Source: Artemis Analytics

Author: Mario Stefanidis

Original Title: Stablecoins Are a Rail, Not a Brand

Compiled and Edited by: BitpushNews

Stablecoins are permeating the traditional financial sector in an uneven yet undeniable manner.

Klarna just launched KlarnaUSD on Stripe's first-layer network Tempo, built specifically for payments; PayPal's PYUSD, issued on Ethereum, has seen its market cap triple in three months, breaking the 1% market share threshold for stablecoins, with its supply approaching $4 billion; Stripe has now begun using USDC to pay merchants; Cash App expanded its services from Bitcoin to stablecoins in early 2026, allowing its 58 million users to seamlessly send and receive stablecoins within their fiat balances.

Although each company approaches it from a different angle, they are all responding to the same trend: stablecoins make fund movement extremely simple.

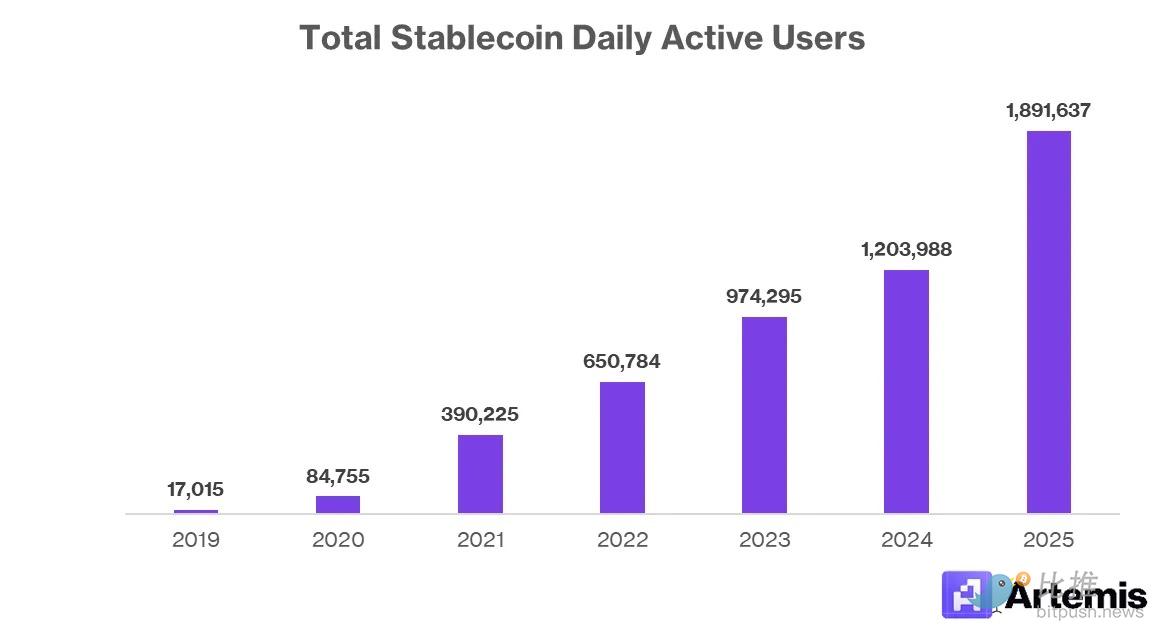

Data Source: Artemis Analytics

Market narratives often jump straight to "everyone will issue their own stablecoin." But this outcome is not logical. A world with dozens of widely used stablecoins is manageable, but if there are thousands, it will descend into chaos. Users do not want their dollars (yes, dollars, whose dominance exceeds 99%) scattered across a long tail of branded tokens, each on its own chain, with different liquidity, fees, and exchange paths. Market makers earn spreads, cross-chain bridges charge fees—this situation of multiple layers taking a 'cut' is precisely the problem stablecoins aim to solve.

Fortune 500 companies should realize that stablecoins are extremely useful, but issuing them is not a guaranteed win. A select few companies will be able to gain distribution channels, reduce costs, and strengthen their ecosystems. Many others may bear the operational burden without achieving a clear return.

The real competitive advantage comes from embedding stablecoins as a "payment rail" into products, not just slapping a brand label on a token.

Why Stablecoins Are Gaining Favor in Traditional Finance

Stablecoins solve specific operational problems for traditional companies that legacy payment rails have failed to address. The benefits are easy to understand: lower settlement costs, faster fund availability, broader cross-border reach, and fewer intermediaries. When a platform processes millions of transactions daily with an annual total payment volume (TPV) in the billions or even trillions, small improvements compound into significant economic benefits.

