作者:flow

编译:深潮TechFlow

2020 年的夏天,被称为“DeFi 之夏”,是加密货币行业一个令人难以置信的时期。DeFi 第一次不仅仅是一个理论概念,而是一个在实践中有效的概念。在此期间,我们见证了多个 DeFi 原生协议的激增——包括 Uniswap 的去中心化交易所(DEX)、aave 的借贷协议、SkyEcosystem 的算法稳定币,以及其他更多项目。

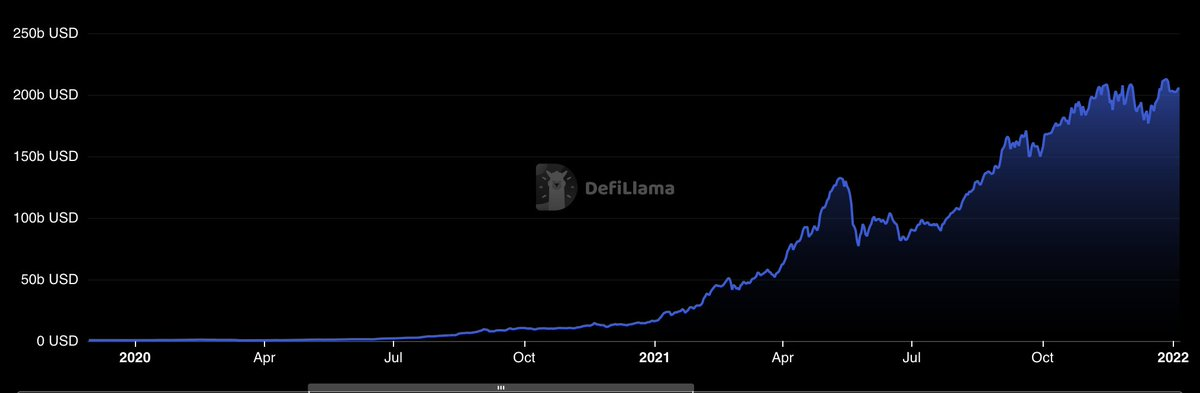

随后,去中心化金融(DeFi)应用中的总锁定价值(TVL)大幅增长。从 2020 年初的约 6 亿美元,到年底 TVL 上升到超过 160 亿美元,并在 2021 年 12 月达到了超过 2100 亿美元的历史新高。这一增长也伴随着 DeFi 领域的强劲牛市。

2020 年至 2021 年底的加密货币 TVL 图表

来源:DeFi Llama

我们可以认为,“DeFi 之夏”的主要催化剂有两个方面:

-

DeFi 协议的突破性进展,使其具备了扩展的能力,并提供了明确的使用案例。

-

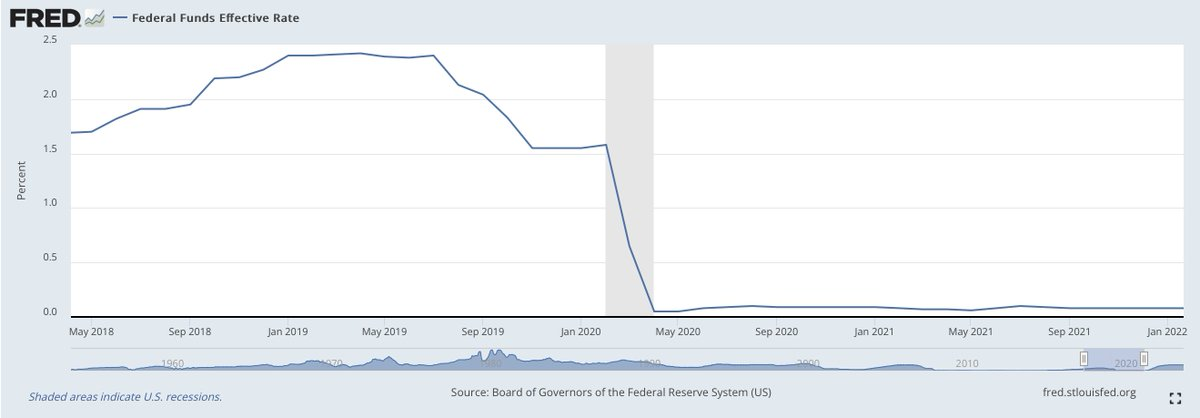

美联储货币政策宽松周期的开始,在此期间,利率被大幅降低以刺激经济。这使得系统中的流动性充裕,并激励人们寻找更具异国情调的收益机会,因为传统的无风险利率非常低。这为 DeFi 的蓬勃发展创造了完美的条件。

