The 2026 FIFA World Cup is set to kick off on June 11th. For a long time, a theory known as the "World Cup Curse" has circulated in the market, suggesting that during World Cup tournaments, major global stock markets often perform weakly, with trading volume significantly shrinking.

Whether you're ready with beer and peanuts to enjoy the matches or plan to trade in the market while watching, we can examine whether the "World Cup Curse" is a real phenomenon. What lies behind the data, and what are the reasons for this observed phenomenon?

Examining the "World Cup Curse" Through Data

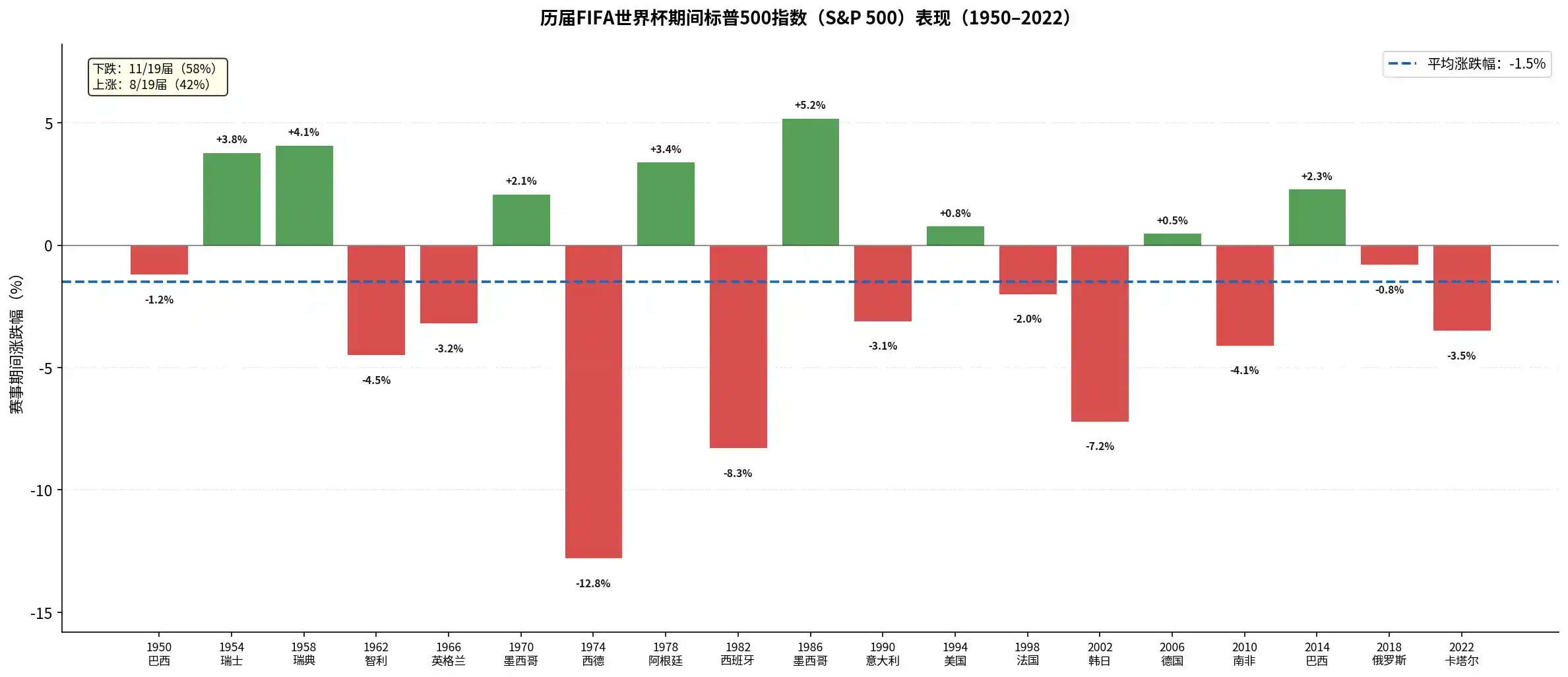

Looking at historical data, the performance of major global stock markets during World Cup periods has generally been poor. Taking the US S&P 500 Index as an example, during the 19 World Cup tournaments from 1950 to 2022, the S&P 500's average expected return during the events was approximately -1.5% to -2.11%.

