• The cryptocurrency market shifted from a rally at the beginning of May to a mid-month pullback and low-volatility consolidation at the month's end. BTC, ETH, and SOL all formed interim highs in early May before entering corrections. Mainstream ETF demand weakened, while perpetual futures trading volume remained high, showing a market structure characterized by weak spot performance and leverage dominance.

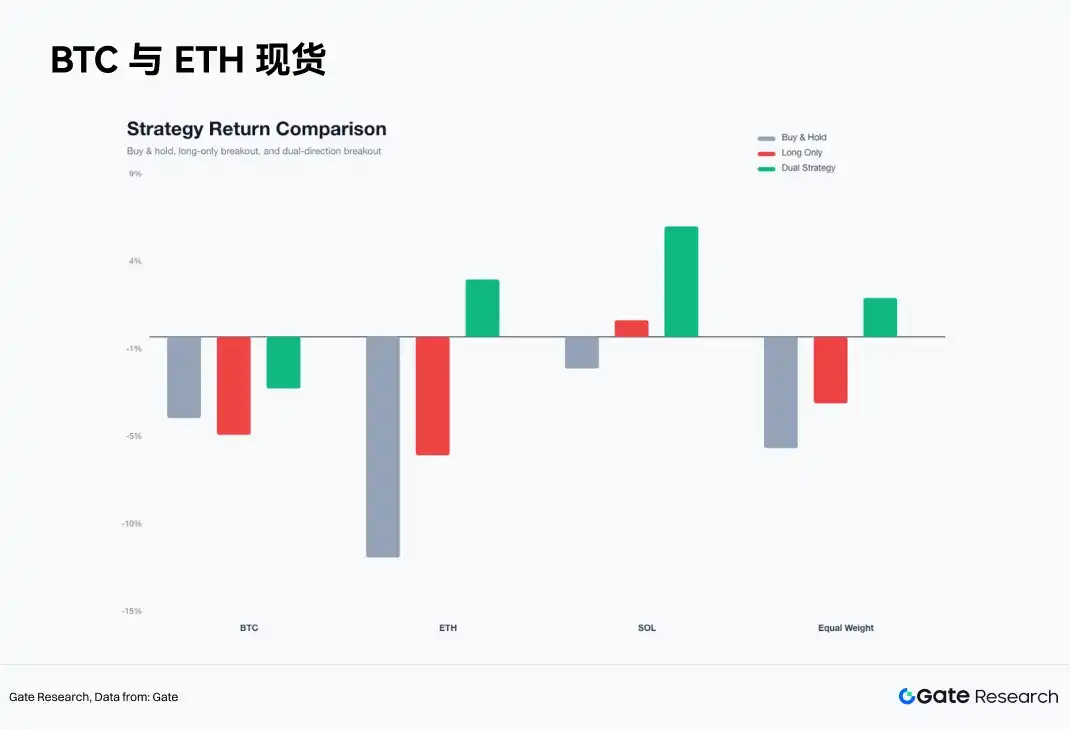

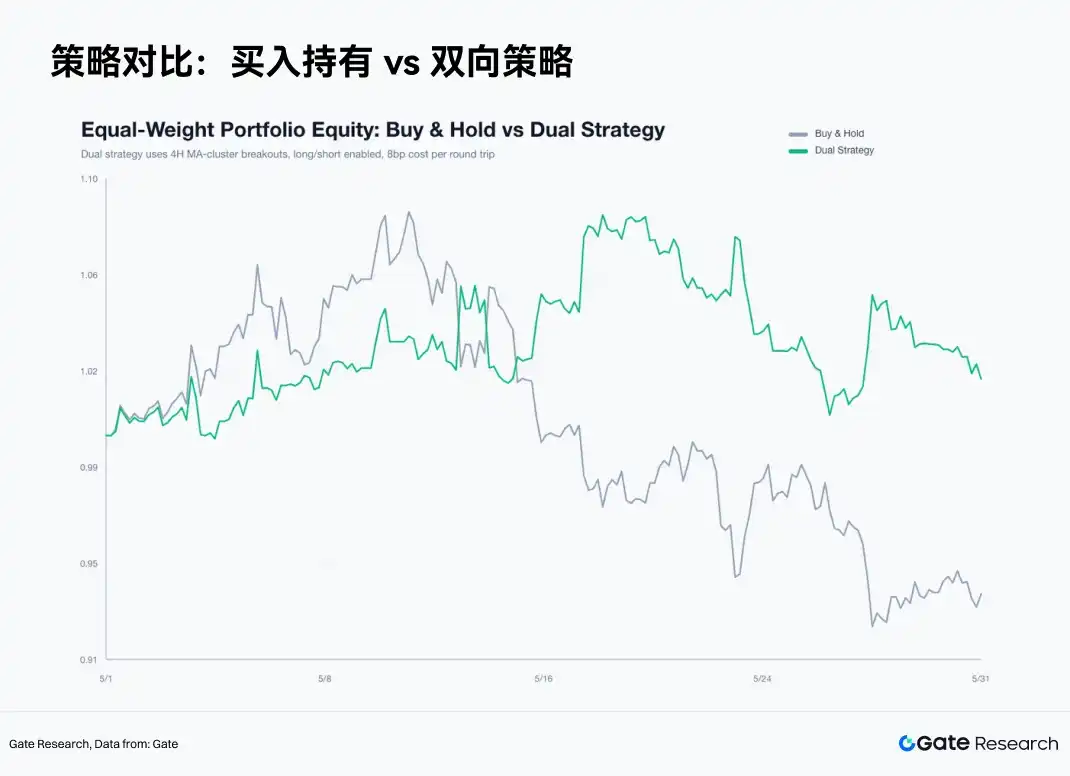

• The two-way moving average cluster breakout strategy performed best. The equal-weighted buy-and-hold return for the three assets was approximately -6.09%, the long-only strategy return was about -3.65%, and the two-way strategy return was about +2.11%. Profits mainly came from short trend phases in ETH and SOL, verifying that the May market was more suitable for two-way trend trading.

