Author: Prathik Desai

Translation: Chopper, Foresight News

Asset tokenization is merging two distinct financial systems: one is the permissionless, 24/7, and highly volatile world of DeFi; the other is the traditional fund industry, which operates on fixed settlement periods and is only accessible to vetted, accredited investors.

The process of bridging these two worlds is extremely complex. However, whoever builds this critical infrastructure layer stands to capture immense industry value. This article deconstructs who is building this connective layer between on-chain and traditional finance and where the ultimate value will flow.

RWA Scale Continues to Expand

The total value of tokenized real-world assets on-chain has surpassed $33 billion, with tokenized U.S. Treasury bonds accounting for approximately $15 billion. Interestingly, in just one year, the share of U.S. Treasuries within the total RWA pie has shrunk from 55% to less than 45%. Newer forms of tokenized funds, such as institutional credit (e.g., ACRED by Apollo) and private credit (e.g., JAAA by Janus Henderson), are experiencing rapid growth.

The maturation of asset tokenization provides corporate treasurers and CFOs with tools for layered risk allocation. Institutions seeking low volatility, high liquidity, and modest returns can opt for Treasury-backed token products. Entities pursuing higher yields and programmability can allocate to higher-risk categories. Today, these underlying Treasury token products are backed by reports from the Big Four auditing firms, meaning security of yield is no longer the primary concern.

If someone asks me what the difference is between on-chain assets and traditional assets, the answer is composability. Leveraging this composability, the same dollar can circulate across multiple channels to generate value, achieving compounded returns. Instant redemptions and multi-channel capital reuse make tokenized funds akin to traditional asset management products with added leverage.

In the traditional financial system, it is difficult to simultaneously achieve high yield, liquidity, and capital turnover speed. A well-operated tokenized product can excel in all three aspects. However, the barrier for "well-operated" is exceedingly high. Bridging the composability between traditional funds and on-chain DeFi presents numerous engineering and regulatory challenges.

Stitching Together Two Distinct Worlds

Blockchain brings the advantages of rapid settlement and low costs to tokenized real-world assets. However, the essence of a tokenized money market fund remains that of a regulated asset management product, not a stablecoin.

It still requires updating its net asset value (NAV) once per business day, according to the fund manager's schedule. It still needs to maintain a KYC-verified holder base. For example, BlackRock's BUIDL has a minimum investment threshold of $5 million, while Circle's USYC is restricted to non-U.S. persons. It still must adhere to redemption cutoff times because the settlement of its underlying Treasury securities relies on off-chain infrastructure, which typically has a cut-off time of 5:00 PM Eastern Time.

These are hard requirements that cannot be circumvented. Removing daily NAV pricing would strip the product of its classification as a money market fund. Opening up permissionless trading would invite immediate regulatory scrutiny from the SEC.

So, how can fund share tokens achieve internet-speed transferability while the fund itself retains its fixed NAV update cycle, accredited investor restrictions, and redemption time windows? The industry requires dedicated infrastructure to handle periodic NAV accounting, phased settlements, and strict cross-chain compliance isolation. A joint report by LayerZero and Centrifuge outlines such a solution.

Three Core Conflict Points Are Key to Successful Integration

The middle orchestration layer must resolve three fundamental conflicts to enable high-speed circulation of fund assets without crossing regulatory red lines.

The first is price.

How should tokens be priced during the interval between daily NAV updates? Some issuers simply freeze the previous day's NAV, a model prone to arbitrage during intraday interest rate fluctuations. Real-time dynamic pricing better reflects the market but is difficult to reconcile with the traditional fund's daily accounting.

The second is compliance.

Should whitelist verification occur at every transaction step, or be consolidated at the vault layer? If every transfer requires identity verification, tokens cannot be integrated into open DeFi. If a vault wrapping model is adopted—where a vault holds the compliant fund shares and only KYC-ed users can mint circulating receipt tokens—compliance checks are performed once, and the receipt tokens can freely participate in various DeFi protocols. Centrifuge's deRWA framework follows this logic.

