Original | Odaily Planet Daily (@OdailyChina)

Author | Golem (@web 3_golem)

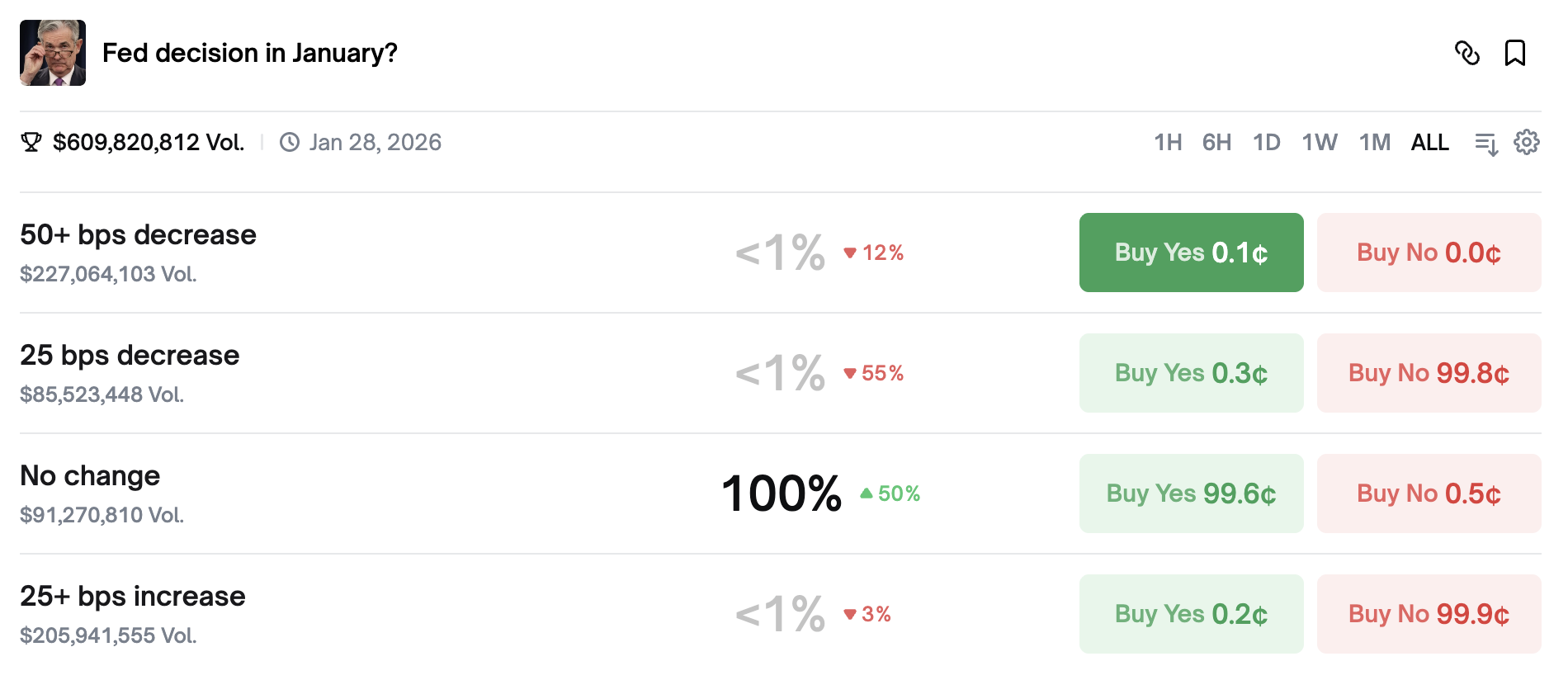

At 3:00 AM Beijing time on January 29 (this Thursday), the Federal Reserve is set to announce its first interest rate decision of 2026; half an hour later, current Fed Chair Jerome Powell will hold a monetary policy press conference. However, there is little suspense surrounding this Fed rate decision, as the market widely expects the Fed to keep rates unchanged. Data from Polymarket shows that the probability of maintaining rates is close to 100%.

Such a high probability has allowed the market to digest in advance the negative impact of the Fed's announcement of "no rate cut" this time. OKX data shows that BTC has fallen by only 0.39% in the past 7 days, basically in a sideways trend, but this period of market "silence" may be broken tonight.

On one hand, although the market almost unanimously believes the Fed will keep rates unchanged this week, there is significant divergence regarding the fiscal path for the remainder of 2026, making this still an important meeting to watch. The Fed's future key policy tendencies, such as whether it will continue to cut rates in 2026 and the frequency of cuts, will affect the market. Should Powell make hawkish remarks like "further observation is needed" during his speech, the market might "drop in response."

