Author: Deep Tide TechFlow

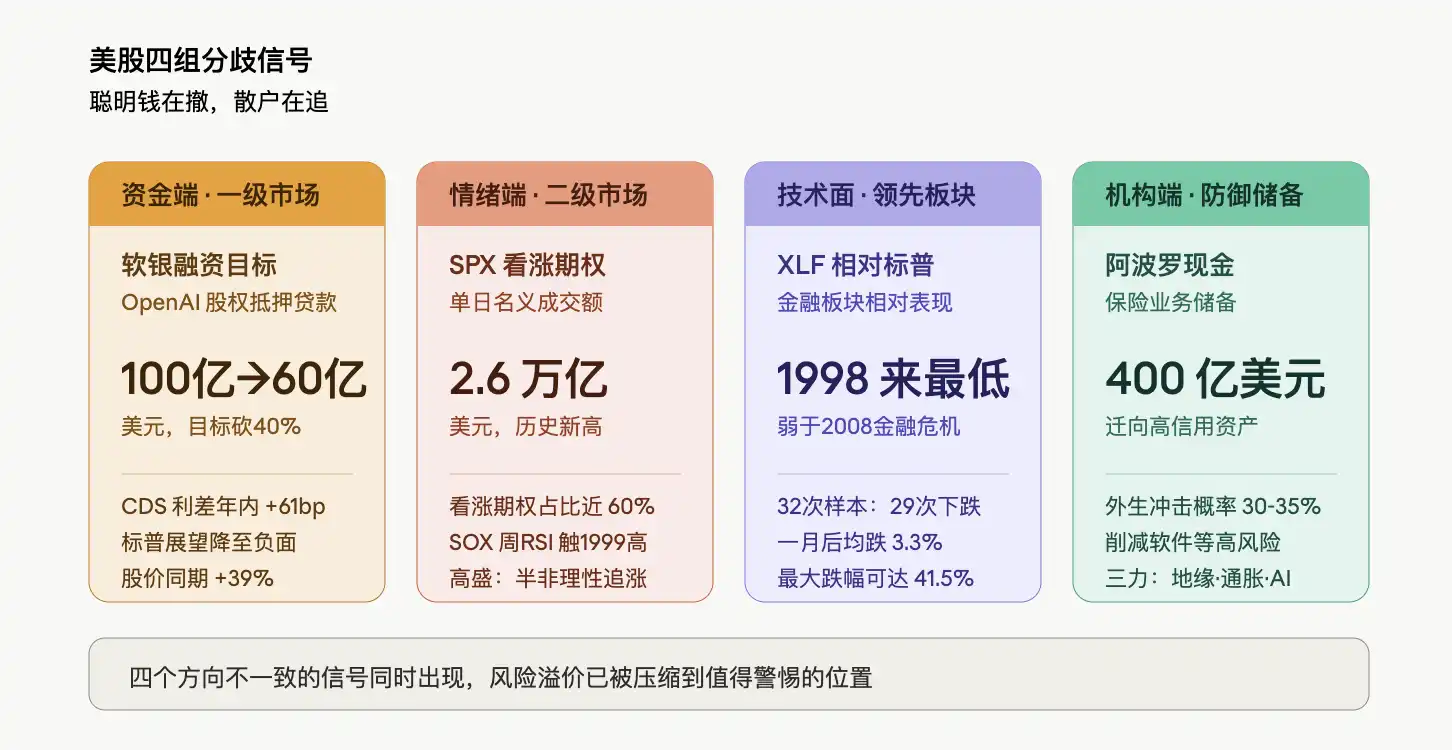

The US stock market is staging an exceptionally unusual divergence: while the S&P 500 repeatedly hits new highs, the financial sector has fallen 6% year-to-date, underperforming the broader market more severely than during the 2008 financial crisis and the Covid shock; meanwhile, the single-day notional trading volume of S&P 500 call options has exceeded $2.6 trillion, a record high, and the RSI for the Philadelphia Semiconductor Index has risen to its highest level since 1999. In the primary market, SoftBank's financing plan, using OpenAI equity as collateral, was forced to cut its target size from $100 billion to $60 billion; on the institutional side, Apollo has hoarded roughly $40 billion in cash within its insurance business. Smart money is pulling back, retail is piling in.