1. Lower Settlement Costs

Most consumer platforms accept card payments and pay interchange fees per transaction. In the US, these fees can be around 1%-3% of the transaction amount, plus a fixed per-transaction fee of approximately $0.10-$0.60 from the three major card networks (American Express, Visa, Mastercard). If payments remain on-chain, stablecoin settlement can reduce these fees to just a few cents. For companies with high transaction volumes and low profit margins, this is an extremely attractive lever. Note, they don't need to completely replace card payments with stablecoins; covering just a portion of the transaction volume can achieve cost savings.

Data Source: A16z Crypto

Some companies choose to partner with service providers like Stripe to accept stablecoin payments settled in dollars. While this is not a necessary step, most businesses want zero volatility and instant fiat settlement. Merchants typically want dollars to enter their bank accounts, not manage crypto custody, private keys, or handle reconciliation issues. Even the ~1.5% variable fee charged by Stripe is significantly lower than the credit card alternative.

One can imagine that large enterprises might initially partner with stablecoin processing solutions before weighing the capital expenditure to build fixed infrastructure in-house. Eventually, this trade-off will also become reasonable for SMBs hoping to retain almost all of the resulting economic benefits.

2. Global Reach

Stablecoins can move cross-border without negotiating with banks in every country. This advantage is attractive to consumer apps, marketplaces, gig platforms, and remittance products. Stablecoins allow them to reach users in markets where they haven't established financial relationships.

End-user foreign exchange (FX) fees for credit cards are typically an additional 1%-3% per transaction, unless using a card that doesn't charge such fees. Stablecoins charge no cross-border fees because their payment layer simply doesn't recognize national borders; USDC sent from a New York wallet arrives in Europe identically to a local send.

For a European merchant, the only additional step is deciding what to do with the received dollar-denominated asset. If they want euros in their bank account, they must perform an exchange. If they are willing to hold dollars on their balance sheet, no exchange is needed, and they might even earn yield if leaving the balance idle on an exchange like Coinbase.

3. Instant Settlement

Stablecoins settle in minutes, often seconds, whereas traditional payment transfers can take days. Furthermore, the former operates 24/7, unimpeded by bank holidays, cut-off times, and other inherent obstacles of the traditional banking system. Stablecoins remove these constraints, which can drastically reduce operational friction for companies processing high-frequency payments or managing tight working capital cycles.

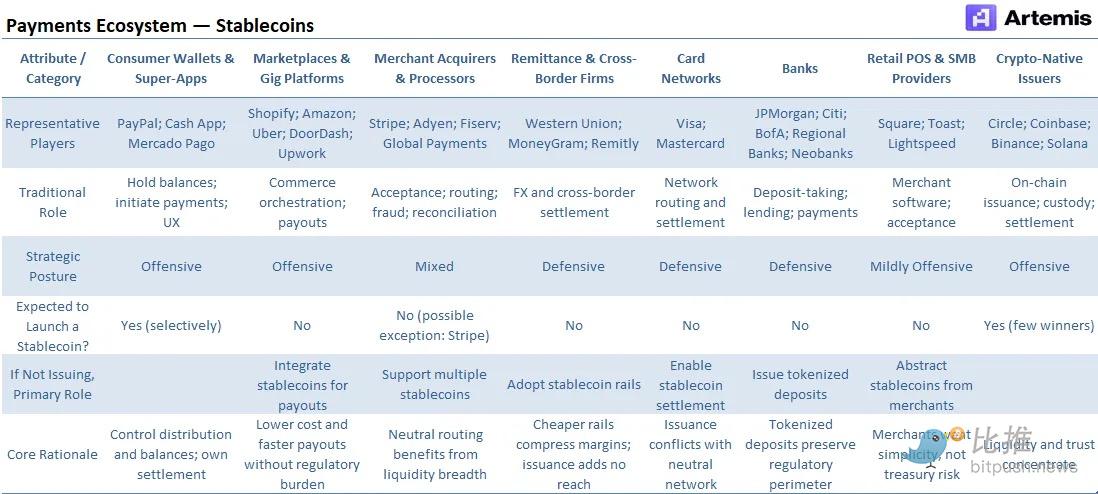

How Traditional Companies Should Approach Stablecoins

Stablecoins create both opportunities and pressures. Some companies can leverage them to expand product reach or reduce costs, while others may face erosion of part of their economics if users shift to cheaper or faster rails. The right strategy depends on a company's revenue model, geographic footprint, and how dependent its business is on legacy payment infrastructure.

