Original | Odaily Planet Daily (@OdailyChina)

Author | Azuma (@azuma_eth)

Iran has become the focus of the world.

On February 28, the United States and Israel jointly launched a large-scale military strike against Iran. About 30 targets within Iran, including the Iranian presidential palace, were attacked. Iran's Supreme Leader Khamenei was confirmed to have died in the attack.

In this attack, prediction markets once again demonstrated their intelligence value distinct from traditional channels. Hours before the airstrike occurred, the probability in related markets around "whether the U.S. military would attack Iran" had significantly increased, and heavy betting by new addresses was also monitored on-chain — in such globally watched public incidents, the fluctuations of prediction markets once again outpaced the reports of mainstream media.

This should have been another moment for prediction markets to declare victory after the 2024 presidential election, but Khamenei's death has plunged the industry into a major discussion about ethical boundaries.

Does Death Count as Stepping Down?

From a micro perspective, the focus of the contradiction lies in the event of "whether Khamenei will step down as Iran's Supreme Leader." As the most watched dynamic in the Iranian situation, leading platforms such as Kalshi and Polymarket had long provided betting options for related events on their platforms. However, the manner (or rather the speed) in which Khamenei ended his rule clearly took people by surprise.

After Khamenei's death was confirmed, Kalshi CEO Tarek Mansour was the first to express opposition to profiting from individual deaths on social media. "We do not list markets that are directly linked to death. When a market might result in death, we design rules to prevent people from profiting from death."