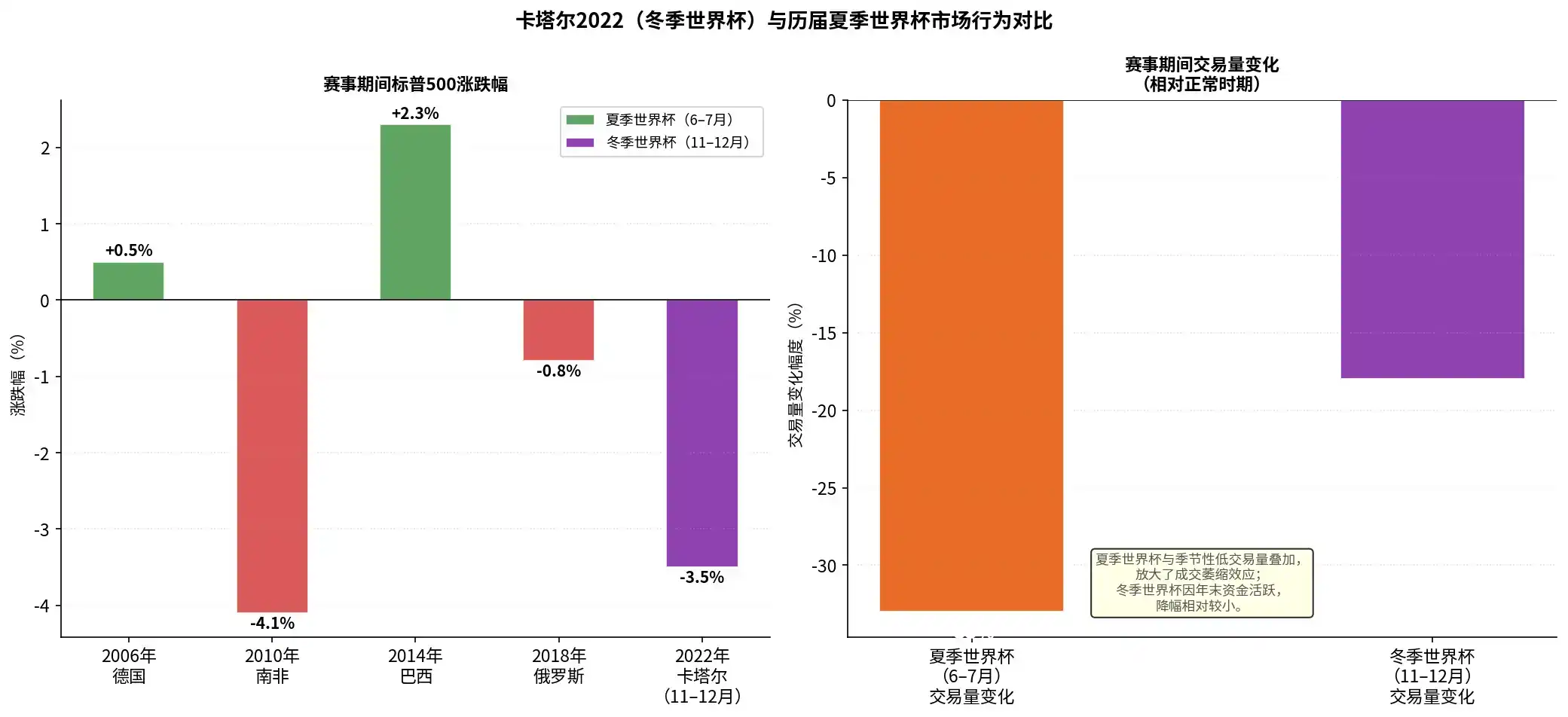

As shown in the chart above, the S&P 500 recorded negative returns in 11 out of the past 19 World Cups (a 58% rate). Notably, in recent years, US stocks declined during the 2010 South Africa World Cup (-4.1%), the 2018 Russia World Cup (-0.8%), and the 2022 Qatar World Cup (-3.5%).

