By | Big Model Home

In the jungle law of artificial intelligence, trust is often more expensive than computing power and more likely to be shattered in the trade-offs of business.

On April 12, MiniMax officially open-sourced its flagship model M2.7, released on March 18, on the HuggingFace platform. The model boasts 229 billion parameters, adopts a MoE (Mixture of Experts) architecture, and requires activating only 10 billion parameters to perform, a series of metrics that point directly to top-tier global closed-source models. On its first day online, it completed adaptations including Huawei Ascend, NVIDIA, and vLLM, sparking industry attention.

However, when developers attempted to deeply engage with the weight files, the appearance of the words "Modified-MIT" in the protocol section instantly dragged this technological feast back into the reality of commercial博弈.

This highly contentious change not only cast a shadow of profit distribution over the "free lunch" but also stung developers seeking a technological safe haven amidst the ecosystems of large companies and startups. For technical leads grappling with workplace anxiety, a legal department's statement that "commercial use requires written authorization" turned the highly anticipated top-tier model's commercial application scenarios into zones of legal uncertainty.

The Trust Hunt of "Open Source" vs. "Open Weight"

In the open-source world, the MIT License symbolizes ultimate freedom and low barriers to entry. Previously, MiniMax's M2 and M2.5 followed this path, and founder Yan Junjie借此 established an image as a promoter of "technology普惠" in the domestic open-source field.

However, the "Modified-MIT" protocol adopted by M2.7 is being questioned by the industry as a form of "nominal openness,实质上的管控" (nominal openness,实质上的 control). Records disclosed by the developer community show that six hours before the weight files went live, the repository protocol still maintained a commercially friendly open-source form similar to Llama 3, but at the moment of official release, it was changed to a modified version requiring "written authorization for commercial use."

This practice essentially alters the契约 spirit of open source. For technical骨干 experiencing an "AI midlife crisis" and trying to use open-source models for internal innovation or entrepreneurship, this "legal uncertainty" is fatal—the final interpretation of so-called "written authorization" rests entirely with the vendor.

In the view of Big Model Home, the core of this controversy is essentially the industry's long-term confusion between two concepts — "open source" as defined by the OSI, and merely opening model files, "open weight". The Modified-MIT protocol, by explicitly restricting commercial use, no longer符合 the globally accepted open-source definition and belongs only to the "open weight" category.

Some netizens stated, "This is not open source at all; this is just公开了模型文件 (公开了 model files)." This gap between name and reality feels more frustrating than simply announcing it as closed source from the start. They指责 that if every vendor uses the MIT name to create "private property," the consensus system of the open-source community will completely collapse.

What's more致命 for developers and enterprises is: MiniMax is already a listed company, and all protocol changes must服从财报与合规 (服从 financial reports and compliance). Today it changes the protocol for "narrowing losses," tomorrow it might charge per Token for "quarterly performance"—the "certainty" of a listed company is always written in the financial reports, not in community promises.

When Technological Ideals Hit the Wall of Commercialization

From an enterprise operation perspective, MiniMax's shift is not without trace. Training a MoE model with 229 billion parameters is a multi-million dollar gamble involving投入的电力、算力集群折旧以及高昂的人力成本 (invested electricity, computing cluster depreciation, and high human costs).

Yan Junjie once publicly stated, "Open source can force us to improve algorithm innovation efficiency and also enhance our global technology brand."

But after MiniMax officially landed on the main board of the Hong Kong Stock Exchange IPO on January 9, 2026, hailed as the "first stock of general artificial intelligence," MiniMax, stepping into the capital market, also had to modify its own rules of the game. With the stock price experiencing剧烈波动 after hitting a high of 1330 HKD (as of April 14 close, the stock price was 951 HKD, down 28% from the peak), the focus of investors is no longer the number of likes on HuggingFace or community reputation, but the hard revenue growth rate and profit inflection point in the financial reports.

