Author:Yuki is short, so is life

Compiled by: Jiahuan, ChainCatcher

Liquidity is the source of confidence in assets. Only with sufficient depth can the market accommodate large transactions, whales can freely build positions, and assets can function as collateral, as lenders need to ensure they can be liquidated smoothly when necessary. Tokenized assets with insufficient depth struggle to attract users, which not only suppresses market participation but also creates a vicious cycle of liquidity drying up.

The original intention of tokenization was to maximize capital liquidity, unlock the utility of DeFi, and open up access to off-chain assets. Its promise is highly attractive: bringing trillions of dollars from traditional financial markets on-chain, allowing anyone to access, lend, and combine them in ways never permitted by traditional finance.

But beneath the surface, most tokenized assets trade in markets that are illiquid and fragile, unable to support sufficient transaction规模. As a prerequisite for composability and financial utility, true liquidity has not yet materialized. The resulting costs and risks may be imperceptible in small transactions, but once large funds attempt to enter or exit, these hidden dangers quickly become apparent.

The Current Liquidity Landscape

The first hidden cost of tokenized assets is reflected in slippage.

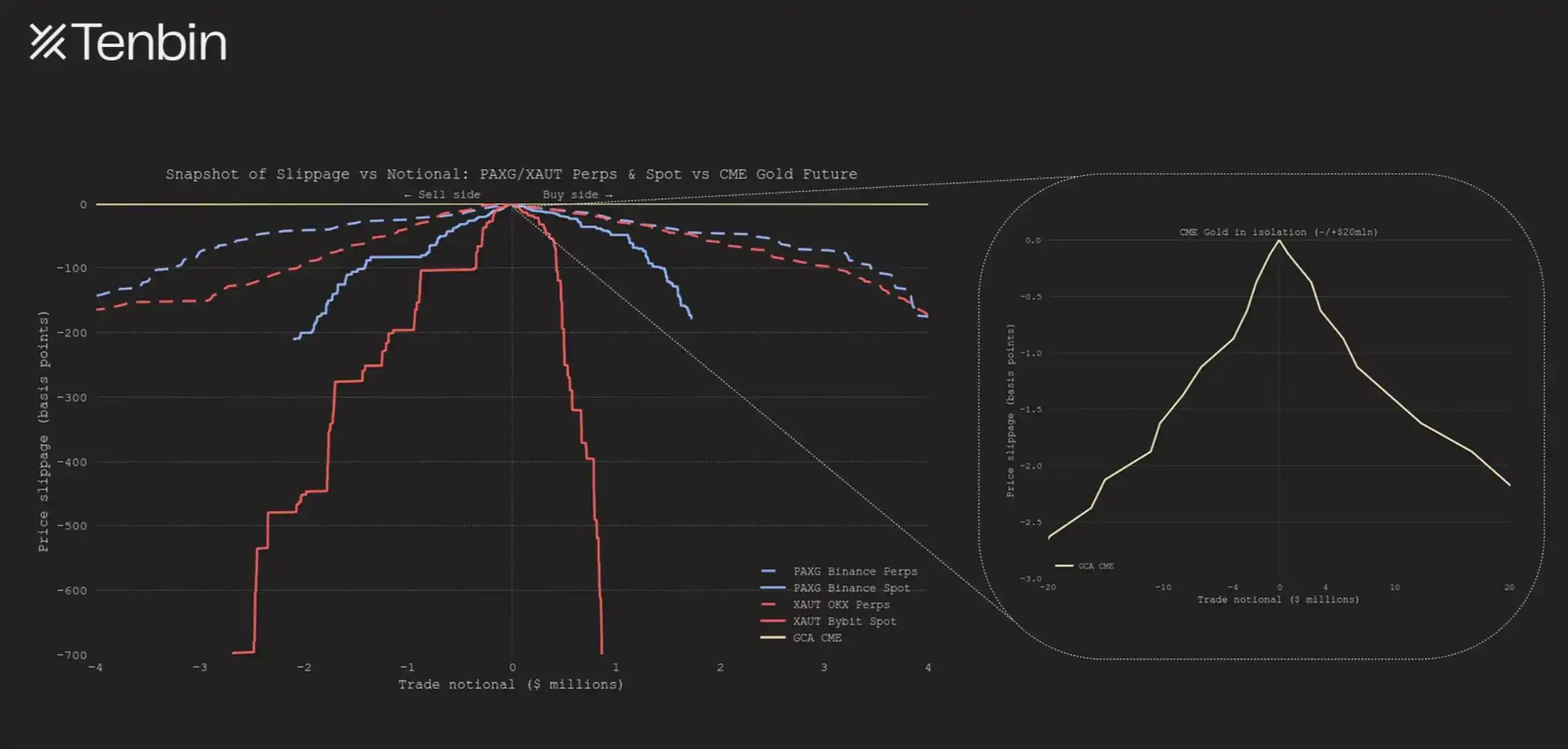

Taking tokenized gold as an example, the chart below compares the expected slippage for different transaction sizes between major centralized exchanges and the traditional gold market. The difference is staggering.

As trade size increases, the slippage for PAXG and XAUT perpetual contracts grows exponentially, reaching about 150 basis points (bps) at a notional value of approximately $4 million. In contrast, the slippage curve for the CME (Chicago Mercantile Exchange) is almost flat against the zero axis, barely distinguishable from the X-axis.

The spot markets for PAXG and XAUT are even more constrained. Although the chart shows the most liquid spot markets for each token, the depth on either side of the order book does not exceed $3 million. This limitation is evident from the early truncation of their curves.

Another chart on the right shows the CME curve separately, highlighting its near-flat liquidity profile. Even at notional values far exceeding $4 million, its slippage remains extremely stable. A $20 million gold futures trade would incur a price impact of less than 3 basis points. CME's liquidity is several orders of magnitude deeper than any cryptocurrency trading venue.