The narrative around AI computing power scarcity continues to drive the accelerated rise of the US tech sector, but the capital flow, sentiment, technicals, and institutional behavior are sending conflicting signals. This divergence itself is more worthy of scrutiny than any single data point.

Lenders Skeptical of OpenAI Valuation, SoftBank Cuts Financing Target by 40%

According to Bloomberg citing sources familiar with the matter, SoftBank has reduced the target size of its margin loan, collateralized by OpenAI equity, from $100 billion to a minimum of $60 billion, a 40% cut. The core resistance lies in valuation, with some investors being courted to participate harboring doubts about how to reasonably value this non-public company, OpenAI. Potential lenders involved in the discussions include private credit institutions, financial institutions, and hedge funds, with related negotiations starting as early as mid-March.

OpenAI's own fundamentals are also under pressure. The company failed to meet its monthly sales targets multiple times in early 2026, with rival Anthropic steadily eroding its share in programming and enterprise markets, and the internal goal of reaching 1 billion weekly active users for ChatGPT by the end of last year was also missed. OpenAI CFO Sarah Friar refuted this, stating the company is meeting its goals and seeing product demand "rise vertically."

SoftBank's own financial leverage is also at historically high levels. The group recently committed an additional $30 billion to OpenAI, having already invested over $30 billion cumulatively; the $40 billion loan completed this March set a record for its US dollar loan size, with part of the funds used to support the latest follow-on investment in OpenAI.

Capital market judgment on SoftBank has shown significant divergence. SoftBank's stock has risen 39% year-to-date, significantly outperforming the 12.3% gain of Japan's benchmark Topix index; however, its credit default swap spreads have widened by about 61 basis points this year. In March, S&P Global Ratings downgraded SoftBank's credit outlook from "stable" to "negative," citing that the investment in OpenAI could harm the company's liquidity and asset credit quality.

The pricing divergence for top AI assets in the primary market is manifesting in the most direct way: lenders are willing to lend 40% less than SoftBank wants to borrow.

Options Market Hits $2.6 Trillion in a Single Day, Goldman Sachs Partner Calls It "Semi-Irrational"

The secondary market presents another picture. On Thursday, the notional trading volume of S&P 500 index (SPX) call options broke through $2.6 trillion, setting a historical record, with nearly 60% of all SPX options that day being calls. Rich Privorotsky, head of Goldman Sachs's One-Delta trading desk, characterized the current US stock market as being in a "spot-up, vol-up chase mode."

The weekly RSI for the Philadelphia Semiconductor Index (SOX) has risen to its highest level since 1999. A Goldman Sachs partner stated bluntly: "It feels like we are in a semi-irrational chase mode." Privorotsky cited 1999 as a more fitting historical analogy, when numerous telecom equipment suppliers had overflowing order books, providing the "physical bottleneck narrative" supporting that rally, highly similar to the current logic around computing power scarcity and AI infrastructure deployment.

QQQ implied volatility has spiked sharply with the rally, with its spread over SPX volatility widening to over 6 volatility points. Goldman's volatility trading desk described this day as "one of the craziest trading days in the past few weeks." Notably, the number of S&P 500 constituent stocks experiencing single-day moves exceeding 3 standard deviations reached 35, the highest level since February 3rd this year.

Bank of America's global equity derivatives research team also pointed out that the S&P 500's latest record-breaking rally is reminiscent of the late 1920s and the 1990s internet bubble, but market pricing for "tail options" remains below the level implied by realized volatility. In layman's terms, the market is chasing the rally but unwilling to pay for downside risk.

Goldman Sachs warned that the dynamics of "spot-up, vol-up" have limited the room for systematic strategies to add further positions; Commodity Trading Advisors (CTAs) are already essentially back to full long positions, and as realized volatility in the upward direction rises, the marginal incremental demand from volatility control strategies is also waning. In other words, programmatic buying from the institutional side is nearing its limit, with subsequent upward momentum relying more on retail and sentiment-driven funds.