2018 年 5 月至 2022 年 1 月的美联储基金利率图表

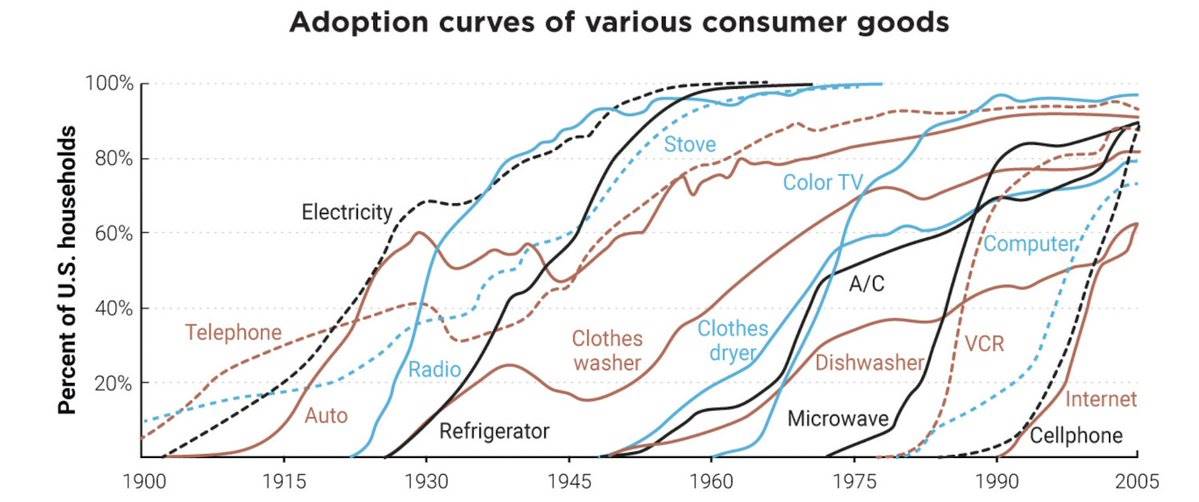

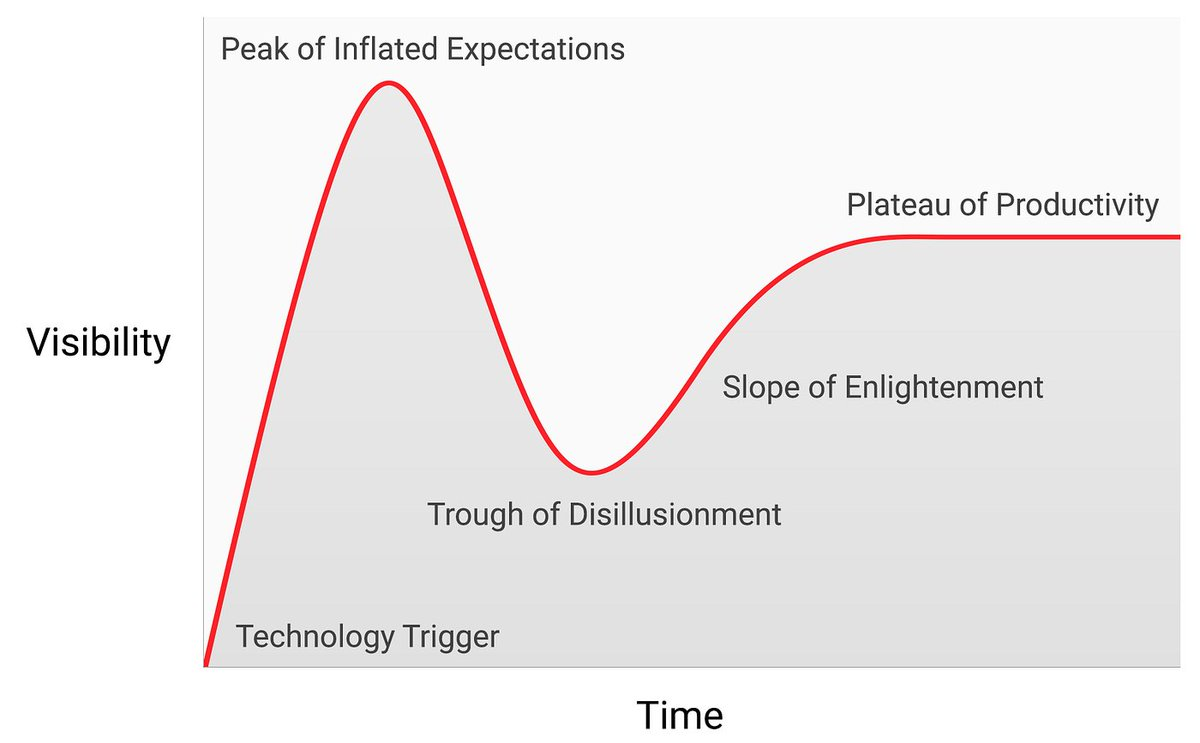

然而,与许多新兴的颠覆性技术一样,DeFi 的采用呈现出一个常见的 S 曲线趋势,通常称为 Gartner 热度周期。

图表展示了各种消费品随时间的采用情况,反映了这一趋势

来源:看涨比特币的案例

总体而言,它的运作方式如下:在“DeFi 之夏”的初期,早期投资者对他们所投资技术的变革性本质有着强烈的信心。对于 DeFi 来说,这种信心源于它能够彻底改变当前金融体系的理念。然而,随着更多人进入市场,热情达到了顶点,购买行为越来越受到投机者的驱动,他们对快速获利的兴趣超过了对基础技术的关注。在这种狂欢的高峰之后,价格下跌,公众对 DeFi 的兴趣减弱,我们面临了一场熊市,随后进入了一个长期的平稳期。

Gartner 热度周期图表

来源:投机采用理论

可以明确地说,这个乏味的平稳阶段并不是 DeFi 的终结,而是朝着大众采纳的真正旅程的开始。在此期间,开发者们继续进行建设,对 DeFi 的坚定信仰者数量也在逐渐增加。这为下一个 Gartner 热度周期的迭代奠定了坚实的基础,这可能会带来更大规模的用户,并且规模可能会更为庞大。

DeFi 复兴

目前来看,DeFi 复兴的前景似乎非常乐观。与上一个 DeFi 之夏的催化因素相似,我们目前有:新一代更加成熟的 DeFi 协议正在开发;健康且持续增长的 DeFi 指标;机构参与者的到来;以及美联储的宽松周期正在进行中。这为 DeFi 的蓬勃发展提供了一个完美的环境。