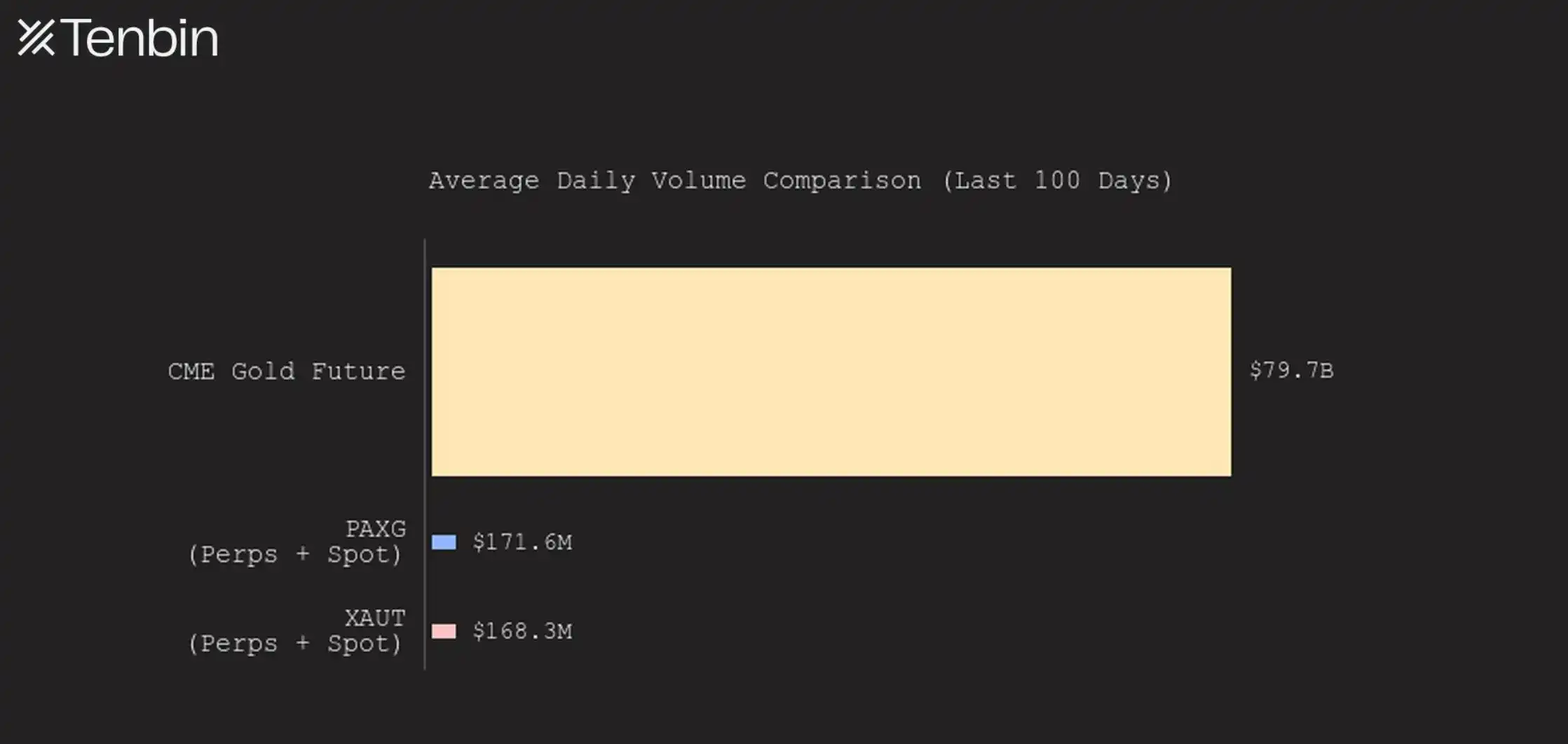

This difference has direct consequences. In deep traditional markets, price impact is negligible even for large trades. In shallow tokenized asset markets, the same trade incurs immediate costs and becomes increasingly difficult to unwind. The comparison of average daily trading volume below clearly shows the magnitude of this gap, which exists not only in the gold market but also for many other assets.

(Chart description: Average daily trading volume comparison: CME Gold Futures vs. PAXG/XAUT Perps & Spot)

So far, these examples have focused on centralized exchanges. What about AMMs (Automated Market Makers)? The short answer is: it's worse.