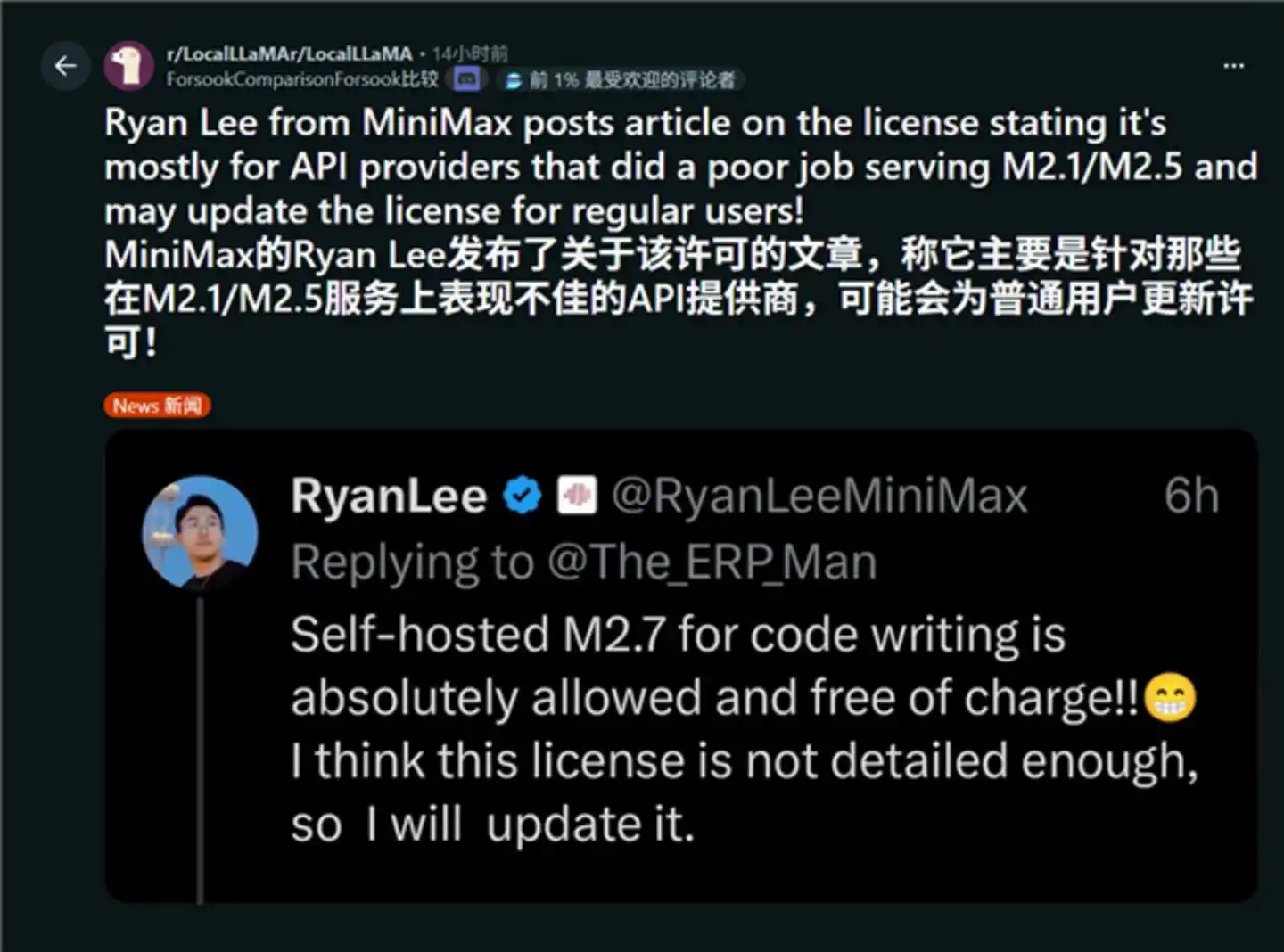

MiniMax Developer Relations负责人 Ryan Lee responded on X regarding the reason for prohibiting commercial use. He mentioned that (under the previous open-source protocol) MiniMax's models appeared on some hosting sites, but some users found the quality to be worse than the official ones after trying them—there was excessive quantization, template errors, silent replacements, or they weren't even their models, leading these users to believe MiniMax's quality was mediocre. The protocol adjustment was due to "third-party hosting platforms胡乱修改模型, causing reputational damage."

This is also a pain point for leading AI companies like MiniMax: sometimes investing money and people in technology普惠 ends up handing a knife to competitors. The anxiety of watching others use your model to create commercial shell products, sell them to clients for huge profits, while you bear the huge server costs, is enough to destroy any idealist's mindset.