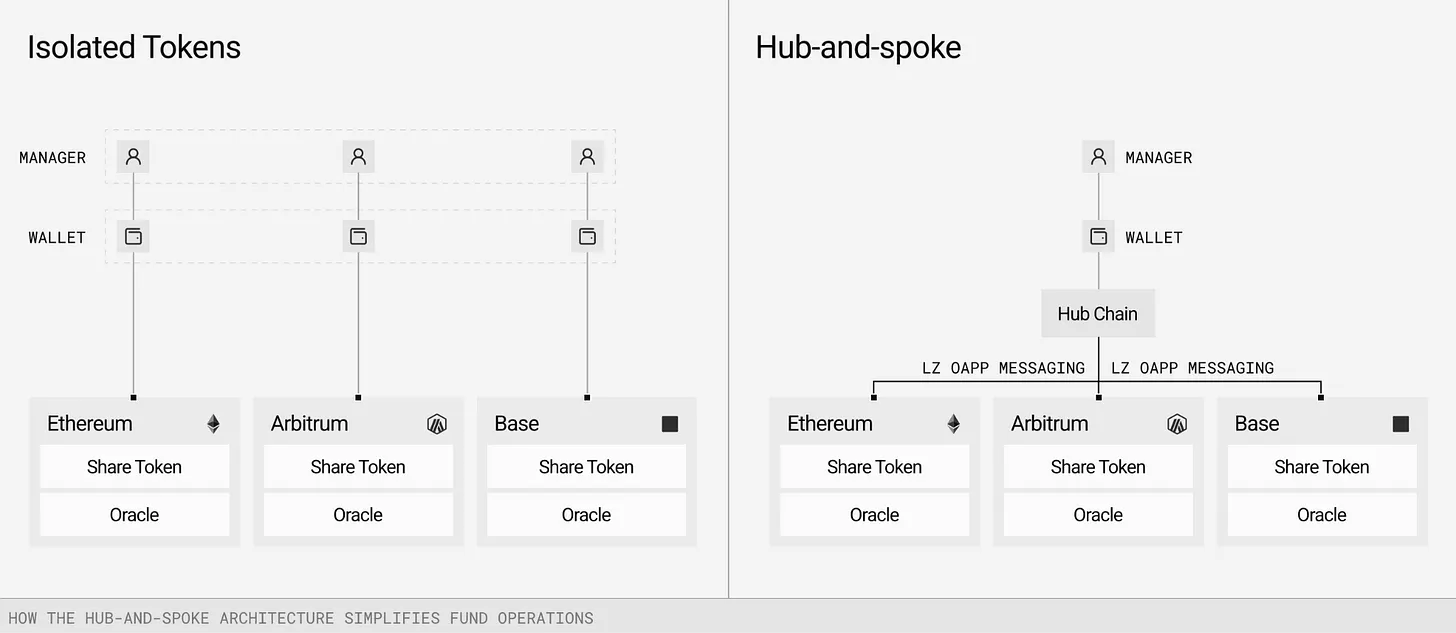

The third conflict arises during cross-chain asset transfers.

When a fund is deployed across multiple public blockchains, a single authoritative data source is needed to track holders and asset valuations. While on-chain data can be updated in real-time, synchronizing accounting across nine different chains is highly error-prone. More points of failure increase the probability of errors.

LayerZero and Centrifuge address this with a hub-and-spoke architecture. In this model, one authoritative chain (the hub) is responsible for managing NAV, accounting, and compliance. A messaging layer (in this case, coordinated by LayerZero) propagates these updates to the spoke chains where the tokens are actually used.

Centrifuge's V3 architecture is built on this model. Each asset pool selects a hub chain as its single source of truth. The spoke chains act merely as deposit/withdrawal and distribution nodes while also offering DeFi composability. LayerZero is responsible for cross-chain synchronization of NAV, compliance instructions, and user position data.

This cross-chain orchestration system establishes a significant industry barrier. A fund's authoritative ledger is maintained by a single set of infrastructure, making it highly irreplaceable. Asset managers handle offline NAV and compliance rules. Blockchains provide on-chain composability. The middle orchestration layer is indispensable, and its value is highly concentrated.

The accounting for assets in transit during cross-chain transfers is the weakest link. When assets move across chains, they briefly fall outside the visible scope of the fund's balance sheet. Centrifuge V3 introduces a mechanism for in-transit asset certificates, ensuring accounting continuity during cross-chain transfers—analogous to the general ledger principle in traditional finance. This seemingly basic feature is essential for institutional adoption.

