随着全球打击网络诈骗、地下支付网络和非法跨境洗钱活动的力度持续加大,名为汇旺支付(HuionePay) 的平台引起了监管的高度关注。该平台涉嫌被用于诈骗资金的接收、转移及出金,尤其是在 TRON 链上通过 USDT 频繁进行链上操作。

为进一步揭示其链上行为特征,慢雾(SlowMist) 基于链上反洗钱与追踪工具 MistTrack 与链上公开数据构建了 Dune 数据统计面板,并在此基础上开展了对汇旺支付(HuionePay) 在 TRON 链上 USDT 存取行为的深入分析。

注:本文数据时间范围为 2024 年 1 月 1 日至 2025 年 6 月 23 日,数据源自慢雾(SlowMist) 制作的数据统计面板:https://dune.com/misttrack/huionepay-data。

链上资金流动

汇旺支付(HuionePay)总存取金额(Sum)

- 提现总额:57,246,854,379 USDT

- 存款总额:54,475,887,524 USDT

存取金额均超过 500 亿 USDT,显示出汇旺支付(HuionePay) 在过去一年半内持续存在大量资金流入与流出,且提现金额始终高于存款金额,两者差值达 27.71 亿 USDT,有较明显的“资金净流出”特征。

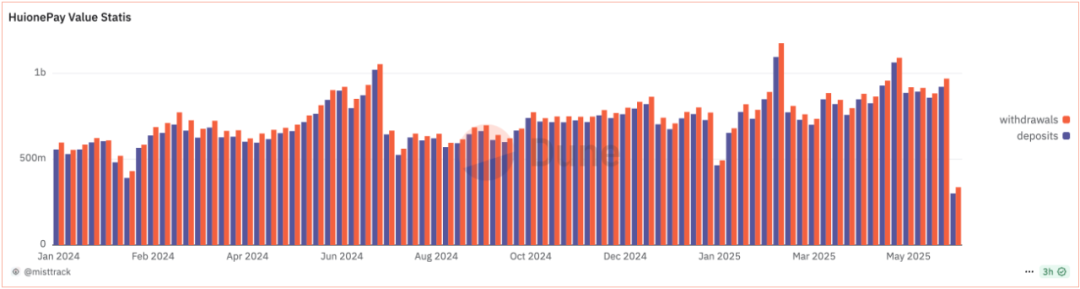

每周资金动向(Value Statis)

图表数据显示,汇旺支付(HuionePay)平台上的资金流动持续活跃,并在以下三个时间节点出现峰值:

- 2024 年 7 月 8 日:首次出现明显高峰,充值与提现均突破 10 亿 USDT。

- 2025 年 3 月与 5 月:两次提现金额接近或超过 11 亿 USDT。

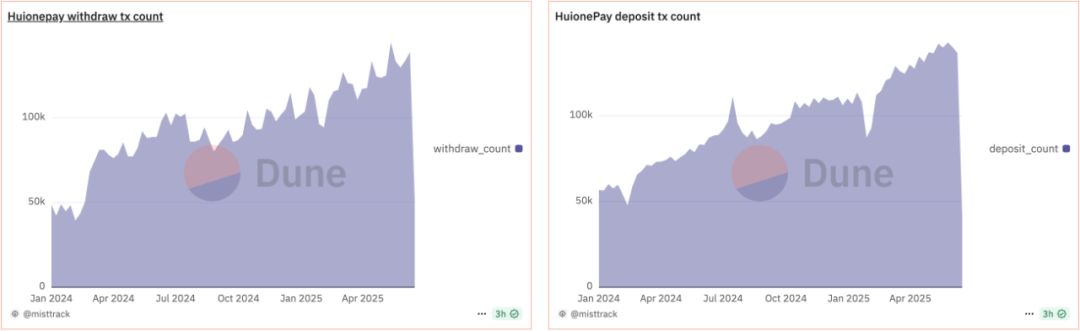

存款/ 提现交易笔数(Tx Count)

数据显示,提现交易笔数自 2024 年 2 月起呈阶梯式上升,在 2025 年 5 月 12 日达到峰值,单日接近 15 万笔,呈现出“高频提款”特征。

相较之下,存款交易数量虽整体增长,但波动较小,存款笔数也稳步增长至每日近 14 万笔,整体用户活跃度并未明显下降。

此外,2025 年 3 月与 5 月的提现金额高峰伴随着交易笔数的同步上涨,两个高峰几乎重合。

用户行为

存取用户数(Users)

自 2024 年初以来,汇旺支付(HuionePay) 在 TRON 链上的活跃存款地址数量从不足 3 万增长至超过 8 万,呈现出稳定增长趋势。需要说明的是,图表数据按地址去重统计,即存款地址大致可视为用户数量,而提现地址则可能为用户自定义的接收地址,无法等同实际用户。存款地址数量的持续增长表明平台仍在不断吸引新用户,不过增长速度呈缓和态势。

活跃地址

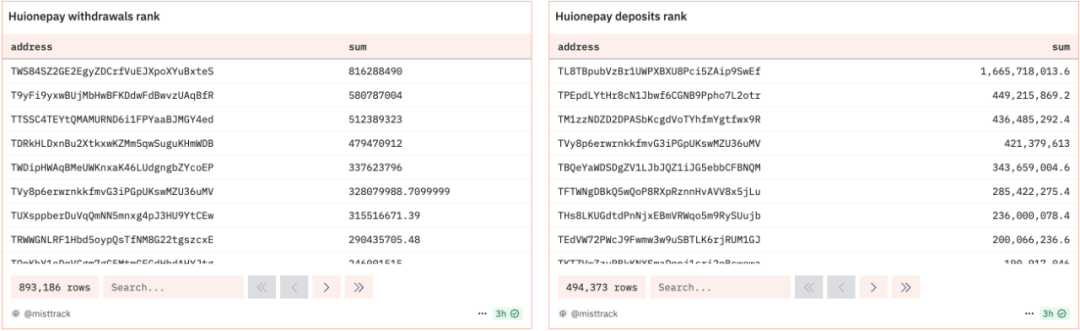

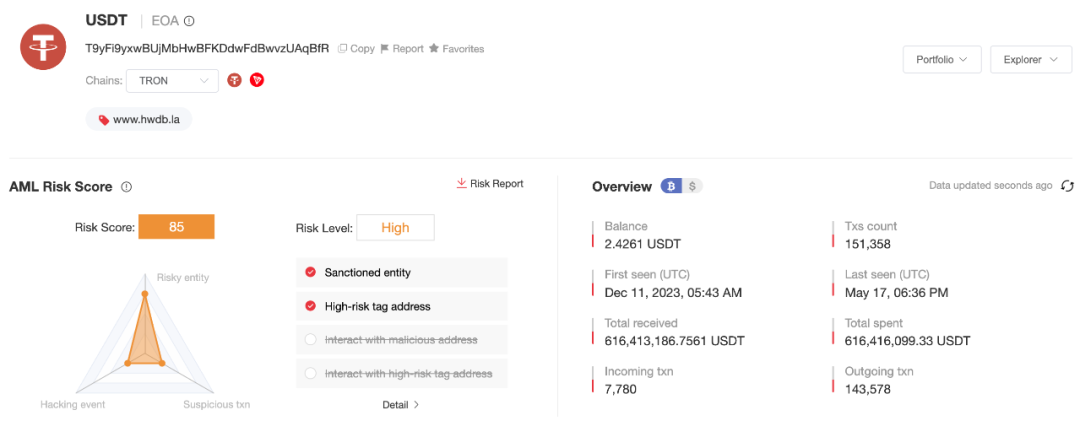

提现地址Top 3

我们使用链上反洗钱与追踪工具 MistTrack 进行分析,汇旺支付(HuionePay) 平台的提现行为呈现出一定程度的“资金集中”特征。其中,排名前三的提现地址如下:

- 地址1 — TWS84SZ2GE2EgyZDCrfVuEJXpoXYuBxteS — 8.16 亿 USDT

- 地址2 — T9yFi9yxwBUjMbHwBFKDdwFdBwvzUAqBfR — 5.8 亿 USDT

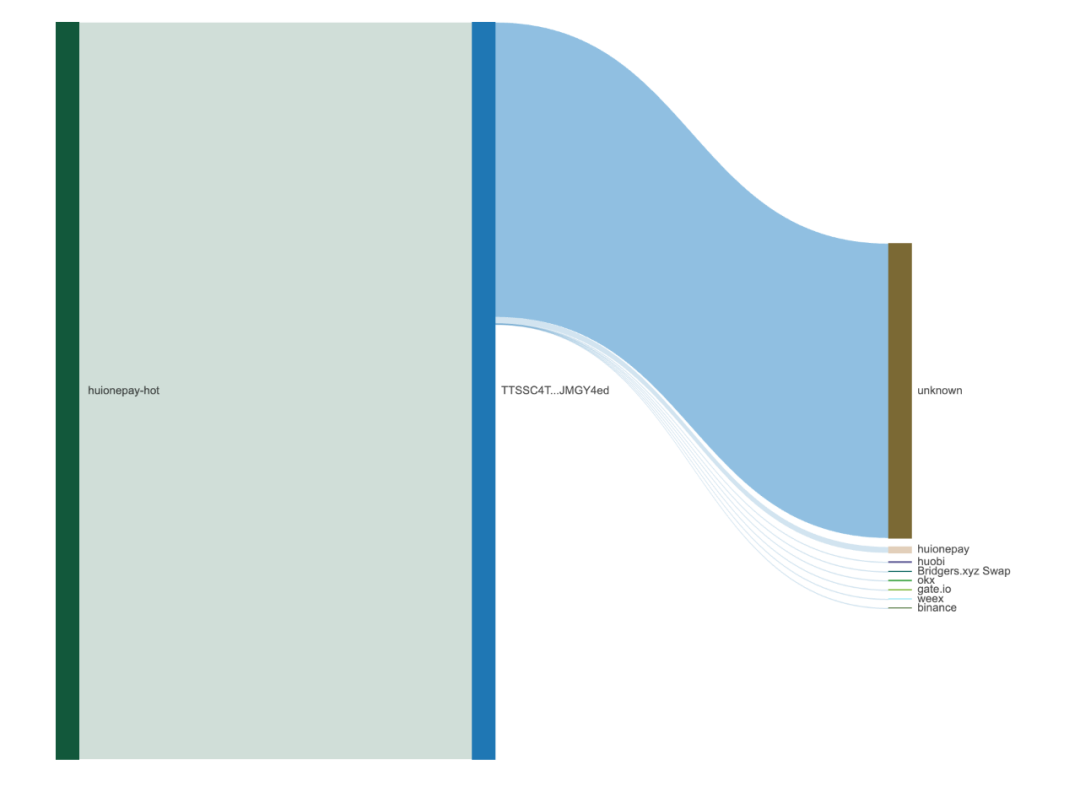

- 地址3 — TTSSC4TEYtQMAMURND6i1FPYaaBJMGY4ed — 5.12 亿 USDT

上述地址的最早交易均可以追溯至 2023 年,长期活跃,链上痕迹丰富。

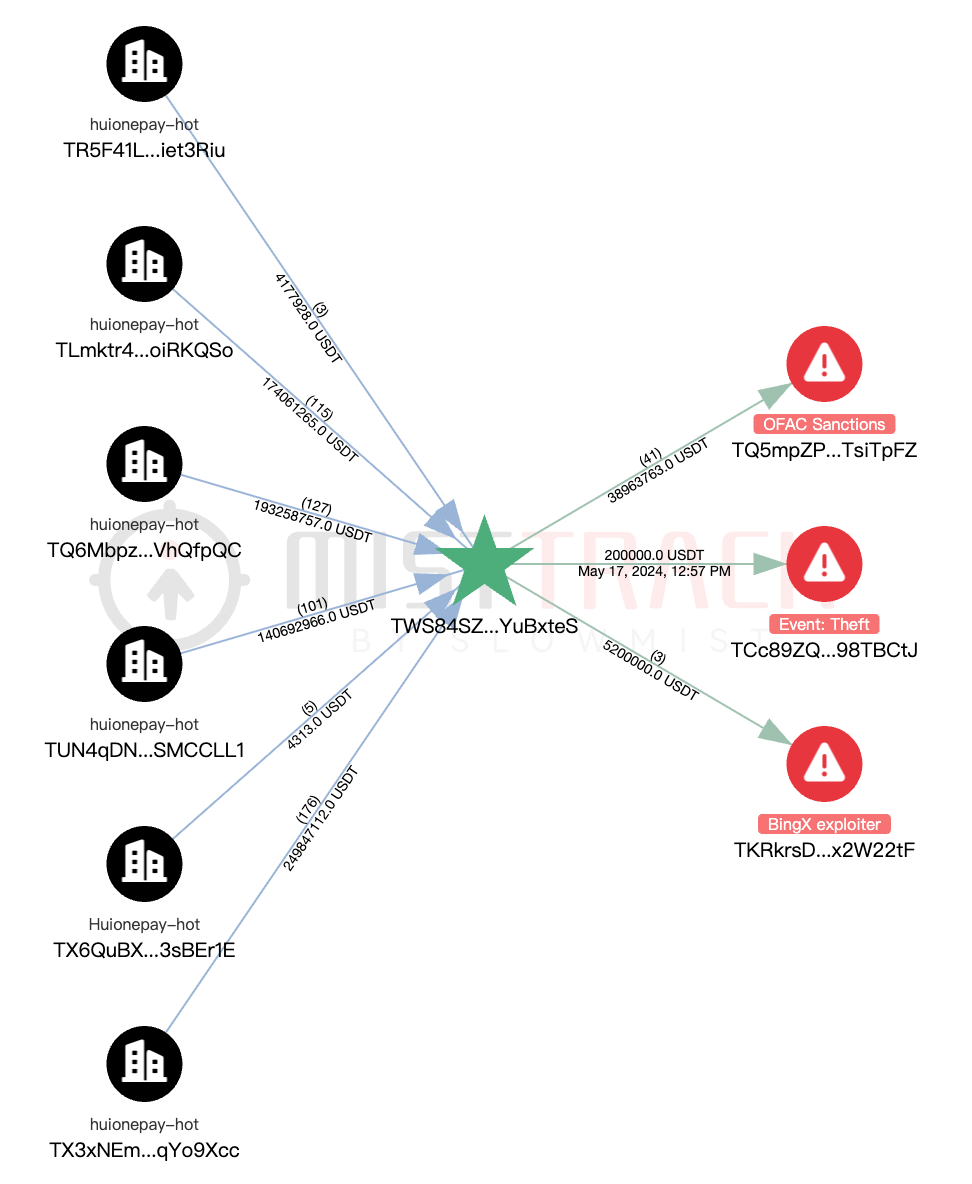

地址 1 不仅从多个汇旺支付(HuionePay)热钱包提币,还与被 MistTrack 标记为“OFAC Sanctions”、“Theft”、“BingX Exploiter”的地址存在交互:

地址2 疑似为好旺担保(原汇旺担保)平台控制的钱包地址。

地址3 与多个交易平台发生交互:

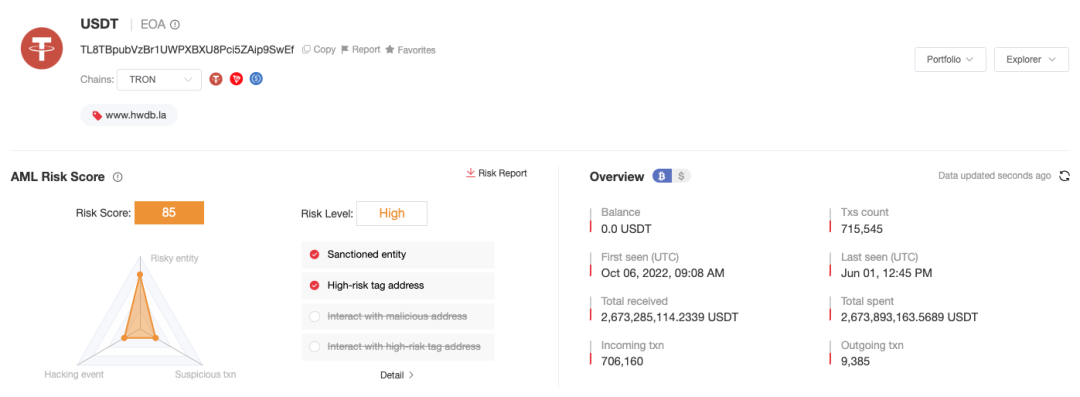

存款地址Top 3

- 地址4 — TL8TBpubVzBr1UWPXBXU8Pci5ZAip9SwEf — 16.65 亿 USDT

- 地址5 — TPEpdLYtHr8cN1Jbwf6CGNB9Ppho7L2otr — 4.49 亿 USDT

- 地址6 — TM1zzNDZD2DPASbKcgdVoTYhfmYgtfwx9R — 4.36 亿 USDT

其中,地址4 的存款高达 16 亿 USDT,为提现金额最高地址的 1.3 倍,最早一笔交易可追溯至 2022 年,疑似为好旺担保(原汇旺担保)平台控制的钱包地址。此外,地址 5 和地址 6 疑似为某平台热钱包地址。

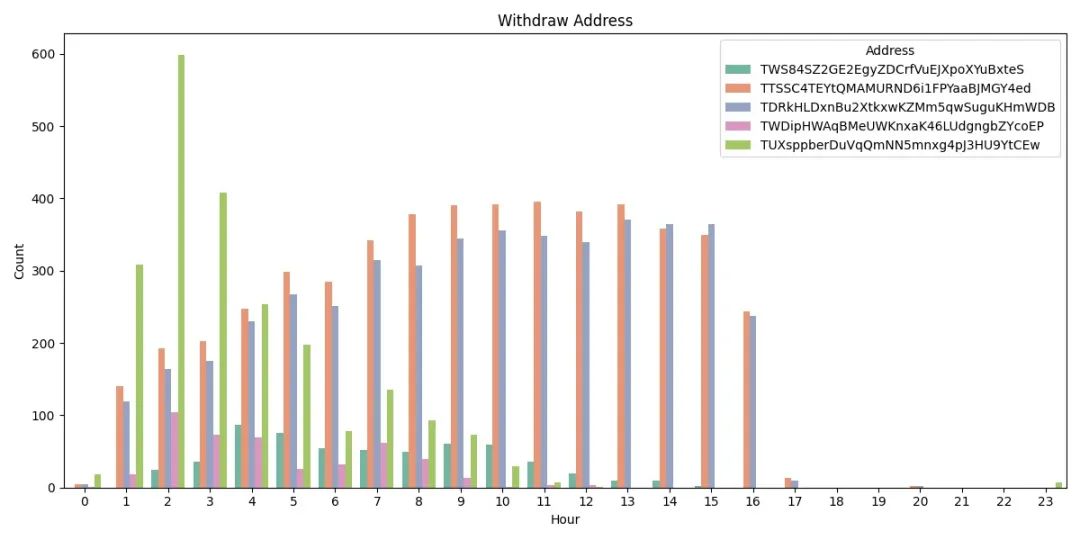

活跃时间

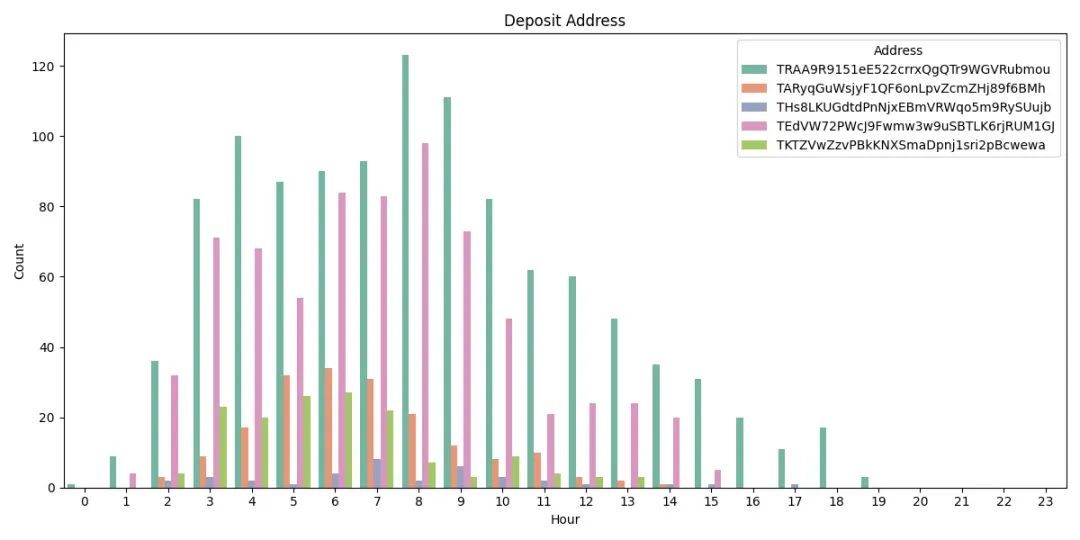

我们随机选取了 10 个在汇旺支付(HuionePay) 进行存款和提现的普通地址,对其操作时间(UTC) 进行统计如下图:

被选取地址的提现交易主要集中在 UTC 时间 01:00 – 16:00,其中 07:00 – 13:00 为高频时段。个别地址,如 TUXsppberDuVqQmNN5mnxg4pJ3HU9YtCEw 在 02:00 – 03:00 出现交易突增。部分提现地址在 15:00 – 次日 00:00 几乎无交易。

被选取地址的存款操作主要集中在 UTC 时间 03:00 – 10:00,与提现地址的活跃时段部分重合。其中,存款地址 TRAA9R9151eE522crrxQgQTr9WGVRubmou 和 TEdVW72PWcJ9Fwmw3w9uSBTLK6rjRUM1GJ 在 03:00 – 09:00 表现出稳定的资金存入行为。

国际监管动态补充

近期的一系列国际监管与执法动态加剧了对 HuionePay 的关注:

- 2024 年 7 月 14 日,Bitrace 表示,Tether 冻结了与 Huione 有关的地址 TNVaKW,金额高达 2,962 万 USDT,该地址疑为担保相关操作钱包。

- 2025 年 5 月 2 日,美国财政部金融犯罪执法网络(FinCEN) 提议禁止美国金融机构为总部位于柬埔寨的 Huione Group 提供代理账户服务。美国财政部长称 Huione 是“网络犯罪分子的首选市场”,涉及平台包括 Huione Pay、Huione Crypto 及 Haowang Guarantee 等。

- 2025 年 5 月 8 日,联合国毒品和犯罪问题办公室(UNODC) 在其报告中指出,Huione Guarantee 已成为东南亚“网络诈骗产业化生态系统”的一部分,其平台累计接收超 240 亿美元加密资金。

- 2025 年 5 月 14 日,Elliptic 报告称,Telegram 封禁了数千个与“Xinbi 担保”相关的加密犯罪频道,平台处理超 84 亿美元可疑交易,与 Huione Group 并列最大加密黑市。

- 2025 年 5 月 15 日,好旺担保(原汇旺担保)在官网宣布因被 Telegram 屏蔽,将正式停止运营。

写在最后

汇旺支付(HuionePay) 在 TRON 链上的资金流动情况、交易频次、活跃地址为进一步理解其链上活动提供了基础数据支持。