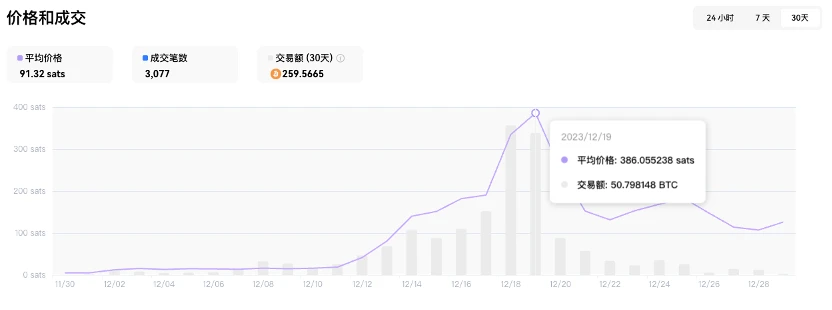

原创 | Odaily星球日报

作者 | jk

从上个月的铭文热潮开始,各大交易所开始不断上线新的铭文,整个铭文市场的交易热度空前高涨。在这种热度当中,涌现了两种完全不同的交易理念:一种是不愿意错过任何一种新的铭文,在一级市场用各种方式手搓或上脚本,之后在场外或者交易所上币之后卖出;另一种是不愿意手打铭文,而倾向在上币之后从二级市场购买,看能否吃到二级市场上币之后的增长红利。

需要注意的是,铭文交易在各个交易所的价格走势和实时价格并不完全相同,且新一代铭文的 meme 化也让涨跌变得更加难以预测。那么,交易所上币到底对于铭文和 memecoin 有什么影响呢?是新一轮涨势的信号,还是大量抛压的前奏?讲得更面向中小投资者一点,就是除了在一级市场打新以外,上币之后是否仍然有上涨空间?

我们梳理了上一轮中几个大热的铭文和资产来具体分析上币对于它们价格趋势的影响。

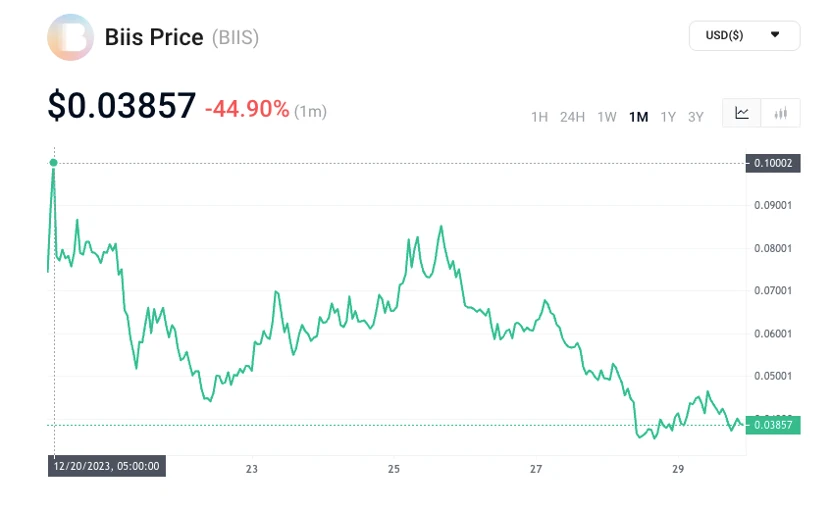

Biis

Biis 价格走势,来源:KuCoin

Biis 价格走势,来源:OKX Ordinals

根据 Coinmarketcap 的数据,biis 目前的 24 小时交易量并不太高;排名第一的是 KuCoin,交易量约为 43 万美元左右,紧随其后的是 XT.com 和 OKX。随着这个顺序,交易量最高的交易所上币似乎代表了 biis 的最高点。

OKX 的上币日期较早,KuCoin 上币日期是 12 月 20 日(交易量紧随其后的 XT.com 则是在 21 日上币),价格最高点出现在上币约 2 小时后,此后一路下跌,在 25 日出现一定涨幅,随后一路下跌至如今的 0.038 美元左右。

针对 Biis,能够从二级市场吃到红利的空间极小,交易量最大的交易所上币之后就代表着抛压。然而,如果能在更早期从 OKX 中买到份额,之后仍有上涨空间。

.com

.com 行情,来源:MEXC

从 BRC 20.com 的 24 小时交易量这一数据来看,MEXC 的最高,HTX 其次,紧随其后的是 XT.com 和 Bitget。MEXC 也是上币最早的交易所,在 12 月 14 日就上线了.com,跟完了从上涨到下跌的一整个周期,在 12 月 19 日出现了价格最高点 7.2 美元,现报 3.397 美元。

Bitget 上币的日期是 12 月 19 日,正好是价格出现最高点的当天,XT.com 在 20 日上币。随后便一直是较缓的下跌趋势。HTX 则在 27 日上币,上币之后的走势已经趋向平稳。

可以看到,单就.com 而言,如果能够跟上最早上币的一波行情,尚且有不少的盈利空间;而随着各大交易所跟上节奏之后,价格就已经开始从高点下滑了。

BNSX

BNSX 价格走势,来源:BitMart

BNSX 的交易量排名中,Gate.io 排名第一,BitMart 和 AscendEX 分别排名第二第三。这三家几乎同时上币,Gate 与 BitMart 在 12 月 18 日上币,AscendEX 在当天晚些时候上币。因而,其后的走势也几乎相同:上币之后价格便一路高涨,到北京时间 19 日达到最高点约 2.49 美元,随后一路下跌。

就 BNSX 而言,几大交易量大的交易所上币之后,盈利空间并不是很大,若是当天能够入场则还有一定的盈利空间, 19 号之后则是略有起伏的下跌趋势了。

MMSS

MMSS 价格走势,来源:BitMart

MMSS 价格走势,来源:LBank

对于铭文 MMSS,交易量排名前列的交易所分别为:BitMart,LBank,Bitget 和 Gate.io。这四所的上币顺序为:BitMart 最早,于 12 月 7 日上币,LBank 于 19 日上币,Bitget 则在 20 日上币。Gate 则最晚,在 27 日上币。可以看到,从 BitMart 上币之后有一段较长时间的红利期,币价在 16 日前后达到顶峰,随后回调了一段时间,在 27 日达到了另一个小高峰。

也就是说,如果能在足够早的时间就从先上币的交易所中买到,那么随后其他交易所带来的上币热潮的盈利空间还是比较大的。

Mice

Mice 价格走势,来源:Bitget

选择一个龙头代币来看,上币的影响对于龙头铭文而言还是比较小的。对于 Mice 而言,交易量最高的交易所分别为 Gate、OrangeX、Bitget 和 BitMart,上币顺序分别为 Gate(16 日),Bitget(18 日),BitMart(18 日),OrangeX(18 日)。上币之后出现了三个顶峰,分别在 19 日, 21 日和 25 日。

可以看到,对于龙头铭文而言,共识已经形成,价格走势更偏向于传统的 memecoin,而非只有一波涨跌的项目,因而交易所上币对于价格的意义有限,上币之后仍然有数个套利空间。

对于非龙头代币而言,交易所上币并不能带来特别多的利好。通过以上的例子可以发现,几个交易量最大的交易所上币的热潮时间段通常也就是币价最高点,这两者出现前后可能只有几个小时或者一天。需要有足够长远的战略眼光,在更早上币的交易所中提早布局,或者干脆在一级市场打新;若是关注到该铭文已经比较晚,在大所都上币之后,二级市场购买的红利期较短,之后基本上是平稳波动或者有跌幅。

而对于龙头代币而言,其已经是事实上的 memecoin;涨跌幅的规律更偏向于市场共识和消息面,研究上币本身对于币价的波动已经意义有限。投资者在面对龙头代币或非龙头代币时,应该更加关注市场动态、交易所的影响以及整体的市场共识,有必要深入研究和分析各种因素。同时,投资者也应当意识到,无论是龙头代币还是非龙头代币,市场的不确定性始终存在,因此谨慎评估风险和潜在的回报是至关重要的。