Original|Odaily Planet Daily (@OdailyChina)

Author|Wenser(@wenser2010 )

The recent market earthquake in the U.S. storage and chip industry triggered by a research report from SemiAnalysis is still fresh in our minds.

As an independent investment research firm with annual revenue potentially exceeding $100 million, today's SemiAnalysis integrates multiple roles including a consulting firm, a model service platform, and a technology lab. The person at the helm of this rapidly growing, highly regarded firm—praised by NVIDIA founder Jensen Huang and AMD CEO Lisa Su—is not a technical expert or an engineer deeply involved in chip manufacturing. Instead, it's a former beekeeper from Minnesota and an "anonymous technical geek" who frequented various American enthusiast forums—a "beekeeper and forum warrior."

This episode of Character Decode by Odaily Planet Daily shares the story of—SemiAnalysis founder Dylan Patel.

SemiAnalysis Founder: A "Forum Geek" Who "Maxed Out His Skill Tree" and Became Self-Taught

Compared to Citrini, which focuses more on macro trends and long-term themes, SemiAnalysis chose to concentrate more deeply on the semiconductor industry. Its founder, Dylan Patel (hereinafter referred to as Dylan), is nothing short of an "industry legend."

Early Life: A Rural Beekeeper in Georgia, America's Version of a "Forum Warrior"

According to Dylan's sharing in a food-interview style show on Latent Space, he grew up in rural Georgia, USA, and attended the University of Georgia. After graduation, he even worked as a beekeeper in Minnesota for about a year and a half.

At that time, he was in a state of "feeling lost." Summarizing his past now, he says: "I feel like I've just gone through many phases of life... It seems there isn't really a clear, direct path to follow." (Odaily Planet Daily Note: This refers to his identity shifts from a chip enthusiast, a semiconductor forum moderator, an anonymous chip blogger, to an investment research firm founder, hedge fund founder, and more roles.)

His entry into the industry was also quite "tumultuous."

As early as age 8 to 12, he was highly active on semiconductor forums as a "forum warrior" (Odaily Planet Daily Note: similar to the domestic tech enthusiast forums like "贴吧," what we commonly call "forum warriors"), teaching himself semiconductor knowledge by reading chip documentation through repairing hardware like Xbox and discussing with community enthusiasts.

Thus, starting as an anonymous chip blogger, he began sharing chip knowledge, discussing chip manufacturing techniques, chip industry supply chains, and other hardcore topics on platforms like Reddit, WordPress, and Silicon Twitter.

In May 2020, Dylan officially founded his personal blog channel, SemiAnalysis, with the goal of providing accurate, independent technical analysis of the semiconductor industry. Looking at that time, before the "AI explosion driven by GPT," the semiconductor industry was still a niche technical field, and there was very little in-depth content of this kind on the market.

Initially, SemiAnalysis was just a very niche personal content channel built on WordPress. Upon repeated suggestions from his good friend Doug, Dylan later migrated it to the Substack platform and switched from a free model to a paid subscription model. (Odaily Planet Daily Note: According to Dylan, this friend joined Substack a few years later.)

From then on, Dylan began building his "personal business system" around the paid content channel, which includes technical content analysis, business consulting, and research report production on semiconductor supply chains, AI infrastructure products, cloud ecosystems, machine learning models, and even more high-tech industries.

SemiAnalysis: From a One-Person Company to a Global Team of Over 60

By 2025, SemiAnalysis has gradually transformed from Dylan's original "one-person company mode" (OPC) into a global company with a professional research team of about 60 people. They also established a professional chip and semiconductor product teardown lab, STEEL (SemiAnalysis Teardown Engineering & Evaluation Lab), in Oregon, USA.

Last year, the firm's revenue reached a scale of $20 million; this year, according to reports from The Information, SemiAnalysis's revenue is expected to exceed $100 million, primarily from hyperscalers, semiconductor giants, startups, and institutional subscriptions/models/consulting. Dylan himself has indicated plans to subsequently establish a VC investment firm. Previously, he had personally invested in about 20 startups, either individually or through SPV structures, and even helped compute giant Fluidstack raise $50 million in funding through an SPV structure.