Look at this XAUT trade from February 2025. A user spent 2,912 USDT to receive only $1,731 worth of XAUT (at the real gold price at the time), paying a 68% premium.

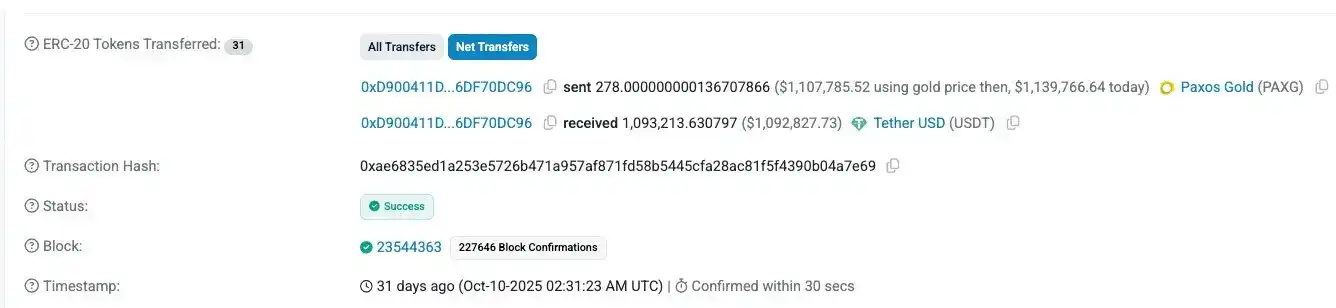

Another trade shows a user selling $1.107 million worth of PAXG (at the gold price at the time) and receiving only 1.093 million USDT, a slippage of about 1.3%. While less extreme, this level of slippage is still unacceptably high in the context of traditional markets, where price impact is typically measured in single-digit basis points, not percentages.

