Author: James Butterfill (Head of Research, CoinShares)

Compiled by: Deep Tide TechFlow

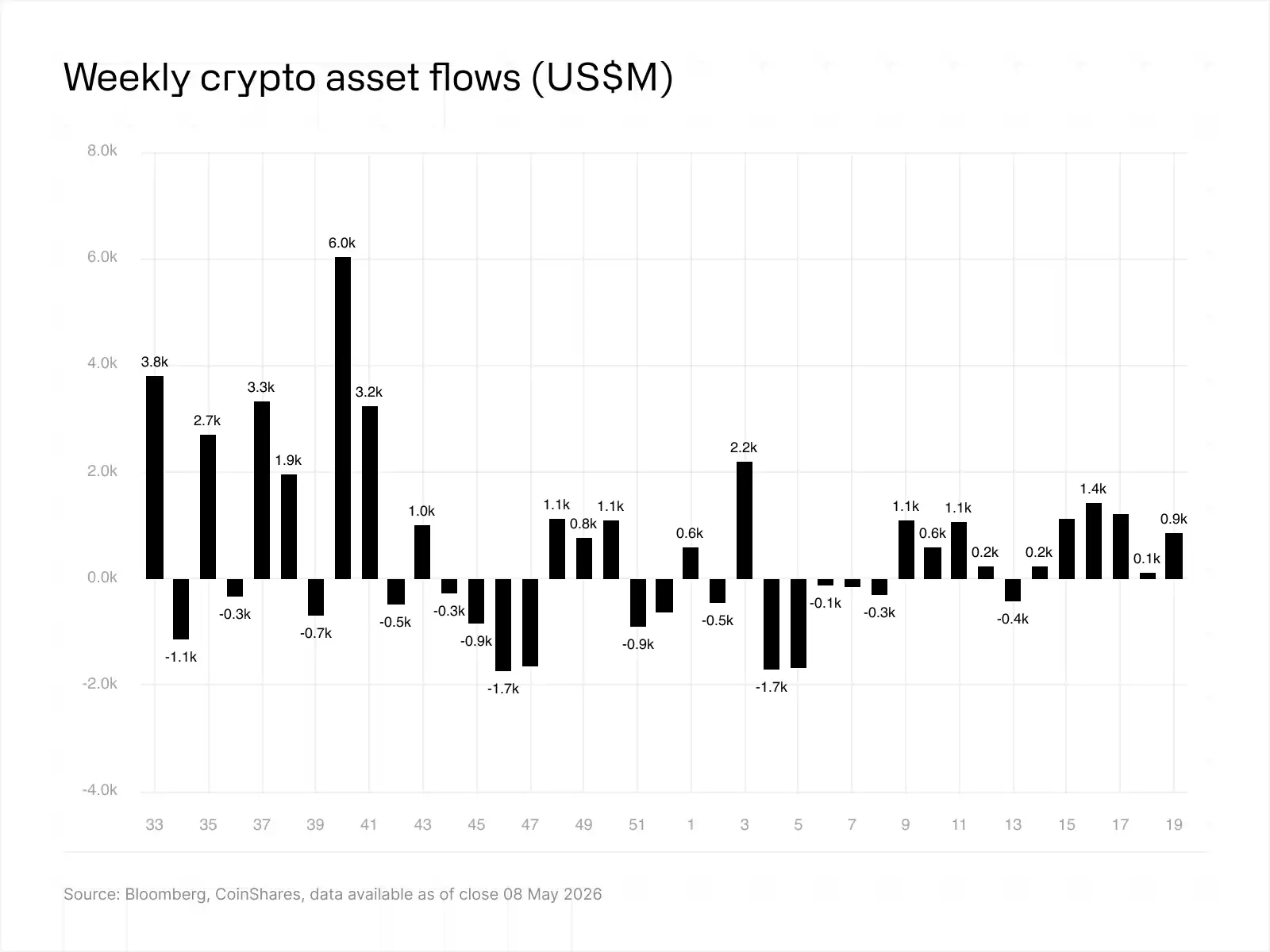

Deep Tide Introduction: The latest weekly report from CoinShares shows that global crypto investment products recorded net inflows of $857.9 million last week, marking the sixth consecutive week of positive flows and the highest single-week inflow since April 24. The direct catalysts were the release of the compromise text for the stablecoin yield provisions in the CLARITY Act and Bitcoin's return above $80,000. Funds from the US market surged to $776.6 million from $47.5 million the previous week. Altcoin participation also expanded simultaneously, with ETH, SOL, and XRP all recording net inflows.