Some companies benefit from adding a stablecoin rail because it strengthens their core product. Platforms already serving cross-border users can settle funds faster and avoid the friction of establishing relationships with local banks. If they process millions of transactions, they can lower settlement costs when payments remain on-chain.

Many large platforms operate on razor-thin transaction margins. If stablecoins allow a platform to bypass even 1-3 basis points of cost on a portion of the money flow, the savings will be substantial. On $1 trillion in annual TPV, a 1 basis point reduction is worth $100 million. Companies on the offensive primarily include fintech-native, capital-light payment rails like PayPal, Stripe, and Cash App.

Other companies adopt stablecoins because competitors might use them to bypass parts of their business model. For example, banks and custodians are highly exposed to stablecoins potentially taking share from traditional deposits, causing them to lose low-cost funding sources. Issuing tokenized deposits or offering custody services might provide them with an early line of defense against new entrants.

Stablecoins also lower the cost of cross-border remittances, meaning remittance businesses are at risk. Defensive adoption is more about preventing erosion of existing revenue than growth. Companies in the defensive camp are diverse, from Visa and Mastercard charging interchange fees and providing settlement services, to Western Union and MoneyGram on the remittance front lines, and banks of all sizes reliant on low-cost deposits.

Given that in payments, whether on offense or defense, adopting stablecoins too slowly could pose an existential threat, the question for Fortune 500 companies becomes: Does it make more sense to issue your own stablecoin or integrate existing tokens?

