2022年8月8日,美国财政部宣布制裁部分与Tornado Cash协议或与之相关的以太坊地址进行交互的地址。

背景

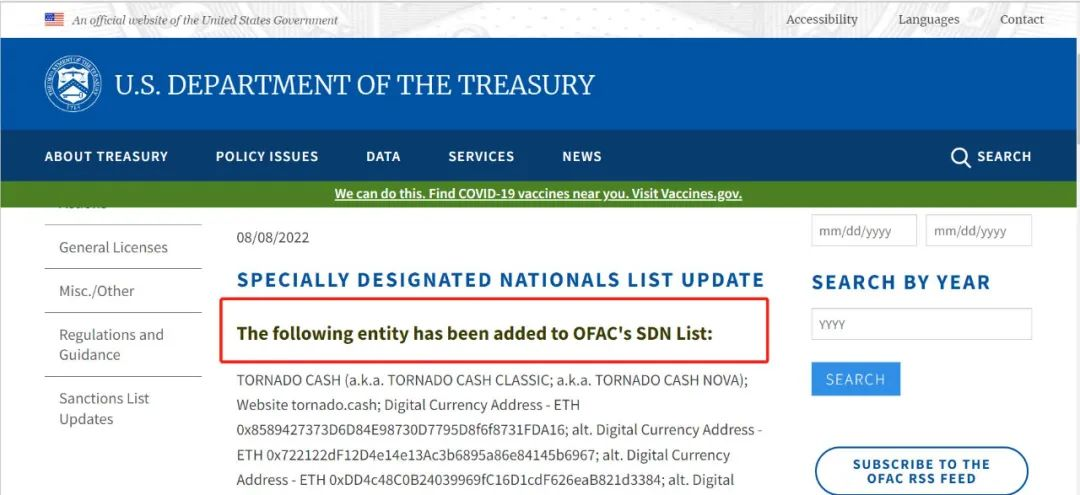

2022年8月8日,美国财政部的海外资产控制办公室(The Office of Foreign Assets Control of the US Department of the Treasury)简称OFAC,的官网显示,将部分与Tornado Cash协议或与之相关的以太坊地址进行交互的地址,放入SDN List(美国特别制定国民名单)

来源:美国财政部

这里解释一下这个SDN List:美国特别指定国民名单是什么,如果被加到了这个名单,名单中的人员会根据OFAC管理的各种制裁计划,个人或者相关实体的财产和财产权益会被冻结。

怎么制裁?

注意,一般而言,美国人(US persons,包括美国公民、合法永久居民、根据美国法律设立的实体以及位于美国的其他组织等)不得与SDN进行任何交易,并且必须冻结他们拥有或控制的SDN的财产和财产权益。SDN也不得接入美国的金融系统。OFAC和美国国务院同时规定牵连美国人违反SDN禁令的外国人可能会受到《国际紧急经济权力法》( International Emergency Economic Powers Act,简称 IEEPA)下的民事和刑事处罚。同时,若外国人就某些商品和服务与SDN List中的实体进行重大交易,则其也可能会受到美国的二级制裁。因此,SDN与非美国人的交易也会在一定程度上受到不利影响。此外,被纳入SDN List也会使得个人或企业遭受一定的声誉损失。

参考资料:

http://www.jcacherm.com/portal/article/index/id/6/cid/4.html

OFAC是个什么机构?

OFAC是个什么机构?

OFAC的使命在于管理和执行所有基于美国国家安全和对外政策的经济和贸易制裁,包括对一切恐怖主义、跨国毒品和麻醉品交易、大规模杀伤性武器扩散行为进行金融领域的制裁,目前的OFAC 仍然是美国最重要的针对特定国家、地区和人员进行的经济和贸易制裁的政府部门。近年来,随着世界性的反贪腐、反洗钱运动的深入,OFAC的政策和指令,已经成为世界金融业,尤其是美国和与美国金融业有密切联系的金融机构无法忽略的经营原则。

有哪些可能的原因?

其实,美国财政部在2022年5月,就对另一个混币服务Blender进行过制裁,理由是它涉嫌帮助某国官方黑客组织(这里主要指Lazarus Group)清洗从 Axie Infinity 窃取的部分资金。

2022年3月23日,FBI对入侵Ronin进行了认定,不法黑客组织为Lazarus Group,而Tornado Cash经常被用作很多犯罪场合。

截至2022年5月初(当时的计价),Lazarus Group已经向Tornado Cash转移了37000个以太坊,大约1亿美元。有专家认为,Tornado Cash目前有172,000个以太坊的余额,在5月左右,某国官方黑客的黑钱,占Tornado Cash智能合约所持余额的20%。

但没有任何可行的方法,能够阻止Lazarus Group往里面添加黑钱。尽管 Tornado Cash运营方也尝试过很多努力,但是并不能限制洗钱,也不能阻止部分不法分子的存款和提款。

根据法律专家Nicholas Weaver的观点,2022年4月19日,Lazarus Group钱包中得到了18256个以太坊(大约5000万美元)。4月28日和29日,这些以太坊被转移到 Tornado Cash,而OFAC发布制裁的12天后,Tornado Cash接受了来自这些被黑来的以太坊。因此OFAC开始考虑对Tornado Cash的制裁,特别是提出这个钱包本身应该被列为受制裁的实体,认为所有参与这个资金池的其他人都在帮助隐藏某些黑来的钱,可能这已经是OFAC计划对Tornado Cash采取行动的开始...