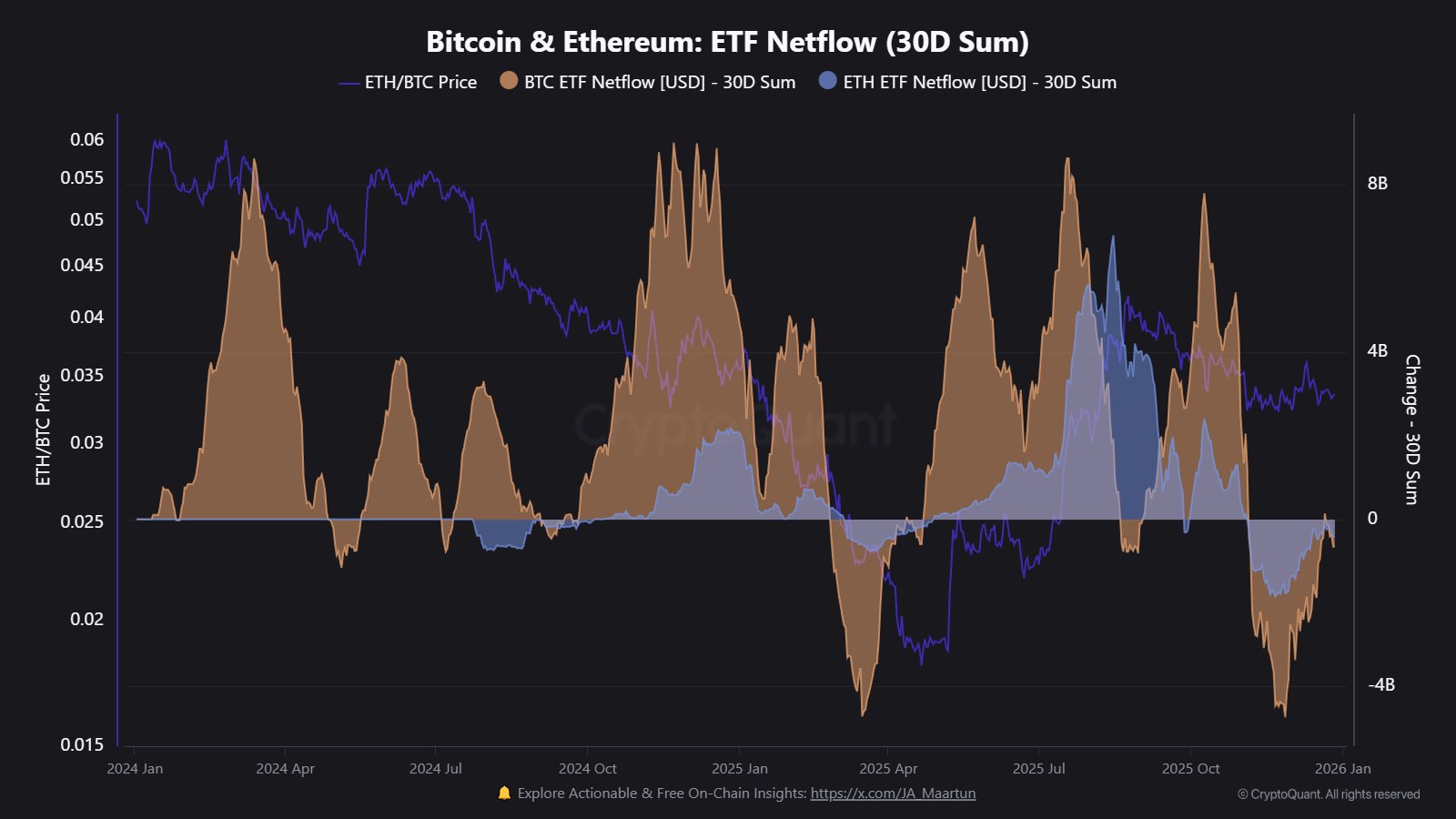

Data shows the 30-day ETF netflow is still negative for both Bitcoin and Ethereum, suggesting capital has been flowing away from the digital assets.

Bitcoin & Ethereum ETF Netflows Have Been Negative Recently

As explained by CryptoQuant community analyst Maartunn in a new post on X, Bitcoin and Ethereum spot exchange-traded funds (ETFs) have faced a negative netflow over the past month.

Spot ETFs are investment vehicles that allow investors to gain indirect exposure to an underlying asset’s price movements. In the context of cryptocurrencies, this means that an ETF investor never has to interact on-chain; the fund buys and custodies the tokens on their behalf.

US spot ETFs are a relatively new phenomenon in the digital asset sector, only getting approval by the Securities and Exchange Commission (SEC) in January 2024 for Bitcoin and July 2024 for Ethereum.

Spot ETFs can look like a convenient mode of investing for traders unfamiliar with cryptocurrency wallets and exchanges. Institutional entities, in particular, prefer to gain exposure through them.

Since their arrival, these investment vehicles have quickly gained popularity by tapping into this demand from the traditional investors and established themselves as one of the cornerstones of the sector.

Below is a chart that shows how the 30-day netflows related to the Bitcoin and Ethereum spot ETFs have changed during their existence so far.