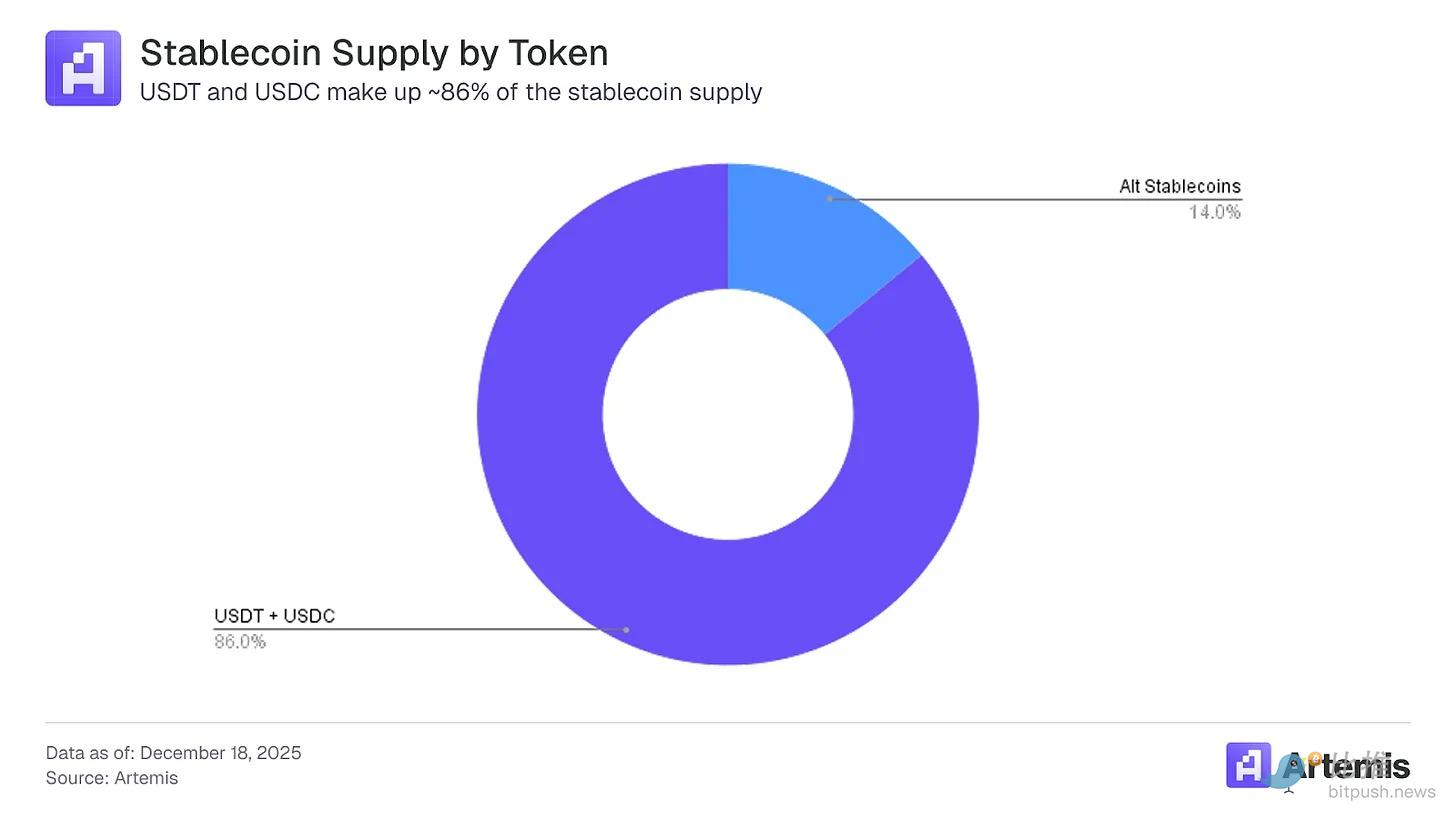

Data Source: Artemis Analytics

Every company issuing a stablecoin is not a sustainable equilibrium. Users want their stablecoin experience to be frictionless, and if they have to pick through dozens of branded tokens in their wallet, even if all are denominated in the same currency, they might prefer fiat instead.

Supply Trajectory

Companies should assume only a small subset of stablecoins will maintain deep liquidity and broad acceptance. However, this is not a "winner-take-all" industry. For example, Tether's USDT was the first fiat-backed stablecoin, debuting on Bitcoin's Omni Layer in October 2014. Despite competitors including Circle's USDC, launched in 2018, its dominance among stablecoins peaked in early 2024 at over 71%.

As of December 2025, USDT's dominance of the total stablecoin supply is 60%, with second-place USDC at 26%. This means alternatives control about 14% (~$43 billion) of the total ~$310 billion pie. While this sounds modest compared to multi-trillion dollar equity or fixed income markets, the total stablecoin supply has grown 11.5x from $26.9 billion in January 2021, with a 63% CAGR over the past five years.

Even at a more modest 40% annual growth rate, the stablecoin supply would reach ~$1.6 trillion by 2030, over five times its current value. 2025 was a pivotal year for the space, thanks to significant regulatory clarity from the GENIUS Act and massive institutional adoption driven by clear use cases.

By then, the combined dominance of USDT and USDC could also decline. At the current pace of ~50 basis points of dominance lost per quarter, other stablecoins could command ~25% of the space by 2030, which, based on our supply projection, is approximately $400 billion. This is a meaningful number, but clearly not enough to support dozens of Tether or USDC-sized tokens.

When there is clear product-market fit, adoption can happen rapidly, benefiting from the tailwind of broader stablecoin supply growth while potentially taking share from existing incumbents. Otherwise, a newly issued stablecoin risks getting lost in the "noise" of stablecoins with low supply and an unclear growth story.

Note, of the 90 stablecoins Artemis currently tracks, only 10 have a supply exceeding $1 billion.

Corporate Case Studies

Companies experimenting with stablecoins are not following a single playbook. Each is responding to pain points in its own business, and these differences are more important than the similarities.

