Author: Zhou, ChainCatcher

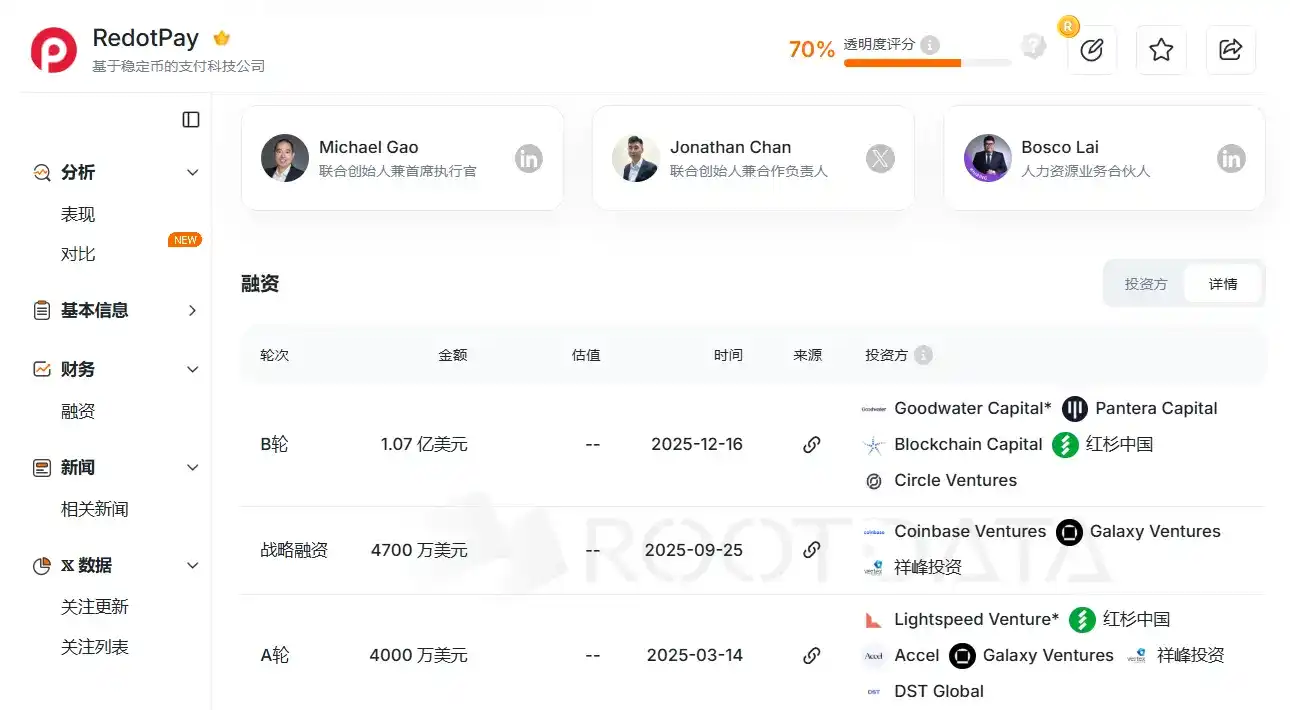

By the end of 2025, Hong Kong-based crypto payment company RedotPay completed a $107 million Series B funding round led by Goodwater Capital, with top-tier institutions such as Sequoia China, Pantera Capital, and Circle Ventures also appearing on the list of co-investors.

Image from RootData

Why Did It Become a Dark Horse in the Payment Track?

RedotPay's story began in early 2023. Its co-founder and CEO, Michael Gao, had worked for top banks such as HSBC and DBS, and was also a core member of加密技术服务商 ChainUp. Additionally, the company's COO Troy Yao and CTO Xinman Fang both have years of experience in the crypto industry or software development, coming from platforms like Huobi or VCB.

According to informed sources, RedotPay was initially invested in and incubated by Yuan Dawei, who began researching Bitcoin as early as 2010. He was one of the early co-founders of Huobi and the founder of库神钱包, wielding significant influence and trust within the early Bitcoin investor community and miner groups. He is also one of the behind-the-scenes operators of several hot tokens in recent years, well-versed in early user growth and narrative logic in the crypto industry.

The team background determined that RedotPay follows a typical Chinese internet playbook: first, seize market share regardless of cost, then raise连续融资 after scale effects form, and finally monetize through diversified financial services.

