Author: Chloe, ChainCatcher

The narrative on Solana is expanding from meme coins to tokenized trading cards. In the past, Pump.fun was almost the representative application for consumer-side revenue on Solana; but entering the second quarter of 2026, Pump.fun's quarterly revenue began to slow down, while Collector Crypt delivered a stronger recent growth curve.

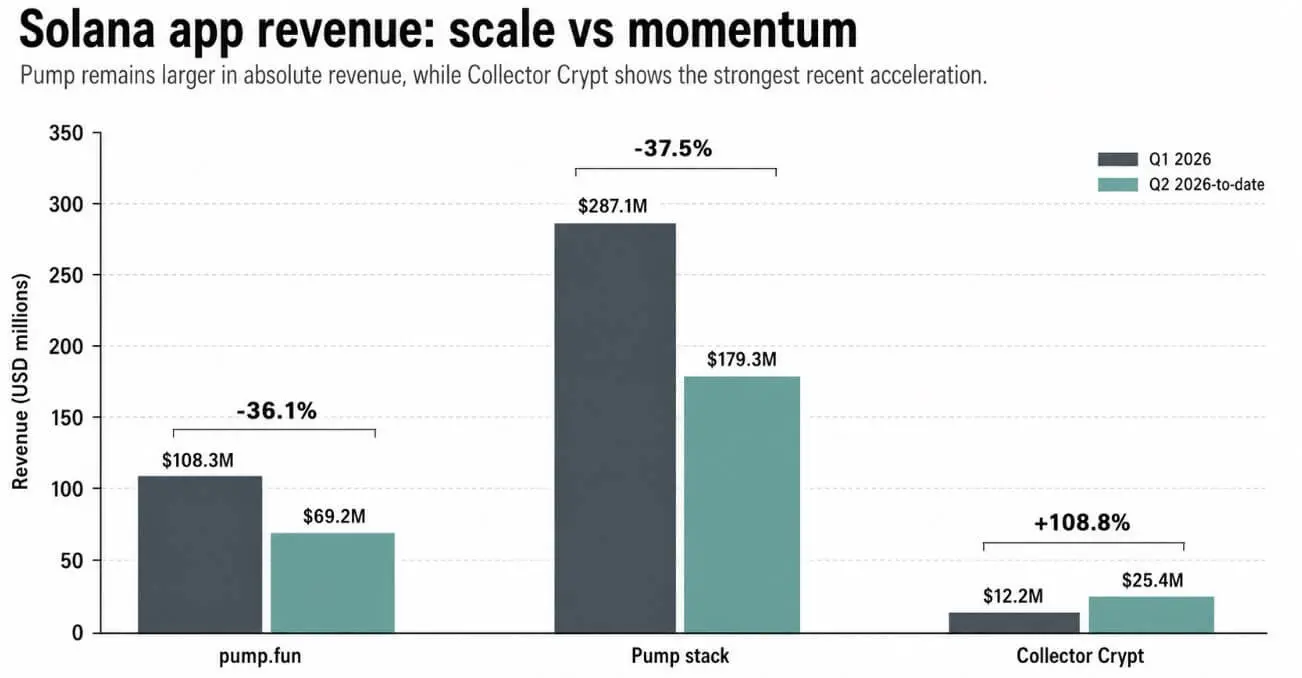

DefiLlama data shows that Pump.fun's revenue in Q1 was $108.3 million, which has dropped to $69.2 million so far in Q2, a decrease of 36.1% compared to the previous quarter. During the same period, Collector Crypt's revenue curve has clearly trended upward.

Collector Crypt's revenue in Q1 was $12.3 million, rising to $25.8 million so far in Q2, a growth of 108.8%; its recent weekly revenue reached $5.1 million, accounting for about 38% of its 30-day total revenue of nearly $13.5 million. This set of data shows that Pump.fun still has a larger scale, but Collector Crypt is gaining stronger short-term growth momentum.