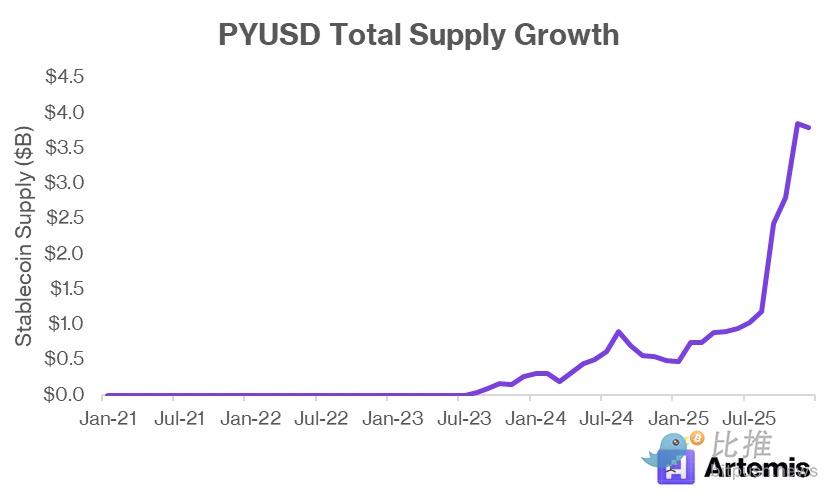

PayPal: Testing New Rails While Defending the Core Business

PYUSD is first a defensive product, second a growth product. PayPal's core business still runs on cards and bank transfers, which is where most of its revenue comes from. Branded checkout and cross-border transactions command noticeably higher rates.

Stablecoins threaten this stack by offering cheaper settlement and faster cross-border movement. PYUSD allows PayPal to participate in this shift without losing control of the user relationship. As of Q3 2025, the company reported 438 million active accounts—defined as users who transacted with the platform in the past 12 months.

PayPal already holds user balances, manages compliance, and operates a closed-loop ecosystem. Issuing a stablecoin fits naturally into this structure. The challenge is adoption, as PYUSD competes with USDC and USDT, which already have deeper liquidity and broader acceptance. PayPal's advantage is distribution, not price. PYUSD only works if PayPal can embed it into PayPal and Venmo workflows.

Data Source: Artemis Analytics

PYUSD is similar to Venmo; both are growth vehicles for PayPal, but not direct revenue generators. In 2025, Venmo will generate ~$1.7 billion in revenue, only about 5% of its parent company's total. However, the company is successfully monetizing through the Venmo Debit Card and "Pay with Venmo" products.

PYUSD currently offers users a 3.7% APY reward rate for holding the stablecoin in their PayPal or Venmo wallet, meaning PayPal is at best break-even from a net interest margin perspective (holding US Treasuries as collateral for the supply). The real opportunity is in the flow of funds, not the stock. If PYUSD reduces PayPal's reliance on external rails, lowers the settlement cost for some transactions, and keeps users inside the ecosystem rather than flowing off-platform, PayPal is a net beneficiary.

Furthermore, PYUSD supports defensive economics. The "disintermediation" risk from open stablecoins like USDC is real; by offering its own stablecoin, PayPal reduces the chance its services become an external layer that must be paid for or routed around.

Klarna: Reducing Payment Friction

Klarna's focus on stablecoins is about control and cost. As a buy-now, pay-later (BNPL) provider, Klarna sits between merchants, consumers, and card networks. It pays interchange and processing fees on both ends of a transaction. Stablecoins offer a way to compress these costs and simplify settlement.

Klarna helps consumers finance purchases over short and long terms. For payment plans spanning months, Klarna typically charges 3-6% of the transaction plus ~$0.30. This is the company's largest revenue source, compensating it for processing the payment, bearing credit risk, and increasing merchant sales. Klarna also offers longer installment plans (e.g., 6, 12, 24 months), where the interest it charges consumers resembles a credit card.

In both cases, Klarna's focus is not on becoming a payment network, but on managing internal flow of funds. If Klarna can settle with merchants faster and cheaper, it improves its margins and strengthens merchant relationships.

The risk is fragmentation—unless the Klarna-branded token is widely accepted outside its platform, there's little benefit to Klarna for users holding balances of it long-term. In short, for Klarna, a stablecoin is a tool, not a product.

