Kevin Warsh assumed the role of Chairman of the U.S. Federal Reserve Board on the 22nd, local time.

With a background in Wall Street investment banking and firsthand experience handling the 2008 financial crisis, Warsh lacks the traditional academic pedigree of a central banker. Yet, he has put forward the unconventional policy stance of "balance sheet reduction + interest rate cuts," aiming to reshape the operational rules of the Fed's monetary policy.

His drive for reform—changing the Fed's decision-making mechanism and tightening its policy communication—offers a fresh approach for a Fed trapped in the dilemma of "fiscal expansion while monetary tightening is stalled." It also introduces new uncertainties for global capital markets, the credibility of the U.S. dollar, and the landscape of global asset allocation.

This seemingly routine personnel change is far from a simple power transfer. It is a pivotal turning point that will reshape the Fed's decision-making logic, impact the performance of core assets like U.S. Treasuries, the dollar, and commodities, and further rewrite the global monetary and financial order. Below, Enjoy:

Source丨Mi Kuang Investment

April 21, 2026. The hearing room of the U.S. Senate Banking Committee was packed.

The man sitting in the witness seat had declared personal assets exceeding $130 million. His wife is an heir to the Estée Lauder family, with a combined estimated wealth of around $2.7 billion. He is the wealthiest candidate for Fed Chair in the institution's 112-year history.

His name is Kevin Warsh ( Kevin Warsh ).

(Elizabeth Frantz/Reuters)

On Friday, May 22, Trump presided over a swearing-in ceremony at the White House, formally passing the mantle of the Federal Reserve to Warsh. Warsh became the man in control of the world's most powerful financial institution.

01 How Exactly Does the Fed Decide on Interest Rates?

Many believe the Fed Chair decides alone, but that's not the case.

Interest rate decisions are voted on by the Federal Open Market Committee ( FOMC ), with 12 voting members each casting one vote; majority rules. The Chair's power lies in setting the agenda and guiding public discourse.

In other words, he decides what to discuss and how to discuss it, but ultimately relies on vote counts.

Following the FOMC meetings in March, June, September, and December each year, the Fed releases two key tools:

-

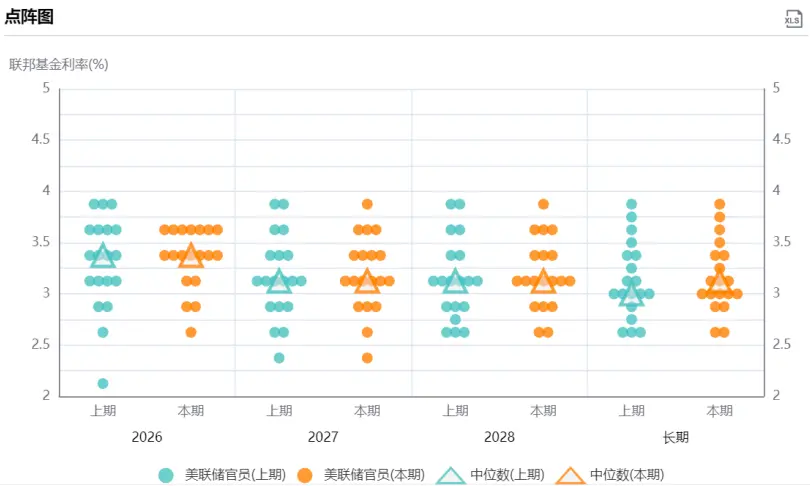

One is the Dot Plot ( Dot Plot ). Each member anonymously marks their own interest rate expectations for the future, compiled into one chart. The market reads dovish or hawkish signals from this.

