The cryptocurrency industry is approaching its “Netscape moment,” as steady progress in blockchain infrastructure and the rise of regulated investment products drive a new wave of institutional adoption, according to Paradigm co-founder Matt Huang.

The crypto sector is “facing its ‘Netscape’ or ‘iPhone’ moment,” Huang wrote Sunday in a post on X. “It’s working bigger than ever before, far beyond our wildest dreams. Both the institutional parts and the cypherpunk parts.”

Netscape launched the first easy-to-use web browser for mainstream users in 1994 before going public with a successful initial public offering (IPO) in August 1995, marking the first building block that triggered the internet’s mass adoption.

However, Microsoft saw the large-scale interest and capitalized on it on it by freely bundling Internet Explorer as a pre-installed component of the Windows operating system, outcompeting Netscape to become the most widely used internet browser.

Onchain usability meets regulated access

In the crypto world, Bitcoin’s (BTC) peer-to-peer model and decentralized finance (DeFi) have enabled a new vision of an open, programmable financial system that cuts out intermediaries.

At the same time, centralized platforms and traditional investment vehicles are attracting a growing share of new capital because they are easier to use and fit within familiar regulatory frameworks.

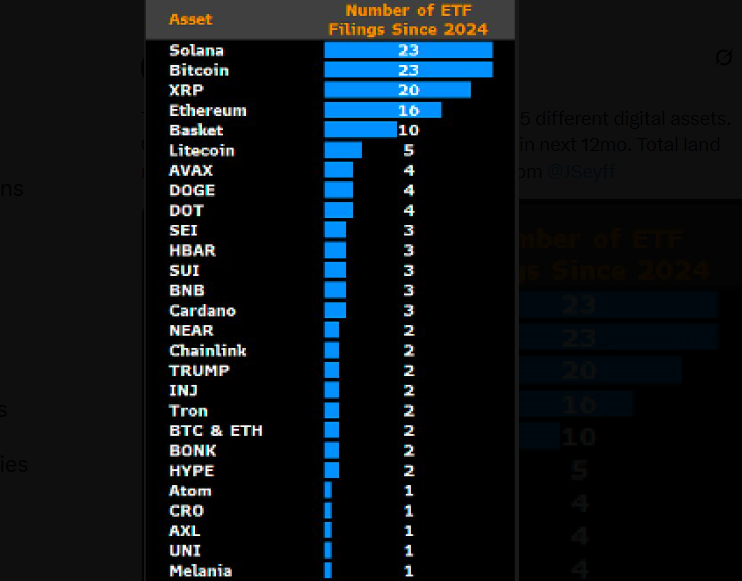

About 200 crypto-based exchange-traded products (ETPs) could launch on the market in the next year, with 155 awaiting approval as of Oct. 22, according to Bloomberg’s senior ETF analyst, Eric Balchunas.

Crypto ETPs provide easier access to altcoins for traditional investors on brokerage platforms that don’t have an account on a centralized cryptocurrency exchange.

Related: Prediction markets emerge as speculative ‘arbitrage arena’ for crypto traders

Onchain products are becoming easier to use, while “regulated” investment vehicles are making crypto more accessible, signaling that the industry may be at the tipping point ahead of mass adoption, Lacie Zhang, market analyst at Bitget Wallet, told Cointelegraph.

“ETFs and similar products legitimize digital assets but don’t replace what onchain systems uniquely offer, such as direct ownership, programmable settlement, and real-time transfers.”

She added that regulated access points tend to pull more liquidity onto underlying networks by drawing in institutional capital and new participants, rather than “displacing onchain activity.”

Related: Bitcoin now settles Visa-scale volumes, but most is for wholesale, not coffee

Despite some concerns about centralization, the rise of centralized finance (CeFi) platforms and ETFs is an “expansion of the onchain economy,” not an inherent threat, according to Marcin Kazmierczak, co-founder of RedStone, a blockchain oracle solutions provider.

“The Netscape moment isn’t about onchain versus CeFi. It’s about the broader crypto ecosystem finally attracting capital that actually stays around long-term,” he told Cointelegraph, adding that the two ecosystems are “not adversarial.”

Netscape moment or dot-com bubble repeat?

However, the crypto industry may still risk a market crash akin to the dot-com bubble, considering that the majority of revenue is derived from speculative memecoin trading for some blockchain networks.

On Solana, memecoin trading accounted for 62% of the network’s decentralized app revenue in June, and the majority of its $1.6 billion in revenue for the first half of 2025.

To reach its true potential, the developers need to focus on advancing the industry’s real-world utility, as the only “real risk” to the industry is a “slowdown in technological development,” according to Edwin Mata, lawyer, co-founder and CEO of tokenization platform Brickken.

“What matters is that onchain environments continue creating functionality, automation, and new market structures, because that is where fundamental value is produced,” he told Cointelegraph.

Magazine: Solana vs Ethereum ETFs, Facebook’s influence on Bitwise — Hunter Horsley