Author: Etherealize

Compiled by: Deep Tide TechFlow

Deep Tide Introduction: Stripe wants everyone to use Tempo, JPMorgan wants to push its own chain, Circle intends to launch Arc—giants will never build on a rival's infrastructure. This is precisely Ethereum's opportunity: when everyone refuses to submit to a company-controlled foundation, the only choice is a neutral layer that no one controls.

Ethereum is replaying the history of the Internet and Linux.

"Stripe wants everything to happen on Tempo, but JPMorgan wants everything on the JPMorgan chain, Circle wants everything on Arc, and so on. They will never reach an agreement. Major players will never agree to build on another major player's infrastructure. This is why Ethereum is the only option. It is the only way forward—as the neutral infrastructure everyone can accept."

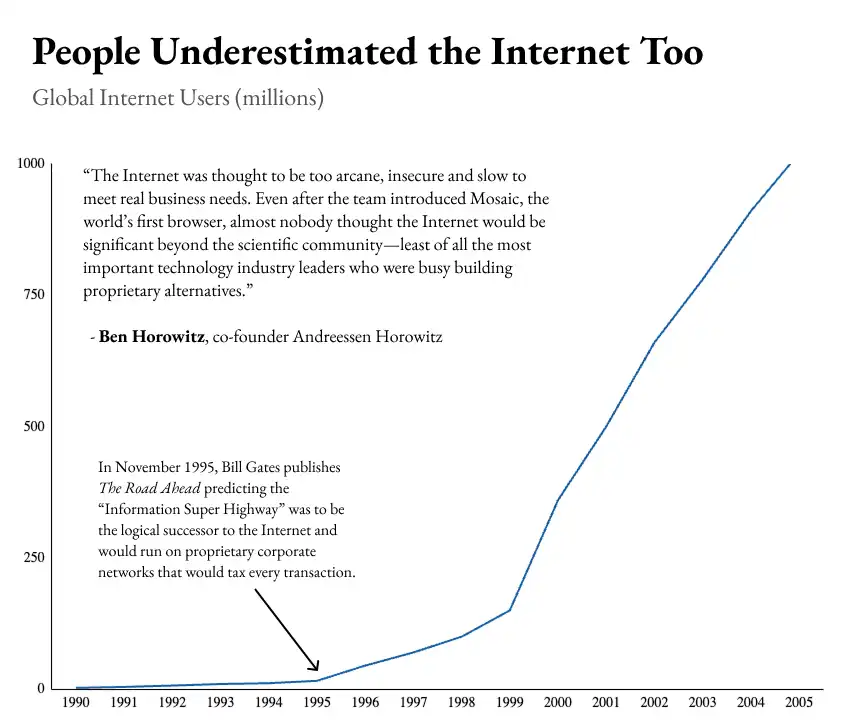

In 1995, most of the technology elite were convinced the Internet would lose out to proprietary corporate networks. They were wrong, and today's critics of Ethereum are likely to be wrong for similar reasons. The most famous example is Bill Gates, who predicted in his book *The Road Ahead* that the future of digital commerce would not run on the open Internet but on proprietary networks owned by companies like Microsoft and Oracle. This was once the consensus. As a16z co-founder Ben Horowitz wrote: "Almost no one thought the Internet would have a significant impact outside of scientific circles—the greatest skeptics were precisely the most important technology industry leaders busy building proprietary alternatives." Linux went through the same thing. Throughout the late 1990s, Sun Microsystems dominated the high-end Unix server market, but by the early 2000s, it lost most of its business to open-source Linux running on cheap generic hardware.

The same pattern is playing out today in financial infrastructure. Companies perceive opportunities and threats, racing to build proprietary blockchains within their controlled walled gardens. For a while, proprietary versions appear to be winning—they are faster, have better user experiences, and boast large business development teams. Then they are slowly swallowed by an open, credibly neutral alternative, because no company can keep up with the pace of permissionless innovation forever, and no serious participant will build on infrastructure controlled by a competitor.