Summarizing the data, perhaps it's not that Pump.fun has lost scalable growth, but rather that the sources of consumer fees on Solana are beginning to diversify. The meme coin sector remains vast, but tokenized trading cards, random card packs, physical redemption, and on-chain secondary markets are becoming another consumer scenario capable of generating real fees, real transactions, and truly retaining users.

Are Collector Crypt's Profit Sources Stable?

The core operational model of Collector Crypt is to hold physical graded trading cards in custody and mint corresponding NFTs on Solana. Users who purchase random card packs receive digital cards linked to real physical cards; they can then choose to hold the NFT, sell it on-chain, sell it back to the platform, or redeem the physical card.

Collector Crypt's revenue mainly comes from random card pack sales, secondary market transaction fees, and royalties; when calculating revenue, it also deducts buyback costs incurred when users sell cards back to the platform. Furthermore, Collector Crypt purchases trading cards in bulk, acquiring inventory at discounts of about 5% to 15%; after users open packs, if they don't want to keep the cards, they can sell them back to the platform at a price roughly 7% to 15% below market value.

This allows Collector Crypt to retain an operating profit margin of about 4% to 5%. According to estimates, for a $1,000 card pack, Collector Crypt's comprehensive profit margin is about 5.14%; after deducting incentive costs such as user rewards, the net profit margin is about 4.44%.

This model has garnered attention because it's not just about selling on-chain pictures, but about connecting on-chain transactions with real-world collectibles. Collector Crypt surpassed $1 billion in cumulative trading volume in May 2026; the platform opened over 215,000 tokenized trading card packs in a single week, and more than 30% of users have redeemed physical cards.

