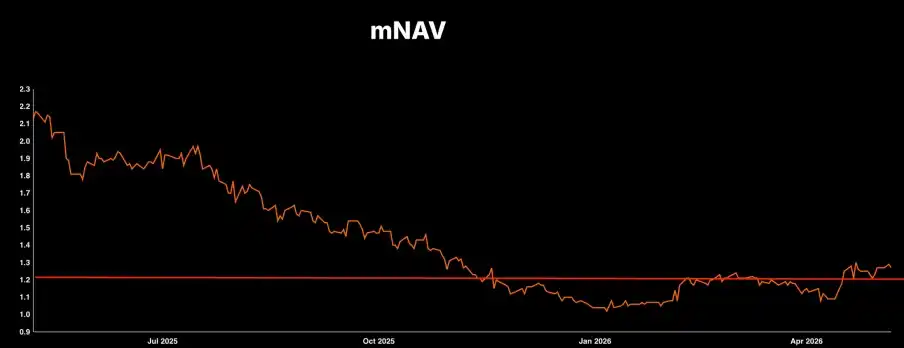

This MicroStrategy (MSTR) earnings report has completely changed its game: it used to be "mindlessly print shares to buy Bitcoin," but now the company has provided a clear-cut metric – a 1.22x mNAV (asset value premium). This number will determine whether MSTR buys or sells coins next.

● For MSTR:

○ Premium > 1.22x: Continue the old playbook: issue high-priced shares, take the money to buy BTC.

○ Premium < 1.22x (the core reversal): It no longer makes sense for the company to issue more shares. Management has explicitly stated that if the premium falls below this level, they will sell BTC, use the cash to repay debt or repurchase shares.

● How to arbitrage: If MSTR's premium falls below 1.22x, it will trigger a conditional arbitrage opportunity: "long MSTR, short BTC." Because at that point, the company will personally step in to "sell Bitcoin, buy its own shares." The company's selling action will close the price gap. Management's stance is the core confidence behind this arbitrage trade.

● For STRC (Preferred Stock): Previously, people feared that a MicroStrategy blow-up would render these 11.5% dividend preferred shares worthless. Now, the official statement "will sell Bitcoin to repay debt if necessary" means STRC has a solid safety net; it's no longer a Ponzi gamble.

● For the broader BTC market: The myth of "MicroStrategy will never sell" is shattered, which is negative for short-term sentiment. The benefit is that the company's proactive selling to reduce leverage completely eliminates the future risk of a "forced, cascading liquidation" during a deep bear market.

Diamond Hands No More: The 1.22x mNAV is the Lifeline and Bitcoin's Bull/Bear Dividing Line

Over the past two years, there has been much FUD in the market regarding MSTR, particularly about how they manage their leverage and interest expenses. Bitcoin is an asset without cash flow, yet MSTR has to pay significant interest for financing it. Where would this come from? In this Q1 earnings call, management personally declared: they will sell Bitcoin if the mNAV premium falls below 1.22x.

This is equivalent to revealing the company's "bottom card" and "auto-execution program":

● Above the waterline (balance sheet expansion phase): The company is a die-hard BTC bull. As long as retail investors are willing to give a premium higher than 1.22x, MicroStrategy can engage in "risk-free arbitrage balance sheet expansion." Issue shares to raise capital -> massively buy BTC -> increase book assets -> push the stock price higher. This positive flywheel keeps spinning.

● Below the waterline (defensive balance sheet contraction phase): The flywheel slams on the brakes. If MSTR trades at too steep a discount relative to its Bitcoin holdings, issuing more shares would mean selling company assets at a discount. Management very rationally stated that at this point, selling BTC for cash, using it to pay dividends, manage debt, or directly repurchase MSTR common shares at low prices would provide the greatest value enhancement for existing shareholders.

This means MSTR finally has a hard "value support line." It is no longer a runaway train without brakes.

Arbitrage Opportunity: Long MSTR / Short BTC when the mNAV premium falls below 1.22

What is the biggest fear in arbitrage? It's finding an excellent price discrepancy, but the market remains irrational for an extended period (e.g., MSTR stays at a discount), and eventually, your hedge position gets worn down by funding rates or interest costs.

However, the 1.22x threshold provided by MSTR this time offers an arbitrage opportunity with strong certainty.

In-depth practical logic:

● Strict trigger condition: Only when MSTR's mNAV premium falls significantly below 1.22x.

● Position entry: At this point, MSTR's price is "excessively undervalued" relative to its underlying BTC assets. Traders should go long MSTR and simultaneously short an equivalent market value of BTC.

● The winning underlying logic: Even if market participants don't close the gap, MicroStrategy's management will force it to converge. Once the threshold is breached, to maximize "Bitcoin per share," management will initiate their promised self-rescue operation – "sell BTC, repurchase undervalued MSTR shares." Do you see it? The direction of your long/short position will be completely synchronized with the official market intervention direction of MicroStrategy's tens of billions of dollars. You don't need to predict whether BTC will rise or fall tomorrow; you just need to calmly capture the "price gap convergence" profit, which is essentially risk-free.

Monitoring tip: Currently, MSTR's premium is fluctuating around 1.28x, not yet triggering the arbitrage condition. Blindly opening positions is premature. However, it has already entered an excellent targeting zone. Set up price alerts and wait for it to drop below the threshold before acting.

3. Significantly Enhanced Safety Net for STRC (Preferred Shares)

STRC offers a high dividend yield of 11.5%. In the previous bearish narrative, MicroStrategy was a gambler with massive leverage. Once Bitcoin faced a black swan event like a halving or more in price, MicroStrategy's cash flow would break, and STRC preferred shares would instantly become worthless.

But the Q1 earnings report completely revealed the company's true financials, not only refuting the shorts but also giving fixed-income investors a dose of confidence:

● Impressive asset thickness: On the liabilities side, the company has $13.5 billion in preferred shares and $8.2 billion in convertible bonds. On the asset side, there is a corresponding $64 billion in BTC reserves. The net leverage ratio is a negligible 9%, which is considered extremely robust in traditional finance.

● Extreme downside stress test: Even if the crypto market experiences another major crash, with BTC plummeting 90% from current levels (all the way down to $7,300), selling their coins would still be enough to repay all net debt.

● Cash moat: As a last resort, even if Bitcoin liquidity dries up and they can't sell quickly, the company still holds $2.25 billion in pure cash on its books. The interest earned from this cash alone, even at a savings rate, would be enough to cover the future 1.5 years (annual $1.5 billion) of debt interest and preferred dividends without lifting a finger. Overall, as long as BTC appreciates by a mere 2.3% annually, STRC's interest obligations can be perfectly covered.

The most crucial expectation reversal lies in this: management has broken the dogma of "never selling coins." This means they will proactively and gradually sell Bitcoin to preserve the company's credit rating and ability to pay interest before an extreme crisis hits. STRC has completely shed the label of "crypto Ponzi high-yield debt." Its risk pricing logic is now moving closer to that of traditional high-quality corporate bonds, making it highly likely to attract allocation buys from traditional institutional funds.

4. Impact on the Broader BTC Market: Losing a "Die-hard Buyer," Removing a "Cascade Liquidation Landmine"

The sentiment shock from this earnings call on the broader BTC spot market is two-sided, requiring traders to view it through different timeframes:

● Short-term pain (sentiment negative): Retail investors previously viewed MicroStrategy as a "bottomless pit" that only buys and never sells, providing perpetual support. Now, management's admission that "they will sell if valuation is wrong" directly shatters this bullish totem. In the short term, this is a significant blow to market optimism and speculative hype.

● Long-term benefit (structural upgrade of the foundation): Traders who understand a bit of cycle history know why the last bear market (2022) fell so hard. Because giants like LUNA, Three Arrows Capital, and Celsius "held on to the bitter end," until liquidity completely dried up and they were forcibly liquidated, leading to cascading sell-offs. The current MicroStrategy is no longer a "believer" swept up by狂热; it's a savvy "Wall Street veteran" who knows how to crunch numbers. It has set a clear early warning line for selling and understands how to proactively reduce leverage by adjusting its portfolio at the onset of a crisis. This is equivalent to defusing the largest "systemic liquidation nuke" hanging over the crypto market in advance.

Summary: MicroStrategy remains the largest "BTC bull commander-in-chief" in the entire U.S. stock market. However, it has evolved from a reckless charger into a precise calculator that knows when to advance and retreat, even harvesting market sentiment in reverse.