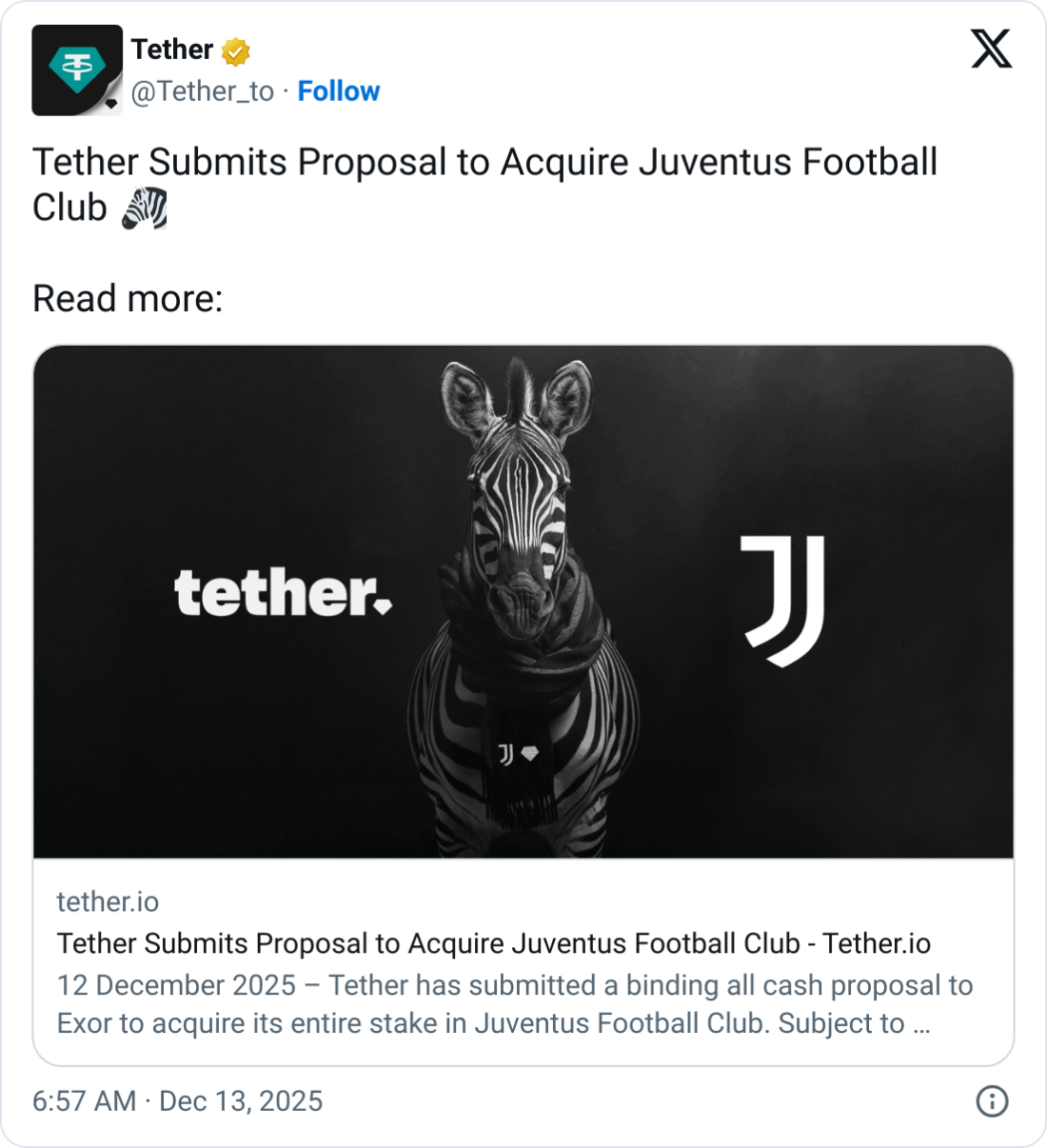

Crypto stablecoin issuer Tether says it has launched a bid to fully acquire the Italian professional soccer club, Juventus Football Club, which has reportedly already been shot down.

Tether said on Friday that it submitted a binding all-cash proposal to Exor, the holding company of the Agnelli family, for its 65.4% controlling stake in Juventus that it has held for over 100 years.

If Exor agrees, then Tether will make a “public offer for the remaining shares at the same price.” Juventus is a public company with a market capitalization of 944.49 million euros ($1.1 billion), having closed trading on Friday up 2.3% to 2.23 euros ($2.62).

However, AFP reported that Tether’s bid has already been rebuffed, with a source close to Exor saying that “Juventus is not for sale.” Exor and Tether did not immediately respond to Cointelegraph’s request for comment.

Tether promises $1.1 billion investment

Tether said it’s prepared to invest 1 billion euros ($1.1 billion) in the support and development of Juventus if the transaction completes.

“Tether is in a position of strong financial health and intends to support Juventus with stable capital and a long horizon,” said Tether CEO Paolo Ardoino.

“For me, Juventus has always been part of my life,” Ardoino added. “I grew up with this team. As a boy, I learned what commitment, resilience, and responsibility meant by watching Juventus face success and adversity with dignity.”

Related: Major fantasy sports operator enters prediction markets with Polymarket

Tether, which issues the self-named stablecoin Tether (USDT), has looked to expand its business beyond the token and has taken up investing in artificial intelligence, robotics and a health platform.

The company first bought a stake in Juventus in February and boosted its stake to over 10% in April.

It has since looked to boost its influence on the club and, in October, nominated its deputy investment chief, Zachary Lyons, along with Francesco Garino, to the football club’s board of directors.

The bids have paid off, as Juventus shareholders approved Garino’s appointment to the board of directors last month.

Magazine: Peter McCormack’s Real Bedford Football Club puts Bitcoin on the map