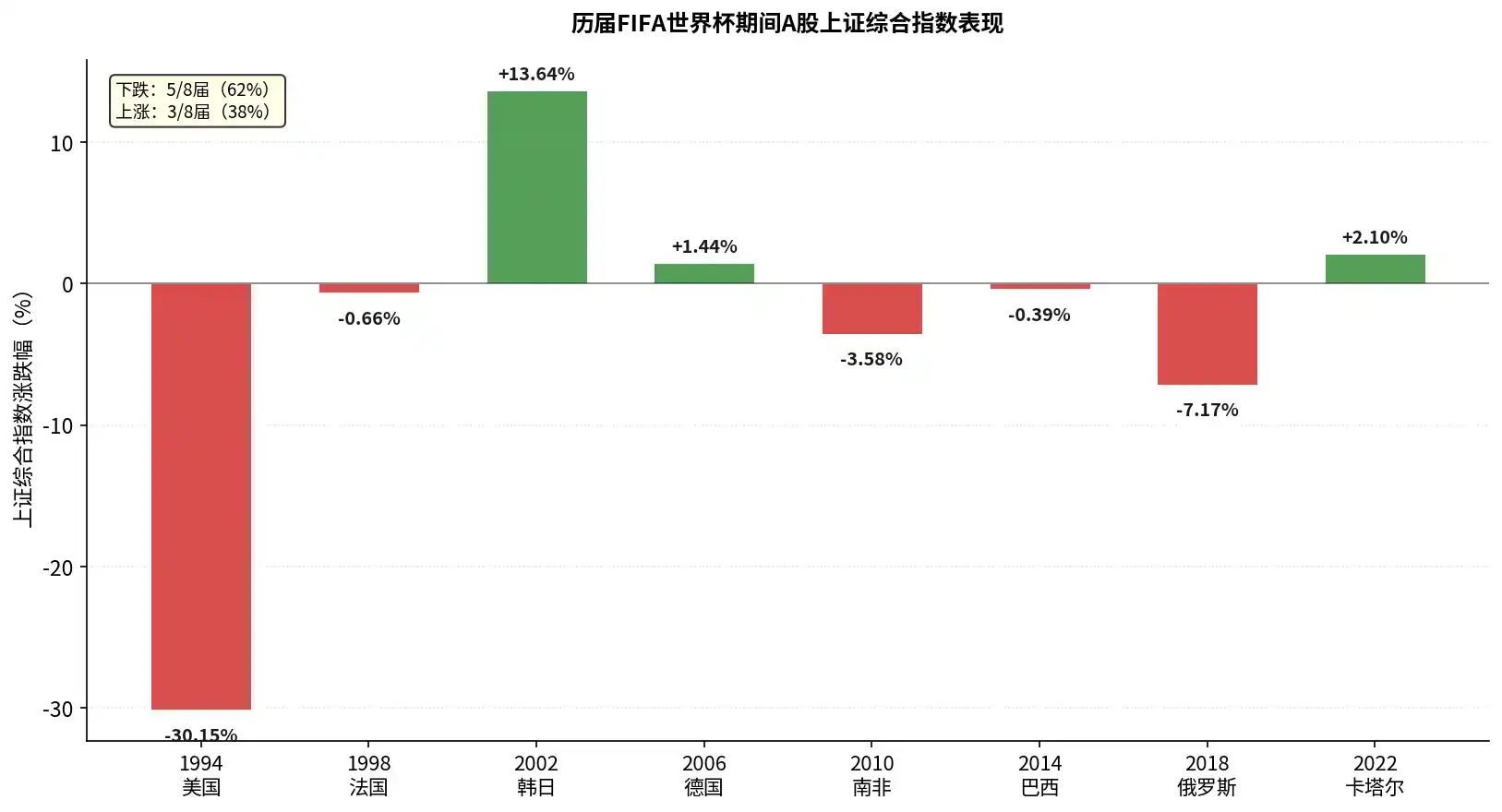

The A-share market has not been spared either. Statistics show that in the 7 World Cup periods since 1994, the Shanghai Composite Index fell 5 times, a decline probability as high as 71%. Among them, the index plunged 30.15% during the 1994 US World Cup and fell 7.17% during the 2018 Russia World Cup. It only posted gains during the 2002 World Cup (stimulated by favorable policies) and the 2006 World Cup (during a super bull market).

Now let's look at the cryptocurrency market:

- 2010 South Africa World Cup period: rose about 15%

- 2014 Brazil World Cup period: fell about 7.1%

- 2018 Russia World Cup period: fell about 16.5%

- 2022 Qatar World Cup period: rose about 4.3%

With the data presented, let's analyze the reasons.

Causes of the "World Cup Curse"

Does the World Cup really have a significant impact on market performance? It has an impact, but not a major one.