In his 1997 essay "The Cathedral and the Bazaar," Linux contributor Eric Raymond attempted to explain why open, permissionless infrastructure tends to win in the long run. Since Fred Brooks' *The Mythical Man-Month*, the accepted wisdom was that software had to be built by small, tightly managed teams under a single architect because communication costs increase quadratically. However, Raymond saw thousands of contributors (most of whom had never met) working simultaneously on different parts of the Linux kernel, surpassing multibillion-dollar companies. If traditional software was carefully crafted like a "cathedral," then the "bazaar" was Raymond's description of the chaotic, public, distributed development model accidentally discovered by Linus Torvalds—he gave away the kernel source code for free and accepted patches from anyone willing to submit. The guiding philosophy, in Raymond's words, was "release early, release often, delegate everything you can, and be open to the point of promiscuity," resulting in an operating system that ran most of the web by the early 2000s.

Raymond's explanation was that the bazaar avoids the quadratic communication cost problem because contributors do not coordinate directly with each other. They coordinate through patches and releases with the codebase, with maintainers integrating their work into a medium that everyone then coordinates around. As he put it, "The principle behind Brooks's law has not been repealed, but its effects can be swamped by other non-linear factors in the presence of a large developer population and cheap communication."

Another mechanism Raymond identified is that the bazaar eliminates the distinction between users and developers. In the cathedral, users are customers reporting bugs to a service desk. In the bazaar, users are co-developers reporting bugs by fixing them or describing them with enough technical detail for others to fix. Raymond explained that in the open-source community, "every problem is transparent to someone." Collective collaboration surpasses any centralized competitor:

"The Linux world in many ways behaves like a free market or ecosystem, a collection of self-interested agents trying to maximize utility, a process that produces a self-correcting spontaneous order more delicate and efficient than any centralized planning."

You can see this happening on Ethereum. Fabian Vogelsteller wrote the ERC-20 standard, now used by every stablecoin because he found no clean way to support tokens while building a wallet—each token had a different interface. The ERC-721 standard for NFTs came from the people making CryptoKitties. Uniswap, now the largest decentralized exchange of its kind in the world, originated from a blog post by Vitalik Buterin, built by mechanical engineer Hayden Adams with no financial background. None of them needed permission to improve the network. As Sun Microsystems co-founder Bill Joy said, "No matter who you are, most of the smartest people work for someone else." In a permissionless system, innovation can come from anywhere.

The difference between the bazaar and the cathedral is that the integration layer in the bazaar is thin, public, and based on credibility rather than authority. Coordinators like Linus Torvalds or Vitalik Buterin lead because contributors choose to follow, and contributors choose to follow because the coordinator's decisions can be inspected, criticized, and forked if necessary. The Internet has thin centralized integration in the form of the IETF and IANA. Wikipedia has its editorial process. Every project that gains a sustained advantage from permissionless innovation combines truly open contribution with structured integration, preventing the chaos critics fear. And the integration layer must operate through credibility, not coercion, or it fails.

The bazaar also requires a foundation that no one can capture. If Torvalds tried to privatize the kernel, contributors would fork the project and continue elsewhere. Raymond developed this idea in *Homesteading the Noosphere*, arguing that open source had developed a property rights theory similar to Locke's theory of land ownership: developers establish ownership by homesteading a project (writing the initial code), maintain it through continued contribution, and can transfer it through legitimate inheritance. The credibility of open licenses is the formal mechanism; the norms of the Internet noosphere are the social mechanism. Take away either, and contributors will go work elsewhere, where their contributions won't be appropriated.

In the Ethereum community, Vitalik Buterin formalized this requirement as "credible neutrality." A coordination mechanism is credibly neutral when the rules are transparent, apply equally to all participants, are difficult to change, and participation is open to anyone willing to abide by the rules. These four properties are extracted from systems that can attract contributions at scale. The Internet, Linux, and Wikipedia all have versions of these four properties. Proprietary networks, walled gardens, and corporate blockchains do not.

Over a sufficiently long time horizon, credibly neutral systems usually win. Open networks replaced proprietary ones; Linux replaced proprietary Unix; Wikipedia replaced Encarta and the Encyclopædia Britannica. Each time, proprietary alternatives had real advantages—focused products, more capital, customer support teams, professional marketing and business development teams—and each time, those advantages eroded as the open ecosystem matured and network effects reversed. Once an open alternative crosses the threshold in accumulated contributions, tools, and credibility of not changing the rules, closed systems can almost never compete.

