Crypto analytics firm Santiment says that the dwindling supply of stablecoins may be a sign that a massive Bitcoin (BTC) breakout is on the horizon.

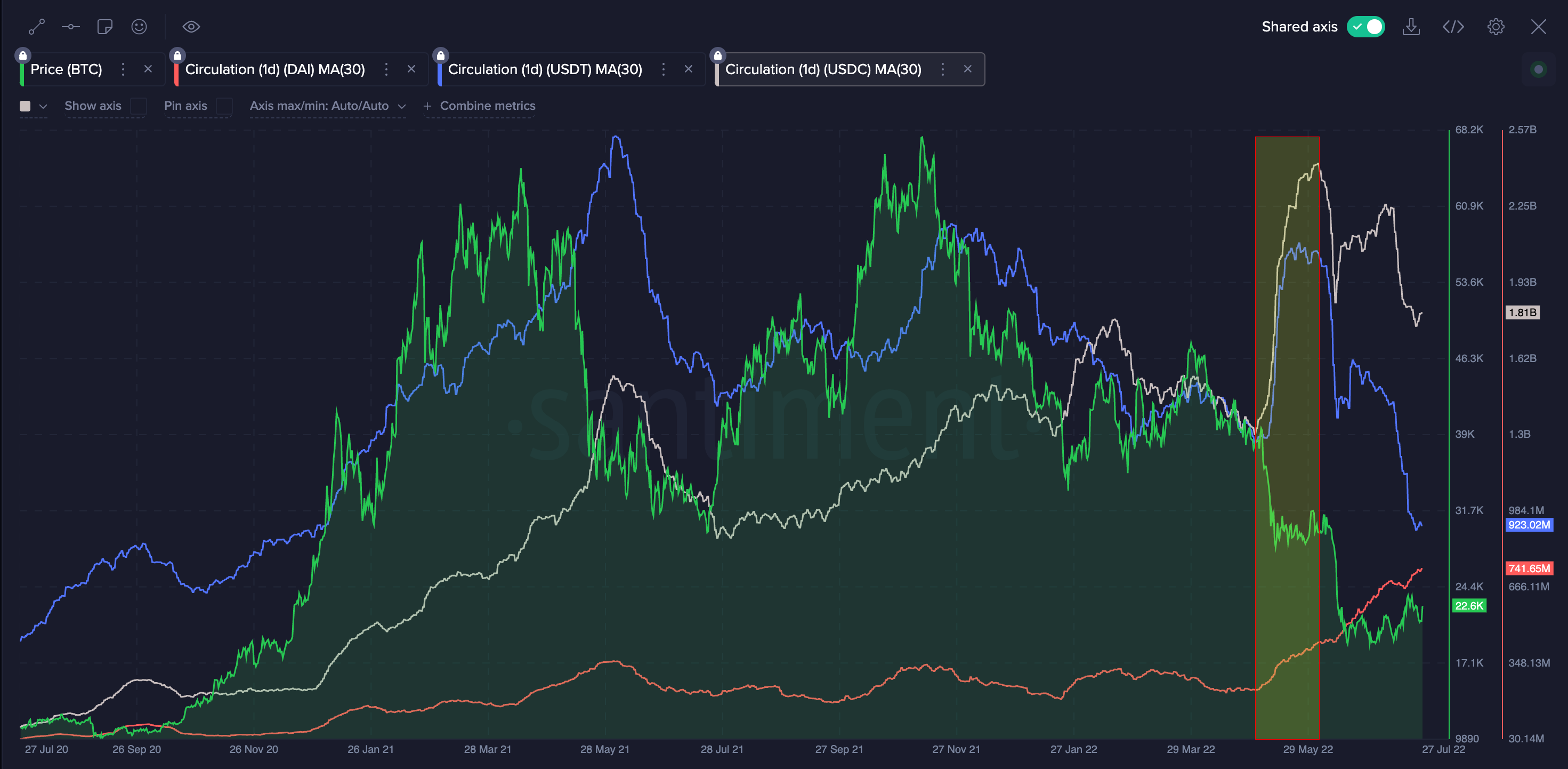

According to the market intelligence firm, the circulating supply of Tether (USDT) and USD Coin (USDC), the two biggest stablecoins by market cap, has been dramatically decreasing since May 2022.

Santiment says that the volume of these two assets continues to decline even as the price of Bitcoin rises, which in the past has foreshadowed parabolic BTC rallies, specifically in July 2021 right before the king crypto went from the $29,000 level all the way to $69,000.