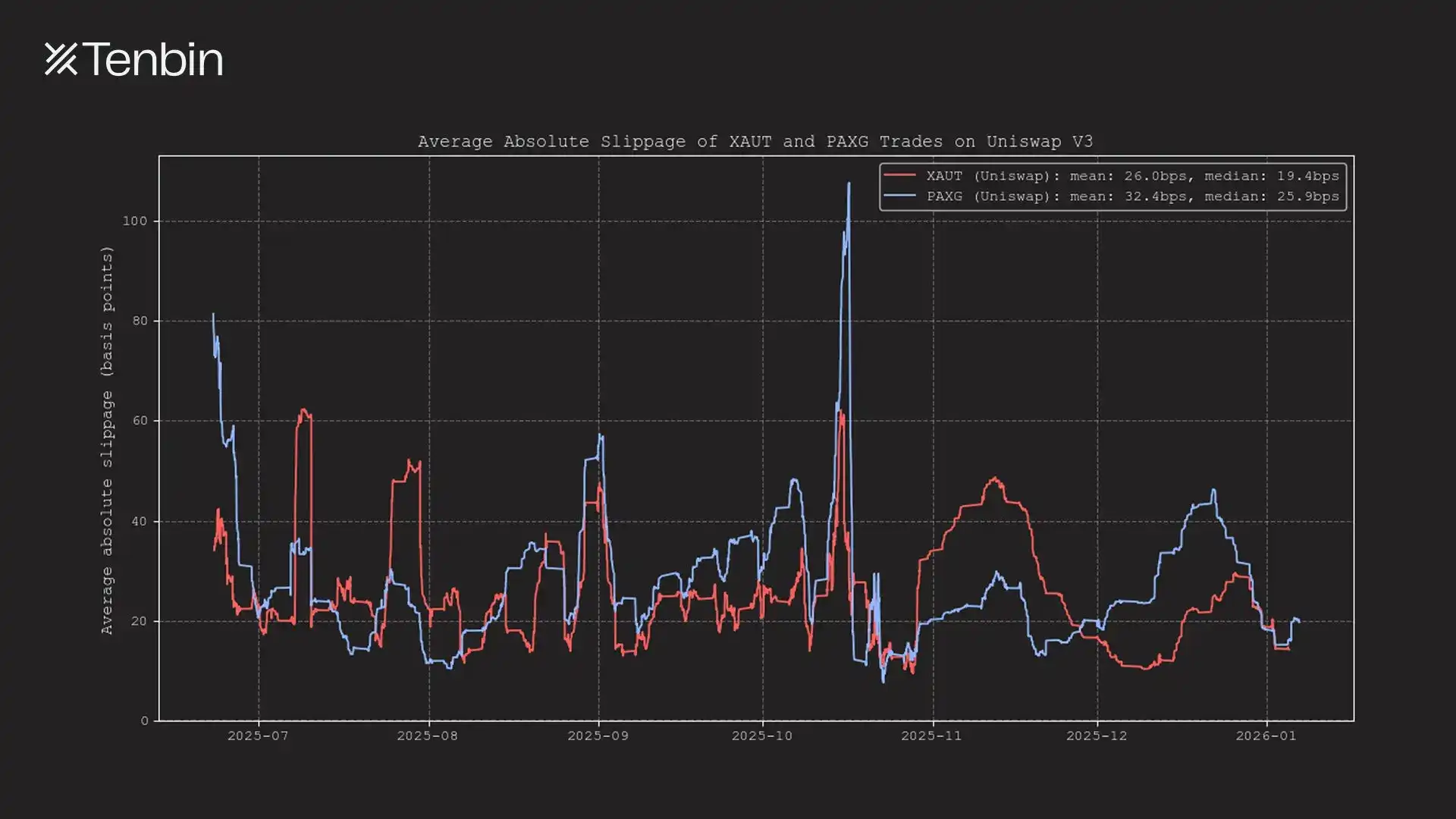

Furthermore, over the past six months, the average slippage for XAUT and PAXG trades on Uniswap has ranged between 25 and 35 basis points, occasionally even exceeding 0.5%.