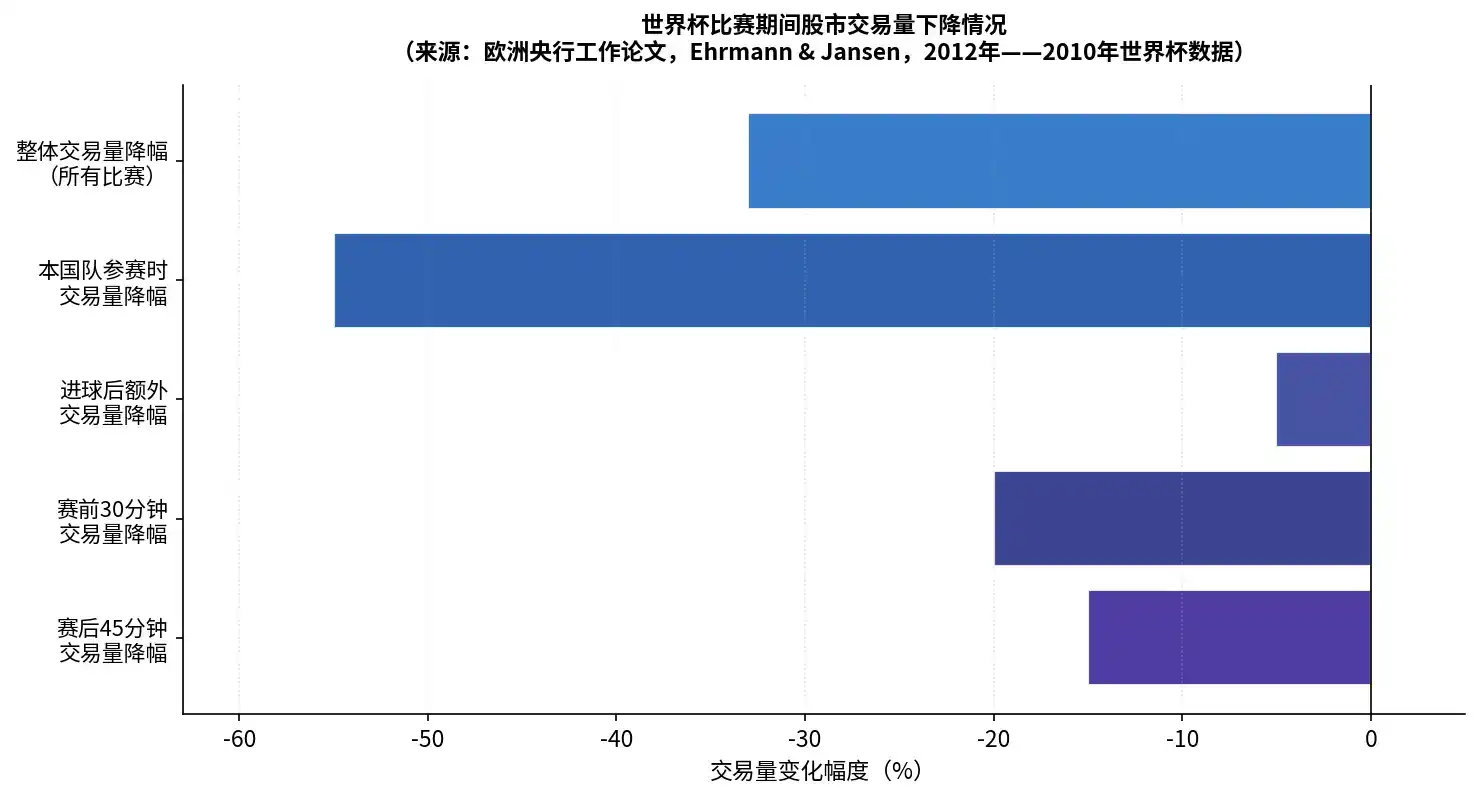

First, looking at the impactful part. A paper from the European Central Bank (ECB) analyzed minute-level trading data from 15 international stock exchanges during the 2010 World Cup. The study found that stock market trading activity indeed decreased during World Cup matches:

- Overall trading volume dropped by about 33% compared to normal levels.

- When the home country's national team was playing, trading volume plummeted by 55%, and the number of trades fell by 45%.

- Key events in matches (like goals) led to a further 5% drop in trading volume.

Match results also affect the mood of fans in various countries. Research found that when a country's national team lost a World Cup match, that country's stock market often showed significant negative abnormal returns on the next trading day (up to 49 basis points). This negative sentiment from a match loss does spill over into investment decisions, leading to market sell-offs.