Specifically, RedotPay's core business is driven by a Visa co-branded debit card. Users top up cryptocurrencies like USDT and BTC into the App, and can then use the card for instant settlement through the global Visa payment network, including offline ATM withdrawals, supermarket刷卡, online subscriptions, and Apple Pay/Google Pay, with the system automatically handling the清算 of cryptocurrency to fiat.

On this basis, RedotPay further衍生出 Global Payout (local fiat代付), P2P fiat trading zone, and the Earn & Credit financial module with interest-earning and lending functions.

- Visa payment card: Supports direct stablecoin settlement, covering over 100 countries globally.

- Global Payout: Supports direct withdrawal of local fiat (e.g., BRL, NGN).

- OTC and P2P market: By introducing local OTC merchants, users can directly buy or sell cryptocurrencies with local currency.

- Earn生息: Increases资金停留时长 through financial products.

- Crypto Credit: Provides credit lines collateralized by coins.

Image from RedotPay APP

RedotPay's early landscape was highly focused on emerging markets with剧烈 fluctuating fiat exchange rates, such as Nigeria, Brazil, and Southeast Asia.

- May 2023: RedotPay officially launched in Hong Kong and quickly obtained an MSO license.

- October 2023: Officially launched virtual Visa cards and physical cards, supporting Apple Pay and Google Pay.

- August 2024: User base surpassed 5 million.

- March 2025: Completed a $40 million Series A funding round led by Lightspeed.

- June 2025: Officially launched the Global Payout (global代付) function.

- September 2025: Received $47 million in strategic investment,引入 Coinbase Ventures and other capital, valuation reaching the $1 billion mark.

- October 2025: Announced that the P2P market supports trading in over 50 local fiat currencies.

- December 2025: Completed a $107 million Series B funding round, introducing top institutions like Sequoia China, Pantera Capital, and Circle Ventures. Meanwhile, the company disclosed that its global registered users exceeded 6 million, annualized payment volume exceeded $10 billion, covering over 100 countries, and it had already achieved profitability.

According to informed sources, its global registered real users have now exceeded 10 million, with the latest valuation potentially reaching $2 billion. From its official start in 2023 to achieving stable profitability now, RedotPay took less than three years, which is rare in the illiquid crypto market.

Its growth logic is a combat model called the "Army System." Simply put, it abandons high-cost online user acquisition and instead builds an offline distribution network.

An anonymous crypto card entrepreneur emphasized that RedotPay initially relied almost entirely on this ground promotion system, maintaining high card issuance fees and transaction fees to leave significant profit margins for the offline promotion teams. Currently, its virtual card issuance fee is $10, the physical card is $100, and each transaction includes about a 1% handling fee.

The high profit-sharing mechanism makes every local KOL, OTC merchant, community leader, and even micro-loan intermediary a promoter of RedotPay.

An industry observer stated that RedotPay's traffic experienced a step-change growth in early 2025, and almost all of it came from user主动搜索, which means it formed word-of-mouth diffusion among scenario-specific populations, making its user acquisition efficiency top-tier in the early stages.

According to official data, as of November 2025, RedotPay added over 3 million new users in that year alone, with annual payment volume growing nearly three times year-on-year. Industry insiders said that among RedotPay's users, there might be a group of core users with high consumption capacity and frequency, contributing a significant proportion of revenue.

Valuation Premium Behind the NeoBank Closed Loop

However, how far can a strategy relying on high fees to maintain incentives go?

Although users are willing to pay high costs at this stage, relying on high fees to 'feed' offline agents is essentially trading financial spreads for growth speed.

In the highly competitive environment of crypto payments in 2026, RedotPay seems to be caught in a paradox: to maintain agent loyalty, it must maintain high profit-sharing; but to cope with erosion by licensed giants, it must lower fees.

The high valuation given by the capital market is clearly not just paying for the bid-ask spread (Spread). In fact, what capital values is who can make users leave their money behind, and the market is currently paying a premium for this potential banking attribute.

The真正值钱的地方 of RedotPay lies in the high degree of completion in their transition from a payment tool to a crypto-native bank (NeoBank).

Pure payment channels have extremely low毛利 and are极易被替代, while RedotPay, through the Earn interest-earning and Crypto Credit lending functions, builds a complete资金闭环 of "top-up - earn interest - borrow - consume," preventing users from topping up and leaving immediately.