为了更清晰地了解这一情况,让我们分析这些组成部分:

迈向 DeFi 2.0

多年来,DeFi 协议和应用程序从 2020 年最初的炒作浪潮中经历了显著的演变。许多第一代协议面临的问题和局限性已经得到解决,从而构建了一个更加成熟的生态系统。这就是我们现在所称的 DeFi 2.0 运动的出现。

一些关键的改进包括:

-

更好的用户体验

-

跨链互操作性

-

改进的金融架构

-

改进的可扩展性

-

增强的链上治理

-

改进的安全性

-

适当的风险管理

此外,我们已经看到多个新用例的涌现。DeFi 不再仅仅局限于早期阶段的交易和借贷。像重新质押(restaking)、流动质押(liquid staking)、原生收益(native yield)、新的稳定币解决方案以及现实世界资产 (RWA) 代币化等新趋势,使得生态系统更加生机勃勃。更令人兴奋的是,我们看到新的基础设施仍在不断开发。最近引起我注意的是基于现有借贷基础设施构建的链上信用违约掉期 (CDS) 和固定利率/期限贷款。

健康且不断增长的 DeFi 指标

自 2023 年底以来,DeFi 活动复兴,我们见证了一波新的 DeFi 协议的涌现。

首先,观察加密生态系统中的总锁仓价值 (TVL),我们发现,在经历了长时间的平稳期后,动能开始回升。从 2023 年 10 月的 410 亿美元,TVL 几乎增加了三倍,在 2024 年 6 月达到了 1180 亿美元的局部高点,然后回落至当前约 850 亿美元的水平。虽然这仍低于历史最高点 (ATH),但仍然是一个显著的上升趋势。有很强的理由认为,这可能是 TVL 长期上升趋势的第一波。