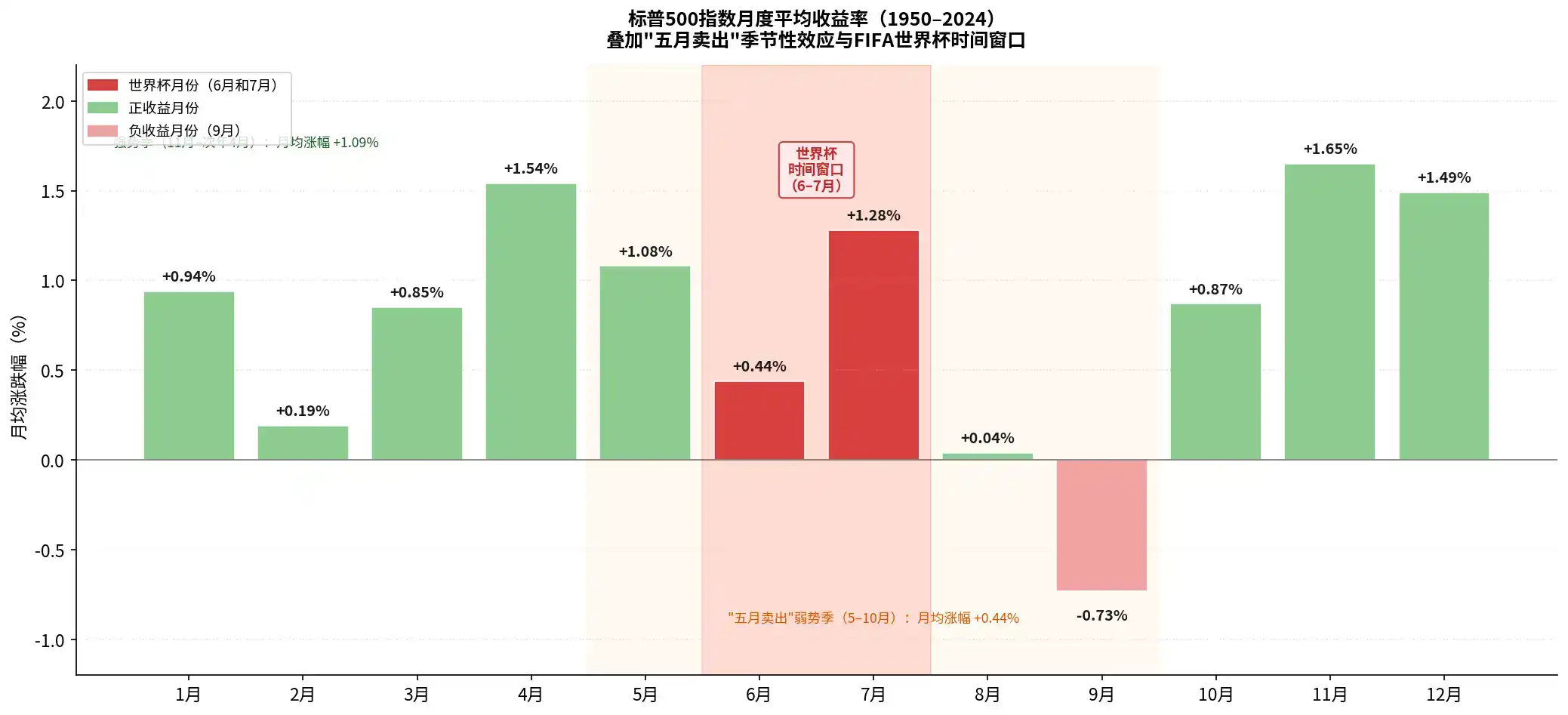

But why is the impact considered not major? Wall Street has an old adage, "Sell in May and go away." The stock market itself exhibits seasonal patterns, with May through October typically being the weakest performance period of the year (especially June-August). Traditional summer World Cups (June-July) happen to fall within this seasonal lull window.

As shown in the chart above, among the average monthly returns throughout the year, June (+0.44%) and August-September are often the most lackluster or even negative months. This means traditional summer World Cups (typically held from mid-June to mid-July) coincide with the window in the year when the stock market has the least upward momentum.

The 2022 Qatar World Cup was the first World Cup historically held in the Northern Hemisphere winter (November-December). This unique timing provides a "controlled experiment" to test the above theory.

Although the S&P 500 still fell 3.5% during the Qatar World Cup (mainly driven by the Fed's aggressive rate hikes), looking at trading activity, the decline in trading volume during the winter World Cup (about -18%) was significantly smaller than during traditional summer World Cups (-33%). This suggests that when the World Cup is detached from the summer lull, its liquidity-draining effect on the market weakens. This also indicates that a significant portion of the "World Cup Curse" should be attributed to the seasonal low of June-July itself.

Compared to the stock market, the cryptocurrency market better proves that the World Cup's influence on markets isn't significant. From Bitcoin's inception to now, during the 4 World Cups, its price movements can actually be traced to more direct catalysts:

- 2010 South Africa World Cup: On May 22, 2010, a story we're all familiar with happened—programmer Laszlo Hanyecz used 10,000 bitcoins to buy two pizzas, completing Bitcoin's first real-world goods transaction, giving it initial real-world value consensus. Three days after the World Cup closing ceremony (July 17, 2010), the famous Mt.Gox exchange officially launched, marking Bitcoin's entry into the era of organized trading.

- 2014 Brazil World Cup period: Bitcoin was in a bear market following the burst of the 2013 bull market (which peaked above $1,100). In February 2014, Mt.Gox, then the world's largest Bitcoin exchange, declared bankruptcy after losing hundreds of thousands of bitcoins to a hack, dealing a devastating blow to the entire industry. During the World Cup, market sentiment remained fragile. Additionally, on June 27, the US Department of Justice auctioned nearly 30,000 bitcoins seized from the "Silk Road," further increasing selling pressure and uncertainty in the market.