Source: Federal Reserve Dot Plot

-

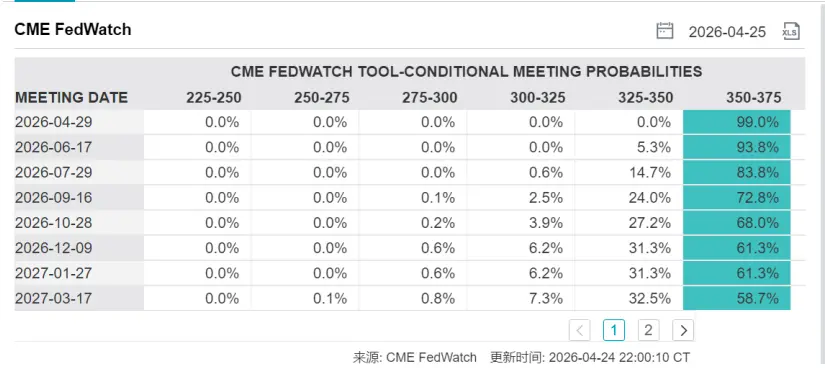

The other is called the Summary of Economic Projections ( SEP ), containing forecasts for GDP growth, unemployment, and inflation. Market traders often combine this information with the Chicago Mercantile Exchange's FedWatch tool to translate it into probabilities of rate cuts or hikes, a common chart (as shown below).

Understanding this mechanism is important because the first thing Warsh aims to change upon taking office is this very mechanism itself.

02 The Richest Fed Chair Ever: Wall Street's Spokesperson?

Let's first look at Warsh's resume. When reading it, one gets the feeling that this isn't the CV of a government official, but more like a Wall Street who's who.

Warsh was born in 1970 in Albany, New York. He holds a bachelor's in public policy from Stanford University and a J.D. from Harvard Law School. After graduation, he joined Morgan Stanley in mergers and acquisitions, later becoming vice president and executive director. In 2002, he was selected by George W. Bush to serve in the White House as Executive Secretary of the National Economic Council.

In 2006, the 35-year-old Warsh was appointed as a Governor of the Federal Reserve Board, one of the youngest in Fed history at the time. During his tenure, he was a core member of Ben Bernanke's team handling the 2008 financial crisis, responsible for communication and coordination with major Wall Street financial institutions. He was a key intermediary in events like the Bear Stearns acquisition, Lehman Brothers' collapse, and the AIG bailout.

After leaving the Fed in 2011, Warsh joined legendary investor Stanley Druckenmiller's Duquesne Family Office, with an annual salary exceeding $10 million. He also served as a director at UPS and South Korean e-commerce giant Coupang, and was a research fellow at Stanford University's Hoover Institution.

Financial disclosures from April 2026 show Warsh's personal assets range from $131 million to $226 million. He holds a large position in the hedge fund Juggernaut Fund, and holds shares in Polymarket, SpaceX, and several cryptocurrency companies. His wife, Jane Lauder, is the granddaughter of the Estée Lauder founder, with a personal wealth estimated by Forbes at approximately $1.9 billion. In 2018, Powell was considered the wealthiest Fed Chair upon confirmation, with assets ranging from $19 million to $75 million. Warsh's assets are several times larger than Powell's.

From his resume, I believe he deeply understands the operational logic of capital markets—such as liquidity, leverage, and the transmission chains of balance sheet expansion.

03 A Non-Technocrat?

Frankly speaking, Warsh is not an academic central banker.

He does not hold a Ph.D. in economics and has not published influential papers in academia. Compared to Ben Bernanke (a Princeton economics professor during the subprime crisis) and Janet Yellen (formerly a professor at UC Berkeley), Warsh's academic background is noticeably thinner.

Yet, he has put forward a policy proposition that the market is very focused on: Balance sheet reduction + interest rate cuts.