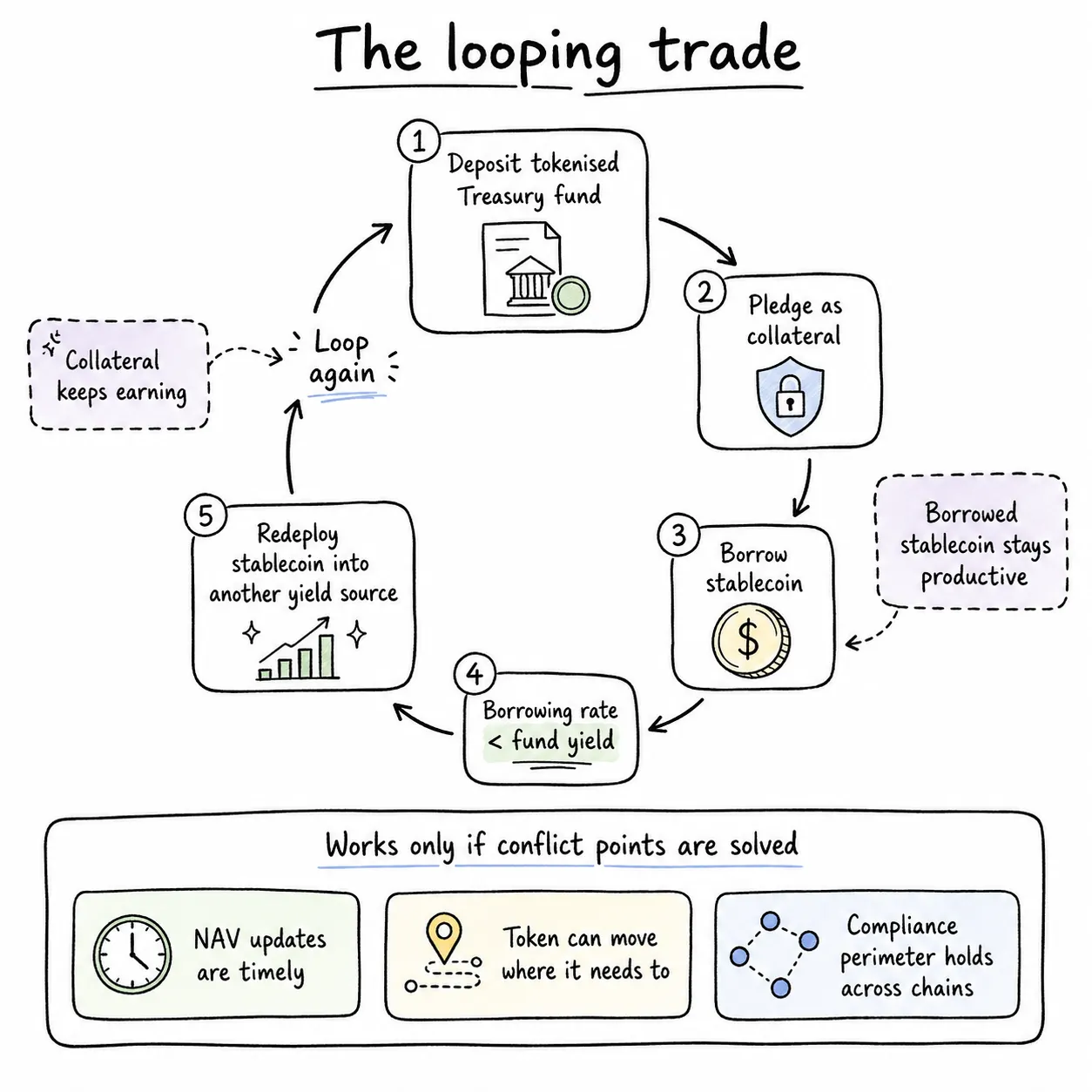

Despite these conflicts, why would institutional investors consider tokenized funds?

The core advantage is recursive staking arbitrage. A corporate treasury deposits into a tokenized Treasury fund and pledges the shares as collateral to borrow stablecoins. If the borrowing rate is lower than the Treasury fund's yield, the position naturally generates a positive carry. The borrowed stablecoins can then be deployed into another yield-bearing asset, creating a potentially infinite loop to amplify cash flow returns.

The entire recursive arbitrage loop is only viable if the three major conflict points mentioned earlier are properly resolved. In the past, the industry saw significant arbitrage opportunities due to mechanism flaws: small tokenized products had NAV updates delayed by 2-4 hours, allowing carry traders to front-run the difference. Redemption conflict risks are equally significant. If the off-chain underlying assets hit redemption limits while the on-chain smart contract continues to process instant redemptions, it creates a large number of unfilled orders.

Currently, large private credit funds and business development companies are facing this scenario. Two weeks ago, Apollo's $26 billion private credit fund, ADS, faced a wave of redemptions, with investors requesting withdrawals totaling 16.8% of the fund's shares. The platform was forced to cap daily redemptions at 5%. If this product had simultaneously issued tokens, the conflict between on-chain instant redemptions and off-chain redemption limits would have been direct. In Q2 of this year, redemption requests for large private credit funds reached $15.6 billion, up from $13.9 billion the previous quarter.

Cross-chain messaging failures mid-transaction and partially settled assets are also high-frequency risks. For each type of failure in this system, licensed entities must bear regulatory accountability to earn the trust of institutional capital.

Tokenization is not simply about putting Treasuries on-chain or adding a new digital asset class. Infrastructure builders must break traditional constraints, allowing investors not to choose between yield, liquidity, and capital turnover. If a tokenized system can uphold regulatory risk controls while enabling multi-purpose value generation from a single pool of capital, institutions holding trillions in cash will inevitably deploy at scale.

As mentioned in last week's article, SWIFT, as an orchestration layer, holds far greater value than the banks at either end. Similarly, the Visa network's profitability nearly surpasses that of all its partner banks except JPMorgan Chase. In the evolution of the financial industry, whoever controls the middle orchestration layer will lock in the capital market dividends of the next decade. Centrifuge is deeply focused on fund-side infrastructure, while LayerZero is building the cross-chain communication foundation. Together, they are positioning themselves at the core of this critical sector.