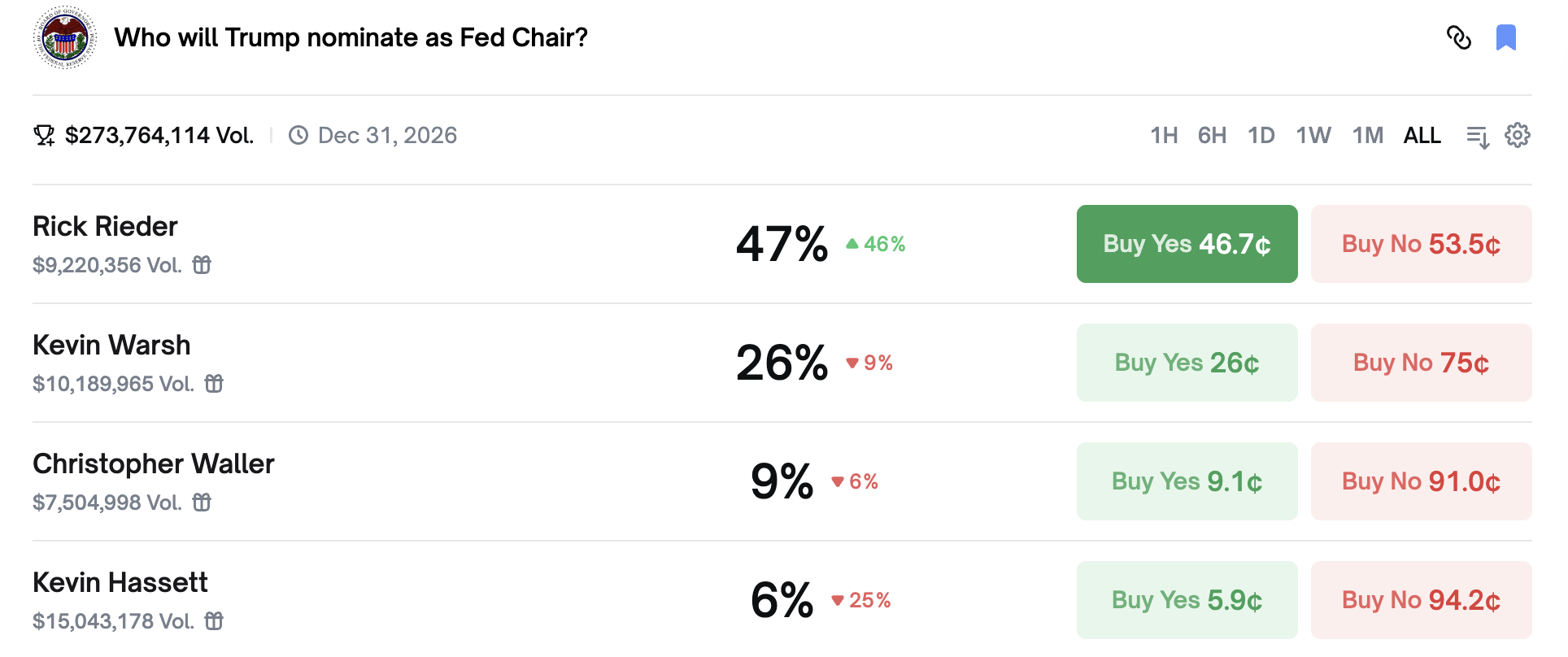

On the other hand, the announcement of the successor to the Fed Chair will also have a long-term impact on the market. The shortlist has been narrowed down to four individuals. Trump previously stated he has a preferred candidate but is waiting for the right time to announce, and this right time could very well be tonight.

2026 Rate Cut Direction Remains Uncertain

Since last September, the Federal Reserve initiated a new rate-cutting cycle, implementing three consecutive rate cuts. If rates are held unchanged this week, it would be the first pause since the cycle began. At this point, the market is not concerned about the reasons for holding rates steady, but rather whether this is a brief pause to observe before continuing rate cuts, or the beginning of a prolonged pause, or even the start of a rate-hiking cycle?

Previously, the general market view was that 2026 would be a year of further quantitative easing by the Fed.

Reason one: From a data perspective, the US labor market indeed shows signs of weakness. Non-farm payrolls increased by only 50,000 in December 2025, with an unemployment rate of 4.4%. While there hasn't been "massive layoffs," it remains in a state of "low hiring and cooling demand." Reason two: The Fed might still believe that Trump's tariff policies will not have a long-term impact on inflation (Odaily: Powell cut rates in September 2025 based on this factor). Reason three: Trump has publicly stated that he would choose a "dovish" figure as the next Fed Chair.

However, some in the market believe there is uncertainty about the Fed continuing to cut rates in 2026. Some analysts argue that unless the job market deteriorates significantly, it will be difficult to see rate cuts before mid-year, as the pace of inflation decline is not sufficient to convince hawkish members.