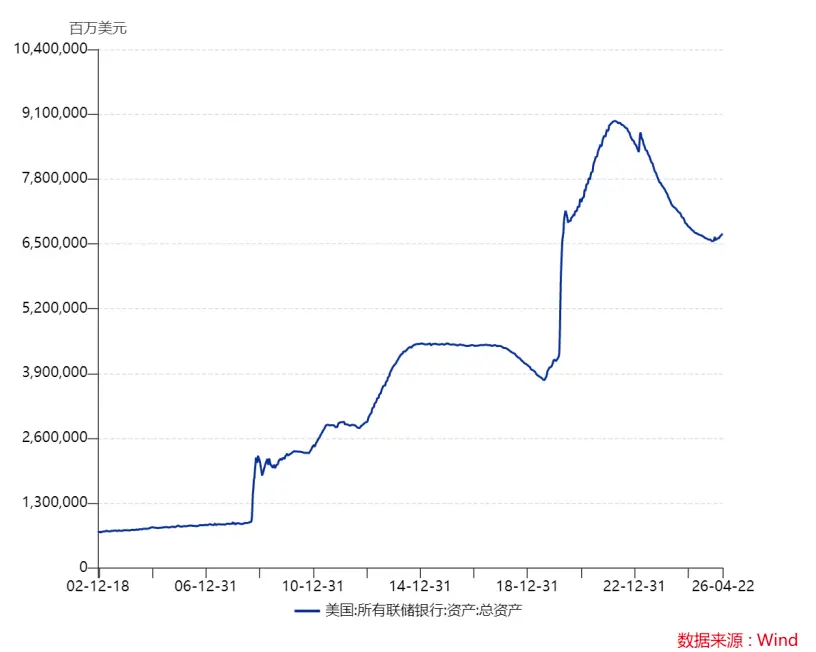

Warsh's theoretical logic is as follows: Since September 2024, the Fed has cumulatively cut rates by 175 basis points, yet long-term Treasury yields have risen instead of falling. He believes the problem lies in the Fed's massive $6.7 trillion balance sheet. Balance sheet expansion itself is equivalent to a hidden rate cut; his exact words were, "If the printing press could quiet down, policy rates could be lower." Therefore, theoretically, balance sheet reduction is needed to create space for the interest rate tool to be truly effective.

Rate cuts and balance sheet reduction are two entirely different things.

Rate cuts are a price tool, adjusting the federal funds rate; balance sheet reduction is a quantity tool, shrinking the size of the balance sheet. Rate cuts are easing, balance sheet reduction is tightening—they move in opposite directions. Warsh's idea is to tighten quantity first, then ease price, but this requires extremely high operational precision.

There's an even more critical problem: It is almost impossible for the Fed to reduce its balance sheet further.

Quantitative tightening under Powell officially ended in December 2025. The balance sheet shrank by over $2 trillion from its pandemic peak of nearly $9 trillion, stabilizing at around $6.7 trillion. The Fed is currently maintaining the status quo: purchasing enough Treasuries to match the growth in bank reserve demand—neither expanding nor contracting the balance sheet.

Warsh and Fed Governor Miran, among others, advocate restarting balance sheet reduction. However, the problem is that the fiscal side is pressing the accelerator hard in the opposite direction. The deficit is expanding, and tax cuts under the "Big and Beautiful Act" are set to be increased further, meaning the Treasury needs to continuously issue new debt. If the Fed simultaneously restarts balance sheet reduction—meaning it stops rolling over maturing Treasuries or even sells them—it would create a situation where two sellers are competing for the same pool of buyers. Long-term interest rates could spiral out of control. The dismal result of the 20-year Treasury auction in May 2025 was a warning signal.

The core contradiction now is that fiscal policy is expanding the balance sheet, while monetary policy's attempt to contract it is blocked.

The fiscal side is ballooning to historically extreme levels, while the Fed's balance sheet can't shrink. Therefore, the scalpel Warsh can actually wield is not on the balance sheet itself, but on the monetary policy framework. He can redesign the inflation target framework, reduce reliance on forward guidance, and enforce stricter communication discipline among Fed officials. In short, he can't change the Fed's size, but he can change how the Fed communicates and the logic behind its decisions.

Analyzing Warsh's public speeches, congressional testimonies, and media interviews from 2009 to 2025 paints a clear picture: During the Obama era, he was a staunch hawk.

Citadel Securities once published a report titled " A Framework for Chair Warsh," which noted that during his tenure, Warsh gave 13 public speeches specifically emphasizing upside risks to inflation—a period when core PCE inflation rarely exceeded 2.5% and unemployment once reached 10%.

In 2010, he voted in the FOMC in favor of Bernanke's $600 billion QE2 plan, but simultaneously published an article in The Wall Street Journal attributing economic weakness to the Obama administration's fiscal and regulatory policies. During Trump's first term, his stance began to shift.

In 2018, after being passed over by Trump for the Fed Chair nomination, Warsh warned in The Wall Street Journal that Trump's protectionist trade policies would harm economic growth. By 2024-2025, his attitude shifted again.

In September 2024, after the Fed cut rates by 50 basis points, Warsh criticized the move as "an impulsive act lacking theoretical justification." Just 13 months later, in November 2025, he wrote in The Wall Street Journal advocating for more aggressive rate cuts from the Fed.

Critics point out that Warsh's monetary policy stance seems to adjust with changes in the White House occupant—more flexible under Republican presidents, more hawkish under Democratic ones. However, one could also view this as the hallmark of a pragmatic monetarist: not bound by any single theoretical framework, making judgments based on the prevailing political and economic environment.