• Under low-volatility compression, disciplined trading outperforms subjective judgment. The EMA12 exit mechanism effectively controlled false breakout losses, and the 3R take-profit preserved trend gains. The current market remains in a phase of directional selection; identifying the state, controlling risk, and executing two-way signals is a superior trading framework to subjectively chasing rallies.

The primary contradiction in the May crypto market was the divergence between price action and market structure after the initial rally, with weak spot buying and active leverage trading diverging. BTC, ETH, and SOL all formed interim highs in early May before entering pullbacks and low-volatility consolidation. BTC retreated from its 4H closing price of $77,117.4 at the start of the month to $73,684.0 at the month's end, a monthly return of -4.45%. ETH fell from $2,283.02 to $2,007.0, a monthly return of -12.09%. SOL retreated from $83.90 to $82.44, a monthly return of -1.74%. SOL's closing decline was smaller, but it reached a high of $98.40 during the month before retreating to around $80.00, indicating significantly higher intra-month trading volatility than suggested by its monthly return.

The strategy backtest results for the month are clear. The equal-weighted buy-and-hold return for the three assets was approximately -6.09%; the long-only moving average cluster breakout strategy return was about -3.65%; the two-way moving average cluster breakout strategy return was +2.11%. The two-way strategy achieved an excess return of about +8.2% compared to buy-and-hold. Profits mainly came from short trend legs after mid-May, with ETH and SOL being the most significant contributors.

The effective trading framework for May was: first, identify moving average cluster compression; then, allow price to complete its directional choice, either up or down; use EMA12 to manage failed signals, a fixed 2.5% stop-loss to limit single-trade losses, and a 3R take-profit (3 * 2.5%) to preserve trend gains. This framework suited May's market structure of low win rate, high reward-to-risk ratio, and concentrated trend legs.

U.S. stock market factors reinforced this view. In May, AI-heavyweight stocks had earnings and industry momentum support. Nvidia reported strong quarterly earnings, with Q1 FY2027 revenue around $81.6 billion, and its market cap briefly touched the $5 trillion milestone again. The correlation between BTC and the S&P 500 remains high, with public samples showing the 30-day correlation reached about 0.74 within 2026 and was still around 0.6 near the end of May. Cryptocurrency assets did not detach from the U.S. stock market risk budget framework in May. Continuous BTC ETF outflows, weakening ETH ETF demand, and a high share of perpetual trading volume collectively led to crypto underperformance compared to U.S. tech giants.

I. Market Structure: Early-Month Rally, Mid-Month Weakness, End-Month Low Volatility

The first phase of May occurred from May 1st to May 6th. BTC rose from $77,117.4 to $82,828.2, ETH rose from $2,283.02 to $2,423.99, and SOL extended its rally to touch $98.40 on May 11th. During this phase, short-term moving average clusters shifted upward, volatility was within a controllable range, and the market exhibited characteristics of a recovery rally. SOL showed leading elasticity, indicating a willingness among capital to take higher risk exposure at the start of the month.

The second phase began on May 7th. BTC failed to stabilize above $82k, ETH could not sustain above $2,400, and SOL formed its monthly high near $98. Upside breakout signals began to fail frequently, with prices falling back to the EMA12 and repeatedly triggering exits. Long trades in BTC triggered stop-losses after May 14th, long trades in ETH consistently failed after May 6th, and SOL entered a clear downtrend leg after May 15th.

The third phase concentrated from May 22nd to the month's end. BTC moved down to around $73k, ETH approached $2,000, and SOL returned to around $82. Price volatility narrowed, moving average cluster width decreased, and the market entered a new state of compression.

Intra-month drawdowns verified asset roles. BTC's maximum intra-month drawdown from high to low was about 12.5%, ETH's was about 18.8%, and SOL's was about 18.7%. BTC serves as the risk anchor, while ETH and SOL act as amplifiers of risk appetite. After BTC weakened, ETH and SOL's drawdowns were faster; at a strategic level, this necessitates reducing the long-side weighting of high-Beta assets.

II. Capital Structure: Stablecoins Remain, Mainstream ETF Demand Weakens

As of May 31st, the total market cap of stablecoins was approximately $3.2 trillion, and DeFi TVL was about $2.51 trillion. The underlying US dollar liquidity did not experience a systemic retreat. CEX 24-hour spot trading volume was approximately $1.242 trillion, while CEX perpetual trading volume was about $8.944 trillion, with perpetual volume being roughly 7.2 times that of spot volume. Price discovery is increasingly borne by the derivatives market.

ETF flows became a significant pressure point in the latter half of May. Public news indicates that BTC spot ETFs experienced net outflows for nine consecutive trading days, totaling about $2.8 billion, including a single-day net outflow of approximately $649 million at one point, with BlackRock's IBIT seeing a single-day outflow of about $448 million. ETH ETFs also faced pressure, with a net outflow of about $241 million in the last week of May.

