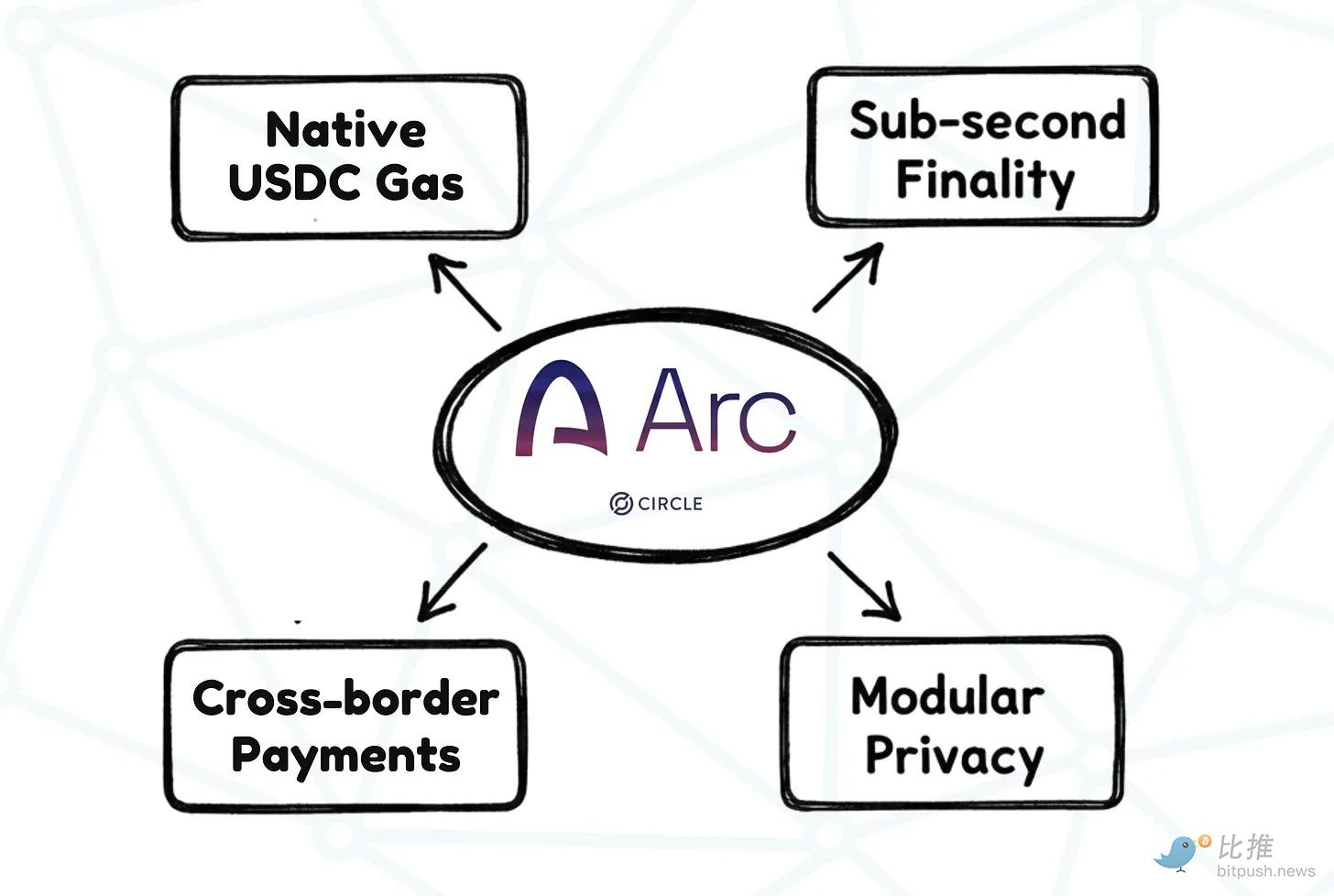

Arc is the transformation Circle is betting on.

