Author: José Sanchez & Kelvin Koh

Compiled by: Deep Tide TechFlow

Deep Tide Introduction: In February 2026, the way traditional financial institutions entered DeFi underwent a qualitative change: no longer through strategic partnership announcements, but by directly purchasing governance tokens and routing products to decentralized infrastructure.

Within five days, Citadel bought ZRO, BlackRock bought UNI and listed BUIDL on UniswapX, Apollo committed to acquiring 9% of Morpho's token supply over four years. Spartan Group believes this is the true inflection point for the institutionalization of DeFi.

Full Text Below:

Inflection Point for DeFi Institutionalization

February 2026, within just five days, a cluster of landmark institution-crypto collaborations emerged, which we believe marks a qualitative change in how traditional finance participates in on-chain infrastructure.

Citadel Securities announced an investment in LayerZero's ZRO token; BlackRock listed its $2.5 billion BUIDL fund on UniswapX and purchased UNI tokens; Apollo Global Management committed to acquiring up to 9% of Morpho's total governance token supply over four years.

Previously, the NYSE had already announced on January 19th the launch of a tokenized securities platform supporting 24/7 on-chain settlement. The pattern is clear: institutional capital is shifting from exploration to real on-chain execution—buying tokens, acquiring governance rights, routing products to decentralized infrastructure.

This wave of entry differs from previous cycles in three ways.

First, these are direct token purchases that create economic alignment, not advisory arrangements or pilot declarations.

Second, the related products are actively operating with real revenue: BUIDL manages $2.5 billion, Morpho supports over $900 million in active loans for Coinbase, LayerZero has settled over $70 billion in USDT0 cross-chain transfers.

Third, institutions chose public, permissionless protocols, not proprietary closed systems, indicating that the composability and network effects of existing DeFi infrastructure are more valuable than the control offered by custom systems.

The NYSE kicked off this show on January 19th, announcing plans to build a blockchain-based venue supporting 24/7 trading and instant on-chain settlement of tokenized stocks and ETFs, combining its Pillar matching engine with a blockchain post-trade system. Although still subject to regulatory approval and implementation details are relatively limited, this is the highest-level directional signal: the world's most iconic stock exchange is targeting on-chain settlement as core infrastructure.

LayerZero followed on February 10th with Zero, a new L1 designed for institutional-grade financial infrastructure. Citadel Securities made a strategic ZRO token purchase, significant for a firm handling about 35% of US retail stock trading.

DTCC will explore using Zero to expand its tokenization and collateral management capabilities; ICE is evaluating the chain for 24/7 trading infrastructure; Google Cloud joined to explore AI Agent micropayments; ARK Invest holds both equity and token positions, with Cathie Wood joining the advisory board.

Tether also announced a separate strategic investment in LayerZero Labs on the same day. Zero is expected to launch in Fall 2026, with three zones: a general EVM environment, a privacy-focused payments zone, and a dedicated trading zone.

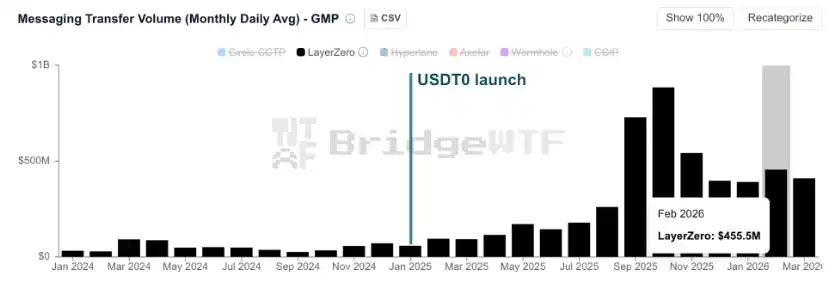

Institutional interest reflects proven throughput capability. USDT0—Tether's omnichain stablecoin built on LayerZero's OFT standard—has facilitated over $70 billion in cross-chain transfers since January 2025.

As shown in the figure below, daily settled value accelerated sharply after USDT0's launch, transforming LayerZero from a messaging layer into critical financial infrastructure.

Figure: USDT0 has facilitated over $70 billion in cross-chain transfers since launch

Source: BridgeWTF

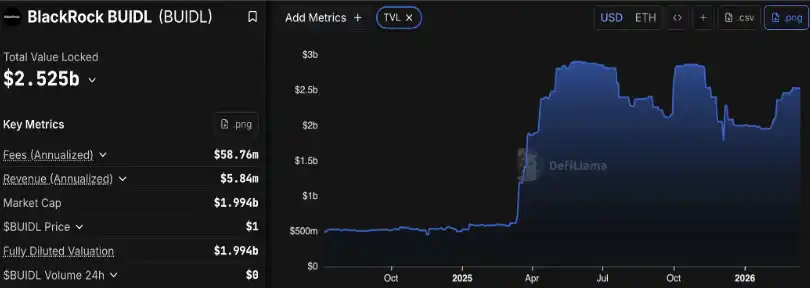

The next day, BlackRock's $2.4 billion BUIDL fund (the largest tokenized US Treasury product) was listed and made tradable on UniswapX, marking the first time a BlackRock product became accessible via decentralized exchange infrastructure.

Securitize handles compliance and whitelisting, while Wintermute, Flowdesk, and Tokka Labs compete for quotes through UniswapX's RFQ framework. BlackRock also disclosed a strategic UNI token purchase (specific terms not yet public), its first DeFi governance token on its balance sheet.

Although BUIDL's access is still limited to qualified purchasers with a minimum of $5 million, Securitize CEO Carlos Domingo stated that the infrastructure is designed to scale to retail products over time.

The decision to list on Uniswap reflects BUIDL's evolution from a niche experiment to an institutional-scale product. Since launching in March 2024 with a $40 million size, the fund peaked at nearly $2.9 billion in mid-2025 and currently has a TVL of around $2.5 billion.

Figure: BlackRock's BUIDL fund currently has a TVL of $2.5 billion

Source: Defillama

On February 13th, Apollo Global Management signed a cooperation agreement, committing to acquire up to 90 million MORPHO tokens over 48 months, approximately 9% of the total supply.

In addition to the token acquisition (valued at approximately $110 million at mid-February prices), Apollo will also collaborate to build on-chain lending markets, extending its blockchain footprint—part of its credit strategies are already tokenized via Securitize (ACRED) and Anemoy (ACRDX).

This deal is one of the most significant collaborations to date between an institution and a native DeFi protocol.

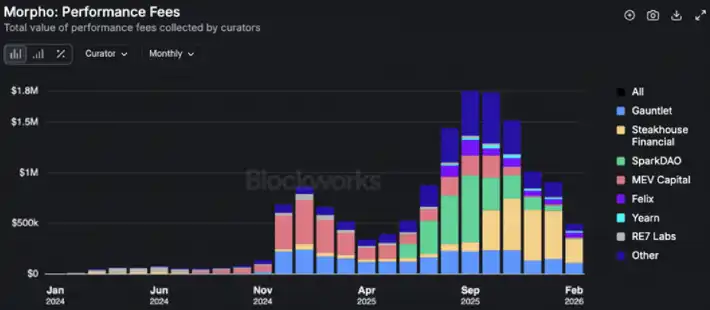

The opportunities for institutions within Morpho extend beyond token ownership. The protocol's architecture allows any entity to become a vault curator, building lending markets with customized risk parameters. Curators can earn performance fees from generated yield and management fees (capped at 5%) from AUM, creating a sustainable revenue model for institutional participants.

Perhaps the most convincing validation of the infrastructure is the CeFi-DeFi "Mohawk" model pioneered by Coinbase: retail users borrow against BTC and ETH collateral through the Coinbase interface, while Morpho acts as the lending engine on the backend, currently supporting over $900 million in active loans and $1.7 billion in collateral.

This proves that institutional-grade DeFi can be abstracted and scaled to operate behind familiar consumer interfaces, with users not needing to interact with the underlying protocol.

For Apollo, the vault curator economics, the validated distribution channel via Coinbase, and the governance influence gained through token accumulation together form a strong positioning in the on-chain credit space.

This convergence validates the design choices of permissionless, composable protocols and suggests sustained demand for governance tokens of infrastructure layer projects.

Key risks remain in execution: regulatory approval for the NYSE platform and Zero is pending, institutional token purchases may test protocol governance, and the gap between announcements and sustained on-chain activity remains significant. Nonetheless, the directional signal is unmistakable.

Figure: Morpho vault curators have generated substantial fee revenue

Source: Blockworks Research

Looking ahead, we expect these partnerships to deepen further once the CLARITY Act is passed. The Act passed the House in July 2025 by a vote of 294 to 134 and is now advancing in the Senate, where the Banking and Agriculture Committees need to reconcile their respective draft versions before a full vote.

The main point of contention is the treatment of stablecoin yield: the banking side is pushing to restrict interest payments on stablecoin balances, while crypto firms argue this would push innovation overseas.

July is widely seen as a key deadline before the August recess; if missed, the next window will be delayed until the fall. Once enacted, the CLARITY Act will provide the US's first comprehensive digital asset regulatory framework, clarify SEC/CFTC jurisdiction, establish a registration path for digital commodity exchanges, and provide legal certainty for tokenized products.

For protocols like Morpho and Uniswap, this will remove the regulatory ambiguity that currently constrains the scope of institutional cooperation. We believe this will unlock a second, broader wave of TradFi-crypto integration.