However, capital did not completely leave the crypto asset space. Altcoin ETFs like SOL and XRP saw small net inflows, and new ETF narratives like HYPE also gained attention. Capital migrated from mainstream BTC and ETH ETFs towards thematic ETFs and higher-beta assets. This structure indicates the core issue was cooling demand for mainstream spot assets, with capital participating in local rotations and short-term trades.

Derivatives data is consistent with this. Active buy/sell ratios for BTC, ETH, and SOL were all below 1, indicating slightly stronger active selling pressure. Funding rates were around 0.01%, not reaching extreme crowding levels. The May market was in a typical state: active leverage trading, insufficient spot follow-through, weak active buying pressure, and price breakouts prone to turning into false moves.

III. U.S. Stock Linkage: AI Giants Support Nasdaq, Crypto ETF Outflows Create Pressure

May's crypto performance must also be viewed within the U.S. stock market risk appetite framework. The correlation between BTC and the S&P 500 remained high, with the 30-day correlation reaching around 0.74 within 2026 and still around 0.6 near the end of May. On a broader scale, BTC behaved as a high-Beta risk asset this month, lacking stable, independent safe-haven characteristics.

The core support on the U.S. stock side came from AI and large-cap tech stocks. Nvidia reported strong quarterly earnings in May, with Q1 FY2027 revenue around $81.6 billion; its stock price hit new all-time highs and briefly retouched the ~$5 trillion market cap milestone. AI-heavyweight stocks supported Nasdaq risk appetite through earnings confirmation. Cryptocurrency assets lack a comparable earnings anchor, with prices influenced by ETF flows, derivatives leverage, and liquidity expectations.

This cross-asset divergence impacted May strategy results. U.S. tech giants have earnings drivers, while BTC and ETH mainstream ETFs saw outflows, leading to a reallocation of capital within large risk assets. Traditional capital continued buying AI giants with higher earnings certainty, reducing willingness to allocate to BTC ETFs. Crypto long breakouts lacked spot demand, causing high-volume breakouts to easily turn into sell-the-news events.

May's macro data calendar also compressed the risk budget. Key monthly data included NFP, CPI, PPI, the second GDP estimate, and PCE. Employment, inflation, and growth data directly impacted U.S. Treasury yields, the dollar, and Nasdaq valuations, which then transmitted to BTC ETF flows and perpetual funding rates. Towards month-end, the market began focusing on early June data releases like employment, ISM, JOLTS, ADP, as well as the FOMC meeting and options expiry. Crypto's low-volatility compression occurred around these events; position unwinding and reduced risk budgets are plausible explanations.

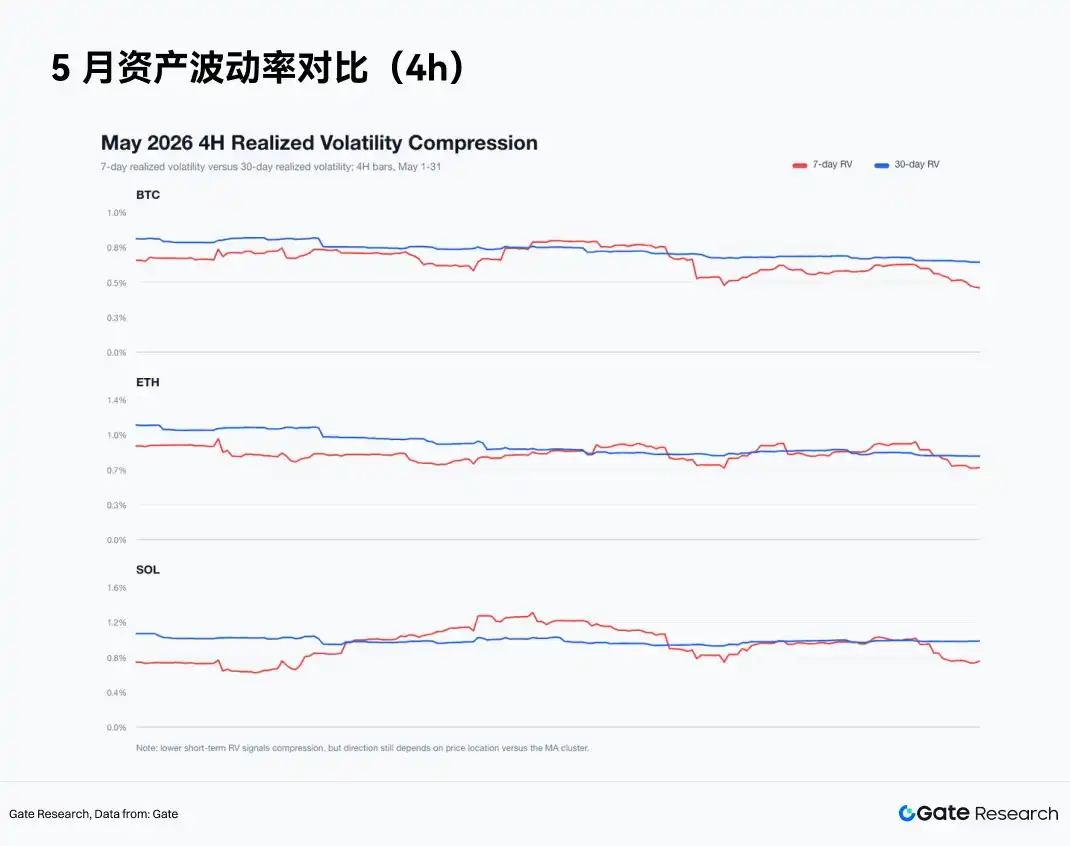

IV. Volatility: Short-Term Compression Forms, Price Strength Lacking

By the end of May, BTC's 7-day 4H realized volatility was approximately 0.46%, and its 30-day 4H realized volatility was about 0.64%; ETH's were around 0.7% and 0.81% respectively; SOL's were around 0.76% and 1% respectively. Short-term volatility for all three major assets was lower than medium-term volatility, indicating the market had entered low-volatility compression.