图表显示了加密领域 TVL 的演变

来源:DeFi Llama

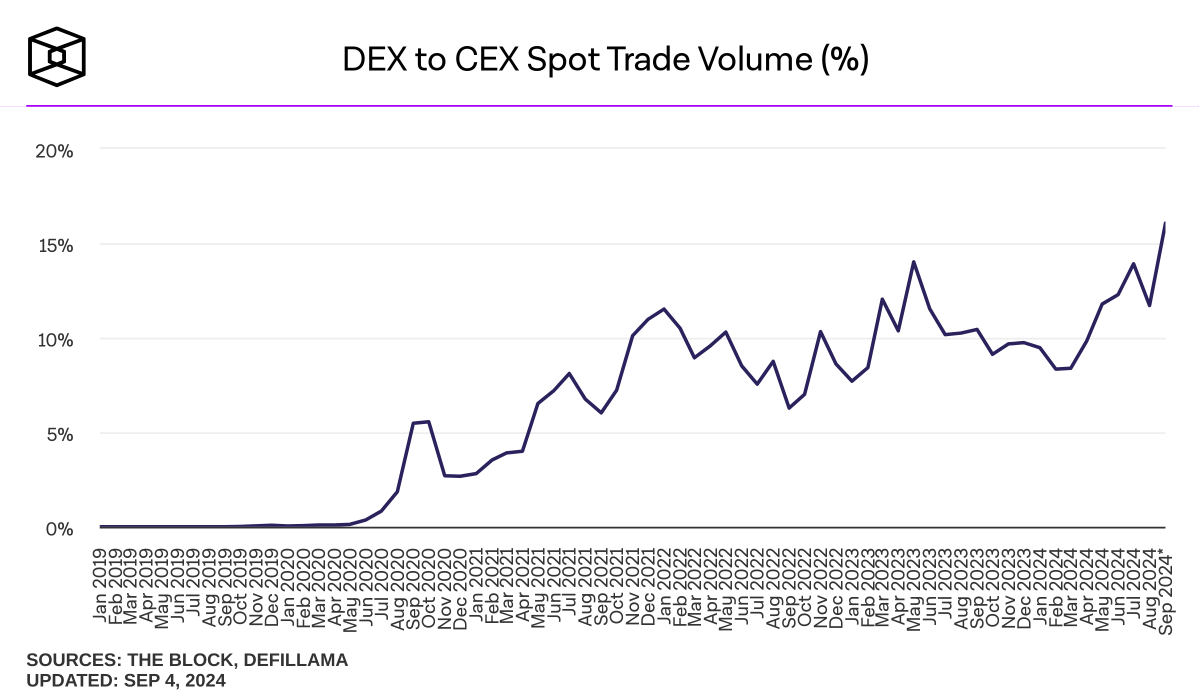

另一个有趣的指标是去中心化交易所 (DEX) 和中心化交易所 (CEX) 之间的现货交易量,这一指标衡量了这两者之间的相对交易活动。同样,我们注意到一个积极的长期趋势,表明越来越多的交易量正在转移到链上。

图表显示了 DEX 与 CEX 之间的现货交易量

来源:The Block

最后但同样值得注意的是,DeFi 领域在更广泛的加密生态系统中所占据的关注度在最近几个月有所上升。在一个竞争激烈、每个人都在争夺注意力的市场中,DeFi 开始再次引起关注。

DeFi 的关注度持续上升。

如果特朗普获胜,很难想象哪个行业会受益更多。

机构参与者的到来

在“DeFi 之夏”期间,第一波 DeFi 参与者主要是试图掌握这一新技术的个人,而新一波 DeFi 协议开始吸引一些大型传统金融机构进入 DeFi 领域。

今年 3 月,全球最大的资产管理公司贝莱德在以太坊区块链上推出了其首个代币化基金——贝莱德 USD 机构数字流动性基金(BUIDL 基金),允许投资者直接在链上赚取美国国债收益。这是贝莱德的首个 DeFi 计划,取得了明显的成功,基金的管理资产已超过 5 亿美元。

贝莱德代币化实物资产基金 $BUIDL 自推出以来在四个月内超过了 5 亿美元的里程碑,因为代币化国库市场仍在不断扩大。

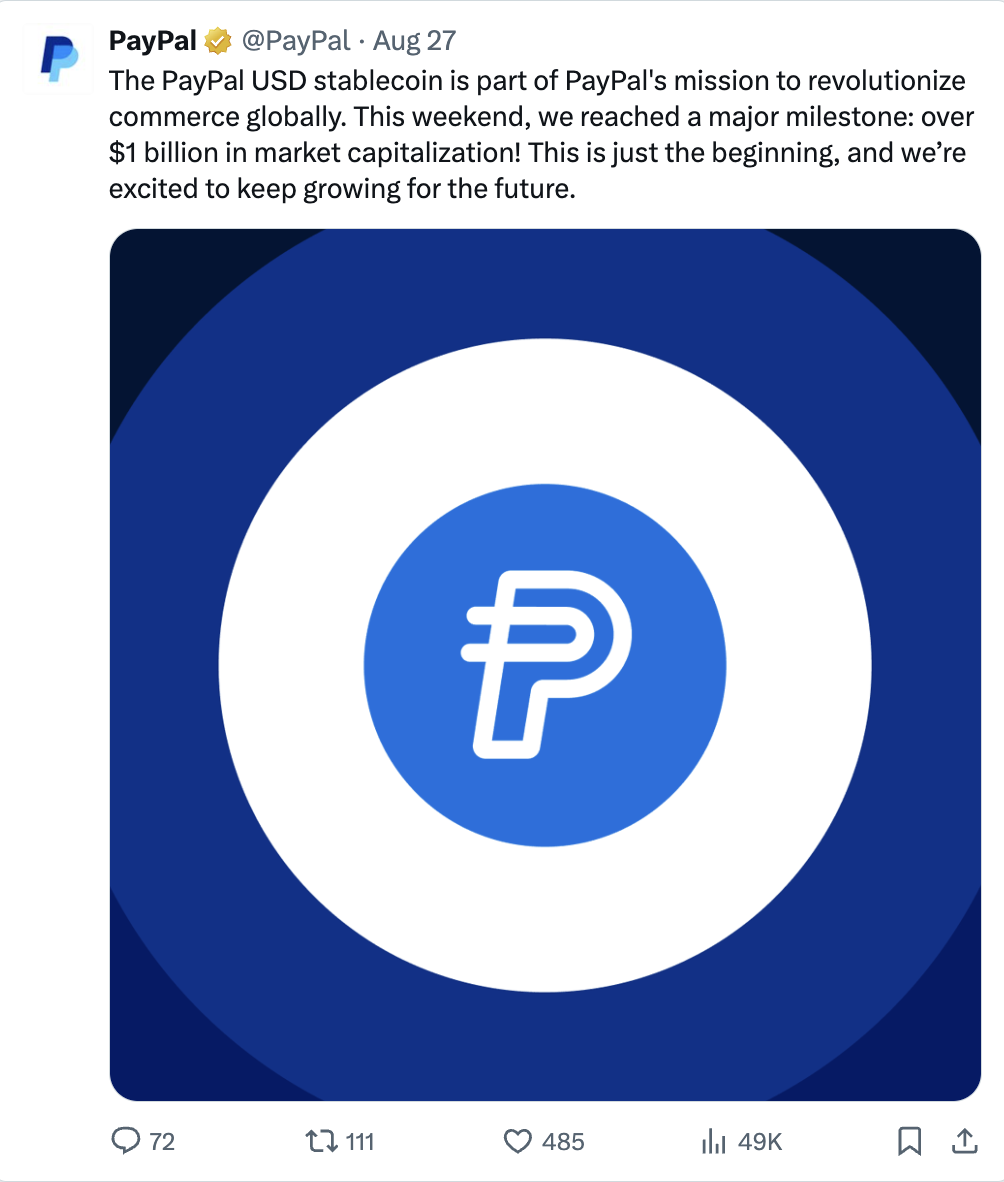

机构兴趣增长的另一个显著例子是 PayPal 的 PYUSD 稳定币,该稳定币最近达到了一个重要里程碑:在推出仅一年后,其市值就超过了 10 亿美元。

PayPal USD 稳定币是 PayPal 全球革新商业使命的一部分。在这个周末,我们达成了一个重要的里程碑:市值超过了 10 亿美元!这仅仅是个开始,我们对未来的持续增长充满期待。