At the April 21 hearing, Warsh laid out this line of thinking, explicitly stating his intention to push for institutional change at the Fed ( regime change ). He believes Fed officials talk too much. In his view, "Pursuing truth is more important than repeating talking points."

04 Independence: What He Said, and What He Didn't Say

The core exchange at the hearing revolved around one question: Can you resist Trump's pressure for rate cuts?

Warsh's answer was carefully crafted. In his opening statement, he wrote: "Monetary policy independence is crucial." When Senator Kennedy asked if he would be Trump's "puppet," he replied: "Absolutely not. The President has never asked me to pre-judge, commit, fix, or determine any rate decision." But he also inserted a crucial line: "When elected officials, whether the President, Senators, or Representatives, express their views on interest rates, I don't see that as particularly threatening to the operational independence of monetary policy."

The subtext of this statement might be: Trump publicly demanding rate cuts is not seen by Warsh as a threat to independence. It's just expressing an opinion. Compare this to Powell in 2019, who chose to directly ignore similar pressure from Trump's tweets, emphasizing at a press conference, "We will not be influenced by short-term political considerations."

Warsh's phrasing is more flexible, giving the White House more space in public discourse.

Additionally, Warsh has long advocated that the Fed should " stay in its lane," narrowing its scope of functions and avoiding involvement in social and fiscal policy discussions. This aligns with Trump's desire to curb the Fed's administrative power.

05 What Does This Mean for Asset Allocation?

Back to practical questions. The real constraints Warsh faces upon taking office are: restarting balance sheet reduction is blocked by fiscal expansion, cutting rates is constrained by inflation not yet meeting targets, and framework reforms require majority support in the FOMC... Regarding these, I have the following thoughts:

First, volatility in the U.S. Treasury market is likely to remain elevated. Fiscal expansion and monetary tightening being stalled means pressure from Treasury supply won't subside. Warsh wants to reduce the balance sheet but can't, while the Treasury keeps issuing debt. The market needs more private buyers to absorb the supply. Long-term rates are more likely to rise than fall, and Treasury volatility measures may stay high. For investors holding U.S. Treasuries, the certainty of short-duration instruments is higher than that of long-duration ones; don't bet on direction in long bonds.

Second, the long-term credibility anchor of the U.S. dollar is loosening. This is a structural trend. A recent in-depth report by Huatai Securities' strategy team deconstructed "de-dollarization" into three levels: de-dollar assets (private capital selling), de-dollar reserves (central bank reduction), and de-dollar settlement (trade payment shifts). The three reinforce each other but progress at different paces: de-dollar assets are pulse-like and sentiment-driven; de-dollar reserves and settlement are slow processes measured in years or even decades.

As of the end of 2025, the U.S. dollar's share of global foreign exchange reserves had fallen to 56.77%, the lowest since 1994. This figure was 73% in 2001.

Third, cracks are appearing in the petrodollar system. Data-wise, by March 2026, the share of RMB settlement in Middle Eastern crude oil trade with China had surpassed 41%, making the RMB the second-largest settlement currency for Middle Eastern oil trade for the first time; Iran has been settling 100% of its oil sales to China in RMB since January 2026; the daily average transaction volume of China's Cross-Border Interbank Payment System reached 920.5 billion yuan in March, hitting a 12-month high.

There is a dimension easily overlooked here: If Warsh can rebuild the Fed's policy credibility through framework reforms, it might actually slow down sentiment-driven de-dollarization trades in the short term, as market confidence is partially restored. However, in the long run, as long as the pattern of fiscal expansion and monetary tightening being stalled persists, the downward shift in the dollar's credibility anchor will not stop. This has little to do with who chairs the Fed.

For ordinary investors, the core response strategy is diversification. In an environment of increasing U.S. dollar credit volatility, gold, as a reserve asset without sovereign credit risk, remains an indispensable part of a portfolio. Meanwhile, the weight of RMB assets, particularly Chinese government bonds, is being passively increased in the global asset reallocation.

The CSRC's recent Announcement No. 7 is quite interesting and worth contemplating. In my view, it represents an important link in the process of RMB internationalization, and I would be happy to discuss it given the opportunity.

But the market has already begun pricing in the "Warsh Era."

★ Disclaimer: The above represents only the author's personal views and is intended for reference, learning, and exchange purposes only.

Original Link