In a surprising shift, Polymarket has moved beyond simply hosting bets on future events and is now working to build the full infrastructure behind those wagers.

According to reports, Polymarket has acquired Brahma, a company specializing in crypto and DeFi infrastructure. This means Polymarket wants better technology to make its platform faster, smoother, and more on-chain.

Polymarket has grown rapidly, now valued at an estimated $18–20 billion, boosted by heavy activity during the 2024 elections. Yet with that growth come new challenges.

What is Polymarket trying to revamp with Brahma?

One of the core problems is liquidity imbalance. This means popular wagers, like elections or major sports events, attract a lot of money and activity.

Whereas, smaller or niche wagers struggle because not enough people are betting on them. That makes prices less reliable and the markets less useful.

Citing examples, Fortune added,

Larger event contracts, like those in sports or politics, easily bring lots of money into the pool. But smaller wagers focused on niche areas such as, for instance, the outcome of a bowling match in Spain, struggle to amass a sizable amount of liquidity.

Therefore, by acquiring Brahma, Polymarket is trying to fix this by improving how liquidity is distributed across markets. The plan also focuses on making trading more efficient and strengthening its blockchain-based system.

Remarking on this initiative, Shayne Coplan, founder and CEO of Polymarket, told Fortune,

Building reliable infrastructure across blockchain networks and traditional financial rails is hard—there are no shortcuts.

That said, Brahma, founded in 2021, has already processed over $1 billion in transactions, and by bringing its team in-house, Polymarket is effectively shutting down Brahma’s external operations to focus entirely on its growth.

