原文作者:Lisa,LD Capital

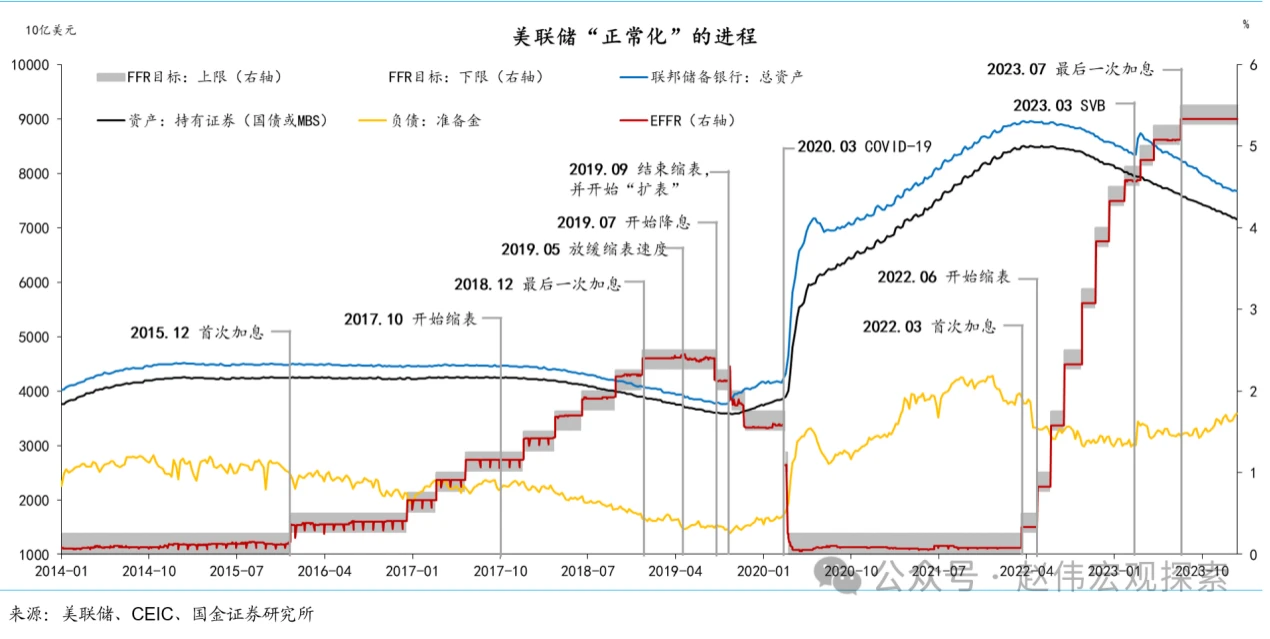

几乎所有的资产价格都要受到美联储货币和财政政策的影响,BTC 自然也不例外,身处 crypto 市场需要时刻关心美国经济的各项数据、联储官员讲话的态度、货币政策走向等。随着 BTC 现货 ETF 的通过,美元潮汐对 crypto 市场的影响将愈加显现。本文将主要围绕下图回顾在不同阶段 BTC 价格的走势。

美联储最后一次加息至开始降息

时间: 2018/12 至 2019/7

BTC 价格表现:先横后涨,约 3500 上涨至 12000 美元

主升开始时间: 2019/4 (与缩表减缓 2019/5 时间相近),可以认为市场提前 3 个月交易降息预期。

该历史时期对应了当前市场所处阶段,目前距离美联储最后一次加息时间(2023/7)已经过去约 6 个月,与过去类似的,BTC 价格也在 2023 年 10 月份(加息停止后的 3 个月)迎来了一段主升行情。近半年 BTC 价格较大程度收到了 ETF 预期的影响,但从时间和形态上依旧巧合地符合了过去一次周期的规律。

美联储开始降息至疫情扰动前

时间: 2019/7 至 2020/3

BTC 价格表现:先跌后涨

开始降息后价格下行,约从 10000 跌至 12 月的 7000 ,跌幅 30% (期间 2019/9 结束缩表并未产生明显正面影响 ), 2019 年 12 月至 2020 年 2 月反弹至 10000 。