Low-volatility compression suggests the market is approaching a directional choice, but does not imply an upward breakout. At May's end, BTC closed at $73,684.0, with the EMA12 around $73,776.35; ETH closed at $2,007.0, with the EMA12 around $2,016.34; SOL closed at $82.44, with the EMA12 around $82.39. BTC and ETH remained in weak territory, while SOL had just returned near the EMA12. Price strength is insufficient; low volatility appears more like consolidation after a decline.

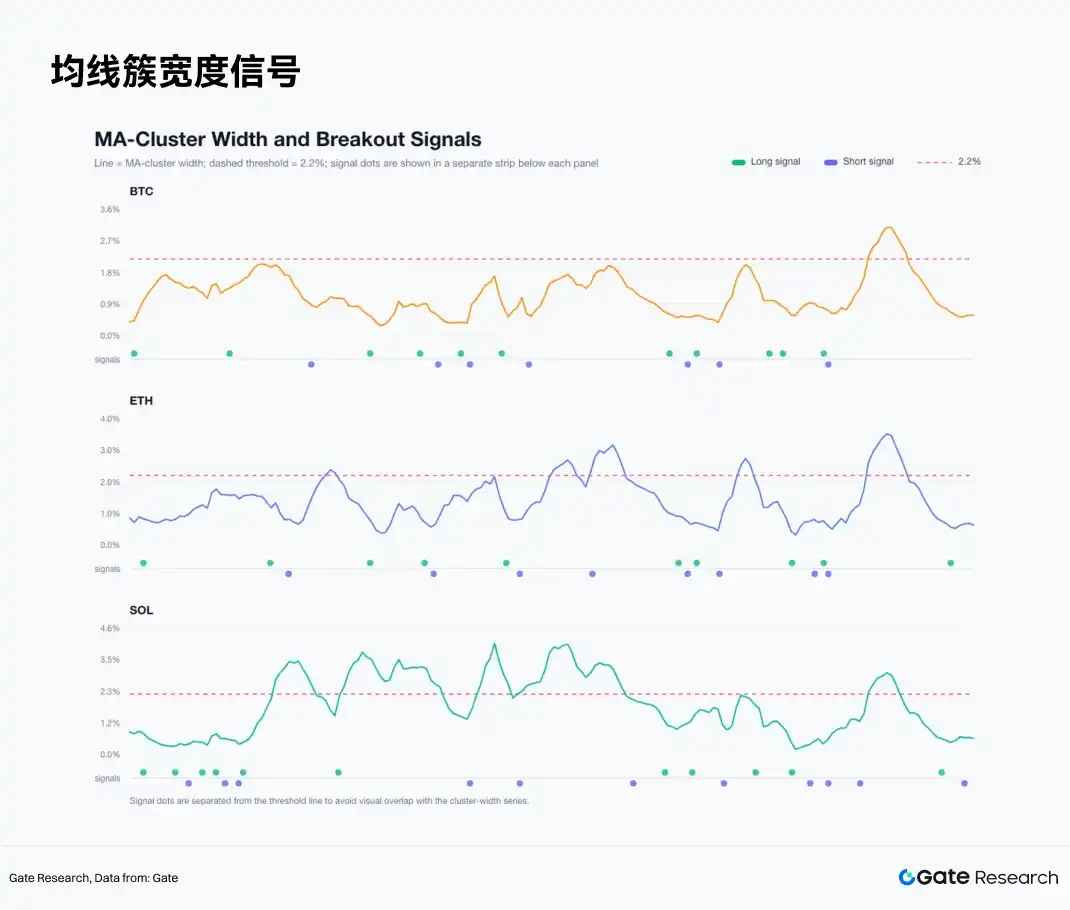

Moving average cluster width shows a similar state. At month-end, BTC's cluster width was about 0.57%, ETH's about 0.63%, and SOL's about 0.58%, all below the 2.2% strategy threshold. This environment frequently triggers breakout signals. May's data shows that after moving average cluster compression, two-way trading must be permitted. Trading only long breakouts systematically misses downtrends.

V. Strategy Backtest: 4H Moving Average Cluster Compression Breakout System

The strategy uses six moving averages to form a cluster: EMA6, EMA12, EMA24, SMA6, SMA12, SMA24. The cluster width equals the maximum value minus the minimum value of the six moving averages, divided by the current closing price. If the previous candle's cluster width is below 2.2% and the current candle closes above the cluster's upper bound, go long at the next 4H open. If the previous candle's cluster width is below 2.2% and the current candle closes below the cluster's lower bound, go short at the next 4H open.

Exit rules are fixed. Exit long positions if price closes below the EMA12. Exit short positions if price closes above the EMA12. Single-trade stop-loss is set at 2.5%, and take-profit is set at 3R, i.e., 7.5%. If both take-profit and stop-loss are triggered on the same candle, priority is given to stop-loss. A round-trip transaction cost of 8 basis points is deducted. Any open position at month-end is closed at the last 4H closing price.

This report tests two strategy variations. The long-only version only trades upside breakout signals. The two-way version trades both upside and downside breakout signals. May's results show the two-way version better fits the market state.

