近日,WEEX 交易所的平台币 WEEX Token (WXT) 正式上线。

时逢加密市场持续调整,不少山寨币已跌回熊市,市场如惊弓之鸟,WXT 在此时上线似乎有些生不逢时。但 WXT 上线后只经过短暂的洗盘便日拱一卒地稳步攀升,截至目前累计上涨 20% ,在当前一片恐慌的市场氛围中彰显平台币的蓝筹底色和价值支撑。

WXT 币的价值支撑是什么?适合长期持有吗?有哪些方式可以获得 WXT 空投?本文将结合白皮书对 WXT 的代币经济模型、持有者权益、通缩机制等进行详细介绍。

价值支撑:WXT 成为「金铲子」

发行 WEEX Token (WXT) 的初衷是为了践行 WEEX 「用户至上,合作共赢」的承诺,将平台发展红利与用户和合作伙伴共享,同时借助 WXT 绑定更多忠实用户和合作伙伴,实现 WEEX 平台持续长远发展。

为此,WXT 被赋予一篮子持币福利,包括:

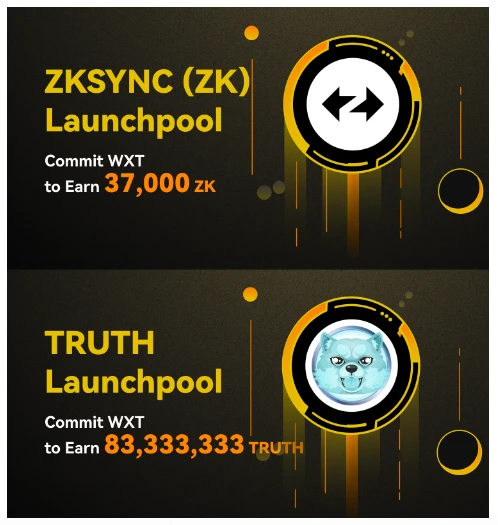

Launchpool:用户质押 WXT 即可参与 WEEX Launchpool 项目挖矿,免费获得热门代币空投。截至目前,WEEX 已举办 2 期 Launchpool 活动,分别送出 83, 333, 333 TRUTH 和 37, 000 ZK。

Launchpad:持有 WXT 的用户可优先参与 WEEX Launchpad 新币发行。根据 WEEX 2024 年 Launchpool & Launchpad 计划,持有 WXT 的年化收益率高达 64% 。

费率折扣:使用 WXT 抵扣 WEEX 现货交易手续费,可享 30% 费率折扣;持有一定数量 的 WXT,还可享受专属的梯度合约手续费折扣(当前为 20% )。

邀请奖励升级:持有 100, 000 WXT 超过 30 天,邀请奖励增加 15% 。

VIP 尊享:持仓超过 1, 000, 000 WXT 的用户,专享大额充提币加速服务。

阳光普照:持有 WXT 的用户可参与瓜分热门代币空投,包括各类项目 token、USDT 体验金等。

持币生息:WXT 持有者未来可在特定理财产品上赚取额外的利息奖励。

投票上币:持有一定数量的 WXT 享受上币特权。

这一系列持币权益,使 WXT 成为获取空投、手续费减免、奖励升级的「金铲子」,将为持有者持续带来财富收益,浇筑 WXT 的价值基石。

生态基石: 55% WXT 激励社区

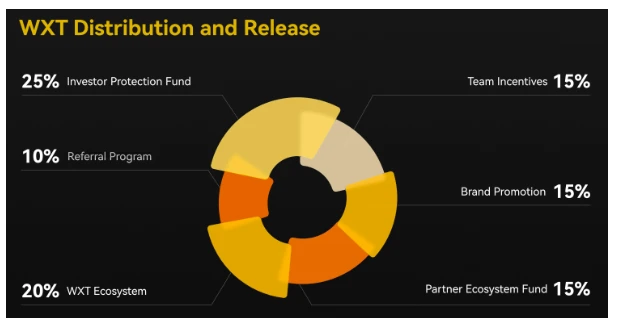

WXT 被设定为全球生态激励通证,用于激励 WEEX 交易所社区的合作伙伴、贡献者、先驱和活跃成员。从代币经济模型来看, 55% 的代币将分配给活跃用户、合作伙伴及团队贡献者,并设置了长达 10 年的锁定期,以确保 WEEX 长期战略和阶段性目标有序实现。