Looks like the value of the metric has been negative for both of these assets in recent weeks | Source: @JA_Maartun on X

As is visible in the graph, the 30-day spot ETF netflow has been negative for both Bitcoin and Ethereum since a while now, suggesting that the funds have been witnessing sustained net outflows.

The situation has improved a bit most recently, but the indicator is still red for both assets, sitting at -$656 million for BTC and -$422 million for ETH. The weak demand in the market is similar to the phase of outflows from the first half of 2025.

Back then, demand eventually made an explosive return, with Bitcoin and Ethereum witnessing sharp price rallies. It now remains to be seen whether a comeback will happen this time or if the slowdown in demand is here to stay for now.

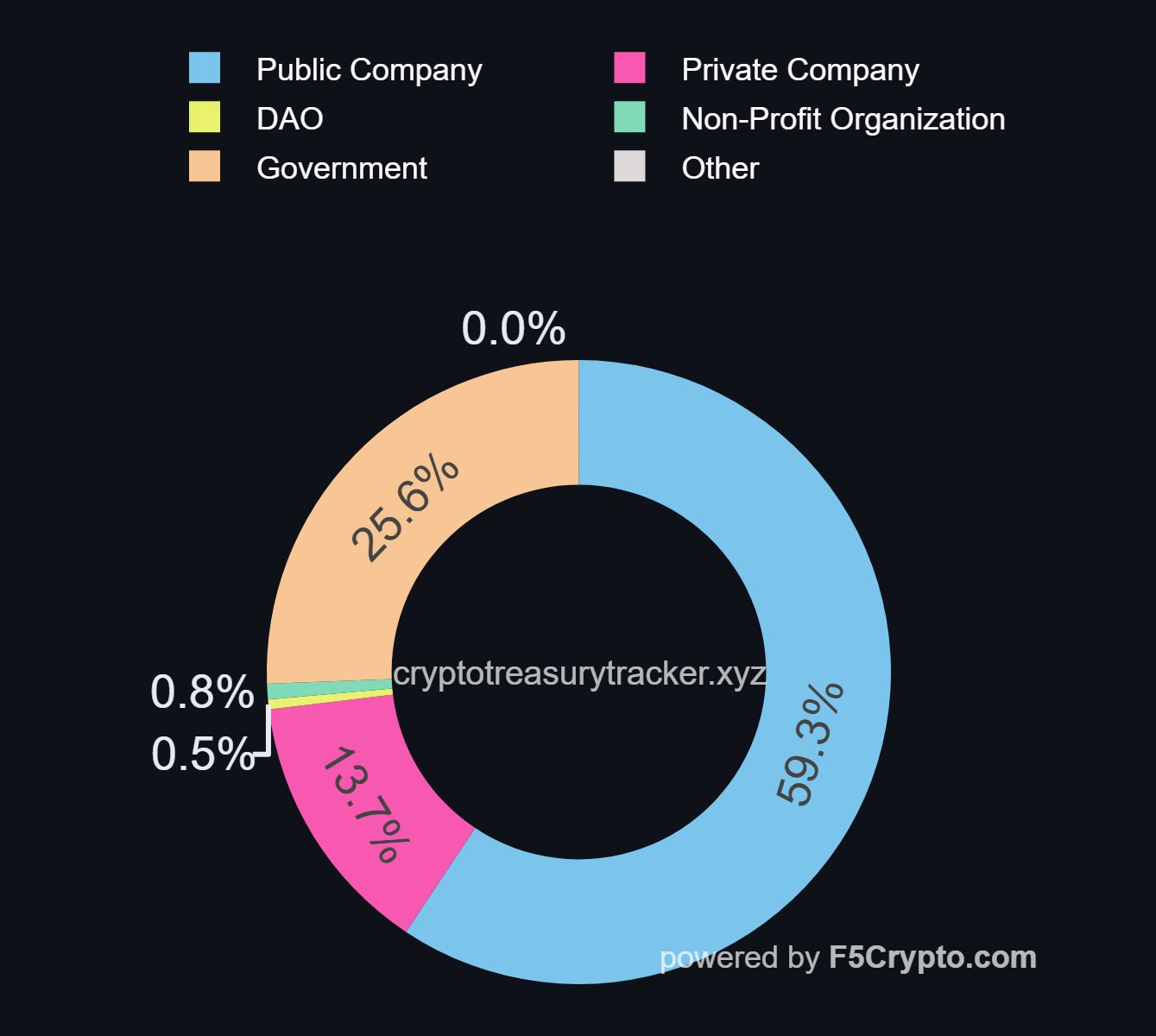

Another relatively recent source of demand in the market is digital asset treasuries. As highlighted by institutional DeFi solutions provider Sentora in a new X post, holdings of cryptocurrency treasuries now exceed $185 billion across 368 entities.

The breakdown of treasuries across various sectors | Source: Sentora on X

Out of this amount, 73% of the digital asset treasuries are controlled by companies, while the rest is in the hands of governments.

BTC Price

At the time of writing, Bitcoin is trading around $88,100, unchanged from last week.

The price of the coin seems to have been consolidating recently | Source: BTCUSDT on TradingView