- 2018 Russia World Cup period: A bear market adjustment following the end of the 2017 bull run. The ICO bubble had burst, and global regulation was tightening comprehensively. During the World Cup, the crypto market faced continuous negative news. On June 22, the major Korean exchange Bithumb was hacked, losing $30 million. In early July, the US SEC again delayed/rejected multiple Bitcoin ETF applications.

- 2022 Qatar World Cup period: In early November 2022 (the week before the World Cup opening), FTX collapsed. Meanwhile, the Fed announced a 50-basis-point rate hike on December 13, with continued tightening of macro liquidity, adding insult to injury.

It's also important to consider that Bitcoin, as an asset traded 24/7 globally, is less affected by traditional seasonal holiday patterns. Its own 4-year "halving cycle" is very pronounced. In the face of macro liquidity and its own cyclicality, the World Cup effect is essentially negligible.

Investment Opportunities During the World Cup

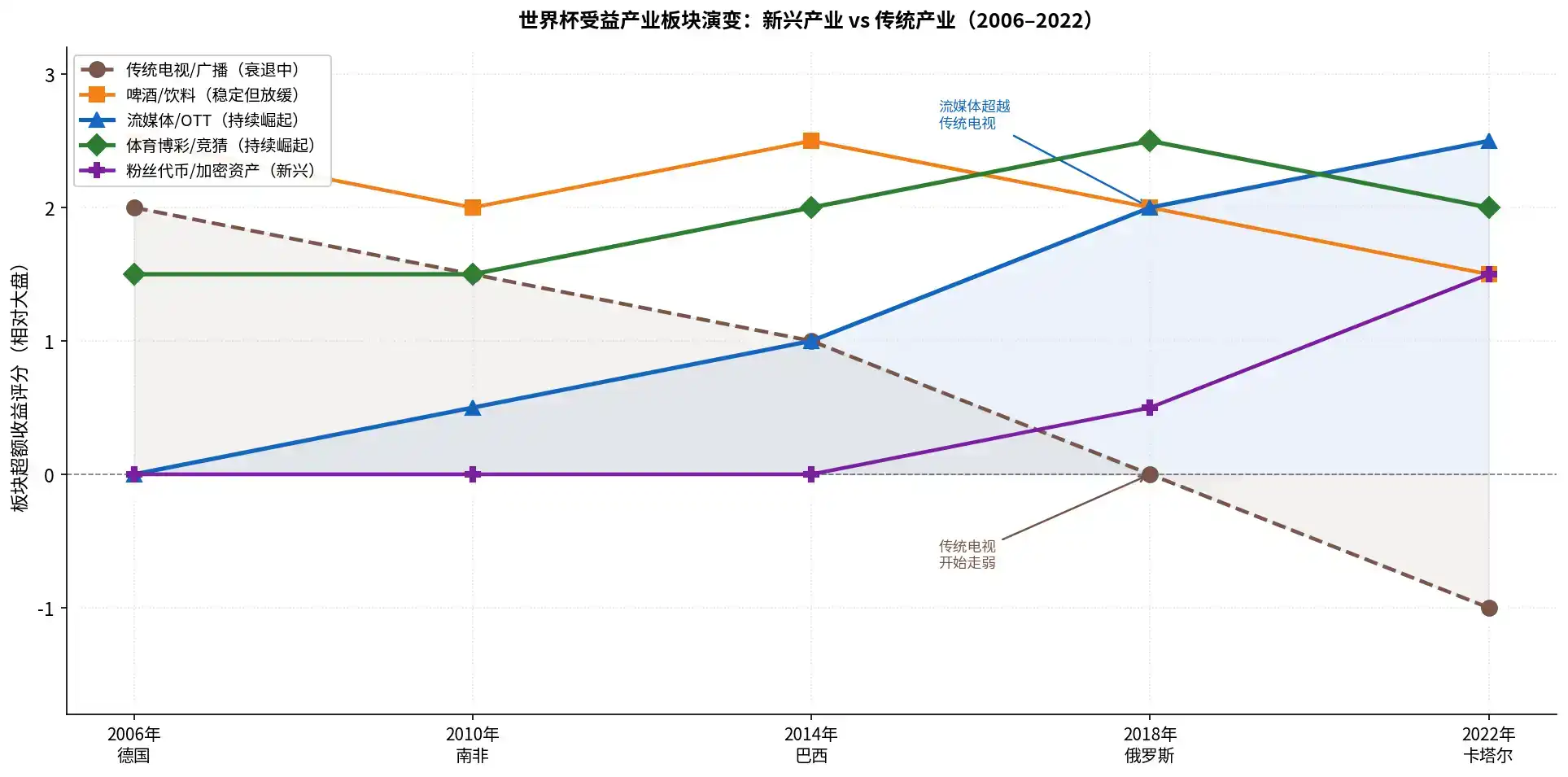

With technological advancement and changes in consumption habits, the landscape of World Cup beneficiary industries has changed over the past two decades (2006-2026).

In the past, we all watched the World Cup on TV. During the 2006 and 2010 World Cups, traditional TV and set-top box manufacturers often achieved significant excess returns.

But by the 2018 Russia World Cup, although traditional TV broadcasting rights revenue still accounted for a large portion, the excess returns for TV manufacturers had dropped to 0. By 2022, domestic TV sales during the World Cup decreased rather than increased, with the industry seeing both volume and price declines. Related listed companies' stock prices also underperformed the broader market.

Streaming has officially replaced traditional TV as the core channel for watching the World Cup. The 2022 Qatar World Cup set a new record for streaming viewership. If you're bullish on World Cup viewership, perhaps more attention should be paid to streaming companies with exclusive broadcasting rights that can convert viewership into revenue.

