近期,一家名为Mystonks的“美股上链”平台因冻结用户资金而引发广泛争议。据了解,该平台以“用户资金来源不合规”为由扣留了大量资产。

从金融合规的角度看,这种处理方式是极不寻常的。一家规范的金融机构在识别到可疑资金时,标准做法是拒绝接收并原路退回,同时向监管部门提交报告。平台方直接“扣留”资产,本身就对其声称的“合规性”打上了一个巨大的问号。

而Mystonks平台,一直以持有美国MSB牌照和合规发行STO作为其核心宣传点。那么,这些所谓的“合规”资质,真相究竟如何?笔者进行了一番调查。

一、 “合规STO”的真相:备案不等于许可,私募不等于公开

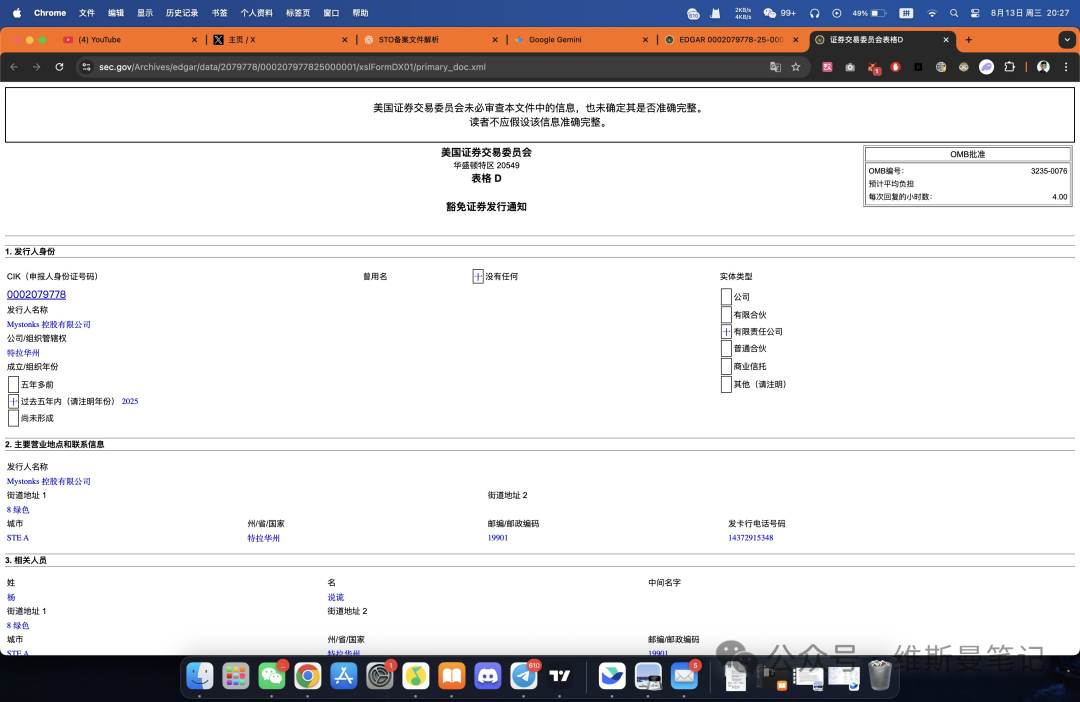

在探究过程中,笔者发现Mystonks的宣传并非毫无根据。在美国证券交易委员会(SEC)的公开数据库中,确实能查到 Mystonks Holding LLC这家公司的备案信息。

这份文件(Form D)的核心要点如下:

●备案类型:基于Regulation D 506(c)规则的私募豁免。

●发行对象:仅限“经认可的投资者”(Accredited Investors)。

●发行规模:57.5万美元,且最小投资门槛为5万美元。

这份文件恰恰是问题的关键所在,也是平台宣传中误导性最强的地方。

首先,Form D是一份通知性备案,而非经营许可。它只代表公司向SEC告知了有一次私募的发行行为,SEC仅作存档,不代表对该公司资质、项目真实性的任何审核或背书。

其次,也是最重要的一点,该备案严格限定了发行对象。Regulation D是为私募设计的豁免条款,其目标是少数符合资格的富人或机构投资者(即“经认可的投资者”)。而Mystonks作为一个向公众开放的交易平台,其绝大多数用户显然不符合此标准。

因此,Mystonks的行为可以理解为:拿着一份仅限于向少数富人小范围募资的备案文件,去公开从事需要严格牌照的证券交易业务。

这种做法,本质上是利用普通投资者对美国证券法规的陌生,进行的概念混淆。要合法地向公众提供证券代币交易服务,平台需要的是**ATS(另类交易系统)或Broker-Dealer(经纪自营商)**等高阶牌照,而这与一份简单的Form D备案有着天壤之别。

二、 被滥用的MSB牌照:与资金安全无关的“反洗钱”备案

谈完相对复杂的STO,我们再来看那个更为普遍的宣传工具——美国MSB牌照。

关于MSB牌照,投资者需要认清一个核心事实:它的价值和意义被市场上的许多项目方严重夸大了。

MSB(货币服务业务)的监管机构是美国财政部下属的FinCEN,其核心职责是反洗钱(AML)。也就是说,FinCEN只关心平台是否按规定上报可疑交易,以打击金融犯罪,但它完全不负责保障用户的资金安全、审查平台的商业模式或技术能力。

更重要的是,MSB的申请门槛极低,通过中介机构,在海外即可轻松完成注册,甚至无需在美国设立实体办公室。这使其成为许多项目低成本、快速“包装”自身合规形象的首选道具。

当一个主要服务于非美国用户的平台,反复强调其MSB牌照时,投资者需要明白,这更多是一种营销策略,而非其具备强大金融实力的证明。

结语:从Mystonks看懂一类平台的“合规”套路

Mystonks的案例并非孤例,它为我们清晰地揭示了一类平台在灰色地带惯用的“合规”包装手法。放眼市场,大量交易所和金融平台都在复用着类似的剧本,投资者需要对此建立清醒的认知。

这类平台的典型套路可以归纳为:

1. 第一步:用MSB牌照作为营销的“敲门砖”。利用其“美国官方”的背景和极低的获取成本,快速建立基础的、看似可靠的形象。

2. 第二步:用“偷换概念”的方式解读证券备案。将一份有限的、有严格限制条件的备案文件(如私募备案),包装成全面的、可向公众提供服务的经营许可,利用信息不对称进行深度误导。

3. 第三步:利用地域和法律差异进行“精准营销”。它们深知其业务无法在美国本土落地,便专攻对美国法规不熟悉的海外用户,形成“墙内开花墙外香”的局面。

作为投资者,我们应当从这些套路中吸取教训。在判断一个平台是否真正合规时,请记住两个基本原则:

●真正的合规是昂贵的、有形的。它意味着高昂的牌照申请费、保证金、实体办公室租金和本地法务团队开销。那些轻易获得的、看不见摸不着的“合规”,其价值也必然是廉价的。

●真正的合规是透明的、具体的。它敢于清晰地公示其牌照类型、编号、监管范围和限制条款。凡是模糊的、大而化之的“合规”说辞,背后往往都经不起推敲。

在投资决策中,请将“合规”二字从一个营销词汇,还原成一个需要被严格审视的法律事实。守住这条底线,才能最大程度地保护我们的资产安全。