For Minimaxes: Is it the羽毛 of the brand, or the活路 of business? It's a painful multiple-choice question.

Undoubtedly, Yan Junjie's ideal ultimately succumbed to the survival anxiety of commercialization.

On March 2, Minimax's first full-year financial report showed: 2025 revenue of $79.04 million, a surge of 158.9% year-on-year, but behind this, the annual loss widened from $465 million in 2024 to $1.872 billion in 2025. The adjusted net loss was still as high as $250 million, meaning for every $1 earned, they still lost over $3. More critically: over 60% of expenditure was directed towards computing power and model training. Training a model like M2.7 costs tens of millions of dollars per round. Meanwhile, the B-end open platform (API/commercial authorization) is Minimax's only high-growth, high-margin sector, with 2025 revenue of $25.96 million, a year-on-year increase of 197.8%, growing much faster than the C-end.

The tightening of the M2.7 protocol is essentially MiniMax circling its wagons. It allows research and individual developers to continue using it for free to retain the seeds of the ecosystem; but it strictly prevents commercial use to ensure every blade of grass grows in its own field during the upcoming commercialization harvest period.

Riding the "open source" traffic wave while keeping legal risks and income interpretation rights firmly in hand. This is not "ideal succumbing to reality," but "securing profit expectations first, then talking about community sentiment." From a business management perspective, it's无可厚非, but it also taints the originally pure open-source spirit with a strong whiff of "client mindset."

The Polarization of Rule-Followers and Performance-Seekers

In the game of large models, certainty is far more important than pure performance parameters.

Developers are a simple group; they are willing to stay up late tuning parameters for you, willing to fix bugs for you on GitHub, provided you respect their rules of the game. After the M2.7 open-source incident, the global developer community experienced severe polarization.

Pragmatic "performance-seekers" believe: Since the performance rivals GPT and it's free for research, it's无可厚非 for vendors to seek commercial收益.

However, in global open-source developer communities, the vocal majority of "rule-followers" felt a severe "trust幻灭" (trust disillusionment). On mainstream communities like Reddit, many voices have already turned to fully open-source series like Qwen.

Why? Because for enterprise users, "certainty" is far more important than "performance".

If a company's open-source promise can be微调 at any time based on "commercial anxiety," then who dares to build their core business on its foundation? Changing the protocol name today, will it charge per Token tomorrow? This fear of future uncertainty is quickly反噬 the technology brand that MiniMax worked hard to build.

The once most radical, purest open-source benchmark has now become a typical case of "definition confusion" in the global community. This shattering of trust is clearly not something a few PR responses can mend.

Survival Rules for Developers in the AI "Post-Open Source Era"

It's not just MiniMax's M2.7 protocol modification; previously, Ali's Lin Junyang's departure also caused震动 in the AI open-source industry. As more large model companies step into the capital market, many worry that the large-scale open-source era of "contributing for love" is accelerating towards its end.

The future large model industry might evolve into two ecosystems: one is the true "public good," like Llama, Qwen, backed by large consortia, using open source to exchange for monopoly on underlying standards; the other is conditional gifts like M2.7, which are more like "commercial show flats"—you can look, you can try staying, but to move in (commercial use), please turn the corner and pay the service fee.

In fact, in the context of large companies, survival itself is a morality. But if you choose pragmatism, please put down the banner of lofty ideals; if you choose commercial licensing, please stop蹭 the光环 of MIT.

This incident demonstrates three survival rules for all AI practitioners in the "post-open source era":

First, all "free" things have an expiration date. When selecting an architecture, the first step is not to test parameters, but to have legal review the protocol. Especially for those responsible for promoting projects within large companies, every word in the protocol could become a stain on your review six months later.

Second, "OpenWeights" does not equal "OpenSource". Future industry narratives will revolve more around the former. We must learn to get used to these "gifts with locks" and reassess their value within商业 logic.

Third, trust itself is an asset. Vendors焦虑 revenue, developers焦虑 changes. This bidirectional anxiety is precisely the阵痛 of the current AI industry bubble being squeezed out.

As of publication, Yan Junjie himself has not publicly responded. Perhaps in his calculation logic, compared to the虚无缥缈 community reputation, obtaining real commercial authorization contracts is the ticket to growth that MiniMax pursues.