Under this logic, users top up USDT into the App, retain funds through the Earn (interest-earning) function, and then use Credit (collateralized lending) to obtain fiat credit for consumption. As an industry observer said, even if only 10% of the $10 billion transaction volume is converted into retained沉淀, the interest spread and financial derivative income generated will make its profit margin far exceed that of traditional payments.

BKJ market负责人伯言 believes that the key to RedotPay's success lies in its early courage to make product decisions围绕真实使用场景, because users' real needs are the source of development momentum.

However, behind the seemingly beautiful closed loop lies a liquidity game. 伯言 also reminded that once there is insufficient risk control buffer between interest earning, credit granting, and consumption, in极端行情 or during liquidity紧张, the highly nested financial closed loop may face极大的承压风险.

Under the NeoBank shell, whether the assets have achieved true legal隔离 is the next拷问 it must answer.

Compliance Concerns and Boundary Racing

From another perspective, RedotPay is actually utilizing the window period where regulation has not yet fully covered emerging markets to complete a race关于效率与合规边界.

After all, behind the prosperity of the payment track始终存在 the达摩克利斯之剑 of compliance.

Chaintech founder Kevin Piao emphasized that the famous "compliance cliff" theory同样适用 in the Web3 payment field, meaning the smaller the scale, the safer; the larger the scale, the more dangerous.

Early rapid growth is usually because监管的灰色地带 or bank risk control滞后性 are utilized. But when transaction volume突破某个临界点 (e.g., tens of millions of USD per month), it triggers deep compliance audits from the card issuer (Issuer) and clearing network (Visa/Mastercard). Many once-popular加密卡商 died here.

Although RedotPay has been actively布局合规 and spends high compliance maintenance costs, the challenge it faces still lies in the dynamic upgrade of regulatory standards.

RedotPay adopts a "jigsaw puzzle-style compliance" structure. Although it holds an MSO (Money Service Operator), Money Lender license, and TCSP (Trust or Company Service Provider) license in Hong Kong, and has obtained VASP registration in places like Lithuania and Argentina, this does not mean it can rest easy.

Mankun Law Firm lawyer Liu Honglin analyzed that this组合整体属于 'the business can run, and it can also be explained to regulators,' but it is not one license that covers everything.

Why is it called a jigsaw puzzle? Because it actually stacks together businesses like收款,换汇,转账,跨境兑付,借贷, and生息, which have completely different legal categorizations in traditional finance.

The biggest risk of this structure is that certain links in the product chain may only "look similar," but their legal定性 remains in a gray area.

Lawyer Liu Honglin pointed out that Hong Kong's MSO essentially regulates "fiat exchange," but "stablecoin-to-fiat exchange" is not automatically considered a foreign exchange business in many countries. Furthermore, the real regulatory gray areas are concentrated in the担保执行 of crypto-collateralized lending and the性质定性 of Earn products.

Regarding the Earn interest-earning function, which has attracted much capital attention, Lawyer Liu直言, such products are极易被视为未经注册的证券化产品或集体投资计划 from the perspective of regulators in many countries. "Regulators believe you are issuing financial products with return expectations to the public and should be subject to securities law regulation, not bypass it using 'crypto innovation.' The hefty fine imposed by the U.S. SEC on BlockFi is a lesson from the past."

In the Crypto Credit (crypto-collateralized lending)环节, although the money lender license solves the "lending资格," crypto assets as collateral have far less legal certainty than traditional collateral.一旦遭遇极端行情 or清算纠纷, whether its担保权益 can obtain court support still lacks a mature legal framework.

Conclusion

The crypto market in 2026 is in a collective window期走向台前的 IPO window期. RedotPay and its competitors are accelerating. In January this year, its core competitor Rain announced the completion of a $250 million Series C funding round, with a valuation reaching $1.95 billion.

For RedotPay, licenses are just the shell; continuous compliance内功 is the lifeblood, and this is the team's most fragile一环. Whether it can repair its jigsaw structure through compliance内功 before regulators close the net will determine whether it ultimately becomes a financial giant in the crypto world or merely a流星 in payment history.

In short, this race about efficiency, greed, and boundaries has already entered the second half.

Click to learn about open positions at ChainCatcher