5.1 Long-Only Strategy: Quality of Upside Breakout Signals Declines

The long-only strategy was largely ineffective. BTC had 11 trades, a return of -5.36%, a win rate of 18.2%, and a maximum drawdown of -10.08%. ETH had 10 trades, a return of -6.49%, a win rate of 10.0%, and a maximum drawdown of -10.64%. SOL had 11 trades, a return of +0.91%, a win rate of 18.2%, and a maximum drawdown of -7.11%.

BTC's long-only profits were concentrated in the first two trades. Entry on May 1st, exit on May 4th, net profit +2.09%. Entry on May 4th, exit on May 7th, net profit +0.92%. Signal quality declined afterward; the long trade entered on May 14th triggered a stop-loss, net loss -2.58%.

ETH's long-only performance was weakest. Entry on May 1st to exit on May 5th, net profit +3.17%. All subsequent 9 long trades resulted in losses. ETH's upside breakouts were mostly weak rebounds, not trend expansions.

SOL's long-only strategy generated a slight profit, coming from two trades. Entry on May 5th, exit on May 8th, net profit +3.95%. Entry on May 8th, triggered 3R take-profit on May 10th, net profit +7.42%. Most other signals were losing trades. SOL was the only asset with a positive return via the long-only strategy this month, with profits highly concentrated.

5.2 Two-Way Strategy: Short Trend Legs Contribute Most Profits

The two-way strategy significantly improved results. BTC's two-way strategy return was -2.83%, ETH's was +3.14%, and SOL's was +6.05%. The equal-weighted two-way strategy return for the three assets was +2.11%, compared to an equal-weighted buy-and-hold return of about -6.09% over the same period.

BTC's two-way strategy still resulted in a loss, but the loss magnitude was smaller than the long-only strategy. BTC had 18 trades total, a win rate of 22.2%, and a maximum drawdown of -10.74%. Two short trades contributed most: short entry on May 15th, exit on May 20th, net profit +2.35%; short entry on May 26th, exit on May 30th, net profit +3.42%. BTC had numerous false signals in mid-May, causing losses from frequent long/short switches.

ETH's two-way strategy returned +3.14%, with 18 trades, a win rate of 38.9%, and a maximum drawdown of -8.26%. Key trades were: short on May 15th, triggered 3R take-profit on May 17th, net profit +8.03%; short on May 26th, exit on May 29th, net profit +2.68%. ETH's long signals failed, with short legs constituting the main profits.

SOL's two-way strategy returned +6.05%, with 22 trades, a win rate of 22.7%, and a maximum drawdown of -8.17%. SOL provided both long and short trend trades. Long on May 8th, triggered 3R take-profit at 16:00 on May 10th, net profit +7.42%. Short on May 15th, triggered 3R take-profit on May 17th, net profit +8.03%. SOL's trend elasticity was strongest, but trading noise was also highest.

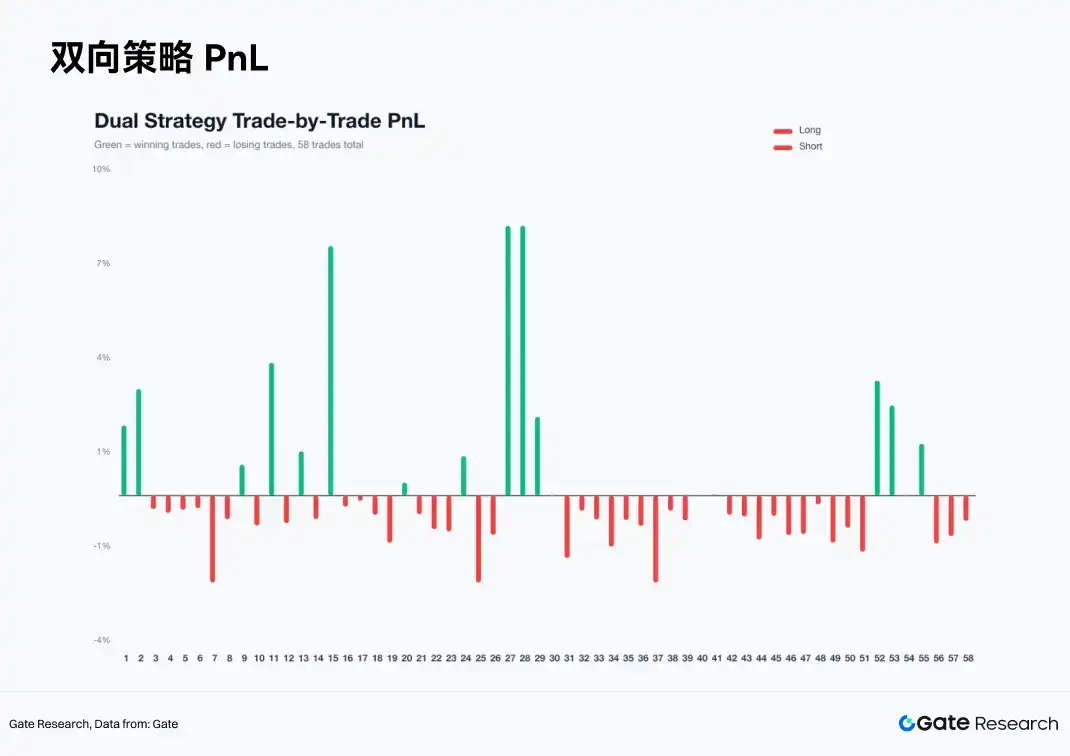

5.3 Trade Distribution: Low Win Rate Structure, Few Large Trades Determine Profits

Among all 58 trades in the two-way strategy, the number of profitable trades was limited. BTC's win rate was 22.2%, ETH's was 38.9%, and SOL's was 22.7%. Strategy profits came from a few large trend trades, while losses were controlled by the EMA12 exit and fixed stop-loss.

