Author:Social Graph Ventures

Compiled by: Jiahuan, ChainCatcher

In the past sixty days, the U.S. capital market structure has undergone more changes than in the past decade. The SEC has outlined a blueprint for tokenized securities. Nasdaq has been approved for token settlement trading. The DTC has received a no-action letter. The New York Stock Exchange announced a partnership with Securitize to launch a tokenization platform.

@fundrise's closed-end fund VCX, which holds @AnthropicAI, @OpenAI, and @SpaceX, saw its premium soar to over 1900% of its Net Asset Value (NAV). Retail investors paid 26 times the actual value of the underlying assets to gain exposure.

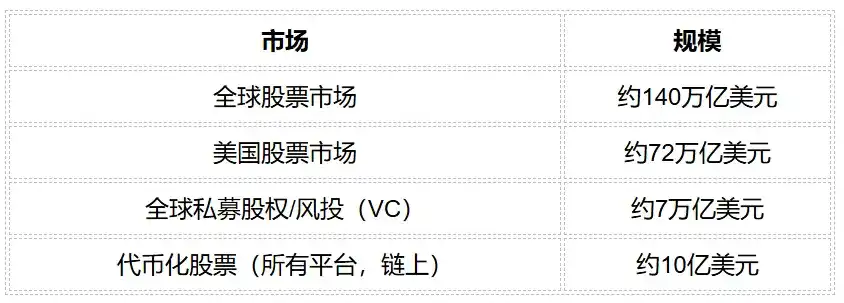

This is not rational pricing; it's a failure of the market structure. The global stock market is worth approximately $140 trillion. And tokenized stocks today? About $1 billion. The penetration rate is only 0.0007%.

How Stocks Are Tokenized: Four Models, Participants, and User Pathways

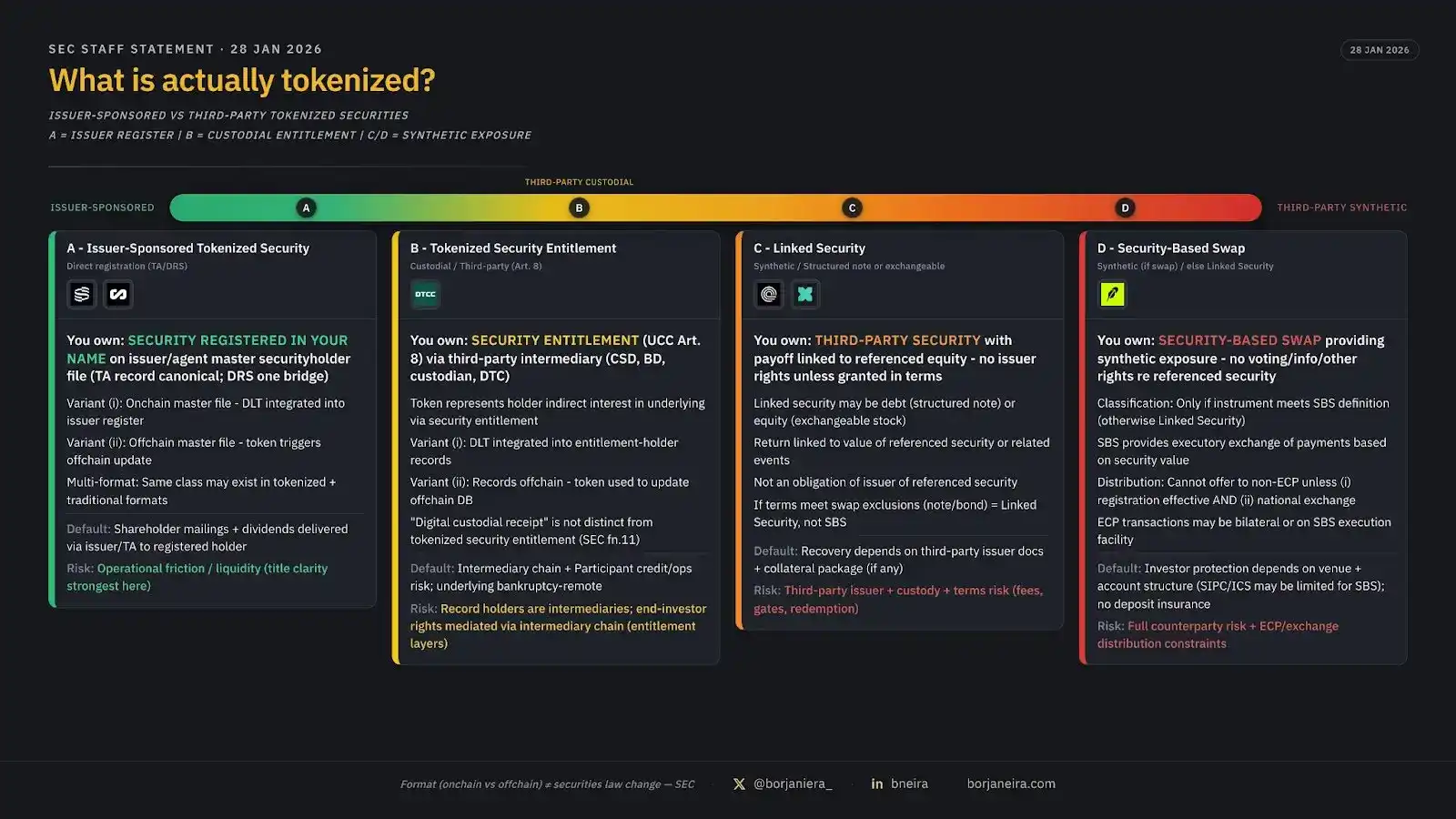

The SEC's statement in January 2026 not only reiterated that "tokenized securities are still securities" but also established a precise classification of how tokenization actually works. Researcher Borja Neira (@borjaneira_) created one of the clearest visualizations of this framework, showing the evolution from issuer-sponsored to third-party synthetic models.