External Influence: High Recognition from Jensen Huang, AMD CEO, and Others

After nearly 6 years of development, Dylan and SemiAnalysis have become the "industry textbook" and "must-read guide" in today's AI and semiconductor sectors.

Previously, NVIDIA founder Jensen Huang mentioned SemiAnalysis multiple times in his speeches at GTC Developer Conferences and publicly praised the details of its reports, especially regarding NVIDIA's InferenceX benchmarks, which amounted to a form of "public endorsement."

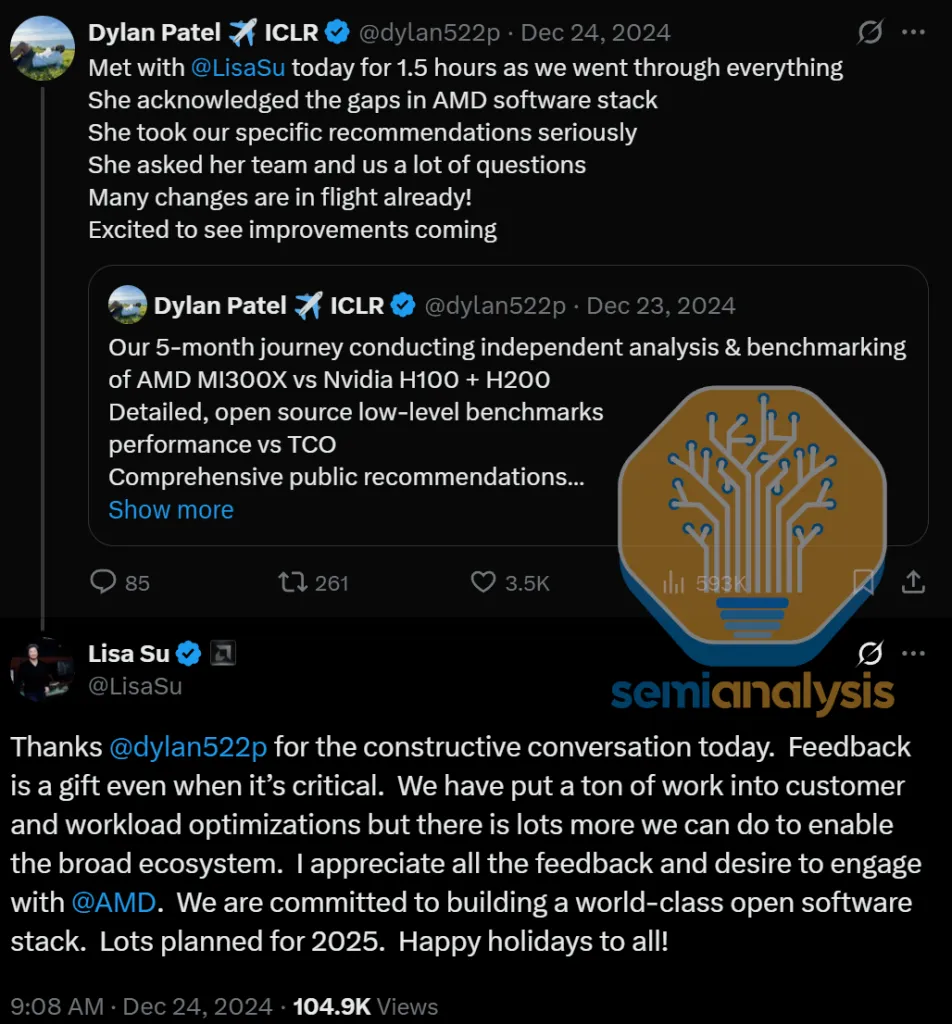

Earlier, in December 2024, after about 5 months of in-depth testing and benchmarking of AMD's MI300X GPU, the SemiAnalysis team published a critical report titled "MI300X vs H100 vs H200 Benchmark Part 1: Training - CUDA Moat Still Alive." The report pointed out that although the AMD MI300X GPU had good hardware specifications on paper, its ROCm software stack had significant shortcomings (e.g., many bugs, poor usability, immature ecosystem), leading to a far inferior actual user experience compared to NVIDIA's CUDA software stack architecture, making it ineffective as a powerful product for training work.