Cumulative profit per trade shows the strategy's net value oscillated upward in early May, was boosted in mid-May by ETH and SOL short trades, and continued to benefit from BTC and SOL short trades in late May. Losses concentrated during phases of frequent long/short switching. The system is characterized by low win rate and high reward-to-risk ratio, suitable for markets with clear trend legs, not dense consolidation.

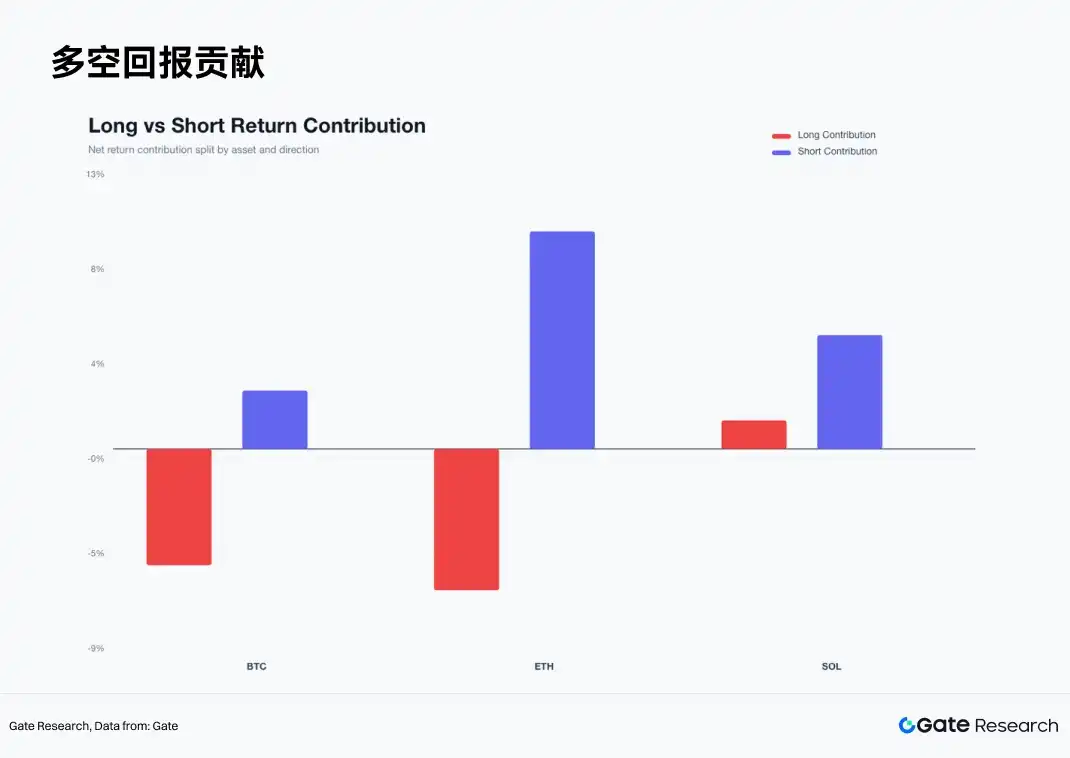

A breakdown of long/short contributions further clarifies the profit source for the month. BTC's long-side contribution was negative, short-side positive. ETH's long-side contribution was negative, short-side significantly positive. SOL had positive contributions from both long and short sides, with the short side more stable. May's main theme was a downtrend following failed rallies.