Model A: Issuer-Sponsored Tokenized Securities (Direct Registration)

How it works: The company itself integrates blockchain into its primary security holder register. When tokens are transferred on-chain, ownership on the official register is updated synchronously. You own the security registered in your name, not a claim, not an equity certificate, but real stock.

Who's doing this: Galaxy Digital is the first publicly traded company to tokenize its SEC-registered equity. Through a partnership with the Opening Bell platform (acting as an SEC-registered transfer agent), GLXY shareholders can now tokenize their shares on Solana, store them in their own crypto wallets, and even use them as collateral in DeFi protocols like Kamino.

Pain point: Model A requires the issuer to opt-in actively. Galaxy chose to do this for its own shares, but Apple, Tesla, and Nvidia have not. This is the fundamental limitation: Model A only works when the company itself decides to participate. You cannot tokenize someone else's stock in this model.

User pathway: You need to be a KYC-verified investor on the Superstate platform. You verify your identity, connect your wallet, and can then tokenize GLXY shares you already hold (or acquire). You can transfer them between whitelisted wallets and use them in permitted DeFi protocols.

Omnibus Account

Before explaining Models B, C, and D, it's necessary to understand the omnibus account, as it is the core architecture underlying most tokenized stock platforms today.

What is an Omnibus Account? Simply put, it's an account where assets from multiple clients are pooled together. The broker or intermediary holds this commingled asset on behalf of all clients, presenting it externally (and to the custodian) as one large pool, while internally tracking each client's individual share.

Why this is important for tokenization: When platforms like @OndoFinance, @DinariGlobal, or @xStocksFi tokenize stocks, they typically purchase the underlying stocks, hold them in an omnibus account with a broker-dealer or custodian, and then issue blockchain tokens representing each user's proportional, indirect claim on that pool.

You hold the token, the platform holds the stock; you own an indirect claim, not direct ownership.

Model B: Tokenized Security Entitlements (Custody / Third-Party)

How it works: A regulated third party (DTCC, broker-dealer, custodian) holds the actual shares and issues blockchain tokens representing security entitlements (what the SEC calls "digital custody receipts"). This token represents your indirect interest in the underlying security through a chain of intermediaries.

There are two variants:

- Variant (i): The blockchain itself is the record of ownership, directly integrated into the entitlement holder's ledger.

- Variant (ii): The record is kept in a traditional database off-chain, and the token is used to update that database.

Who's doing this: This is the direction institutional infrastructure is moving. Nasdaq (approved for token settlement trading, expected first launch Q3 2026), NYSE (partnering with Securitize to build a platform), and DTC (received a no-action letter in December 2025) are all building Model B systems.

Your broker holds your stock as usual, but the settlement layer moves to the blockchain. The ownership structure remains the same, settlement is faster.

User pathway: For institutional-grade Model B, the experience will ultimately be identical to buying stock at Schwab or Fidelity; you won't even know it's settled on a blockchain.

For retail, it's not live yet. When Nasdaq launches token-settled trading in Q3 2026, it will be a seamless experience for existing brokerage clients.

Model C: Pegged Securities (Omnibus Model / Structured Notes)

How it works: A third party issues a financial instrument, typically a structured note, debt instrument, or contractual claim, whose value is pegged to a reference stock. You don't own the stock; you own the third party's promise to pay you based on the stock's performance. No voting rights, no direct claim on the underlying asset.

Most tokenized stock platforms operating today fall into this category. They buy stocks, hold them in an omnibus pool, and issue tokens representing your claim on that pool.

Who's doing this:

-

Ondo Global Markets (@OndoFinance) The dominant player by market cap (over $650M total market cap across Ethereum, BSC, and Solana). Offers over 200 tokenized US stocks and ETFs, including Walmart, Tesla, Visa, UnitedHealth, etc.

-

User pathway: KYC required, open to non-US users, tokens are ERC-20 tokens tradable on DEXs and usable in some DeFi protocols. Ondo holds the underlying assets in an omnibus structure through licensed partners.

-

xStocks (@xStocksFi) The second-largest platform, with a $205M market cap, operated by infrastructure linked to Kraken. Over 100 tokenized assets, has processed over $25 billion in cumulative trading volume, capturing 95-99% of all tokenized stock trading activity on Solana.

-

User pathway: KYC required, use a Solana wallet, buy/sell on Jupiter DEX.

-

Dinari (@DinariGlobal) The first broker-dealer registered specifically for tokenized stocks. Over 200 dShares assets. Partners with Flow Traders for institutional liquidity. Built on Avalanche.

-

User pathway: KYC, connect wallet, buy dShares tokens, trade 24/7.

-

Backed Finance (@BackedFinance) Focuses on the EU, regulated in Switzerland. Tokenizes stocks (bTSLA, bNVDA, bGOOGL) and ETFs into ERC-20 tokens on Ethereum. Targets institutions/qualified investors.