The same pattern is now playing out at every layer of financial infrastructure. SWIFT, Visa, and Mastercard, and today's consortium chains pitched to institutions, are different products with different histories, but structurally they are the same bet: centrally controlled infrastructure with a potential landlord. For forty years, SWIFT was a neutral pipeline owned by its member banks, until the U.S. pressured it to cut off Iranian banks in 2012 and several Russian banks in 2022. Despite corporate governance and Belgian registration, SWIFT ultimately answers to the U.S., and the rest of the world took note. China accelerated CIPS, Russia built SPFS, India expanded UPI, Brazil's Pix became the backbone of BRICS Pay. Visa and Mastercard started as bank cooperatives too, then became toll booths charging merchants 1.5–3.5% per transaction. The consortium chains being pitched today (like Canton, Tempo, Arc) have the same flaw: a landlord whose interests may diverge from those building on it.

"The original vision of consortium blockchains—5 banks or big companies getting together to create their own chain—has basically failed," explained Vitalik Buterin. "It ends up inheriting most of the disadvantages of centralization and most of the disadvantages of decentralization at the same time." As he describes it, the problem is that the first few banks feel like equal founders, but the twentieth bank is just joining something competitors already control. You bear all the engineering costs of a distributed system but get none of the benefits of openness, composability, and credible neutrality—the very things that make blockchains worth building in the first place.

The wreckage confirms his point. Between 2017 and 2019, several major banking consortia set out to rebuild trade finance on blockchain. We.trade, backed by a dozen banks including HSBC and Deutsche Bank, went bankrupt in 2022. Marco Polo signed up over thirty banks, liquidated a year later. Contour shut down months after. The Australian Securities Exchange spent six years and roughly A$250 million on a permissioned ledger built by Digital Asset (the company behind Canton today), abandoning the project in 2022. Meanwhile, Ethereum, controlled by no one, has never gone down in its 10+ year history, only grown.

This is why developers choose Ethereum. According to Electric Capital, over one million developers have contributed to the Ethereum ecosystem over its lifetime, with about 232,000 active in the past year alone. No other chain comes close. Part of this is a plain flywheel effect: tools, standards, and job opportunities are on Ethereum, so people learn to build there, attracting more tools and jobs. But developers and institutions also specifically choose Ethereum for its superior decentralization and credible neutrality. For example, last year Robinhood chose to build an L2 on Ethereum instead of its own L1; the company's head of crypto, Johann Kerbrat, explained the rationale:

"You see a lot of companies now building their own L1s. We were excited about the idea of controlling everything you want to build, but creating a truly, properly decentralized chain's security is extremely difficult, and Ethereum basically gives you that for free. When you look at some of the new L1s being created, they aren't really decentralized, nor really secure. At the end of the day, it's basically a fancy database that's a bit slower than an actual database, so we really don't see the value."

Erik Voorhees, founder of Venice AI (a privacy-first AI inference platform with over 3 million users and tens of millions in ARR), laid out a similar rationale a few days ago. When asked why Venice is building on Coinbase's Ethereum L2 Base, Erik replied: "This wasn't even a question for us; the Ethereum ecosystem is the more authentic, more resilient, more robust ecosystem across all smart contract platforms."

The most important property of a blockchain is sovereignty. Bitcoin was revolutionary because it was the world's first sovereign computer platform. Before Bitcoin, all computer platforms belonged to individuals, companies, or governments, which had to obey the will of their owners and the rules of their jurisdiction. But sovereignty obeys only its own rules, and no single entity could impose rules on Bitcoin. Kings and queens were once sovereigns, then nation-states, and now, for the first time, a computer platform can be sovereign. This is why decentralization is so revered in crypto; it is the means to achieve sovereignty. A platform with ten validators obeys the rules of those ten. But a platform like Ethereum, with hundreds of thousands of independent validators spread across every major jurisdiction, multiple independent client implementations, and a foundation that explicitly renounces governance power, has crossed a threshold where no party can credibly claim ownership. Sovereignty is the property that allows a global financial system to build on Ethereum without any participant worrying that another participant, a government, or the foundation will change the rules to their detriment.

Ethereum's lead in sovereignty and credible neutrality comes largely from path dependency that other blockchains cannot replicate. Ethereum launched in 2015 with PoW, ran for seven years, and transitioned to PoS in 2022. During this time, network ownership was distributed through a public crowdfunding in 2014 and GPU mining kept deliberately accessible to consumer-grade hardware. The result was broad token distribution, with no single entity controlling a meaningful share of the network (a key factor for PoS network sovereignty). Modern consortium chains launch as venture capital rounds with concentrated insider allocations, giving a few participants outsized control over the chain's consensus. Competitors can copy the architecture but not the history.