Progress on CLARITY Act Was the Core Variable Driving Fund Flows This Week

Global crypto investment products saw net inflows of $857.9 million last week, marking six consecutive weeks of positive flows and the largest single-week inflow since April 24. James Butterfill, Head of Research at CoinShares, directly attributed this acceleration to legislative progress on the CLARITY Act.

The timeline is clear: On May 1, Senators Tillis and Alsobrooks released the final compromise text for the stablecoin yield provisions; on May 4, the two lawmakers resisted lobbying pressure from the banking industry and maintained the compromise unchanged. A formal markup by the Senate Banking Committee is expected this week.

Bitcoin broke above $80,000 on Monday, reaching a new high since the February pullback. Total Assets Under Management (AUM) rose to $160 billion.

Caption: Weekly Global Crypto Asset Fund Flows, Source: CoinShares

US Fund Rebound Far Exceeds Previous Week

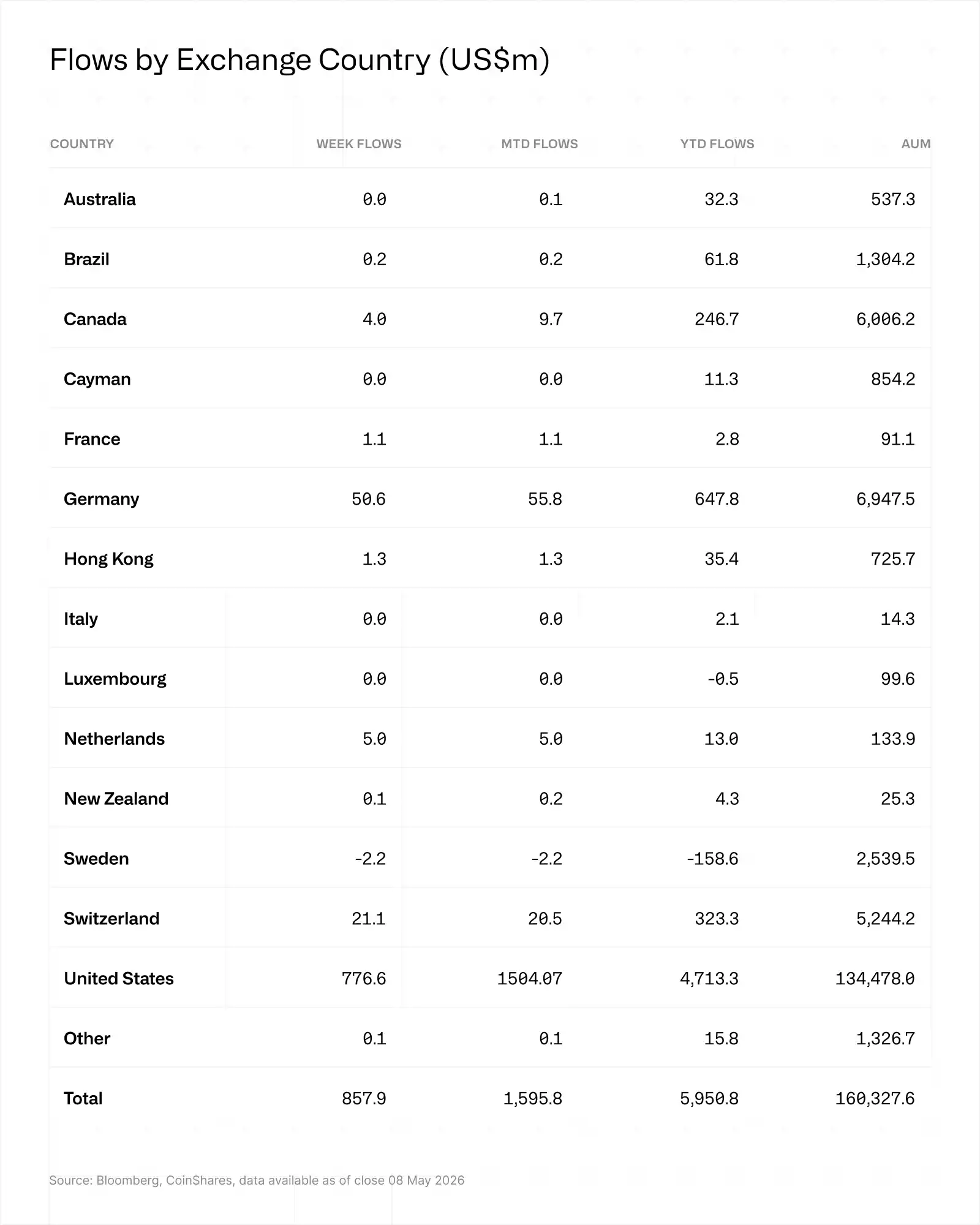

In terms of regional distribution, the United States dominated with net inflows of $776.6 million, showing a sharp rebound compared to the $47.5 million from the previous week.