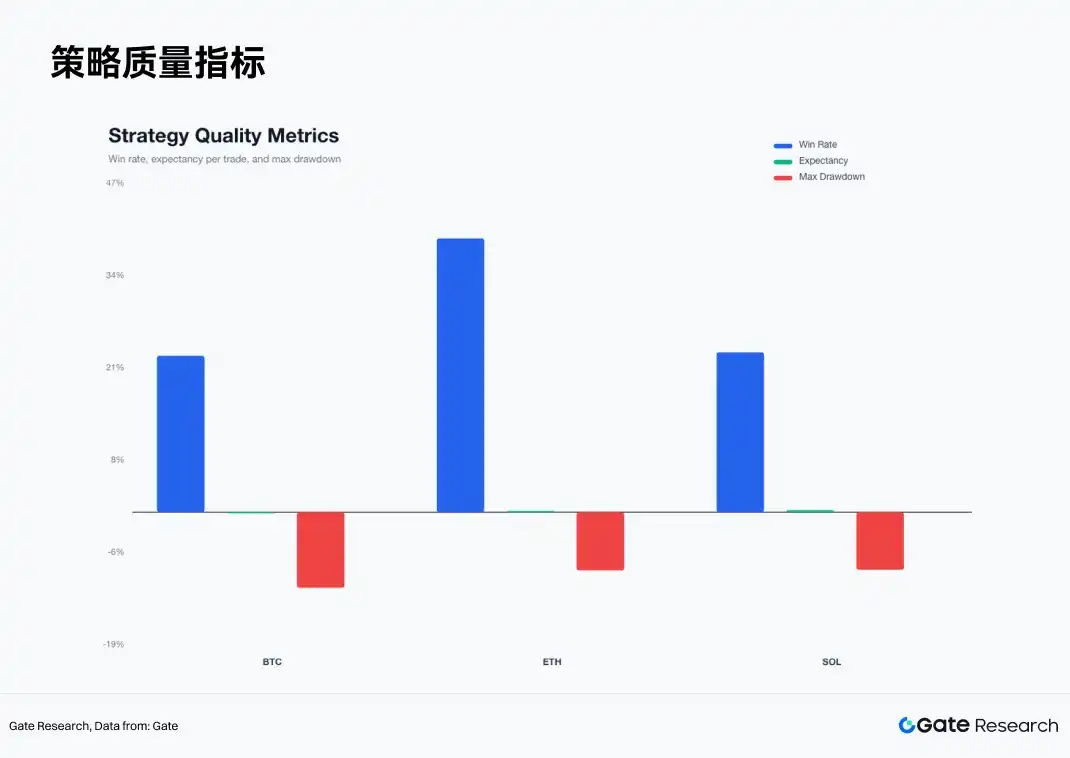

Win rate, expected return per trade, and maximum drawdown show SOL had the highest single-trade expectation, followed by ETH, with BTC weakest. BTC had the highest density of false breakouts, ETH's direction was cleaner, and SOL's elasticity was strongest.

5.4 Exit Mechanism: EMA12 Controls Noise, 3R Preserves Trend Profits

Analysis of exit reasons shows the EMA12 exit accounted for the highest proportion. Many trades did not end via stop-loss but exited when the failed breakout returned near the EMA12. The EMA12 rule reduced holding time and loss expansion from erroneous signals.

The number of stop-loss trades was limited, but losses were concentrated. The number of 3R take-profit trades was very small, but profit contribution was significant. This structure aligns with trend-following strategy patterns: most trades are small losses or small gains, with a few trend trades contributing the majority of profits. In May, removing the 3R take-profit would have prematurely cut SOL and ETH's large profitable trades; removing the EMA12 exit would have expanded losses during consolidation phases.

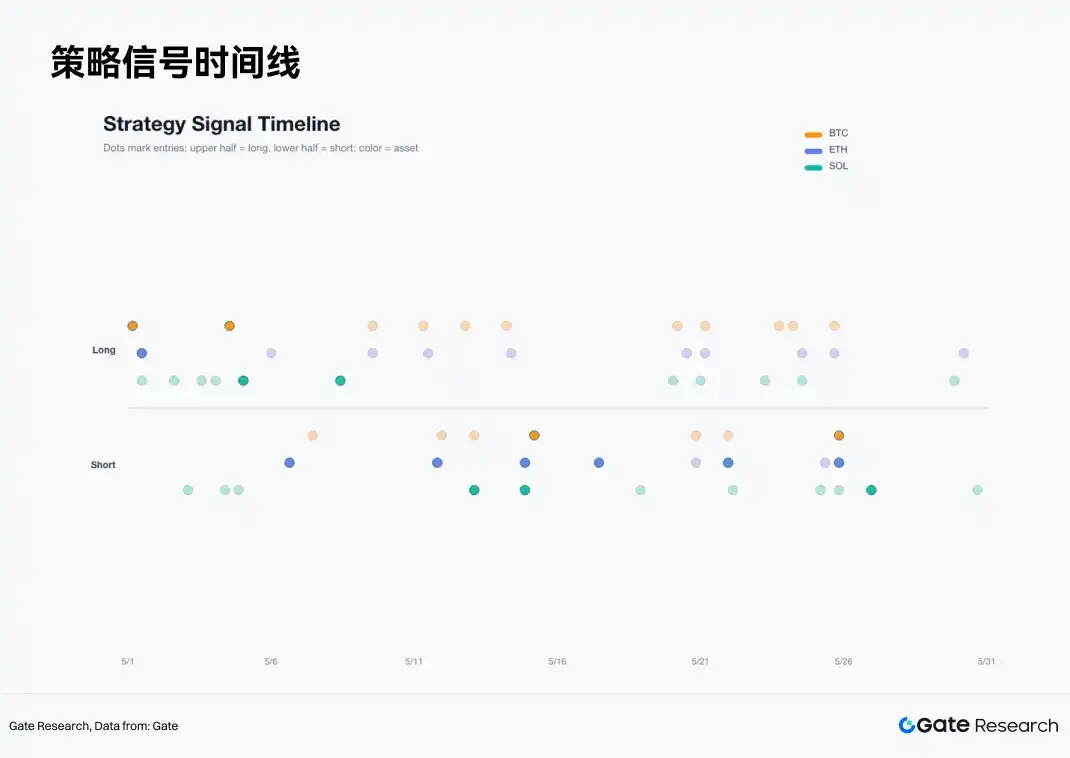

The signal timeline shows dense long signals in early May, increasing short signals in mid-May, and alternating long/short signals in late May. Dense signals do not equate to dense opportunities; truly effective signals concentrated in short windows with clear direction.

5.5 Enhanced Filter Failure: Volume Breakouts Were Traps in May

The report also tested an enhanced filter version. Conditions included: 7-day volatility not exceeding 1.15 times the 30-day volatility, volume not below 0.9 times the 20-period (1 period = 4 hours) average volume, long signals near the 20-period high, short signals near the 20-period low. This version performed worse. BTC's enhanced two-way strategy return was -3.40%, ETH's was -5.03%, SOL's was -2.58%, and the equal-weighted three-asset return was -3.63%.