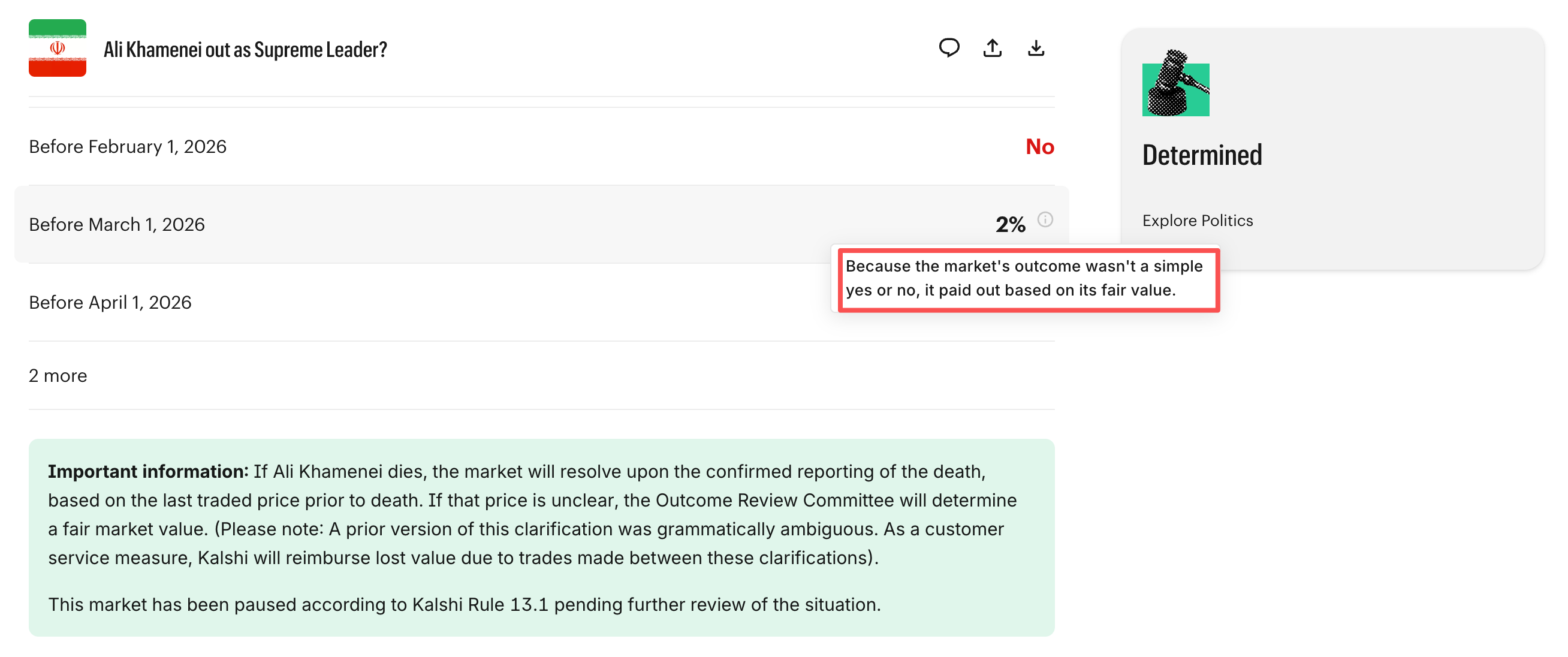

Given that death is now a fait accompli, Kalshi will handle the event related to "Khamenei stepping down as Supreme Leader" as follows:

- Refund all handling fees for this market;

- The market will be settled based on the last trading price before the confirmation of Khamenei's death. All positions, regardless of when they were opened, will be settled at this price;

- If users built positions after Khamenei's death, Kalshi will fully compensate for the price difference cost.

Opening the homepage of the related event on Kalshi shows that the event has been suspended by Kalshi and specially marked. Kalshi also noted that "because the market outcome is not a simple YES or NO, it is settled based on its fair value."

Kalshi's approach has sparked intense discussion in the community.

- Those supporting Kalshi believe that avoiding events related to "death" aligns with mainstream values and the constraints of regulations on commodity contracts (the regulatory system prediction market events currently fall under). Especially considering that prediction markets have shown a certain reactive force on the real world, if boundaries are not set, over time, betting could indirectly incentivize "physical harm or murder," causing prediction markets to gradually become darknet-like.

- Those opposing Kalshi believe that this move undermines the original transactional fairness of prediction markets and also damages their hedging value against real-world sudden changes — those who bet YES did not get the expected returns; although Tarek Mansour claimed that "not a single user will lose even $1 in this market," in reality, those who had bet NO and cut losses early cannot receive corresponding compensation.