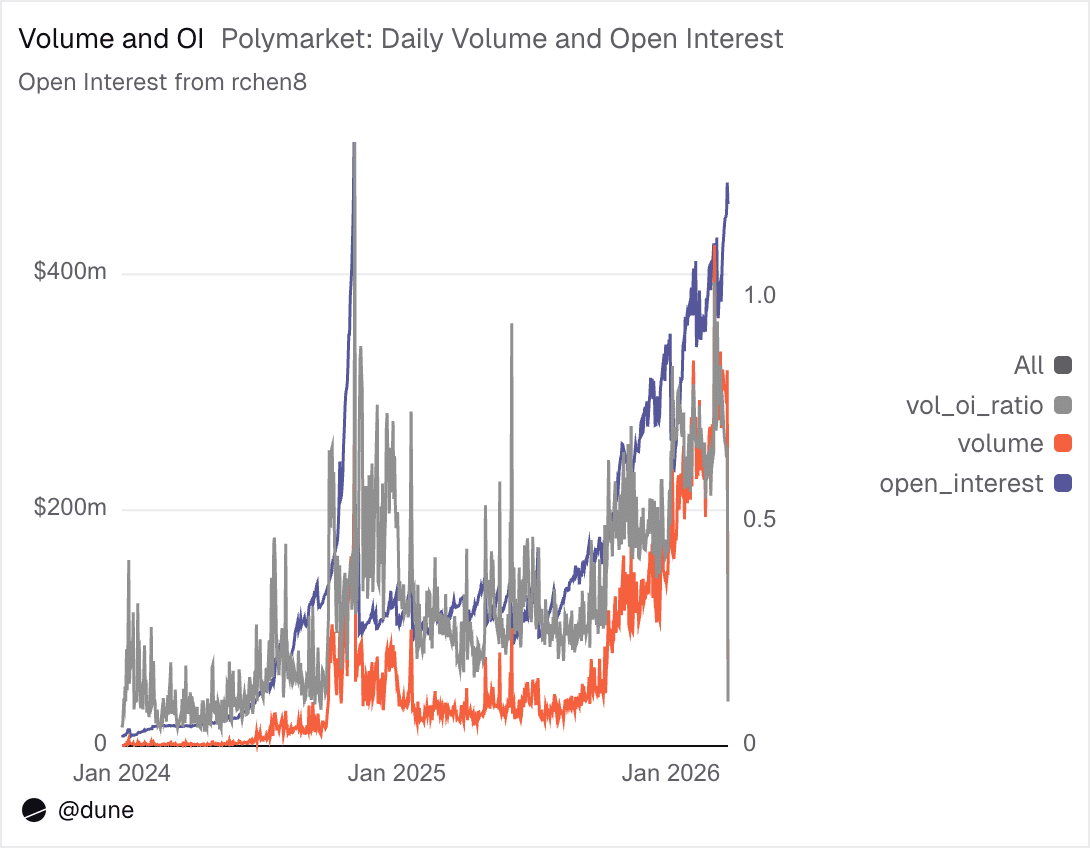

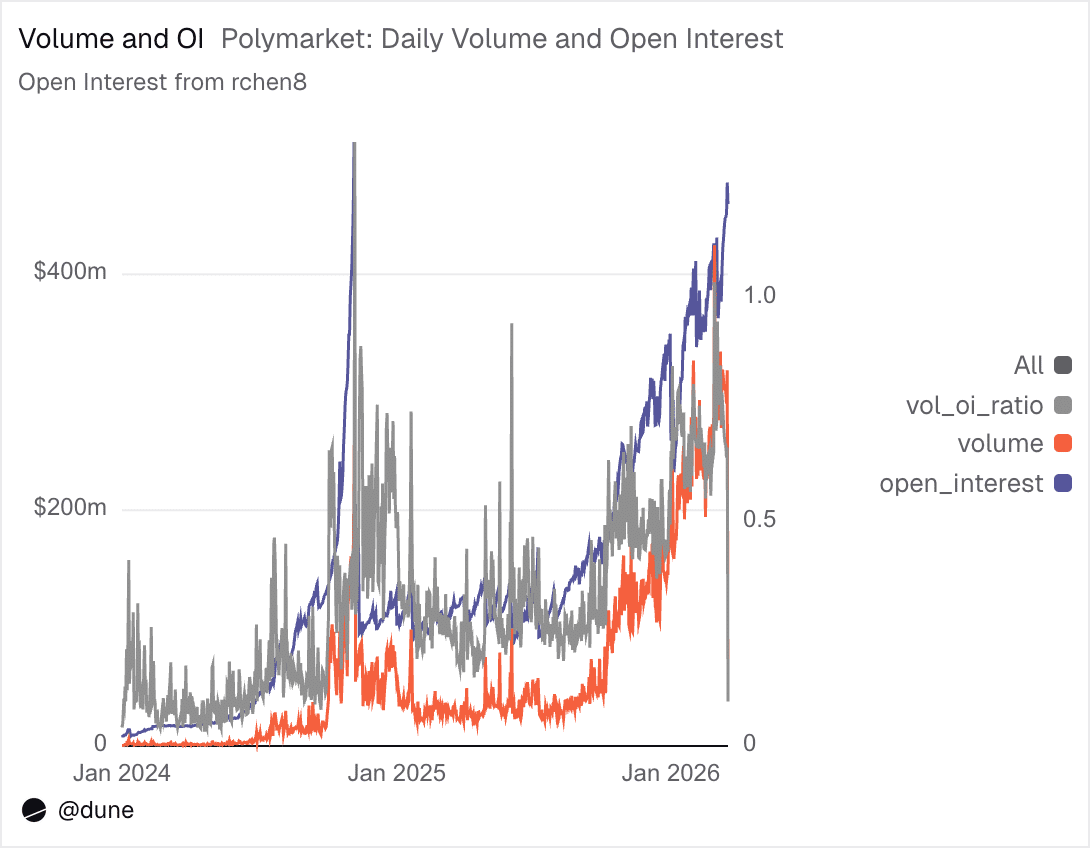

Polymarket’s metrics paint a confusing picture

However, the platform’s internal data suggests that growth is not entirely balanced. While more capital is flowing into the system, as seen in the steady rise in Open Interest, actual trading activity remains inconsistent.

This gap shows that users place long-term bets but trade inconsistently, resulting in low liquidity and one-sided markets.

Even though the platform became very popular during the 2024 election cycle, its dominance didn’t last. Its market share dropped sharply from over 61% to around 32% as the hype faded. However, at press time, Polymarket’s stock price stood at $141.60, marking a more than 20% increase year-to-date.

Is Polymarket losing ground against Kalshi?

In fact, during the 2024 election, its U.S.-based competitor Kalshi took advantage of the slowdown, briefly capturing about 66% market share and handling nearly $1 billion in weekly trading volume.

This competition reflects two very different paths. Kalshi follows a fully regulated approach with no blockchain, DeFi, or token layer.

Polymarket, in contrast, is doubling down on crypto. Besides Brahma, the platform’s CEO is also hinting at a potential POLY token. With a possible 2026 launch, it acts as a strong incentive for users, something regulated platforms like Kalshi are struggling to offer.

Final Summary

- The Brahma acquisition shows that fixing liquidity and market efficiency is now more important than just attracting users.

- Competition from regulated players like Kalshi adds pressure, especially as they gain ground during periods of low hype.