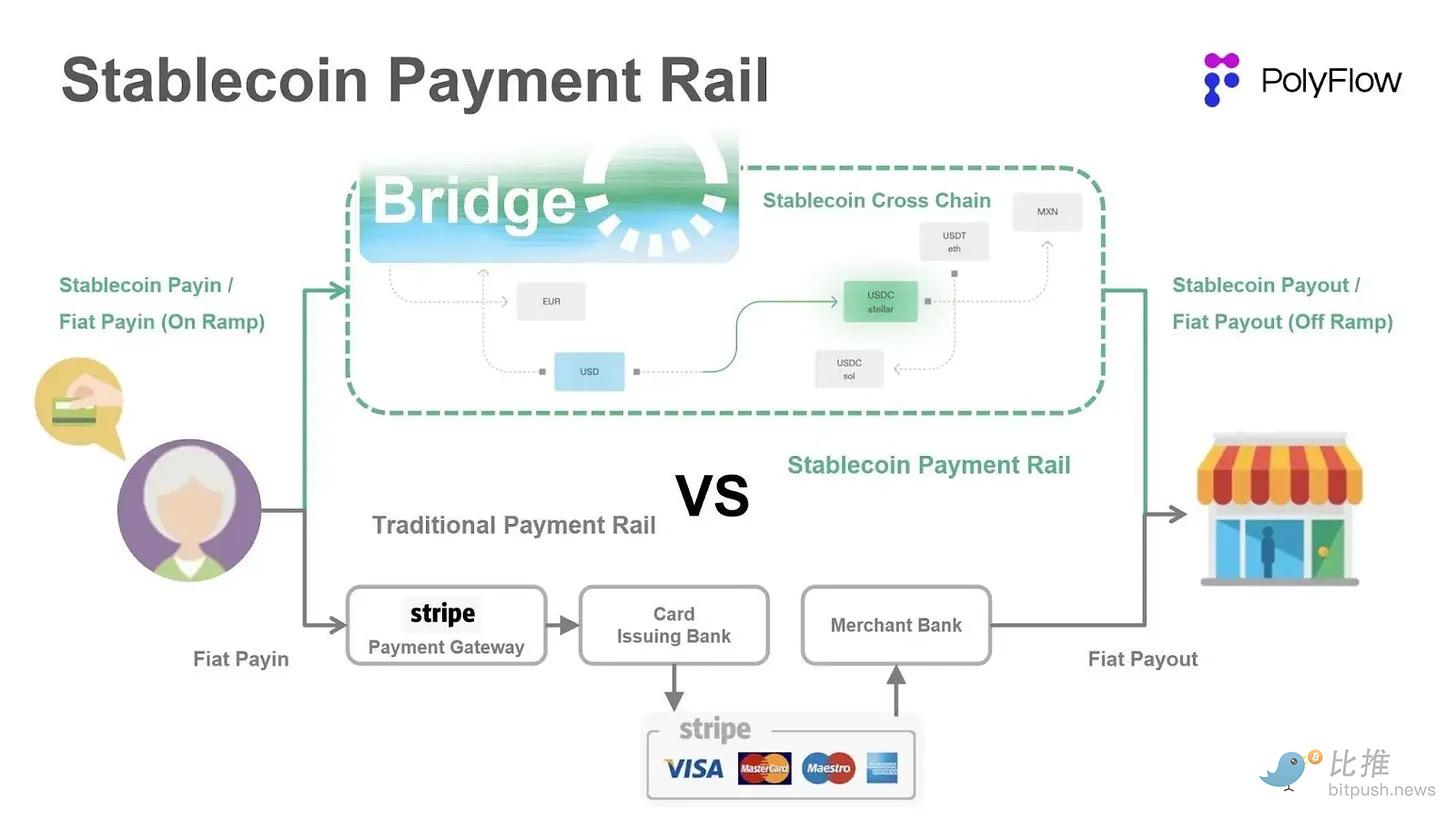

Stripe: Being the Settlement Layer, Not Issuing a Token

Stripe's approach is arguably the most disciplined. It has chosen not to issue a stablecoin, instead focusing on enabling payments and payouts using existing stablecoins. This distinction is important because Stripe doesn't need to win on liquidity, it needs to win on flow.

Stripe's TPV grew 38% year-over-year in 2024 to $1.4 trillion; at this rate, the platform could surpass PayPal's $1.8 trillion TPV despite being founded a decade later. The company's recently reported $106.7 billion valuation reflects this growth.

The company's support for stablecoin payments reflects clear customer demand. Merchants want faster settlement, fewer banking restrictions, and global reach. Stablecoins solve these problems. By supporting assets like USDC, Stripe improves its product without requiring merchants to manage another balance or take on issuer risk.

The acquisition of Bridge Network earlier this year for $1.1 billion cemented this strategy. Bridge focuses on stablecoin-native payment infrastructure, including on/off ramps, compliance tools, and global settlement rails. Stripe acquired Bridge not to issue a token—but to internalize the plumbing. This move gives Stripe more control over its stablecoin strategy and improves integration with existing merchant workflows.

Data Source: PolyFlow

Stripe wins by being the interface to stablecoins. Its strategy reflects its market position, processing trillions in TPV and maintaining double-digit annual growth. Stripe remains agnostic and charges per transaction, regardless of which token dominates. Given the extremely low underlying stablecoin transaction cost, any fixed fee Stripe can charge in this new market pads its profits.