-

Robinhood EU (@RobinhoodApp) Offers about 500 tokenized US stocks on Arbitrum. EU only. On-chain market cap $11.6M. Important note: These are explicitly derivative contracts, not equity. No voting rights.

-

User pathway: Use the Robinhood app in Europe, tokens appear in your crypto wallet.

The risks in Model C are real: if the platform fails, you are a creditor, not an owner. Your claim is against the tokenization issuer's omnibus pool.

Most of these platforms do not have SIPC (Securities Investor Protection Corporation) insurance. The SEC's statement is also clear: this introduces significant counterparty risk that blockchain was supposed to eliminate.

Model D: Security-Based Swap Contracts (Purely Synthetic)

How it works: A swap that provides purely synthetic exposure to a reference security. (Simply put, you and the counterparty agree: you receive the price gains/losses of this stock, the counterparty receives a fixed fee you pay; you swap cash flows, but neither party actually holds the stock.)

No ownership. No voting rights. No information rights. No claim of any kind on the underlying asset. You own a bet on the price.

If the instrument qualifies as a swap under SEC definitions, it can only be offered to eligible contract participants and must trade on a national securities exchange.

Who's doing this: Mainly offshore platforms and crypto-native derivatives protocols. Ventuals sits here, offering perpetual contracts built on @HyperliquidX tracking private company valuations.

Ventuals user pathway: No KYC, no accreditation. Log in with email or social account, a wallet is auto-generated, deposit stablecoins, trade up to 10x leveraged positions on valuations of OpenAI, SpaceX, xAI.

Price discovery is done via an "optimistic oracle" (An optimistic oracle is a mechanism that assumes submitted data is correct unless someone posts a bond to challenge it during a dispute period.). Anyone can propose a valuation by staking collateral. Cumulative trading volume is $200M, 5,342 unique traders.

Key warning about Ventuals, Funding Rate: Like all perpetual contracts, Ventuals charges a funding rate to peg the contract price to the reference valuation. When long demand is overwhelmingly dominant (as it is for companies like OpenAI and SpaceX), longs must continuously pay shorts.

At a typical rate of 0.05% per 8-hour interval, holding a $10,000 long position costs about $15 per day, or $450 per month, which is 4.5% of your position, annualized at ~54%.

Holding a long-term bullish position on a private company through Ventuals would see all returns silently eroded by the funding rate alone. It is a trading tool, not an investment vehicle.

User Pathway: How Does an Average Person Actually Buy Tokenized Stocks?

This is the most important question, and the answers vary widely across platforms.

The most objective assessment: For most retail users today, the entry point is Model C. You do KYC on a platform like Ondo or Dinari, deposit stablecoins, and exchange them for tokenized stock tokens.

It works, it's fast, but you own an indirect claim on an omnibus pool, not actual shares, and DeFi composability is developing. If you are a US citizen, most platforms are not open to you.

A Different Path: Berry

A platform worth watching is Berry (@berryinvesting), a company in our portfolio. Today Berry operates under Model C but is moving towards a model with a key difference: each user owns shares in a separate, individually named brokerage account, not in an omnibus pool.

Each account comes with separate SIPC coverage and excess SIPC insurance. The on-chain tokens issued by Berry (beTokens) serve as proof of the user's actual brokerage holdings, not synthetic claims.

It employs a deeper issuer-first integration strategy, similar to Galaxy's partnership with Superstate, potentially working directly with companies at the transfer agent level for equity tokenization, but for a broader pool of stocks. If executed, this would be a massive upgrade of Model C's protection level to Model A.

On-Chain Data Leaderboard

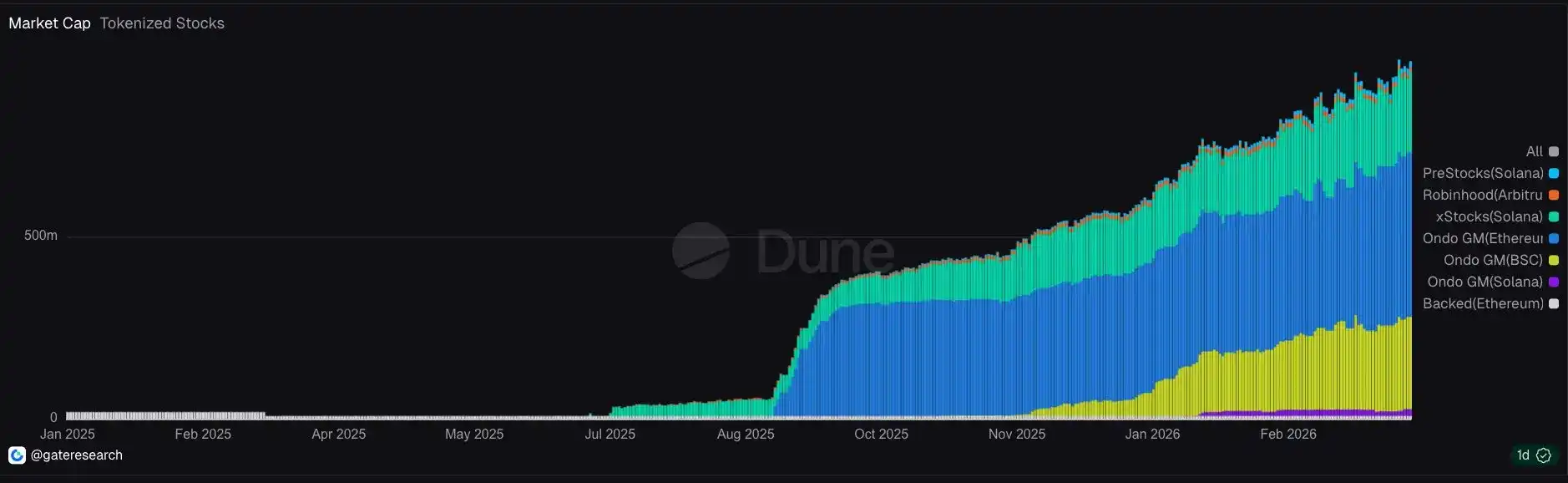

A Dune Analytics dashboard from Gate Research reveals the current reality through on-chain data.