(Chart description: Average absolute slippage for XAUT and PAXG trades on Uniswap V3)

We use gold for this analysis because it is currently the largest non-dollar, non-credit tokenized asset on-chain. But the same pattern applies to tokenized stocks.

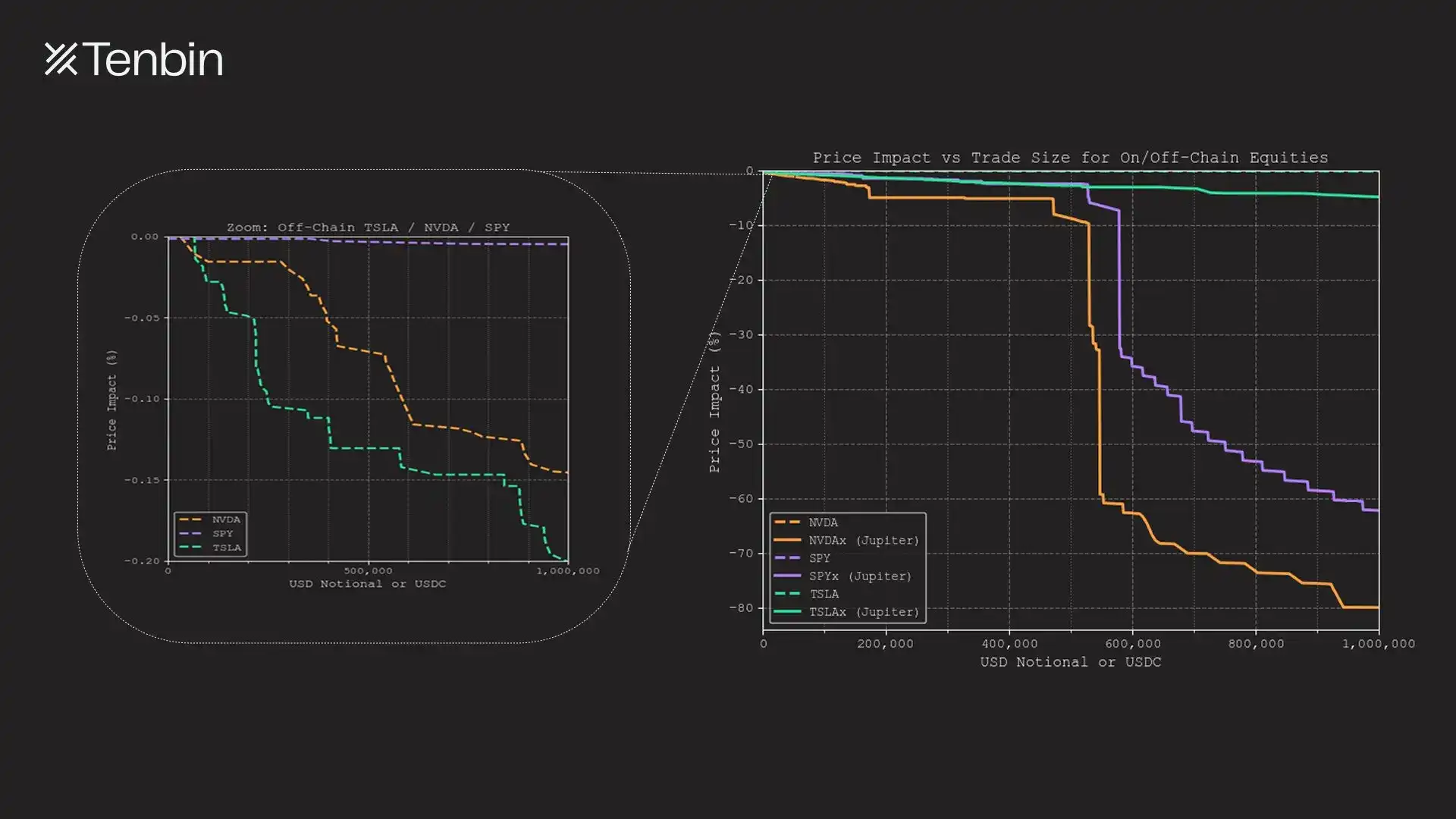

(Chart description: Slippage vs. trade size comparison: Nasdaq's NVDA/TSLA/SPY vs. NVDAx/TSLAx/SPYx)

TSLAx and NVDAx are currently two of the top ten single-name tokenized stocks. On Jupiter, a $1 million trade for TSLAx would incur about 5% slippage. NVDAx faces an insurmountable 80% slippage. In contrast, a $1 million trade for Tesla or Nvidia in the traditional market would incur a price impact of only 18 basis points and 14 basis points respectively (and this doesn't even include the liquidity from off-exchange venues like dark pools).