The Fed's mandate, simply put, is to curb inflation and promote employment. However, in 2025, the US experienced a phenomenon of both a weak labor market and high inflation. The Fed ultimately chose to prioritize the employment issue, thus initiating the rate-cutting cycle. Yet, the reality is that the US inflation rate remains stuck at 2.8%, far above the Fed's 2% target, forcing the Fed to reconsider the impact of tariffs on inflation. Holding rates unchanged this week would also indicate the Fed is beginning to "observe."

Furthermore, although the next Fed Chair chosen by Trump is destined to be "dovish," the new rotating chairs of the Fed's rate-setting committee are predominantly "hawkish." At the beginning of each year, four of the 12 regional Fed presidents rotate onto the rate-setting committee and gain voting rights for the next eight policy meetings. This year's rotating members include Dallas Fed President Lorie Logan, Cleveland Fed President Loretta Mester (referred to as Hammack in the text, likely a reference to Mester's previous role or a mistranslation; Mester is known as a hawk), Philadelphia Fed President Patrick Harker (referred to as Paulson in the text, likely a mistranslation; Harker is considered moderate), and Minneapolis Fed President Neel Kashkari.

Among them, Logan and Mester are seen as "hawkish" figures, both having publicly stated that the Fed should focus on inflation. Harker is seen as "dovish," having expressed a "cautiously optimistic attitude" towards inflation. Kashkari's stance is relatively neutral. The addition of new "hawkish" members might disrupt the previous balance of policy inclinations within the Fed. Even if Trump chooses a "dovish" Chair, they may not be able to sway the entire rate-setting committee.

Moreover, the Fed Chair might not completely follow Trump's wishes in leading rate cuts. Years ago, Trump personally appointed Powell as Fed Chair, but last year, even though Trump promoted Powell, Powell did not "repay" Trump with sustained and significant rate cuts. Under US law, the Fed is independent and can make interest rate decisions based on the current economic situation, not government wishes. Therefore, even if the new Fed Chair promises Trump rate cuts, they might "go their own way" once in office.

This kind of meaningless "political promise" is also a concern for Trump. Last week, Trump said in a speech at the World Economic Forum in Davos, Switzerland, "It's amazing how people change once they get this job," meaning candidates say what sounds good during the interview but emphasize their independence once confirmed.

Considering these factors, Powell's speech after tonight's FOMC meeting will also be closely watched by investors for hints on how long the Fed might pause rate cuts.

This Week's FOMC Meeting Could Be One of the Best Times for Trump to Announce the Fed Chair Successor

Besides this week's FOMC meeting, the successor to the Fed Chair is another macro event that can influence the market. The shortlist has been narrowed down to four: Kevin Hassett, Kevin Warsh, Rick Rieder, and Christopher Waller. According to Polymarket data, Rick Rieder currently has the highest probability of being nominated by Trump at 47%; Kevin Hassett has the lowest probability at 6%.

Rick Rieder is BlackRock's Chief Investment Officer of Global Fixed Income. Although he doesn't have much government experience, he has consistently advocated for supporting low interest rates based on his understanding of the market rather than politics. This resume might attract Trump, who is worried about the new Fed Chair becoming "disobedient" upon taking office. Economists at Evercore ISI, including Krishna Guha, even believe that "if Rick Rieder becomes the new Fed Chair, he might advocate for three rate cuts this year." (Odaily Note: For more information on Rick Rieder, read 《The Last Seat on the Fed Chair Candidate List, What is Rick Rieder's Attitude Towards Crypto?》)

Hassett was once considered the most likely candidate to become the new Fed Chair, with a probability一度 (once) over 80%. But Hassett is Trump's economic advisor, and there were外界 (external) concerns that nominating Hassett would damage the Fed's independence. Additionally, Trump publicly stated that he did not want to lose Hasset within his administration. Therefore, Hassett's probability of selection has declined, though some still believe his nomination probability is higher than 6%.

Trump has repeatedly publicly stated that he would announce his nominee in January. In late December 2025, Trump told reporters in Florida that he would announce the next Fed Chair人选 (candidate) sometime in January; On January 14, 2026, Trump said in an interview with Reuters that he would announce the candidate within the next few weeks; Two weeks later, on January 27, Trump said in a speech in Iowa that he would announce the new Fed Chair candidate soon, but has not done so yet.

Although Trump's answers have been vague each time, it is almost certain that the probability of an announcement in January is very high, and the best timing for the announcement could very well be during this week's FOMC meeting.

As mentioned earlier, Powell's speech tonight will be a key focus for investors. If Powell does not make dovish-leaning remarks, financial markets could suffer, a scenario Trump显然 (obviously) does not want to see. Therefore, if Trump wishes to shift market attention away from the uncertain Powell, he might announce his nominee for the next Fed Chair during tonight's FOMC meeting. This would release the positive news of a "dovish chair" to the market, reducing attention on Powell's speech or mitigating potential negative market impacts.

Tonight, let's wait and see!