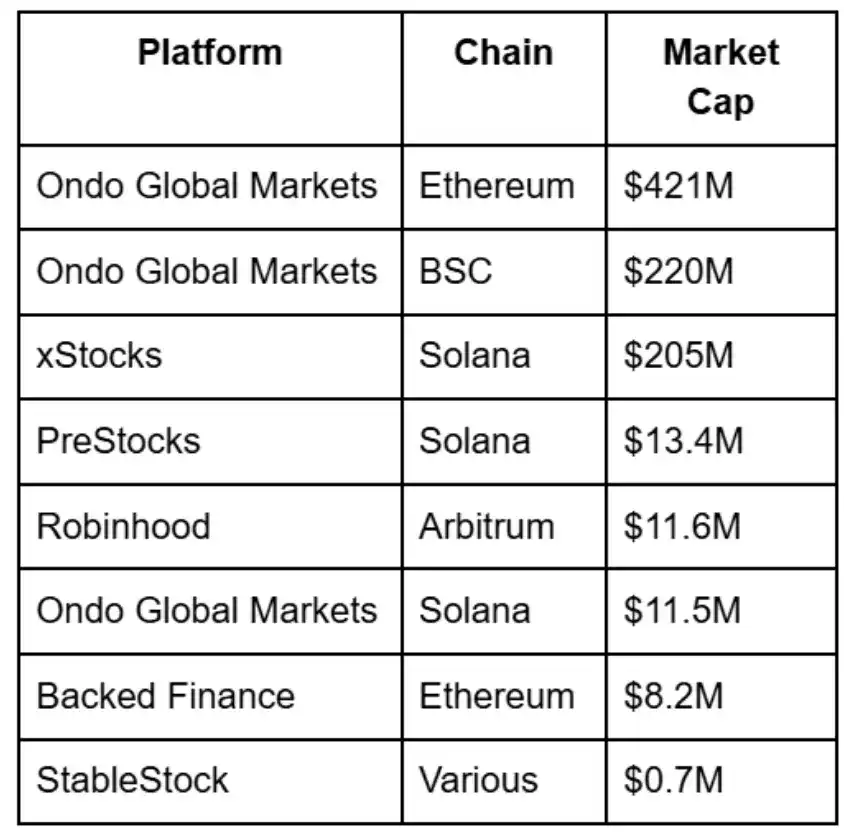

Market Cap by Platform (April 2026)

Total: ~$890 million, up significantly from near zero in January 2025.

Trading Volume and Activity

Market cap data tells only half the story. Trading volume reveals real usage:

- xStocks (Solana): Over $25 billion cumulative volume across 100+ assets. Captures 95-99% of all tokenized stock trading on Solana. This is clearly a retail trading venue.

- Ondo Global Markets: Dominant in TVL/market cap, but lower velocity, more of a "hold" product than an active trading venue.

- Robinhood (Arbitrum): Despite offering ~500 tokenized stocks, the on-chain market cap is only $11.6M. The gap between media coverage and actual usage is stark.

- Ventuals: ~$200M cumulative volume in about 4 months, 5,342 unique traders. Small but extremely active, average position size suggests sophisticated traders here.

- PreStocks (Solana): $13.4M market cap, growing. Offers tokens for xAI, Kalshi, Polymarket, OpenAI, Anduril, SpaceX, and Anthropic.

Assets Actually Being Tokenized

Dune's data reveals interesting patterns in what assets are being tokenized:

- ETFs: SPY, QQQ, etc.

- Large-Cap Tech: TSLA, NVDA, GOOG, etc.

- Crypto-Native Stocks: CRCL, COIN

- Long-Tail Assets: Robinhood has a longer tail of assets

The current competitive landscape has consolidated into what analysts call a "de facto duopoly": Ondo Finance (~58% of total market cap) and xStocks (~24%), with platforms like Backed, Robinhood, etc., splitting the remaining ~18%.

What this number means: 0.0007% market penetration.

Private Stock: Where the Real Excitement Is

Public stock tokenization upgrades the underlying trading infrastructure. Private stock tokenization creates entirely new markets.

The private equity and venture capital market is worth $7 trillion, yet lock-ups of a decade or more, million-dollar entry barriers, and cumbersome annual tax filings exclude the vast majority. However, the hunger for access to these private tickets has never been greater.

Fundrise Case Study: Proof of a Broken Market Structure

When Fundrise listed VCX on the NYSE, the market did something that would alarm every financial planner and excite every tokenization builder: the stock opened at $42, while its Net Asset Value (NAV) was just $19.

It then briefly touched $540 (a 1900% premium), and even after Citron Research shorted it and the price crashed 50%, it still traded at multiples of its actual asset value.