“Stablecoin circulation kept going down even on a growing market. We might say that [the] first significant growth happened on a decreasing circulation. Stablecoins tried to heat up strongly, but no, the market didn’t go up.

The best pattern could be [stablecoins] still decreasing [during a] recovering market. Like nowadays. When stablecoins don’t believe in recovery yet, preferring to wait. We’re probably witnessing the same as July 2021 now, at least on two stablecoins.”

Source: Santiment

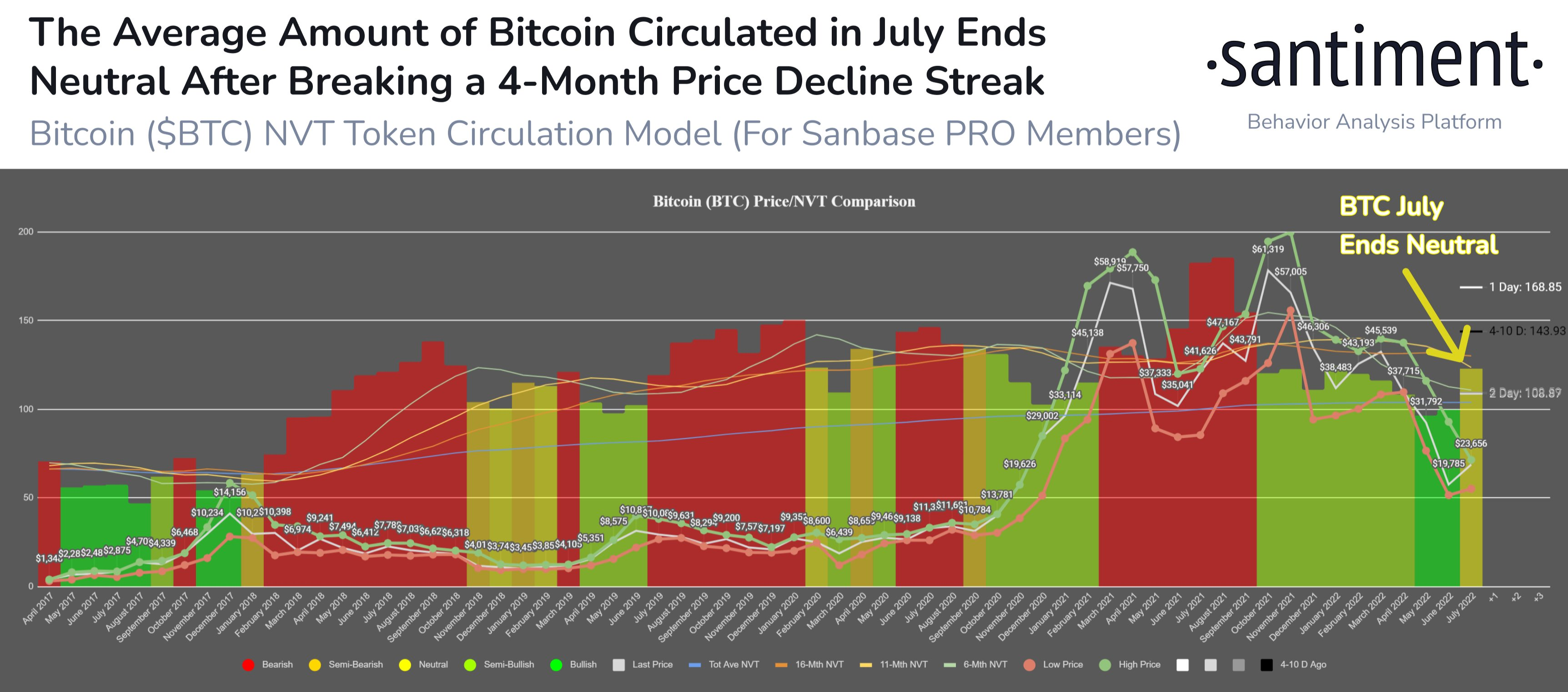

Santiment also notes that Bitcoin’s price is now in line with its valuation based on the network value-to-transaction (NVT) model, a metric aiming to gauge an asset’s price based on the ratio between its daily market cap and daily circulation.

“Bitcoin jumped +18% in July after [the] NVT model’s growing bullish divergence in May and June finally saw a price bounce come to fruition. With a neutral signal now as prices have risen and token circulation has declined slightly, August can move either direction.”

Bitcoin is changing hands at $23,297 at time of writing, a 1.25% dip on the day.