XLF Hits Weakest Relative to S&P 500 Since 1998, Financial Stocks Sound Alarm

If the options market is an extreme reading of sentiment, then the relative performance of the financial sector is a warning signal from the technical front.

The US financial sector has fallen about 6% year-to-date, while the S&P 500 index has risen 7% over the same period and closed at a record high 14 times in the past 17 trading days.

Related data was analyzed in The Crack Beneath the S&P's New High: Financial Sector Down 6% Year-to-Date, $2 Trillion Private Credit Undercurrent Spreading.

The financial sector is seen as a leading indicator due to its core role as a provider of economic liquidity. Concerns in the private credit market are believed to be a major reason for the pressure on the financial sector. Melissa Brown, Global Head of Investment Decision Research at SimCorp, noted that the financial system is highly interconnected, and related risks "have the potential to spread more widely than currently anticipated." He suggested investors might consider gradually "trimming chip stocks" rather than continuing to chase the rally, and certainly not injecting new funds into the market.

Apollo Hoards $40 Billion in Cash, Rowan Estimates 35% Probability of Exogenous Shock

Defensive moves have begun on the institutional side. Marc Rowan, CEO of Apollo Global Management, stated while announcing quarterly results that he estimates the probability of an exogenous shock occurring at 30% to 35%, far above the usual level.

Rowan attributed this risk to the convergence of three forces: a full-scale reset in geopolitics, inflationary pressures driven by trade tariffs and immigration policies, and the profound reshaping of the economic structure by AI. He characterized the current AI wave as "without question the biggest tech cycle" of his career and specifically highlighted the fragility of government finances—compared to corporations and consumers, government balance sheets are already under pressure.

Apollo has taken a series of defensive measures: shifting its fixed-income portfolio towards higher credit quality, reducing exposure to high-risk sectors like software, and hoarding about $40 billion in cash within its insurance business. "This means we are investing with an eye to protecting capital, making sure we can go through the cycle, and if there is an adjustment, we frankly expect it to happen."

Rowan saved his sharpest criticism for industry rivals. He warned that not all insurance companies are running their businesses as they should, with some relying on what he called "outrageous" practices, including Cayman Islands offshore structures, complex mortgage arrangements, and aggressive credit assumptions, making some balance sheets appear stronger than they actually are. "We are concerned about contagion," he said.

It's worth noting that Apollo's performance this quarter was stellar, with assets under management surpassing $1 trillion and fee-related earnings hitting a record high. Choosing its most significant defense at the peak of its own operational performance is, in itself, a judgment.

Consumer End's Tale of Two Cities, Confirming Macro Divergence

Consumer data provides micro-level evidence for the above macro judgment. Whirlpool (WHR) plunged 16% after hours on Thursday, with management describing the current environment as a "sharp deterioration in macroeconomic conditions" and announcing "decisive actions" like price increases and accelerated cost-cutting to restore profitability. The chill in the housing and major appliance sectors forms a stark contrast with the heat in the semiconductor sector.

In contrast, DoorDash stated the second quarter is "off to a good start," demand "remains quite strong," and its stock rose about 10%.

This divergence reflects the underlying logic of current consumer behavior: large expenditures (like renovation, appliances) feel like a recession, while small, immediate consumption (like food delivery) remains almost unaffected. Consumers haven't disappeared; they've just become highly selective, aligning perfectly with the corporate conclusion: AI infrastructure investment is accelerating, while traditional durable goods consumption is contracting.

Place these four sets of signals on the same chart: lenders unwilling to pay $100 billion for OpenAI, the options market betting $2.6 trillion on a single-day rally, the financial sector at its weakest relative level since 1998, and Apollo hoarding $40 billion in cash. This does not constitute a judgment of "imminent crash." Scott Brown himself also emphasized that similar warning signals sometimes persist for a long time before being digested by the market, or may not even materialize. But when the primary market, secondary market, leading sector, and top institutions simultaneously give conflicting readings, it at least means that the risk premium corresponding to current price levels has been compressed to a level worth vigilance.