Circle built Arc as an open Layer 1 blockchain designed for cross-border enterprise payments via stablecoins. It also aims to provide sub-second finality (transaction confirmation speed) and configurable privacy options, masking enterprises' confidential payment data through opt-in privacy features.

By transitioning from a stablecoin issuer to a stablecoin settlement stack operator, Circle aims to build its business model around moving money the way enterprises care about.

In its testnet phase, Circle's Arc has already established partnerships with over 100 companies, including traditional finance and tech giants like BlackRock, Amazon Web Services, HSBC, Standard Chartered, and Visa.

Although Arc is still in the testnet phase and will face a series of challenges before it succeeds (which I will discuss later), I find this move interesting given its timing and the problem it aims to solve.

First, it charges Gas fees (network transaction fees) natively in its own token. Arc is designed to charge low, predictable, and USD-denominated transaction fees in USDC. This eliminates the need for corporate treasury departments to hold ETH, SOL, or any other cryptocurrency just to pay transaction fees.

Second, Arc offers sub-second finality and a 24/7 settlement window. CFOs don't care about shaving off milliseconds like traders do, but they will lose sleep if a payment doesn't settle after they hit "send" because it's the weekend or due to a cross-border intermediary chain.

Third, and perhaps most importantly, is the configurable privacy Arc offers. By explicitly providing opt-in privacy features, it bridges the gap between the built-in transparency of public blockchains and enterprises' need to ensure the confidentiality of sensitive information, such as B2B supplier invoices, fund transfers, and payroll settlements.

The most interesting part is that all these features do not require stakeholders to buy into cryptocurrency ideology. Instead, Arc removes the crypto traits enterprises dislike, such as absolute transparency, fee volatility, and uncertain settlement, enabling blockchain usage in mainstream commerce.

But couldn't Circle build these features on an existing chain? Why build its own blockchain?

Circle has always been "renting the venue." On someone else's chain, Circle would be forced to inherit their fee token, compete with other players for network resources and face congestion, follow their governance rules, and be subject to their network downtime risks. It would also lose an entire revenue stream by not being able to collect fees in USDC. Circle already pays distribution costs to expand USDC's reach on other platforms. By launching its own chain, it hopes to "own the venue" and earn "rent" by offering "space" to everyone using its infrastructure.

However, this is not a race that will be easily won. Circle has no shortage of competitors watching closely.

On the issuer side, Tether remains the biggest threat, with the highest liquidity globally. It has also launched the regulation-friendly stablecoin USAT to strengthen its presence in the U.S. market.

Beyond issuers, players like Stripe pose a threat, building something similar to what Circle is doing with Arc.

In September 2025, Stripe and Paradigm announced Tempo, a payment-first blockchain built around stablecoins. Tempo's architecture allows paying Gas fees with any stablecoin and similarly aims for sub-second finality.

Besides external threats, many things could go wrong with Arc itself.

It might face cold-start difficulties in attracting liquidity and developers. Enterprises won't choose Circle's Arc just because it looks best on paper. Many are already using traditional payment platforms like PayPal and would prefer platforms that already have counterparties and integration services.

Arc's "configurable privacy" will be a contentious topic. The opt-in feature gives enterprises what they want, but it will also draw regulatory scrutiny. Arc must prove to the market that privacy here means "commercial confidentiality with auditability," not just a blind spot that could create new vulnerabilities.

Despite these hurdles, I am optimistic about Circle's opportunity for two reasons.

First is its distribution channels and reputation. Circle doesn't need to prove to the market that USDC is a real dollar token. It's already embedded in countless exchanges, wallets, fintech processes, and increasingly in institutional pipelines. Now a public company, Circle's initiatives look different from any other crypto company. Its public reputation lends credibility to its launches. It also forces Circle to build Arc in a way that can be explained clearly to the compliance and finance teams in boardrooms.

Second is the Circle payment network. Combined with Arc, it can build a network of institutions and payment channels executing real-world transactions within a compliance framework.

Arc could still fail. But does it have any other choice? With the rate-cut era officially here and more cuts likely in the new year, this is the only logical move for an issuer facing intense competition.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush