Source: Jinshi Data

On Wall Street, growing fears about artificial intelligence are hammering the stocks of companies that could become its targets of disruption, from small software firms to large wealth management companies, none have been spared.

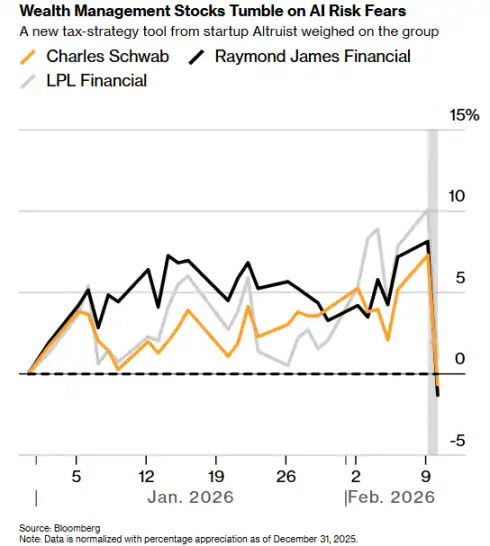

The latest round of selling erupted on Tuesday when a tax strategy tool launched by a little-known startup, Altruist Corp., caused shares of Charles Schwab Corp., Raymond James Financial Inc., and LPL Financial Holdings Inc. to fall by 7% or more.

This marked the steepest decline for some of these stocks since the market crash triggered by the trade war last April. But it is just the latest example of the "sell first, ask questions later" mentality—a mindset that is rapidly taking hold as the hundreds of billions of dollars poured into AI begin to translate into commercial products, sparking anxiety that AI could disrupt entire industries.

"Companies with any potential disruption risk are being sold off indiscriminately," said John Belton, a fund manager at Gabelli Funds.

Over the past few years, advancements in AI technology have been at the forefront of Wall Street, with tech stocks leading the gains. As this rally pushed stock prices to record highs, questions have persisted about whether this is a bubble about to burst or whether it will trigger a productivity boom that reshapes the American corporate landscape.

But since the beginning of last week, a series of AI product launches has triggered a noticeable market shift. Instead of focusing on picking winners, investors are quickly trying to avoid holding any company facing even the slightest risk of being replaced.

"I don't know what's going to happen next," said Will Rhind, CEO of Graniteshares Advisors.

"Last year's story was that we all believed in AI—but we were looking for applications, and as we keep discovering applications that seem increasingly powerful and persuasive, it is now leading to disruption."

For some time, the software industry has been troubled by concerns about AI. Last week, when a new tool from Anthropic PBC triggered sharp declines in stocks across industries such as software, financial services, asset management, and legal services, these worries began to shift more broadly to other sectors.

The same fears hit U.S. insurance broker stocks hard on Monday after the online insurance marketplace Insurify launched a new app using ChatGPT to compare auto insurance rates. On Tuesday, wealth management stocks became the next victim, as the product Hazel launched by Altruist—which helps financial advisors create personalized strategies for clients—dragged these stocks down.

Wealth management stocks plunge on AI risk concerns

Altruist CEO Jason Wenk said he himself was surprised by the scale of the stock market reaction, which wiped tens of billions of dollars from the market value of several investment firms. But he said it sends a strong signal about the competitive threat his company poses.

"People are beginning to realize—the architecture we used to build Hazel, it can replace any job in wealth management," he said in an interview. "Usually these jobs are done by entire teams. And now, AI can effectively do these jobs for just $100 a month."

AI companies like OpenAI and Anthropic have already made solid progress in the field of software engineering with products that help developers simplify and debug code processes, and are now entering other industries.

However, many questions remain about how this technology will be adopted. Take banking, for example, which has periodically faced challenges from electronic services and other technologies, but these have ultimately failed to undermine its dominance.

Gabelli fund manager Belton is one of the skeptics about how Wall Street has shifted from worrying about an AI bubble to fearing its imminent disruption of large parts of the economy.

"There will be winners and losers in every industry," Belton said. But he added: "A rule of thumb is that technological disruption often takes longer to materialize than expected."

This pullback may also reflect widespread anxiety about the sharp rise in stock prices over the past few years, driven by the AI spending boom and an unusually resilient U.S. economy. This has already pushed valuations too high and made investors more sensitive to concerns about a reversal.

"As long as they emit a signal that the market perceives as somewhat negative, the stock will fall 10%, which would never happen in a market that hasn't reached current trading levels," said Graniteshares' Rhind.

For Ross Gerber, CEO of Gerber Kawasaki, the anxiety about AI losers that has been hitting parts of the market over the past week is premature. He said it is still too early to say exactly what the impact will be.

"We can try to extrapolate how AI will change the world in five years, but we just don't know," he said. "The market is trying to judge this while we are still at the beginning of this infancy."