The failure reason was that May's volume breakouts often occurred near interim tops. BTC's enhanced long signal on May 4th entered at $80,322.9, triggered stop-loss within 4 hours, net loss -2.58%. ETH's enhanced long signal on May 6th entered at $2,410.39, triggered stop-loss on the same candle, net loss -2.58%. SOL's enhanced long signal on May 4th also triggered stop-loss.

High volume indicates participation, not quality of capital. In May, high volume more often resulted from topping churn, leverage liquidations, and short-term chasing. Effective filters should incorporate ETF flows, spot trading volume share, active buy/sell ratios, perpetual trading volume share, and U.S. stock market risk appetite. Price and volume alone can identify volatility, not trend sustainability.

5.6 Per-Asset Conclusions

BTC is the State Anchor. BTC's monthly decline was smaller than ETH's, and its drawdown was more controlled. BTC's two-way strategy return of -2.83% indicates BTC itself was not the best asset for returns in May. It is better suited for gauging overall market risk budgets. If BTC cannot reclaim the EMA12 and 30-period moving average area, long-side weighting for ETH and SOL should be reduced.

ETH is the Weakness Mainstream. Monthly decline of -12.09%, extremely low win rate for long breakouts, two-way strategy reliant on short-side profits. ETH failed near $2,400 and broke down through $2,300, $2,200, $2,100 successively. It first needs to repair the $2,100 to $2,200 zone before long-side weighting can be reassessed.

SOL is the Trading Asset. Monthly closing decline was only -1.74%, but the intra-month path was very volatile. SOL's two-way strategy return of +6.05% was significantly higher than BTC and ETH. SOL is suited for trend following, not passive holding. Low win rate, high elasticity, and concentrated trend trades were SOL's core characteristics in May.

5.7 June Strategy Framework

Continue using the two-way 4H moving average cluster breakout system in June. Reduce weighting for one-sided long chasing. Use BTC as a state filter, with ETH and SOL as profit assets confirmed by relative strength. If BTC reclaims the EMA12 and 30-period moving average area, while ETF outflows slow and active buy/sell ratios return above 1, long signal weighting can be increased. If BTC remains below the $74k-$76k zone, the market is still in a weak recovery state.

Keep the U.S. stock filter layer. If Nasdaq and AI leaders remain strong while BTC ETF outflows slow, it indicates improving cross-asset risk budgets. If Nasdaq is strong while BTC ETF outflows persist, it suggests capital favors U.S. tech giants with higher earnings certainty; caution is still needed on crypto long breakouts. If both U.S. stocks and crypto weaken, priority should increase for short signals on ETH and SOL.

Maintain mechanical position sizing rules. Single-trade risk 2.5%, take-profit 3R, EMA12 exit unchanged. Breakout signals alone should not trigger heavy positions. When spot demand is weak, ETF outflows persist, perpetual trading share is high, and active buying is insufficient, reduce weighting for long breakout signals and increase weighting for short breakout signals.

VI. Conclusion

The May cryptocurrency market completed a state transition from recovery to failure. BTC, ETH, and SOL all rallied early in the month; trend quality deteriorated after mid-month, entering low-volatility compression by month-end. Stablecoin and DeFi underlying liquidity remained, but mainstream ETF demand weakened, derivatives trading gained weight, and price discovery leaned towards leveraged markets.

Strategy results provide a clear answer. Buy-and-hold performed worst; long-only breakouts could not adapt to the trend failure after mid-May; the two-way moving average cluster breakout achieved the best results. Equal-weighted buy-and-hold for the three assets returned approximately -6.09%, long-only about -3.65%, and the two-way strategy +2.11%. Profits came from short trend legs in ETH and SOL, as well as SOL's long trend leg early in the month.

U.S. stock market factors provide a more complete explanation. AI tech leaders still had earnings drivers, with heavyweights like Nvidia supporting U.S. stock risk appetite; BTC and ETH ETFs experienced continuous outflows, weakening demand for mainstream crypto assets. The correlation between BTC and the S&P 500 remained high, indicating the crypto market is still influenced by U.S. stock risk budgets and macro interest rate expectations.

The focus for June trading is not about predicting direction in advance. A superior path is to identify the state, execute two-way signals, control single-trade risk, and preserve trend profits. After moving average cluster compression, both upside and downside breakouts can form valid trades. The EMA12 exit mechanism protects the strategy from being dragged down by false breakouts, while the 3R take-profit allows a few large winners to cover many small losses. In the current environment, a disciplined two-way system is superior to subjective rally-chasing.

References

• Gate, https://www.gate.com/trade/BTC_USDT

• Investor, https://investor.nvidia.com/news/press-release-details/2026/NVIDIA-Announces-Financial-Results-for-First-Quarter-Fiscal-2027/default.aspx

• DeFiLlama, https://defillama.com/stablecoins

• CMC, https://coinmarketcap.com/charts/

• BlackRock, https://www.blackrock.com/us/individual/products/333011/ishares-bitcoin-trust

• Coinglass, https://www.coinglass.com/etf/bitcoin

• K33, https://k33.com/research/articles/waiting-and-seeing

Gate Research Institute is a comprehensive blockchain and cryptocurrency research platform providing readers with in-depth content, including technical analysis, hotspot insights, market reviews, industry research, trend forecasts, and macro-economic policy analysis.

Disclaimer

Investing in the cryptocurrency market involves high risks. Users are advised to conduct independent research and fully understand the nature of purchased assets and products before making any investment decisions. Gate bears no responsibility for any loss or damage caused by such investment decisions.