Europe also showed improvement. Germany recorded $50.6 million, slightly higher than the previous week; Switzerland saw $21.1 million, and the Netherlands $5 million. Butterfill believes this indicates that while the buying momentum has returned to the US, there is also broader participation emerging in Europe.

Caption: Fund Flows by Listing Country, Source: CoinShares

BTC Leads, Short Positions Accelerate Unwinding

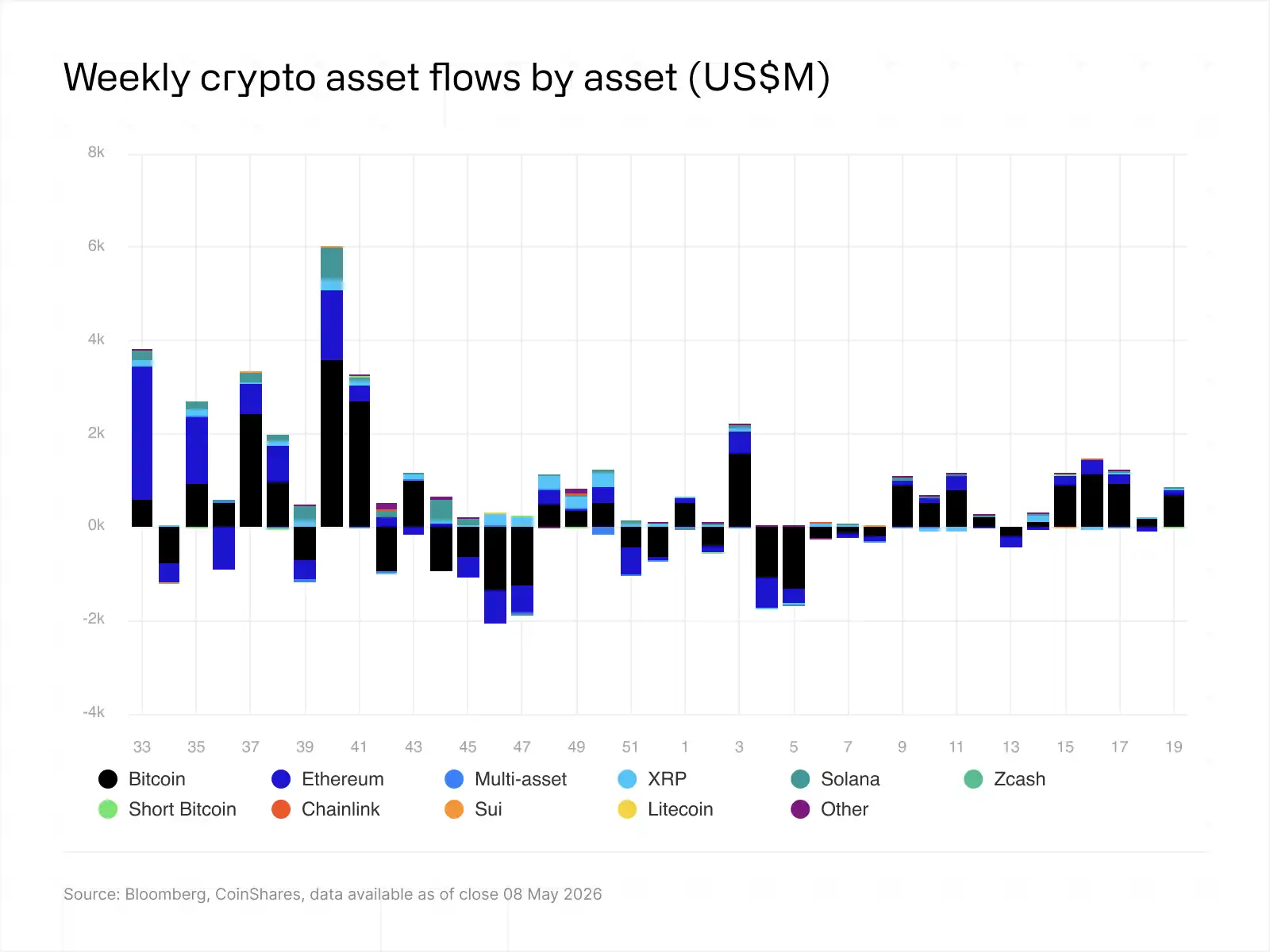

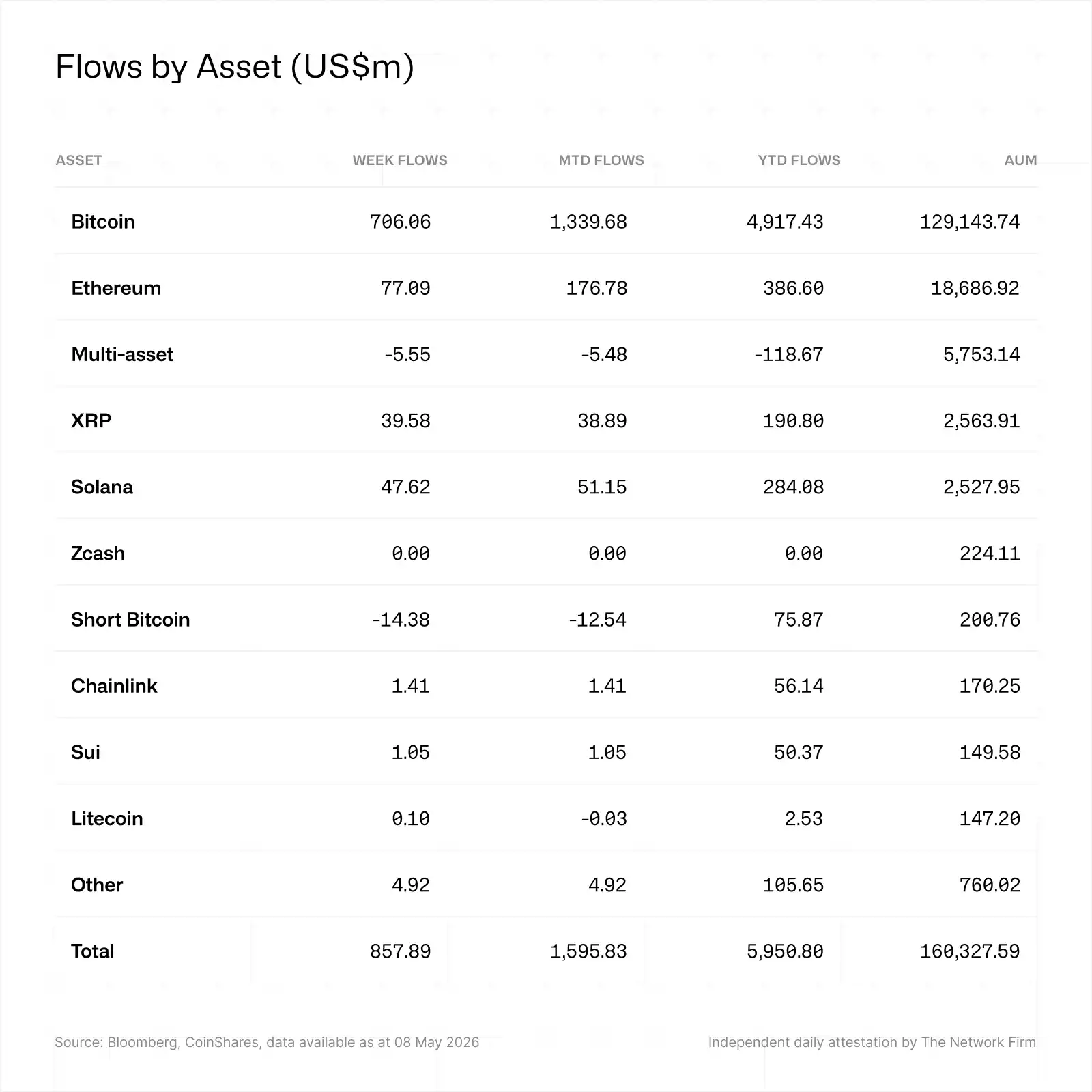

Bitcoin products absorbed $706.1 million last week, bringing year-to-date cumulative inflows to $4.9 billion.

A noteworthy signal to unpack: Short-bitcoin products saw net outflows of $14.4 million last week, the largest single-week outflow in 2026. This suggests hedge positions are being unwound, indicating growing institutional confidence in the rebound.

Altcoins Rebound Across the Board, ETH Reverses Previous Week's Outflow

Ethereum products saw net inflows of $77.1 million, completely reversing the net outflow of $81.6 million from the previous week. Solana recorded $47.6 million, and XRP saw $39.6 million, both showing a significant acceleration compared to recent activity levels.

The only category with noticeable outflows was multi-asset products, with a net outflow of $5.5 million.

Caption: Weekly Fund Flows by Asset Class, Source: CoinShares

Caption: Detailed Fund Flows by Asset, Source: CoinShares

Caption: Assets Under Management Ranked by Specific Asset, Source: CoinShares