The Merchant Pain Point: Simplicity is King

Merchants care about stablecoins for a simple reason: getting paid is expensive, and those costs are visible.

In 2024, US merchants paid $187.2 billion in processing costs to accept $11.9 trillion in customer payments. For many SMBs, these fees are the third-largest operating expense after labor and rent. Stablecoins offer a viable path to alleviating this burden for specific use cases.

Beyond lower fees, stablecoins offer predictable settlement and faster access to funds. On-chain transactions provide finality, whereas credit card or traditional payment processing solutions can have chargebacks or disputes. Merchants also don't want to hold cryptocurrency or manage wallets, which is why early pilots look like "stablecoins in, dollars out."

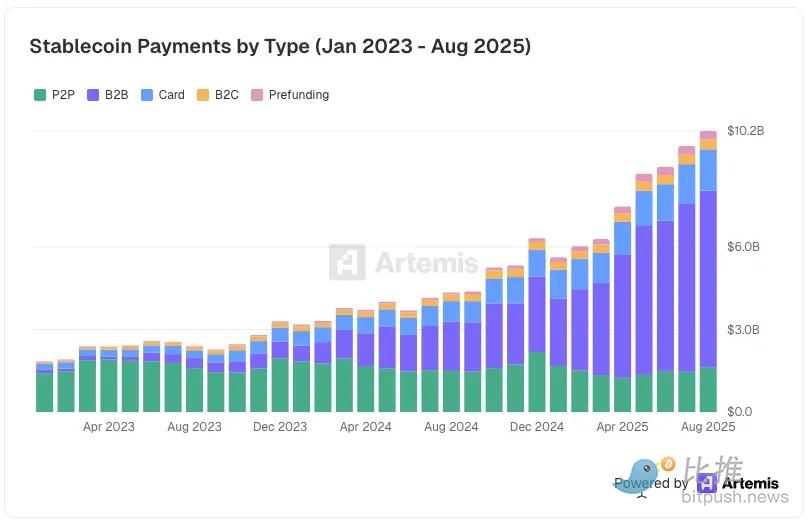

According to Artemis's latest survey in August 2025, merchants are already processing $6.4 billion in B2B stablecoin payments, 10x the volume processed in December 2023.

Data Source: Artemis Analytics

This dynamic also explains why merchant adoption will consolidate quickly. Merchants don't want to support dozens of tokens, each with different liquidity profiles, conversion costs, and operational characteristics. Each additional stablecoin introduces complexity and reconciliation challenges from market makers or bridges, which erodes the initial value proposition.

Consequently, merchant adoption favors stablecoins with clear product-market fit. Stablecoins lacking features that make transacting easier than fiat will fade away. From a merchant's perspective, accepting a long-tail stablecoin offers no significant advantage over accepting none at all.