Beer and sporting goods (like Nike, Adidas) are classic World Cup consumer categories, and their sector performance has been stable across past World Cups, but they also face slowing growth challenges in recent years.

Data from investment bank Jefferies shows that global beer sales grew by 3.6% during both the 2006 and 2010 World Cups. However, data from IWSR indicates that from 2014 to 2024, global overall beer consumption actually fell by 3%, with younger generations leaning more towards low-alcohol or alcohol-free beverages.

This means stocks like Budweiser and Tsingtao aren't hopeless, but new beverage stocks, new-style bars popular with young people, etc., might also perform well.

And compared to buying jerseys and shoes, young people might prefer trading cards, which can highlight advantages on-chain. For example, on the Base chain's fractionalized card platform Grail, the token price for Cristiano Ronaldo cards has surged nearly a hundredfold since May 5, and the token price for Kylian Mbappé cards has risen nearly 300-fold since May 5.

Sports betting is also a classic World Cup beneficiary sector, but the growth of prediction markets has been very rapid as well, though there aren't very good investment vehicles for prediction markets yet.

Conclusion

For a good World Cup viewing experience, stepping away from the market to relax is actually a good choice.

Israeli economists Guy Kaplanski and Haim Levy published a paper in the *Journal of Financial and Quantitative Analysis* in 2010 (cited over 261 times), which stated:

"The average return of the US stock market during World Cup periods is -2.58%, while the average return for all trading days in the same periods is +1.21%. The most natural investment strategy is to short stocks before the World Cup kicks off, which would further reinforce the stock price decline effect."

Although there's no famous instance of directly liquidating positions due to the World Cup, the World Cup window is indeed a period of poor liquidity. Regardless of the specific reasons for market movements being directly related to the World Cup, enjoying the World Cup itself might be the best defensive posture for facing a period of weaker market liquidity.