该阶段是市场 24 年将会进入的阶段,历史上一次降息落地和缩表结束后 BTC 的表现整体为先跌后涨。

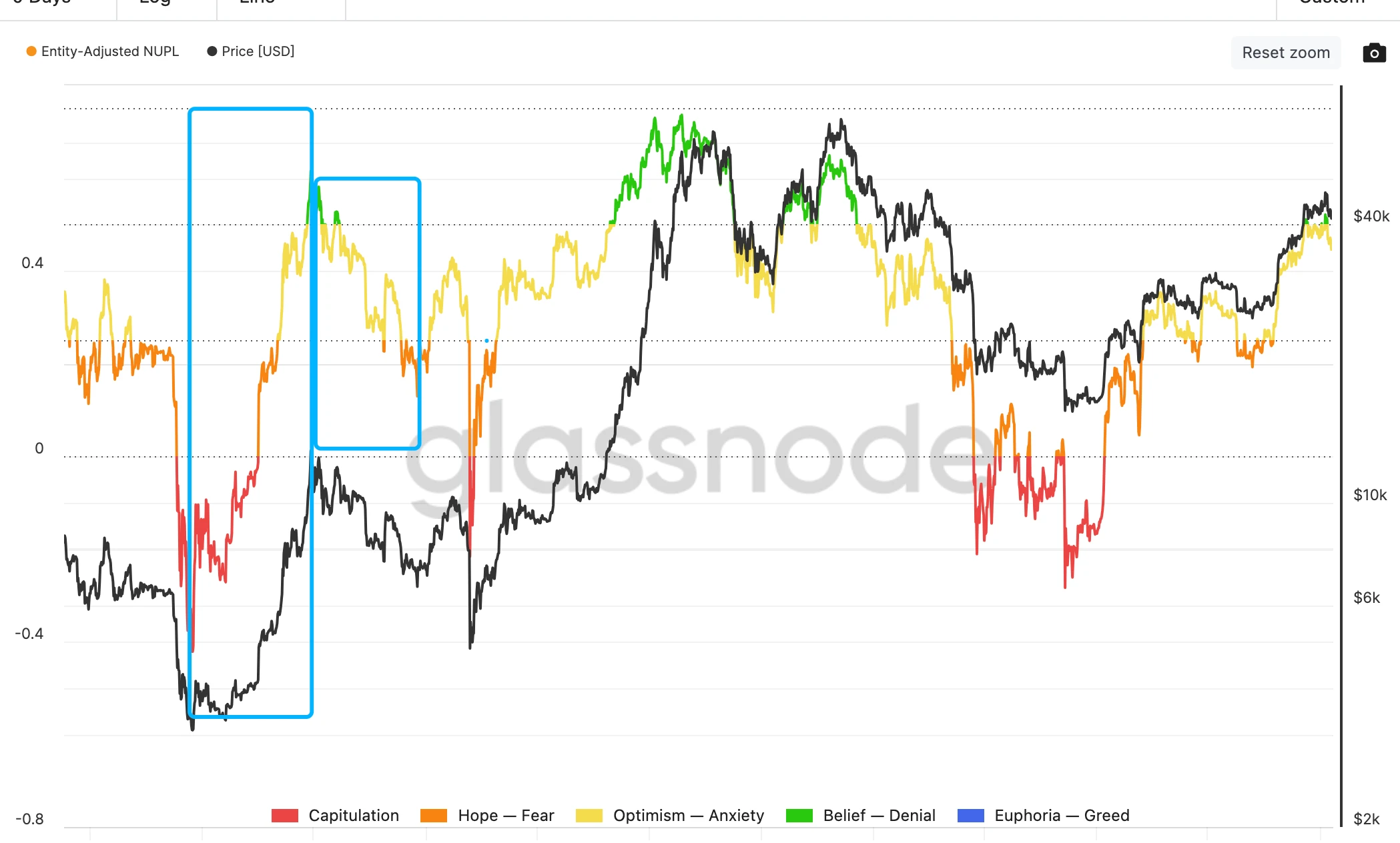

以上两个阶段的配合 NUPL 的角度可以很好地判断阶段性的高低位置。

疫情影响下的宽松阶段

后 2020 年 3 月份,受 covid 疫情影响,美联储迅速降息并开启大规模 QE,叠加 2020/5 的减半,市场短暂下挫后迎来主升浪,BTC 大致从 5000 上涨到 65000 。