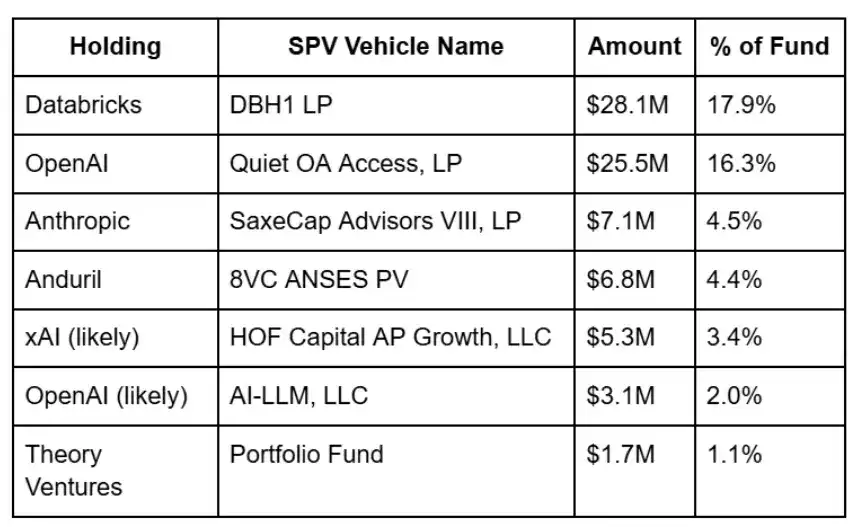

Why? Because VCX's top three holdings—Anthropic, Databricks, and OpenAI—comprise 48.3% of its assets. These are the most sought-after private companies on Earth, and retail investors have virtually no access to them.

As documented by AccessIPOs, the fund's holdings read like a who's who of late-stage AI projects: Databricks ($28M, via DBH1 LP), OpenAI ($25.5M, via Quiet OA Access, LP), Service Titan ($21.3M), dbt Labs ($15M), Anthropic ($7M, via SaxeCap Advisors VIII, LP), Anduril ($6.8M, via 8VC ANSES PV), Canva ($6.2M).

Note that each private company holding is wrapped in an SPV; even the public fund needs intermediary vehicles.

@NoLimitGains and @AccessIPOs have been closely tracking VCX's movements—it's an extremely real case study of what happens when massive demand meets artificially constrained supply.

The LP Market is Bifurcating

The dynamics at the fund level are equally broken. As described by Allocate CEO Samir Kaji (@Samirkaji): the LP (Limited Partner) market is rapidly bifurcating.

Demand for follow-ons in late-stage AI projects is infinite, but it's filled with unauthorized SPVs and fees high enough to destroy returns—one observed example: 15% upfront fee + 20% carried interest (Carry) + 30% of returns over 2x.

Meanwhile, the top 10-20 multi-stage brand funds are oversubscribed. And for emerging managers without a shiny spin-out background or strong operator backing, it's the toughest fundraising environment in a decade.

Molly O'Shea (@MollySOShea, a former VC turned podcast host), also highlights similar dynamics at play across the private market environment.

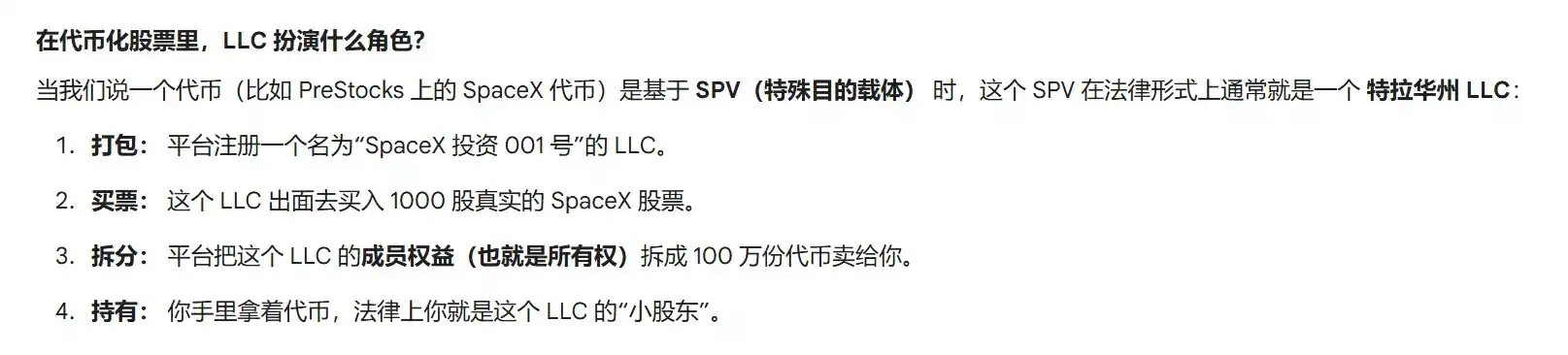

The Challenges of SPVs

An SPV (Special Purpose Vehicle) is a separate legal entity created specifically to hold a single asset, usually a Delaware LLC.

You can think of it as a "shell company" whose sole purpose is to hold a particular stock or investment and then sell shares of that packaged asset to multiple investors. Investors buy not the stock itself, but shares (LP interests) in this shell company.

In venture capital, SPVs are ubiquitous: AngelList Syndicates are SPVs; Access Funds are SPVs within SPVs; every layer of the private market stack relies on them.