Solana's Revenue Ranking Has Not Fully Reversed

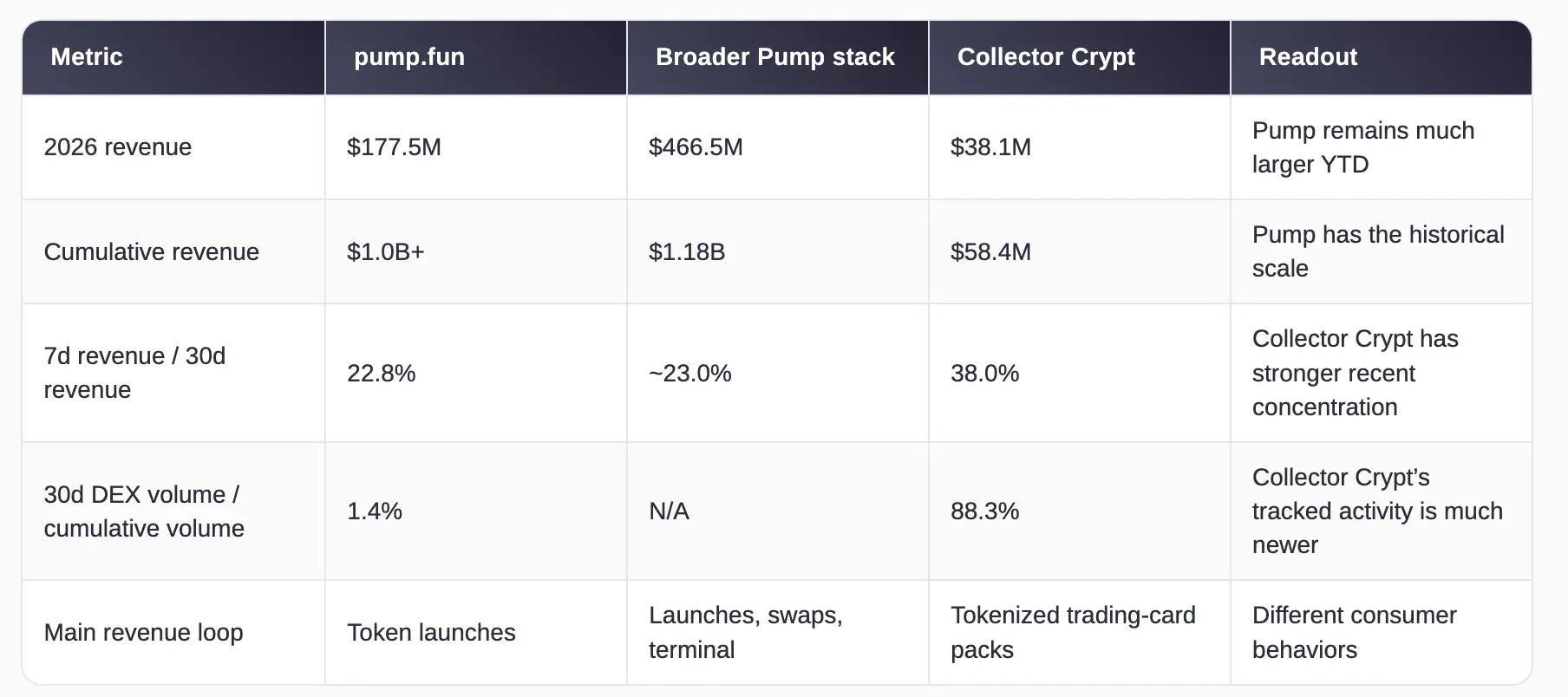

However, Collector Crypt has not truly replaced Pump.fun in terms of total volume. So far in 2026, Pump.fun's revenue is about $177.5 million, and the overall Pump ecosystem revenue is about $466.5 million; in comparison, Collector Crypt's 2026 revenue is about $38.1 million. In cumulative revenue, Pump.fun exceeds $1 billion, the overall Pump ecosystem is about $1.18 billion, while Collector Crypt is about $58.4 million.

Therefore, the so-called "change of hands on the revenue throne" more accurately describes a narrative shift in recent revenue momentum and daily revenue rankings, rather than a complete reversal in historical cumulative scale.

Pump.fun's model relies on a speculative token-issuance cycle: users continuously issue new tokens, trade on early price curves, then some tokens enter public markets, generating fees at various stages. Collector Crypt's model is another type of consumer cycle: users buy random card packs, receive on-chain vouchers corresponding to physical collectibles, and then engage in on-chain trading, instant sell-back, or physical redemption. Both can generate fees, trading volume, and market attention, but they attract users for different reasons.

Pump.fun leans more towards attention, volatility, and early meme coin positions; Collector Crypt leans more towards collecting, scarcity, gamified experience, and real-world asset anchoring. This is also where the focus of the discussion about Solana's consumer applications is changing: revenue is no longer just from meme coin issuance, but can also come from collectible consumption closer to real-world assets.

Conclusion

Finally, the sustainability of Collector Crypt's revenue first depends on whether demand for random card packs can be maintained. If pack demand remains strong, Collector Crypt's 30-day revenue may continue to approach that of Pump.fun; if demand for random card packs cools, the recent high concentration of Collector Crypt's revenue could turn from a growth signal into a risk.

Additionally, the second growth variable for Collector Crypt is whether it can expand from Pokémon cards to sports cards and other collectibles. Data indicates that Pokémon cards currently dominate Collector Crypt's monthly trading volume; but at physical card shows, sports cards and Pokémon card sales are roughly split 50/50, while on-chain sports cards currently only account for 3% to 4% of Collector Crypt's $88 million monthly trading volume.

The third variable for Collector Crypt is regulatory pressure. If multiple jurisdictions begin to scrutinize the random card pack mechanism using a "loot box regulatory framework," it could slow Collector Crypt's growth.

Therefore, barring changes in the macro environment, Pump.fun will likely remain the larger revenue engine, while Collector Crypt will continue to appear at the top of Solana application revenue rankings. In this scenario, consumer application revenue on Solana will no longer rely solely on meme coin issuance but will gradually diffuse into more consumer scenarios.

The key change for Solana is not that Pump.fun has been completely replaced, but that the consumer revenue structure has broadened. Pump.fun proved that meme coin issuance can become a highly revenue-generating consumer application on Solana; Collector Crypt proves that tokenized physical collectibles can also form real revenue, real transactions, and real user behavior.