Since then, Ethereum's lead has only compounded. The platform's sovereignty and credible neutrality attract developers. Developers attract more developers because the libraries, tools, and hiring pools already existing on Ethereum make building there easier than anywhere else. Applications attract liquidity and tokenized assets, which in turn attract institutions. Each layer reinforces the others, and competitors trying to enter have to build all layers at once while Ethereum continues to compound.

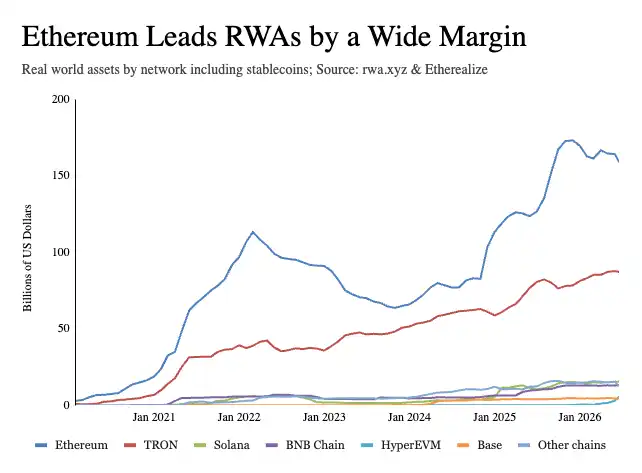

The most established players in the field have already chosen Ethereum. Coinbase and Robinhood chose Ethereum for their L2s. BlackRock and JPMorgan launched their tokenized money market funds BUIDL and MONY on Ethereum. Major DeFi protocols, including Aave, Maker/Sky, Maple, and Uniswap, are primarily on Ethereum. The largest stablecoin issuers settle on Ethereum. According to Token Terminal's Q1 2026 Ethereum Report, Ethereum holds 79% of active DeFi loans, 62% of stablecoins, 73% of tokenized funds, and 84% of tokenized commodities among the top five chains.

Applications are also permissionless, further reinforcing Ethereum's advantages. For example, Uniswap's permissionless listing process allows thousands of long-tail assets to find price discovery and liquidity that no centralized exchange would provide. Aave's lending markets are open and composable, enabling an entire ecosystem of specialized vaults and risk managers to emerge atop its liquidity, extending Aave's reach far beyond what the core team could build alone. Closed systems need gatekeepers to anticipate every use case in advance; open systems do not.

The strongest objection to the "permissionless wins" view is not technical; it's that finance might be the one place where corporate-owned networks are a feature, not a bug. When payments fail or assets end up where they shouldn't, regulators want someone to be accountable. When lawyers show up, "no one in charge" sounds less like an advantage and more like liability. But this objection confuses two things that exist at different layers. Accountability exists at the application layer, not the settlement layer. For instance, token standards like ERC-3643 embed KYC, identity verification, and jurisdictional transfer restrictions directly into a token's smart contract, allowing issuers to whitelist wallets, restrict transfers, and freeze or claw back assets. Privacy works the same way; zero-knowledge cryptography lets institutions settle on public chains while keeping transaction details confidential. On consortium chains, the only people who see your data are you and your closest competitors.

Early on, the Internet was considered too unsafe for real commerce. Then HTTPS made the open web secure enough that nearly all commerce moved onto it, and the issue was never raised again. Skeptics weren't wrong about the early state. They just incorrectly assumed the open web couldn't close the gap.

The banks and fintechs building their own chains today are thinking what AOL and Microsoft thought in the early days of the Internet: build something open, but inside your own walled garden so you can collect rent. But that never works because the walls that give you control are the same walls that block innovation.

A better model is Netscape. Netscape didn't try to own the web; it built the browser that brought the world onto the web. Riding the explosive growth of the open web, it became one of the most important companies of its era. Ethereum's credible neutrality is almost impossible to replicate, and it's already positioned to become the settlement layer for global finance. The winning strategy is to build on permissionless infrastructure, not compete with it.

Disclosure: This analysis is published by Etherealize, an organization focused on institutional Ethereum adoption. The author and Etherealize may hold positions in ETH and other digital assets discussed. This is not investment advice.