SPVs Are Everywhere: Even Inside Public Funds

Looking at Fundrise VCX's holdings reveals how deep the SPV layering goes. Of the fund's ~25 portfolio positions, at least 7 are held wrapped inside SPVs, rather than directly:

This means roughly $77.6M of VCX's assets, nearly half the fund, sits inside SPV wrappers. Each layer adds a layer of fees, a layer of counterparty risk, and a layer of opacity between the investor and the underlying company.

And this is a public fund with SEC reporting obligations. Imagine how deep the nesting goes in private vehicles with no disclosure requirements.

The SPV Market is Exploding

The number of secondary SPVs has grown 545% in the past two years, and the total capital raised through them has grown 1000%. This is a service market worth over $14 billion, projected to reach $27 billion by 2035.

Tens of thousands of SPVs are created annually, and platforms like AngelList, Sydecar, and Allocations make the creation process almost frictionless.

Who Creates SPVs and Why

-

VC Syndicate Leads The most common use case. A syndicate lead finds a deal, creates an SPV on AngelList or Sydecar, and invites their network to co-invest with them. The lead typically takes 20% carried interest.

-

Employees Selling Pre-IPO Stock This is a use case most people don't realize. Employees with vested options who want liquidity cannot simply sell on Robinhood.

Instead, a group of investors forms an SPV to buy those shares. The employee contributes the stock to the LLC and may retain some upside. This keeps the company's cap table clean (now there's one entity instead of 30 new individual shareholders) and helps the company stay below the 500-shareholder threshold that historically triggered public reporting requirements.

-

Access Fund Managers Intermediaries with allocations in hot rounds (Anthropic, OpenAI, SpaceX) create SPVs to provide their LP networks access to co-invest. This is where fee stacking is most extreme.

-

Companies Managing Their Cap Tables Some prefer the SPV structure for secondary transactions as it consolidates shareholders and gives the company more control over who gets on the cap table.

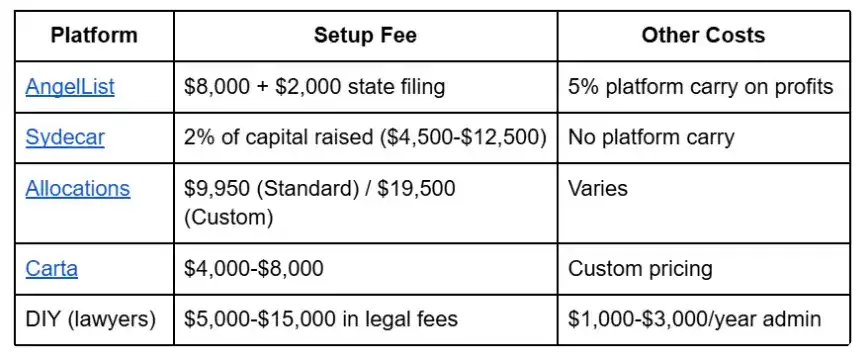

Standard SPV Fees: The Numbers Broken Down

The cost of operating an SPV is significant and compounds over the life of the vehicle:

Ongoing Annual Costs:

Standard Carry Structure:

Carry (carried interest) is the share of investment profits taken by the fund manager, a core incentive mechanism in the VC/PE industry. For example, 20% Carry means: if you invest $1M and ultimately make $2M, $200K of the $1M profit goes to the fund manager, $800K is yours.

- Industry Standard Carry: 20% of net profits

- Setup/Admin Fees Passed to Investors: 0-2% of committed capital at closing

- Some platforms layer their own take on top (AngelList takes an additional 5%)

- Minimum Viable SPV Size: $200K-$500K to keep fee drag below ~3%. Below $200K, fixed costs (setup + annual admin) consume too high a proportion of your returns.

Problems with Traditional SPVs

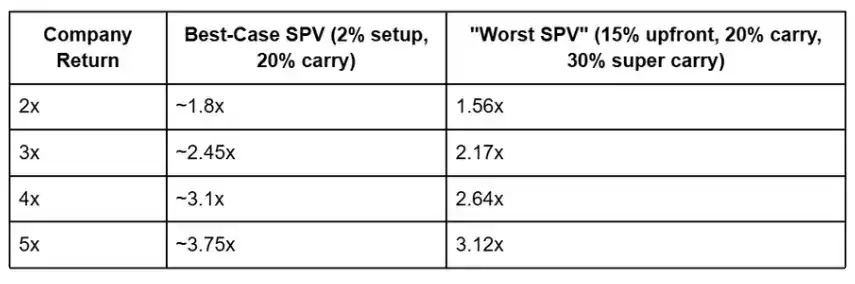

Fee Stacking. When capital flows through a fund of funds into an SPV and then into a co-investment vehicle, the fee layers can be devastating. The worst-case example is 15% upfront fee + 20% carry + 30% of returns over 2x, meaning an investor in a triple-nested SpaceX SPV might need a 3-4x return just to break even.

Platform fees (AngelList's $8,000 + 5% carry) are stacked on top of the lead's 20% carry.

Pricing Opacity. When you buy into an SPV holding SpaceX shares, what price per share are you actually paying? The SPV manager sets the terms; there's no public order book, no price discovery mechanism; you are trusting the middleman completely.

Lack of Liquidity. Once you're in an SPV, you're locked in. Most SPV interests have no secondary market. If you need liquidity in year 3 of a 10-year vehicle, your choices are between "painful discount" and "can't sell at all".