Within hours of the report's release, AMD CEO Lisa Su personally contacted Dylan and spoke with him the next day. Notably, this conversation was originally scheduled for 30 minutes but was extended to 90 minutes due to the large amount of information, numerous feedback issues, and technical detail exchanges involving engineers. This is a rare, in-depth dialogue between the CEO of a multi-hundred-billion-dollar market cap listed company and an independent third-party investment research firm. In the end, Lisa Su publicly thanked him for his "constructive feedback" (even if it was critical) (Odaily Planet Daily Note: Original quote: Feedback is a gift even when it's critical).

AMD CEO Lisa Su's high praise and positive response

In April 2025, SemiAnalysis released a follow-up report again, stating that "more than 4 months later, AMD has accelerated progress in ROCm, developer relations, CI/CD, etc., and the AMD MI450X is expected to beat NVIDIA," also acknowledging AMD's subsequent improvements, making it a landmark case of "independent research directly influencing major company decisions."

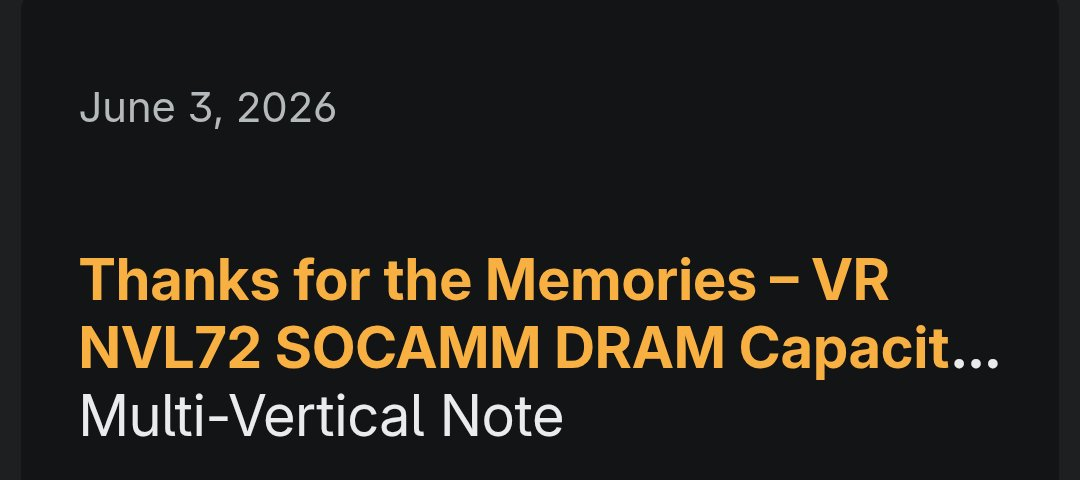

In early June, Citrini analyst Jukan forwarded part of a SemiAnalysis research report, which indicated that "NVIDIA's next-generation AI server cluster Rubin NVL72 made major adjustments to its memory configuration. To cope with tight supply chains and ensure the on-time delivery of Rubin racks, the single-rack capacity was drastically reduced from the original plan of 55TB to 28TB, a reduction of about 50%, using scaled-down 96GB SOCAMM memory modules instead of the previous high-end 192GB modules." Possibly affected by this news, that day, many memory-related stocks, including Micron and SK Hynix, fell under pressure.

In response, Dylan replied: "I love it: when people forward what we say, they often take it out of context. Actually, the original title of our report wasn't this clickbait-style." The image he subsequently posted showed the original report title was "Thanks for the Memories...".

In comparison, SemiAnalysis pays more attention to "technical implementation details," focusing on the real bottlenecks in AI construction (power shortages, supply chain inheritance, inference scaling, NVIDIA ecosystem dynamics, etc.). In optimistic demand judgments, they often embed realistic constraint analysis, making it more suitable for guiding specific investments and industry decisions. For more details on SemiAnalysis, see "From Community 'Hardware Nerd' to AI Circle 'Muddy Waters': How Does SemiAnalysis, With Nearly $100 Million in Annual Revenue, Stir the Semiconductor Market?"

Recommended Reading:

Latent Space Episode 1: Situational Cooking with SemiAnalysis Founder Dylan Patel