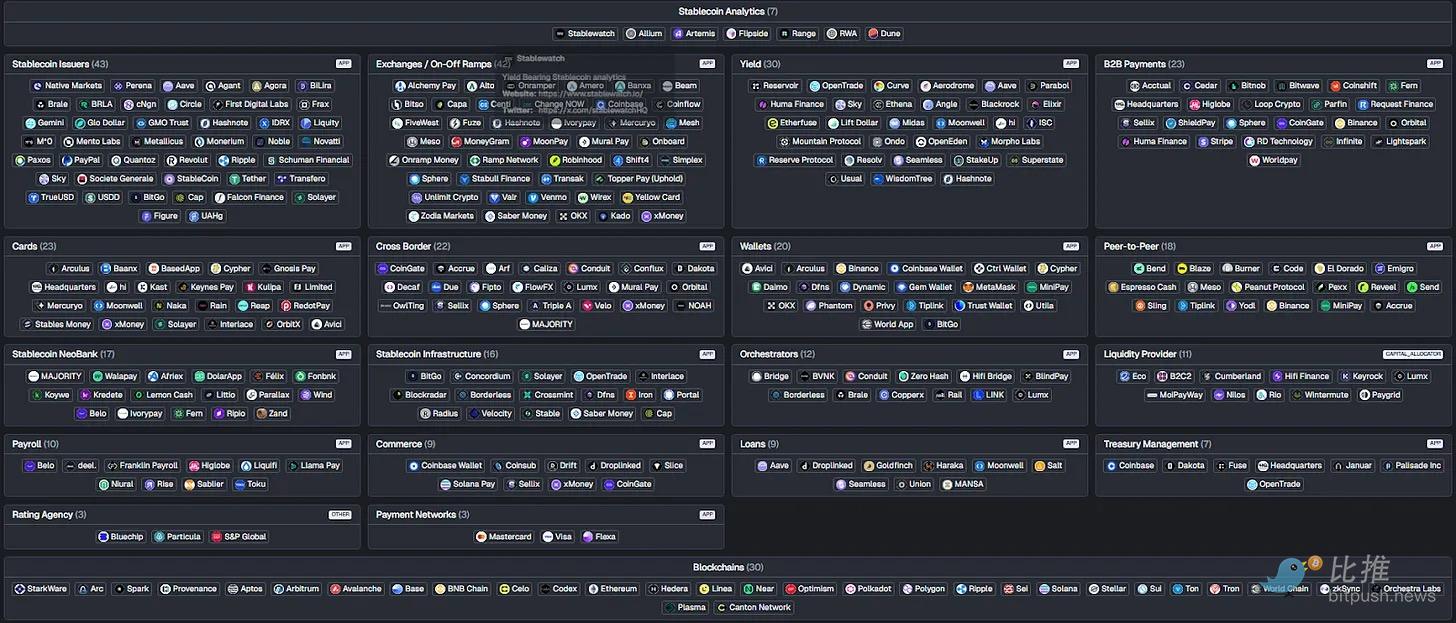

The Artemis Stablecoin Map shows just how messy the current landscape is. Merchants simply won't juggle dozens of on/off ramps, wallets, and infrastructure providers just to convert revenue into fiat.

Merchants reinforce this outcome by standardizing on what works. Processors reinforce this by only supporting assets their customers actually use. Over time, the ecosystem will aggregate around a limited number of tokens worth the integration cost.

Why This Actually Matters

The implication of all this is unsettling for a large part of the stablecoin ecosystem: mere "issuance" is not a durable business model.

A company whose primary product is "we mint stablecoins" is betting that liquidity, distribution, and usage will materialize naturally. In reality, these things only appear when a token is embedded into real payment flows. The "if you build it, they will come" mentality doesn't apply here because consumers face a choice among hundreds of issuers.

This is why issuance-only companies like Agora or M0 will struggle to justify their long-term edge unless they expand their business far beyond minting. Without controlling a wallet, merchant, platform, or settlement rail, they are downstream of the value they are trying to capture. If users can just as easily hold USDC or USDT, there's no reason for liquidity to fragment into another branded dollar token.

In contrast, companies that control distribution, flow, or integration points become stronger. Stripe benefits without issuing a stablecoin; it sits directly in the path of merchant settlement and earns revenue regardless of which token dominates. PayPal can justify PYUSD because it owns the wallet, user relationship, and checkout experience. Cash App can integrate stablecoins because it already aggregates balances and controls the UX. These companies get leverage from usage.

The real takeaway is that if you are upstream in the stack with nothing but a bare token, you are in a market destined for high consolidation.

Stablecoins reward your position in the architecture, not novelty.

Conclusion

Stablecoins change how money moves, not what money is. Their value stems from reducing settlement friction, not from creating new financial instruments. This fundamental distinction explains why stablecoin adoption is happening inside existing platforms, not parallel to them. Enterprises leverage stablecoins to optimize existing business processes, not disrupt their business models.

This also explains why issuing a stablecoin should not be the default choice. Liquidity, acceptance, and integration capabilities are far more important than brand. Without sustained use cases and clear demand, new tokens only add operational burden rather than create advantage. For most companies, integrating existing stablecoins is more scalable than issuing their own—the market naturally favors a few assets that work everywhere over many that work in narrow contexts. Before minting a stablecoin doomed to fail, one must define its offensive or defensive strategic positioning.

Merchant behavior further reinforces this trend. Merchants always pursue simplicity and reliability. They will only adopt payment methods that reduce costs without adding complexity. Stablecoins that seamlessly embed into existing workflows will be favored; those requiring extra reconciliation, conversion steps, or wallet management will be weeded out. Over time, the ecosystem will filter and settle on a handful of stablecoins with clear product-market fit.

In payments, simplicity determines ubiquity. The stablecoins that make moving money easier will survive; the rest will be forgotten.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush