原文作者:ETHGlobal

原文编译:Felix, PANews

10 月 21 日,ETHGlobal 公布入围 ETHGlobal 旧金山黑客松决赛项目,本次竞赛共有 223 个项目参赛,最终 10 个项目脱颖而出,包括 PumpRoyale、VVLDrizzy 和 IP Infinity 等,涉及游戏、版权保护等领域。

本文带你详览这 10 个项目。

PumpRoyale

PumpRoyale 让用户在全球健身挑战中投入 USDC,完成活动,并从失败者池中赢得奖励。

在 PumpRoyale 中,全球用户可以在定期举办的全球比赛中投入任意数量的 USDC。比赛期间,系统会随机提示用户在提示后的 10 分钟内记录自己完成一项基本健身活动的情况。在规定时间内成功完成体育活动的人将获得其押金,而未完成的人将失去押金,这将形成一个失败者池。每场比赛结束后,系统都会随机抽取少数完成健身活动的人,并将获得失败者池的分配。

VVLDrizzy

VVLDrizzy 让创作者可以铸造、加水印和授权病毒式视频,同时赚取收入。媒体机构可以轻松授权经过验证的内容。由 Story Protocol 和 Walrus 提供支持。

VVLDrizzy(病毒式视频授权商)旨在让内容创作者和媒体机构能够轻松获得报酬或支付视频内容授权费用,帮助弥合传统媒体机构在 Web3 采用方面的差距。

IP Infinity

IP Infinity 将 NFT 转变为具有统计数据的游戏对象,并使用虚幻引擎和 AI 驱动的分类将它们集成到程序生成的世界中。

IP-Landers 是使用 AI 模型、区块链集成和游戏开发工具构建。Meta 的 Llama 3.2 视觉模型分析 NFT 图像,生成由 DeBERTa 零样本分类模型分类的文本描述,将它们分类为不同类型的对象。虚幻引擎为游戏提供动力,以程序生成的景观和地牢为特色,带来动态体验。Story Protocol 的平台允许协作创造,而不会产生 IP 纠纷。

OmiSwap

OmiSwap 使用 AI 可穿戴设备实现语音激活的区块链交易,支持跨链传输和无 gas USDC 发送,实现无缝加密交互。

该平台利用由 OpenAI 的 GPT 模型提供支持的高级 AI 来解释自然语言命令。该系统支持多个区块链网络,包括 Base、Polygon、Arbitrum 和以太坊。OmiSwap 使用 Coinbase CDP(加密开发平台)SDK 为不同区块链网络上的用户创建和管理钱包。OmiSwap 支持两种主要类型的交易:向平台上的其他用户转移加密货币(ETH 或 USDC),以及在 Base 网络上在 ETH 和 USDC 之间进行货币互换。

HelloACAI

HelloACAI 是基于代理的链上协作 AI 基础设施。

当前的通用 AI 有助于提出建议,但实际上并不能节省执行时间。AI 缺乏根据请求采取适当行动的能力。多个 AI 代理专注于研究、与网站交互、API、日历、付款等功能。当 AI 协作时,如何确保良好的互动?HelloACAI 通过智能合约做到这一点。与 AI 代理之间的交互受这些合约的约束。HelloACAI 还为通过智能合约构建的 AI 代理提供了注册表。

DAOsaster

DAOsaster 是一个去中心化的灾难响应系统,使用人工智能代理、无人机和区块链进行自主检测和协调,而不依赖于传统基础设施。

项目的初始阶段涉及使用无人机从本地和全球代理收集数据,无人机会调查并收集受灾地区的关键信息。这些数据(包括高分辨率视频文件和照片)存储在 Walrus 上。

为了将这些有价值的内容货币化并分发,利用 Story Protocol,使新闻记者等实体能够铸造和使用这些数据。通过此过程产生的任何利润都会汇回 DAO 合约,AI 代理会使用该合约来管理供应链。当灾难发生时,AI 代理会通过 SKALE 链发起彼此之间的通信,自主分配角色和协调行动。他们利用 Graph 协议快速查询和处理数据,确保响应迅速且高效的操作。

为了增强由 AI 代理管理的 DAO 的流动性和资金,用户可以将任何 AI 资产(从无人机到全能凝胶设备)代币化,从而为社区资源做出贡献。

Chain Waves

Chain Waves 允许用户在区块链上为音频文件添加水印并保护其安全,从而确保为创作者提供所有权证明、版税跟踪和自动争议解决。

工作原理:

铸造您的 IP:上传内容并将其铸造为 NFT。

收取版税:根据您设置的条款,在使用您的 IP 时自动收到版税。

争议解决:如果发现未经授权的使用,请启动由具有法律约束力的合同支持的争议程序。

使用 IP 作为贷款抵押品

主要优势:

法律支持:Story Protocol 的智能合约为知识产权提供法律基础。

透明跟踪:所有使用和版税交易都记录在区块链上,以实现完全透明。

高效的争议处理:利用争议系统快速处理和解决知识产权侵权问题。

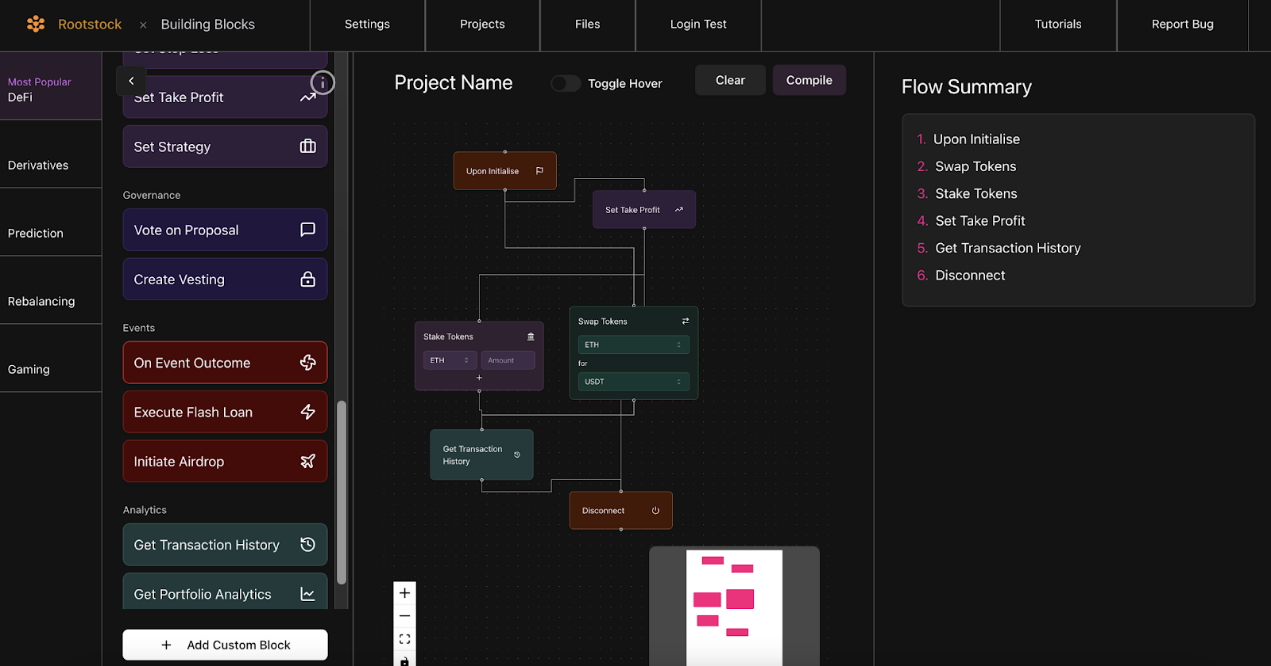

BuildBlocks

BuildBlocks 创建了拖放式(drag-and-drop)智能合约组件,任何人都可以在 Rootstock 上开发、编译和部署经过审计的合约,从而使 Web3 开发变得简单而安全。

BuildBlocks 使用标准的 NextJS、Tailwind 堆栈构建,还使用了可注入钱包、Rootstock 部署和测试网络、用于自动 Solidity 合约编译的 SolC 编译器,以及 SIDAI 的 RAG 管道生成服务。

Uni V4 Backtester

Uni V4 Backtester 是一个机构级的 Uni V4 回测器,可以准确地重播 Uni V3 事件(Swap、Mint、Burn),以查看假定头寸在一段时间内的表现。

Uni V4 Backtester 使用了多种技术来制作这个回测器:Viem(NodeJS)用于获取 Uni V3 池事件;Foundry 用于分叉 Sepolia 测试网并执行回测。

Betsy

Betsy 是 Skale 上的 Web3 投注平台,具有 XMTP 驱动的团体投注消息传递功能。USDC 资金通过智能合约透明处理,AI 帮助确定结果。投注在链上完成和解决,确保安全、无需信任且有吸引力的团体投注。

创建赌注后,小组成员可以在平台内聊天、同意或不同意预测并下注。一旦赌注最终确定,智能合约就会自动转移资金。此外,该平台使用 AI 分析实时体育数据并帮助确定每笔赌注的结果。比赛结束后,AI 会检查预测是否正确,智能合约会相应地分配赢利或损失。