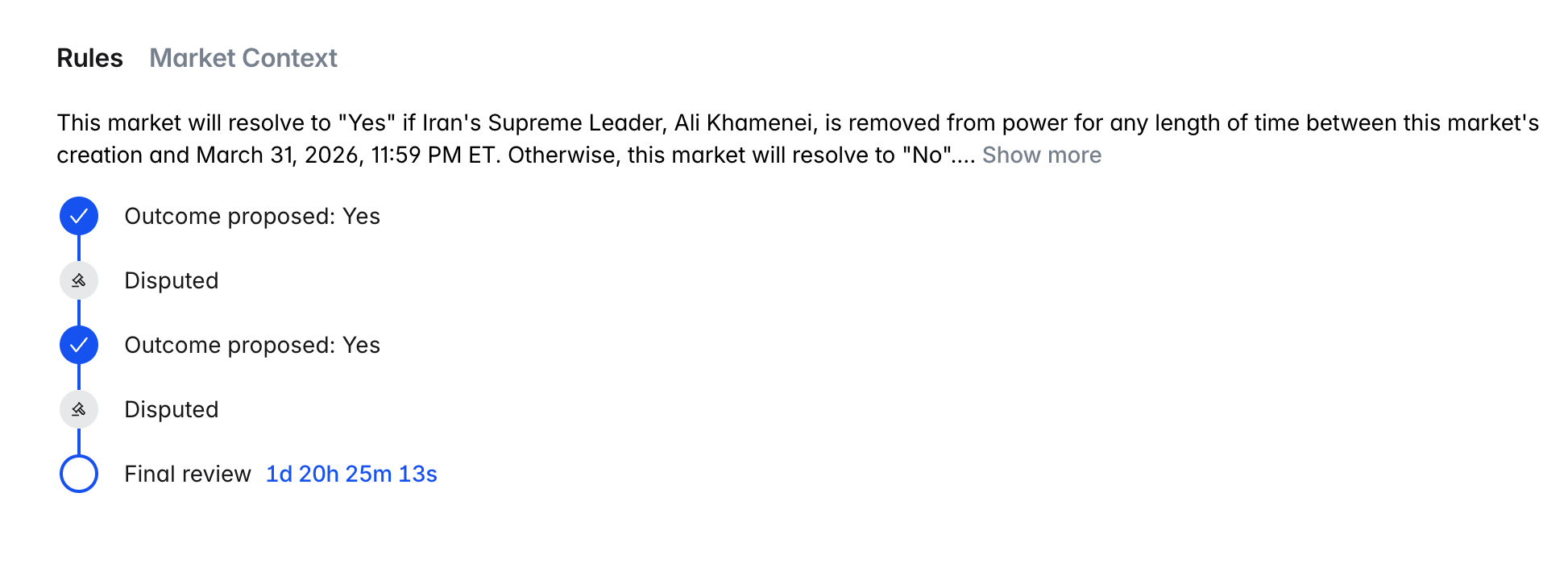

In contrast, Polymarket has not made any statement on this matter, and the event can still be traded normally. The current price for YES shares for stepping down before March 31 is temporarily quoted at 99.9 cents, and NO at 0.2 cents.

In the judgment rules for this event, Polymarket has stated that "if Khamenei resigns, is detained, or otherwise loses his position or is unable to perform his duties as Supreme Leader of Iran within the time specified by this market, it will be considered removal from office," which seems to cover the unexpected death situation. However, disagreements have still arisen in the settlement process of this event — clearly, there are also divisions within the community.

- Odaily Note: For details on Polymarket's adjudication mechanism and the handling process in case of disputes, please refer to "Who 'Defines the Facts'? The Truth About Power and the Space for Malice in Polymarket's Adjudication Mechanism."

Calls for Bans from the Regulatory Side

The debate over whether prediction markets should list events related to "individual death" had already been discussed on the regulatory side days before Khamenei's death drew widespread industry attention.

On February 24, just a few days before the end of Khamenei's life, six U.S. Democratic senators, including Adam Schiff, jointly sent a letter to U.S. Commodity Futures Trading Commission (CFTC) Chairman Michael Selig, requesting that the CFTC categorically prohibit any prediction market contracts that use individual death as a settlement condition or are highly related to individual death.

The legal basis cited in the letter is that according to federal commodity regulations, the CFTC has already "categorically prohibited" contracts involving or referring to terrorism, assassination, war, or similar acts.

Adam Schiff and others stated that such events would create incentives for "physical harm or even death," even constituting a "dangerous national security risk" — "These contracts could incentivize real-world harm because they establish economic reward mechanisms for turbulent events or physical injury and encourage actors to influence or bring about these outcomes for personal gain."

The CFTC did not immediately publicly respond to the letter. A few days later, the news of Khamenei's death quickly made headlines in major media outlets, and Kalshi and Polymarket were plunged into a whirlpool of public opinion before regulators had made a clear stance.

Free Market vs. Social Responsibility

Prediction markets offer a new path to glimpse the probability of future events using market mechanisms, but this does not mean prediction markets are necessarily suitable for all events.

From the perspective of the prediction market's own operation, platforms tend to prefer listing events with clearly defined outcomes that are not easily manipulated by single points to avoid陷入条款解释或公平性争议陷入 (falling into disputes over clause interpretation or fairness); 而从外部影响以及监管压力来看,预测市场则需要尽量避开不符合主流价值观的事件 (from the perspective of external influence and regulatory pressure, prediction markets need to try to avoid events that do not conform to mainstream values) — if the setup of the prediction market itself could lead people to disrupt social order or harm others for profit, then it easily faces ethical and legal challenges.

The controversy over whether "death" related events should be banned is essentially a divergence in倾向 (inclination) towards free markets versus social responsibility. Those emphasizing free markets value the unique advantage of prediction markets in pricing future events more and are unwilling to compromise this ability due to any external restrictions; those valuing social responsibility worry that excessive laissez-faire could gradually evolve into a harm to public interest and social stability. This divergence has a universal solution: as friction emerges and deepens, both sides will gradually find a suitable balance point through struggle and concession.

Like every emerging industry, the regulatory details and industry self-discipline of prediction markets will not materialize out of thin air. The future of the industry will be shaped by participants, regulators, and society together. The path is walked by people. Khamenei's death is pushing prediction markets to personally step out the ethical boundaries.