Author: Curry, Deep Tide TechFlow

The most talked-about layoff news in the tech world recently involves Oracle, the world's largest enterprise database company; most banks and airlines worldwide run its software in their backend systems.

According to CNBC, the company laid off approximately 30,000 employees. A few days later, it appointed a new CFO with a total compensation package of $29.7 million.

30,000 people out, one person in.

Those leaving received severance pay equivalent to a few months' salary on average, while the newcomer's contract alone is worth a year's wages for a thousand people.

This sparked heated discussions on Reddit, with over 6,000 comments. Most are angry that one executive's salary equals that of many workers, feeling the new CFO is overpaid.

Executive pay being multiples or even tens of times higher than that of ordinary employees at major companies is not a new topic. But beyond the compensation itself, what caught my attention is the resume of this new CFO.

The new CFO is Hilary Maxson.

Before joining Oracle, she was the group CFO at Schneider Electric for nearly a decade. Schneider Electric is one of the world's largest energy management companies, with core businesses in power supply solutions for data centers and grids, generating over $45 billion in annual revenue.

Prior to that, she worked at AES Corporation for 12 years. AES is a longstanding U.S. power company focused on building and managing power plants and grids.

In other words, Oracle spent $29.7 million to hire someone whose entire career has revolved around electricity. She has managed power plants, grids, and companies that supply power to data centers... and now she's been hired as CFO by a company that has sold database software for 47 years?

There's another little-known fact about this choice.

Oracle has not had a dedicated CFO for the past 12 years; finances were managed concurrently by former CEO Safra Catz. According to CNBC, after Catz transitioned to executive vice chairman in late 2025, an interim financial officer temporarily filled the role for half a year.

The fact that the company is now specifically reinstating this position and recruiting from the energy industry is more significant than the salary figure itself.

Bloomberg Intelligence analysts interpret this appointment as a sign that Oracle's growth focus has shifted from databases and software to cloud infrastructure, hence hiring a CFO from an industrial company.

The numbers tell the same story.

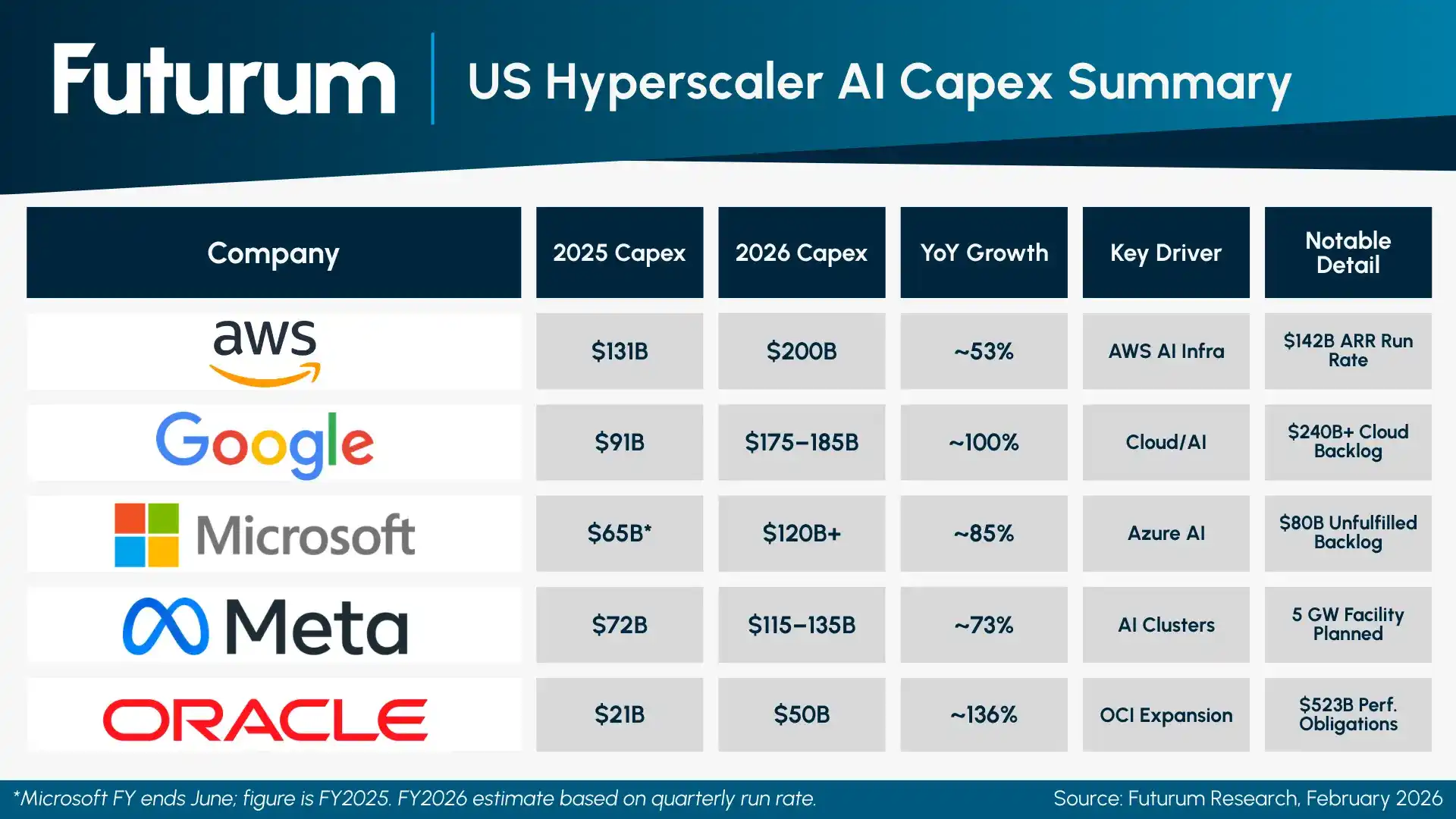

According to Oracle's latest earnings report, the company's cloud infrastructure revenue increased by 84% year-over-year. This year's capital expenditure budget is about $50 billion, almost entirely allocated to AI data center construction, more than double last year's amount. To raise funds, the company plans to secure $50 billion through debt and equity financing. The total value of pending contracts has surged to $553 billion, with one deal with OpenAI alone exceeding $300 billion, according to public information.

A company lays off 30,000 people maintaining old businesses and then entrusts money and authority to someone from the power industry. Reading this move, Oracle's management likely no longer sees itself as purely a software company.

But the capital market isn't buying it yet. Oracle's stock has fallen about 24% this year.

Investors' concerns are specific. Oracle historically made money by selling database software and enterprise applications, with high profit margins where people were the biggest cost. But AI is rewriting the business logic; large models can automatically write SQL and manage databases, gradually eroding the technological barrier Oracle has relied on for 47 years.

Oracle's response is to completely change tracks.

Instead of just selling software, it's turning to building data centers for AI companies. According to public information, Oracle previously signed an infrastructure contract with OpenAI exceeding $300 billion, part of the Stargate data center plan; similar agreements exist with Meta and xAI, pushing the total value of pending contracts to $553 billion.

This year's capital expenditure budget is about $50 billion, almost entirely poured into data center construction.

The two biggest expenses for data centers are chips and electricity. Cooling requires electricity, GPU operations require electricity; the annual electricity bill for a large AI data center can reach hundreds of millions of dollars.

Oracle is now building "gigawatt-scale" data center clusters. What is a gigawatt? Roughly equivalent to the output of a nuclear power plant.

This explains why they're hiring from the power industry.

The new CFO has managed power plants, grids, and companies that supply power to data centers. Oracle no longer needs a financial leader who understands software profit rates, but someone who knows how to spend tens of billions building power infrastructure and ultimately make these investments profitable.

Wall Street analysts are currently optimistic; 27 have given buy ratings, with an average target price of $245, implying about a 70% upside potential. But the gap between a 25% stock drop and analysts predicting a doubling hinges on the same question: whether Oracle can truly transform from a software company into an energy infrastructure company.

At least, they've taken a step in terms of personnel structure. Those leaving are people who wrote code for decades; those entering are people who managed electricity for twenty years.

Sometimes, to understand where a company is heading, you don't need to翻 its strategy PPT. Just see who it hires.