BTC 市场的顶出现在 2021/11 ,距离宽松结束的时间(2022/3 首次加息) 4 个月,可以认为市场提前 4 个月交易加息预期,与此前提前交易降息的时间差较为接近。

在没有黑天鹅事件的情况下,本轮牛市恐难再现这样激进的货币政策和上涨速率或幅度,但方向依旧。

重新开始紧缩,美联储开始加息至最后一次加息

时间: 2022/3 开始加息至 2023/7 最后一次加息;2022/6 开始缩表至目前

BTC 价格表现:约从 46000 最低下跌至 16000 ,下跌约 9 个月后在 2023 年初开始反弹

2023 年初开始 BTC 和纳斯达克指数同步上涨的这段行情可能与市场预期美债利率阶段性见顶和联储加息幅度放缓有关。

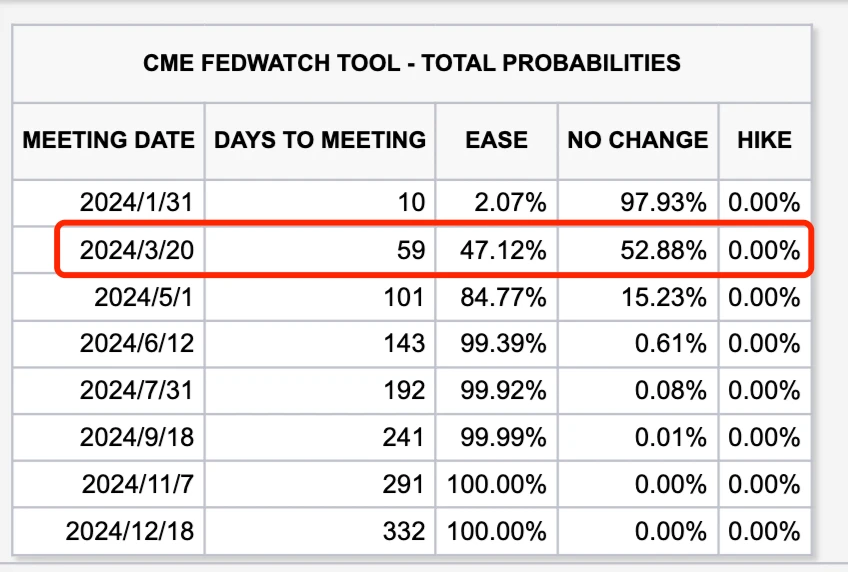

整体看起来降息对 BTC 市场的影响相对缩表更大,那么今年何时开始降息?

美联储主席鲍威尔在 12 月 FOMC 会议后发出“鸽派”信号,导致美联储降息预期升温。而美国最新的数据较为强劲,美国 12 月 CPI 同比增长 3.4% (前值 3.1% ),核心 CPI 同比增长 3.9% (前值 4.0% ),均高于预期,同时劳动力市场仍然紧俏,目前市场预计 3 月不降息概率为 52.88% 。

对于 24 年的预计降息不是在 3 月份就是在 5 月份,刻舟求剑地看,市场可能届时有一波回调。当然现货 ETF 是对市场较大的扰动,利好落地和 GBTC 的抛压是近期影响 BTC 价格的主导因素。同时 BTC 减半的时间也比前一次周期提前不少(前一次的减半发生在开始降息 10 个月后),本次减半恰好夹在市场预期的两个降息起始点中间。虽然减半利好后的上涨通常滞后于其实际发生的日期,但从时间上看仍然能够部分熨平降息后可能的下跌。