这些例子表明,更广泛的金融行业终于开始认可基于去中心化区块链技术构建金融系统的价值主张。引用 PayPal 的首席技术官的话:“如果它能降低我的整体成本,同时又能带来好处,那为什么不去拥抱它呢?”随着越来越多的机构参与者开始尝试这种技术,我们可以认为,这将成为推动 DeFi 领域发展的强大催化剂。

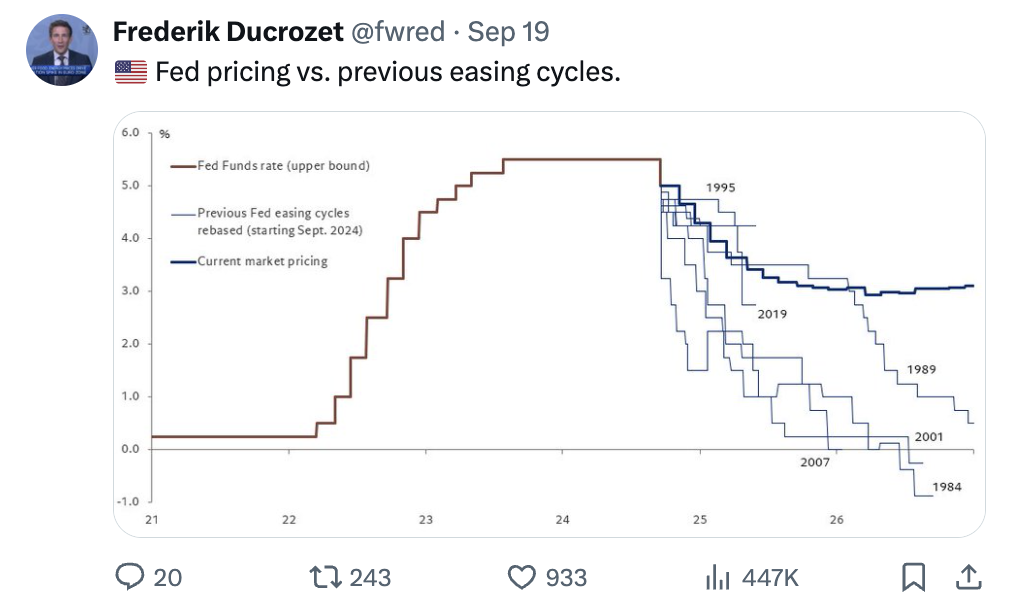

美联储正在进行宽松周期

除了之前提到的几点,目前美国货币政策的走向也是 DeFi 的另一个潜在催化剂。实际上,我们刚刚跨越了经济中的一个重要转折点。这是自美联储开始后疫情时期抗击通胀以来,首次在最近的 9 月 FOMC 会议上进行 50 个基点的降息,这强烈表明新的宽松周期正在进行中。这一点通过美联储基金利率的预期走势得到了进一步证明。

Frederik Ducrozet:美联储定价与之前的宽松周期。

这一新货币宽松周期的开始为 DeFi 牛市论点提供了两个关键支持:

-

这一宽松周期必将增加系统内的流动性。流动性是金融市场的一个关键要素,过剩的流动性是有利的,因为这意味着有更多资金可以进入市场。因此,DeFi 及更广泛的加密市场应该会从中获益。

-

美联储基金利率的下降将相对提高 DeFi 收益的吸引力。简单来说,随着传统无风险利率的降低,投资者将开始寻求其他收益机会。这可能会导致市场向 DeFi 的轮动,因为 DeFi 提供了一系列在稳定币和其他更具异域风情的策略中具有吸引力的收益——这些收益相比于几年前要更加安全和可靠。

历史会否重演?

总的来说,似乎有多个因素汇聚在一起,预示着 DeFi 的复兴。

一方面,我们正在见证几个新的 DeFi 基础设施的出现,这些基础设施比几年前更加安全、可扩展和成熟。DeFi 已经证明了其韧性,并确立了自己作为加密货币中少数几个拥有成熟用例和真实应用的领域之一。

另一方面,当前的货币环境也在推动 DeFi 的复兴。这与上一个 DeFi 之夏的情况类似,而当前的 DeFi 指标则暗示我们可能正处于一个更大上升趋势的初期。

历史虽然不会完全重演,但常常会有相似的情形出现。