Unauthorized Vehicles. Many SPVs circulating around hot companies are not approved by the companies themselves. OpenAI publicly objected to Robinhood's tokenized product in June 2025, stating the tokens "do not represent equity in OpenAI". The same dynamic plays out across the SPV landscape; the hottest companies often have the most unauthorized vehicles circulating.

How Fees Really Destroy Returns

The fee structure in an SPV deal can silently destroy your returns.

The math is straightforward: In such a stacked structure, the company's valuation needs to quintuple for your investment to yield a 3x return. A strong 3x VC exit, after fees, leaves you with roughly 2.17x—only marginally better than a public index fund, but for that return you took illiquid, highly concentrated single-company risk.

Worse, multi-layered SPVs add opacity at every level, making it harder to verify that real equity exists at the bottom of the structure.

The phrase "the structure is part of the investment" is not rhetoric here. If you don't evaluate the fee-stacked structure as rigorously as you evaluate the company itself, you haven't truly done your due diligence.

How People Actually Buy Private Stock Today

For the same question as public stocks, there are vastly different answers. Here is the real experience of various private stock access channels:

Tokenization platforms offer instant, low-cost access, but the ownership claim is weaker, and regulatory uncertainty is real. Synthetic assets like Ventuals give you price exposure, but funding rates make long-term holding prohibitively expensive.

Traditional Secondary Markets

Forge Global (@Forge_Global) (Acquired by Charles Schwab)

Forge is the most famous name in private stock secondaries—facilitating over 27,000 transactions in 600+ private companies. Now owned by Schwab, giving it access to millions of brokerage clients.

How it actually operates: The entire process happens online on Forge's marketplace platform. You create an account, verify accredited investor status ($200k+ annual income or $1M+ net worth), and enter the marketplace.

The platform shows live bid and ask quotes, provides historical pricing via its proprietary Forge Price index, and contextual market signals. You can submit bids on specific companies, negotiate directly (anonymously) with counterparties, and track progress within the platform.

Who is the counterparty? Mostly employees with vested stock, early angel investors, and VCs seeking partial liquidity. Sellers list shares at an ask price. Buyers make bids. Forge matches and facilitates.

Friction is real: Settlement takes 30-45 days after terms are agreed, which includes the company's Right of First Refusal (ROFR) period, during which the company itself can choose to buy back the shares instead of allowing the transfer. Fees range from 2-4% depending on deal size and volume. Minimums are often $100k+, and all parties must be accredited investors.

Who sets the price? No central exchange. Pricing is driven by buyer-seller negotiation, informed by Forge's proprietary data (last matched trades, bid-ask spreads, historical trends). It's closer to a real estate transaction than a stock trade. Forge provides the data and venue, but the market sets the price.

EquityZen (@EquityZen) (Acquired by Morgan Stanley)

EquityZen uses a fund structure: investors buy into an EquityZen fund that holds shares of specific companies. Fees are 2-2.5%, minimums start at $25k. Morgan Stanley's acquisition sends a strong institutional signal: private stock access is a massive market. It now sits within Morgan Stanley's institutional framework, with over 1,000 registered institutional clients.

Hiive (@Hiive_HQ)

Aims to provide a public stock exchange-like experience for private stock. Real-time quotes, anonymous buyer/seller matching. Shows live pricing: SpaceX ($678.65), Anthropic ($525.37), OpenAI ($608.06).

Minimum $25k, 5% fee charged to sellers. Over 1,000 registered institutional clients. This is the most "exchange-like" experience in the traditional private market, but still accredited-only and requires manual settlement.

Bottom line on traditional platforms: They are proven, regulated, and institutional acquisitions (Schwab/Forge, Morgan Stanley/EquityZen) validate the market.

But they are slow (30-45 day settlement), expensive (2-5% fees), restrictive (accredited only, $25k+ minimums), and manual in nature.

Crypto-Native Approaches

Ventuals (@ventuals) Perpetual contracts on Hyperliquid based on private company valuations. $200M cumulative volume, 5,342 traders. No KYC, no accreditation, $1 minimum. Up to 10x leverage.

Ventuals' value proposition: It provides price discovery and trading mechanisms for assets that previously had none. It's a tool for VC investors looking to hedge portfolio exposure or express a view on Anthropic's valuation that didn't exist 18 months ago.

But the funding rate issue is real. When long demand is overwhelming (which it always is for OpenAI, SpaceX, Anthropic), longs must continuously pay shorts.

At typical rates, holding a long position costs ~4.5% of the position per month, annualized at ~54%. A $10,000 long position bleeds ~$450 per month just on funding rates.

This makes Ventuals a short-term trading tool, not an investment vehicle. You are paying a massive premium for synthetic exposure that erodes your returns every eight hours.

PreStocks (@PreStocks)

PreStocks is one of the most ambitious players in tokenized private stock. Its model: buy actual pre-IPO stock, hold it in an SPV structure, and issue tokens on Solana pegged 1:1 to those shares.

Currently supports 22 pre-IPO companies, including SpaceX, OpenAI, Anthropic, xAI, Anduril, Neuralink, Discord, Kraken, and Epic Games.

How it actually works: You connect a Solana wallet, choose a company, and buy the token on Jupiter or Meteora DEX. No minimum investment. No management fees, no cut of your profits. 24/7 trading, instant settlement.