These costs are easily overlooked in small trades but become unavoidable once users attempt to scale. Illiquidity translates directly into real losses.

Are On-Chain Tokenized Markets Dangerous?

Illiquidity not only increases transaction costs but also disrupts market structure.

When liquidity is thin, pricing mechanisms are极易 distorted, order books are filled with noise, and oracle price feeds subsequently inherit this noise. Small trades can trigger chain reactions in interconnected systems.

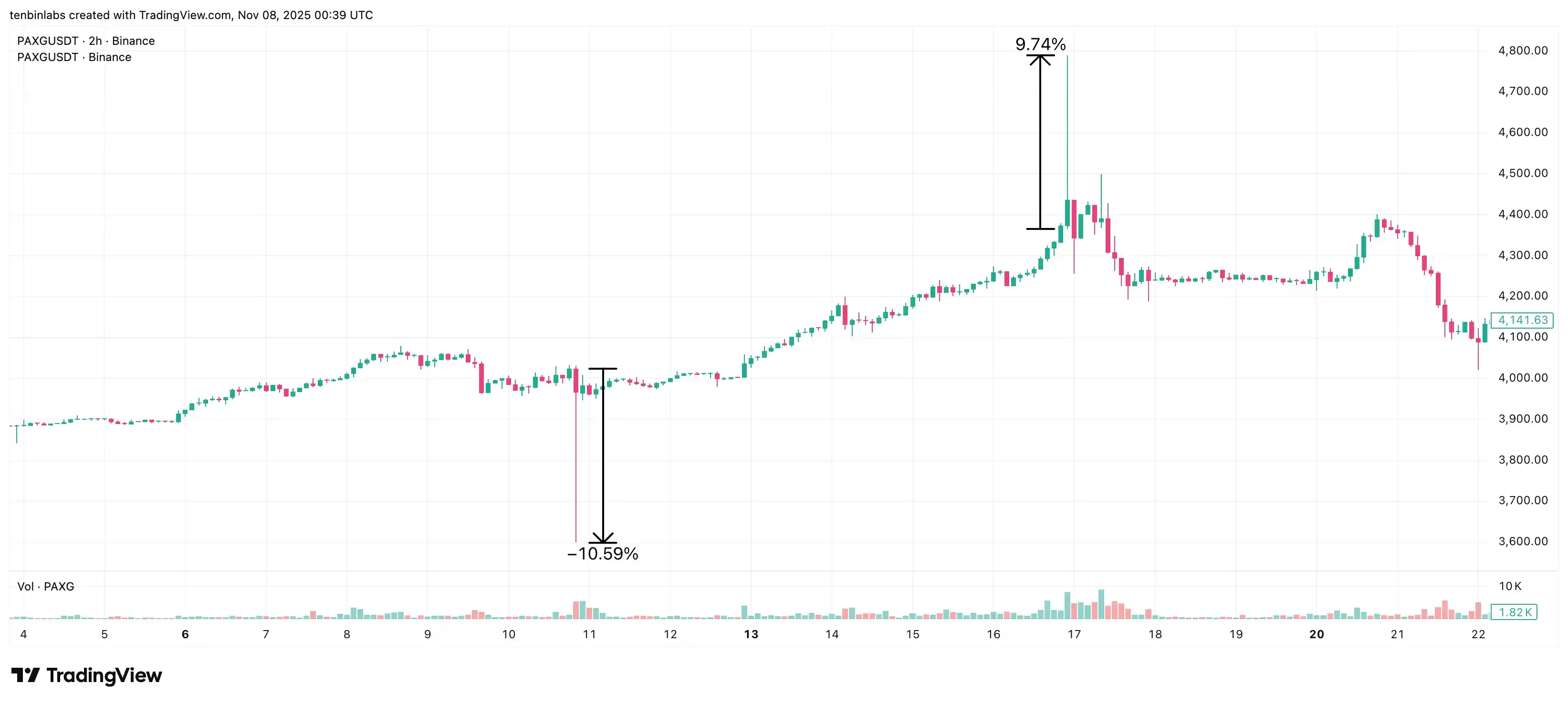

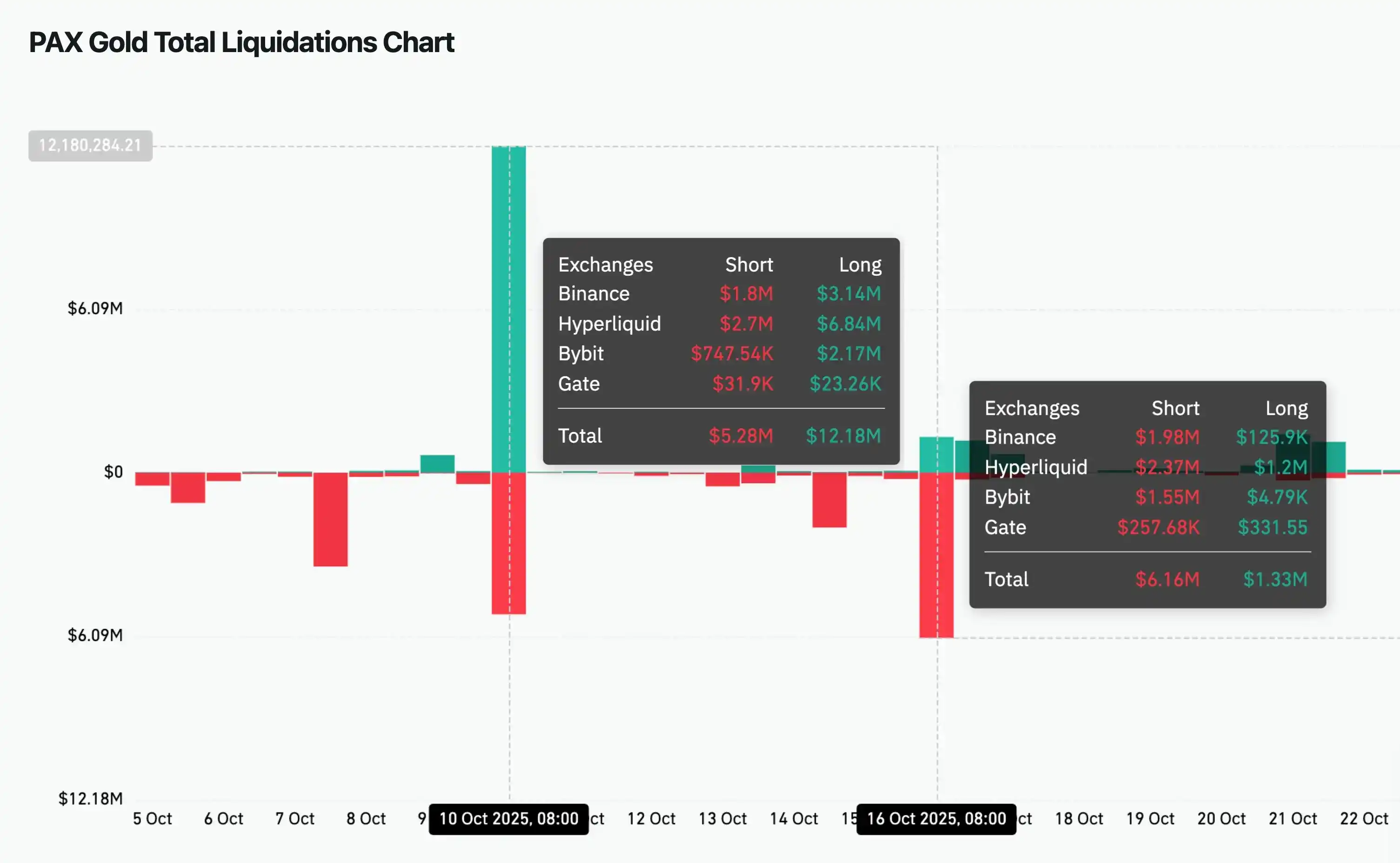

In mid-October 2025, Binance's PAXG spot market experienced two "flash crash" within a week. On October 10th, the price dropped 10.6%; on October 16th, it surged 9.7%. Both moves quickly reversed, indicating they were driven by order book fragility rather than fundamental changes.

Because the tokenized asset ecosystem is highly interconnected, instability in a major trading venue does not remain localized. Binance's spot price carries the highest weight in Hyperliquid's oracle construction. As a result, during these two events, $6.84 million in long positions and $2.37 million in short positions were liquidated on Hyperliquid—a figure that even exceeded the liquidation volume on Binance itself.

This outcome is disconcerting. It demonstrates how a single low-liquidity venue can propagate and amplify volatility across multiple markets. In extreme cases, this also increases the risk of oracle manipulation. Participants who never traded on the original spot market can still suffer losses through liquidations, price distortions, and widening spreads.