活动拉新:10 亿 WXT(10% ),每年释放 1% ,已释放 0.25% 。用于拉新奖励和激励新用户,确保 WEEX 用户和交易量增长速度。

品牌推广:15 亿 WXT(15% ),每年释放 1.5% , 2024 年 12 月开始释放。用于 WEEX 品牌建设和媒体伙伴联盟计划,旨在吸引行业媒体和 优质 KOL 合作,提升 WEEX 及 WXT 的品牌知名度和透明度。

合作伙伴生态基金:15 亿 WXT(15% ),每年释放 1.5% , 2024 年 8 月开始释放。用于回馈 WEEX 交易所合作伙伴,激励长期合作,共享收益。

团队激励:15 亿 WXT(15% ),每年释放 1.5% , 2025 年 4 月开始释放。用于吸引和留存 Web3 顶尖人才,激励团队成员努力实现关键绩效目标和 WEEX 长期发展战略。

其余 45% 包括 WXT 生态基金 ( 20% ,年释放 2% ) 和 WEEX 投资者保护基金 ( 25% ),前者用于支持 Web3 初创项目,与生态伙伴共同成长;后者用于增厚 WEEX 投资者保护基金,保障用户资产安全,让用户交易安心无忧。

从分配机制来看, 50% 以上的 WXT 都将分配给社区和 WEEX 交易所生态伙伴。未来随着 WEEX 用户规模和生态的不断增长,WXT 的持币将不断分散和去中心化、民主化。

从释放周期来看, 75% 的 WXT 锁仓期长达 10 年,超过了至少两轮加密牛熊周期;其余 25% (投资者保护基⾦)虽未设置锁定期,但这部分资金显然也属于长期持有,仅在出现异常情况时用于补偿用户资金的意外损失。

这意味着,WXT 短期内不存在释放压力,有利于维持币价稳定和实现市值管理目标。这样的机制设计也体现了 WEEX 谋求交易平台和生态社区长期繁荣的初衷,坚定团队的「长期主义」信念。

极致通缩: 90% WXT 回购销毁

WXT 最大供应量 100 亿枚,这个数字看着很高,但白皮书承诺,WEEX 将定期拿出平台利润的一部分从二级市场回购 WXT 并永久销毁,直至总供应量最终减少至 10 亿枚,以增强其稀缺性,保证持币者的长期价值回报。回购详情和销毁记录将在区块链上永久公开,确保透明度和市场信任。这将对 WXT 的长期价值产生积极影响,并增强其生态系统。

作为全球 Top 10 衍生品交易所,WEEX 拥有超过 200 万注册用户,市场覆盖全球 30 多个国家和地区,日均交易量超 10 亿美元,平台早在 2022 年「加密寒冬」就开始实现稳定盈利,并保持月均交易量 100% 的高增长。

顶级实力和高速增长为 WXT 的回购销毁提供了坚实保障,而 90% 的通缩目标则意味着 WXT 将在市场合理估值的基础上升值 10 倍,无疑为其币价保持长期坚挺注入了强大信念。

自 2018 年以来,WEEX 团队怀揣「让区块链技术普惠大众」的热忱信念,穿越多轮牛熊,深耕加密货币交易赛道,在加密资产的全周期运营中积累了深厚的市场经验。凭借安全易用、专业合规的服务体验,以及交易深度、一键跟单等产品优势,WEEX 快速成长为一个开放、透明、公正、可信赖的黑马交易平台。

如今,WXT 上线后绑定越来越多的生态合作伙伴,将为 WEEX 的增长飞轮增添新的驱动引擎,实现交易所和平台币相互赋能的协同机制。比如,WEEX 季度总交易量排名前 50 的用户,可以以 20% 的折扣限额认购 WXT,既为 WXT 带来大量优质买盘,又通过激励提升了 WEEX 的整体交易量和用户活跃度。

WXT 当前正在开展合伙人 Presale 和用户「剪彩活动」,合伙人邀请新用户注册赚取积分,根据积分占比解锁 WXT 7 折认购额度;新用户完成注册、KYC、充值、合约交易等任务即可领取 WXT 空投,单人最高可获得 198, 700 WXT。

展望未来,WEEX 将继续以提供安全、隐私保护和用户友好的交易服务为使命,借助平台币 WXT,构建一个涵盖多元化应用的区块链金融生态系统,推动加密货币行业的创新与发展,并与百万用户和合作伙伴共创共享 Web3 发展红利。

WEEX 官网:www.weex.com

WTX 专区:www.weex.com/wxt

WEEX 华语社区:https://t.me/weex_group

WEEX 官方 X:https://twitter.com/WEEX_Official