The tokens are fully composable in DeFi, meaning you can lend them, use them as collateral, or provide liquidity in pools.

Specifics: Over $350M cumulative volume, $5B annualized volume, over 1.5M transactions, 11,500+ token holders. On-chain market cap ~$13.4M.

PreStocks benefits from being rooted in the Solana ecosystem, where tokenized public stocks like xStocks already have active trading, and the trading infrastructure and liquidity pipelines are in place.

What you need to know: PreStocks tokens only give you price exposure; they do not represent any equity. The platform's own disclaimers are very clear: tokens "confer no ownership, voting rights, dividends, information rights, or other legal rights" and "may result in total loss".

The identity of the underlying SPV operator is not publicly disclosed on the website, though the team says they will publish regular external audit reports and offer individual position verification (for a fee), but detailed custody documentation is not yet public. Not available to US citizens.

The transparency gap is a key point to watch. The product design is strong, the fees are fair, and DeFi composability is a real advantage. But for this model to win real institutional trust, the underlying SPV operators must be named, audit reports must be published, and users need clear documentation of the full custody chain from token to actual share.

Jarsy (@JarsyInc)

Jarsy takes a slightly different approach. Core idea is the same, 1:1 asset-backed tokenization, but is more transparent in the acquisition process.

How it actually works: Jarsy gauges investor demand through a pre-sale of tokens. Once a sufficient demand pool is gathered, they use the funds to acquire the actual pre-IPO stock. If the acquisition is successful, the pre-sale tokens convert to official tokens. If the acquisition fails, funds are returned. For every share of underlying stock acquired, exactly one token is minted.

Custody & Transparency: All assets are held in an SPV structure, verifiable via a proof-of-reserves page. Transaction logs and holding records are stored on-chain for auditability. Jarsy claims investors get all relevant economic rights, including dividends and price appreciation, though the legal enforceability of such claims through an SPV wrapper warrants careful scrutiny.

Fees & Access: No management or performance fees. $10 minimum investment. No accredited investor requirement for non-US investors.

The challenge is scale. Current holdings are limited: ~$350k in xAI, ~$490k in Circle, ~$670k in SpaceX. This leads to thin order books, where even medium-sized trades move the price significantly.

Jarsy is at an earlier stage than PreStocks and needs to build significant liquidity for the product to be viable beyond small positions.

A report from Tiger Research outlines the key difference between these platforms and traditional ones: Forge and EquityZen need to match buyers and sellers, taking weeks to settle. Tokenized platforms like PreStocks and Jarsy enable liquidity pools and automated market makers.

This fundamentally provides better execution through continuous counterparty availability, which is why settlement times can drop from 30-45 days to instant.

Important caveat for all crypto-native private stock platforms: PreStocks and Jarsy tokens do not grant legal voting rights and are not endorsed by the companies they represent. US users cannot access. This is early-stage infrastructure, and regulatory risk is real.

The quality of the underlying SPV, who operates it, how the stock is custodied, and the transparency of the fee structure determine whether a platform is a legitimate access layer or just another opaque intermediary.

Our View and Investment Thesis

The infrastructure is being rebuilt. On the exchange side, Nasdaq, NYSE, DTC are moving; on the asset management side, BlackRock, JPMorgan, Franklin Templeton have entered; Schwab acquired Forge, Morgan Stanley acquired EquityZen.

These giants aren't experimenting; they are putting real capital to work. When the underlying pipes change, everything that flows through them changes.

Infrastructure Plays: Securitize ($1.25B SPAC, NYSE partnership) is the most influential private company in the space. Dinari has the first broker-dealer registration. tZERO is building its own chain. These are "picks and shovels" bets.

Ondo Finance ($650M+ market cap, 200+ tokenized stocks) and xStocks ($25B+ cumulative volume) are the on-chain leaders and have found product-market fit (PMF). The question is whether the omnibus model persists or if regulators push towards segregated custody.

The Berry Thesis: Berry's segregated custody architecture addresses the omnibus risk that is undermining trust in every other tokenized stock platform. If the market moves towards requiring segregated account protection (the SEC's framework hints it should), Berry's "brokerage holding verification architecture" becomes the industry standard.

Their focus on the LatAm market opens up a massive, severely underserved market. The shift towards issuer-first integration is their path to massively upgrading the protection level from Model C to Model A.

Private Market Access: The demand is insatiable. VCX's 1900% NAV premium proves it. Schwab's acquisition of Forge and Morgan Stanley's acquisition of EquityZen validate the thesis at the institutional level. A 0.0007% penetrated $7T private market is the largest incremental opportunity in fintech.

The PreStocks Thesis: We see PreStocks as one of the more interesting models in tokenized private stock. The idea of participating in pre-IPO companies starting at $0.01, with zero management fees, fractionalized, and instant settlement is incredibly compelling. But the success of this model hinges on the quality of the underlying SPV.

For PreStocks to truly work at scale, the SPV backing each token needs to be managed by reputable operators, have extremely low and transparent fee structures, clean legal docs, and communicate clearly to users what they actually own (an LP interest in a Delaware LLC, not direct equity).

If they can nail SPV quality, provide clarity on the ownership structure, and build trust around the custody chain, this becomes a powerful access layer for retail investors globally locked out of traditional private markets. We are bullish. But SPV governance is the ultimate unlock.

The key question is not if stocks will be tokenized. The questions are which model wins, which platforms capture that value, and how fast this migration happens.