All of this traces back to the same root cause: a lack of true liquidity in the primary market.

(Chart description: CoinGlass's PAXG liquidation chart)

The Structural Problem of Illiquidity

The illiquidity of tokenized assets is a structural problem.

Liquidity does not automatically appear once an asset is tokenized. It is provided by market makers, who are inherently capital-constrained. They allocate capital to places where inventory can be deployed efficiently, risk can be managed continuously, and where they can exit with minimal time and cost friction.

Most tokenized assets fail on these dimensions.

To provide liquidity, market makers must first mint the asset. In practice, minting involves not only explicit costs (issuers typically charge 10 to 50 basis points in minting and redemption fees) but also operational coordination, KYC, and settlement through custodians or brokers, rather than atomic on-chain execution. Market makers must deposit funds upfront and wait hours or days to receive the tokenized asset.

Once inventory is established, it cannot be redeemed. Redemption windows are typically measured in hours or days, not seconds. Many tokenized assets only allow redemption on a T+1 to T+5 basis, with daily or weekly limits. For larger positions, fully unwinding can take days or even longer.

From a market maker's perspective, this inventory is effectively illiquid and cannot be quickly recycled.

Market makers providing depth must hold inventory through market cycles, absorbing and hedging price risk while waiting for redemption. During this time, the same capital could have been deployed in other crypto markets, where inventory requirements are minimal, hedging is continuous, and positions can be closed instantly; this is why the opportunity cost for market makers in tokenized assets is extremely high.

Faced with this trade-off, rational liquidity providers allocate capital elsewhere.

The current market structure is not suited to solve this problem. AMMs shift inventory risk to liquidity providers while inheriting the same redemption constraints. Order book-based venues merely aggregate fragmented maker liquidity from various exchanges.

The result is a market stuck in a chronically shallow equilibrium. Limited liquidity discourages participation, and low participation further reduces liquidity. The entire tokenized asset ecosystem is trapped in this vicious cycle.

A New Market Structure

Illiquidity is a structural barrier to the growth of tokenized assets.

Insufficient depth hinders scaled positioning, fragile markets propagate instability across protocols and venues. Assets that cannot be reliably exited cannot serve as trustworthy collateral. In today's tokenized model, liquidity remains constrained, and capital efficiency remains low.

For tokenized assets to truly achieve scaled adoption, the market structure must change.

What if price and liquidity could be mapped directly from off-chain markets, rather than being rediscovered and cold-started on-chain? What if users could access tokenized assets at any scale without forcing market makers to hold illiquid inventory? What if redemption was fast, predictable, and unrestricted?

The failure of tokenization stems not from putting assets on-chain, but from never truly putting the markets that underpin them on-chain.