A Democratic U.S. Senator from California is introducing new legislation targeting crypto‐driven prediction markets

An Act Against Death

On March 10, Democrat U.S. Senator Adam Schiff (California) and Representative Mike Levin (CA-49) introduced the DEATH BETS Act, a bill aimed explicitly at banning prediction market contracts tied to terrorism, assassination, war or an individual’s death on any platform registered in the Commodity Futures Trading Commission (CTFC). This includes regulated venues like Kalshi or Polymarket’s newly U.S. licensed arm, plus other designated contract markets (DCM) that list event contracts via brokers.

The current law, the Commodity Exchange Act, gives authority to the CFTC to bar contracts tied to terrorism, war or assassination if they are deemed to be “contrary to the public interest”. Schiff’s proposed bill would revoke such flexibility: the senator argues that the agency has too much discretion as it rewrites prediction‐market rules under Chair Mike Selig:

At a time when CFTC Chair Selig has indicated that he will rewrite the rules on prediction markets, the CFTC can no longer be granted this discretion. The DEATH BETS Act will unequivocally ban these contracts.

The DEATH BETS Act And The Crypto World

The proposed bill follows the Senate Democrats pressure to the CFTC to “halt prediction contracts that involve betting on physical injury, death or war”, as stated on a letter sent to Chair Michael Selig in February 23. The letter specifically quotes Polymarket’s on-chain “dangerous prediction contracts” on whether the Artemis II would explode, if Venezuela’s former regime head Nicolás Maduro would be removed from power and if Ukraine’s Myrnohad would be captured by Russian forces.

“The Wild West”

In Senator Schiff’s words, the prediction markets have turned into “the Wild West”:

There is no justification for gambling on lives, or public benefit to be derived by such a market. With regulators turning a blind eye, prediction markets have rapidly become the Wild West.

Now, the Iran war episode takes the spotlight, as the Senator’s office highlights that a bet on whether Iran’s Ali Khamenei would be “out as Supreme Leader” had $54 million in trading volume on Kalshi before it was paused. There are hundreds of millions in Iran‐related bets, with a reported 10 wallets making over $1.2–1.4 million in profit right before U.S. strikes.

Rep. Levin stressed the importance of not letting “someone make money off the outbreak of war or the deaths of American service members”.

We already saw what that looks like: over half a billion dollars was wagered on the timing of U.S. military strikes on Iran alone. That is unacceptable, and this legislation puts a stop to it.

What The DEATH BET Act Means For Traders

Under the DEATH BET Act, CFTC‐supervised platforms will likely become safer but more limited, while riskier war/death flows are pushed further into offshore or permissionless crypto venues, where legal and reputational risks spike. Bets on elections, inflation points and macro data will continue to be safe game, but Washington aims to draw the line on banally “gambling” with the lives of real people.

The DEATH BET Act isn’t a ban on crypto prediction markets, but it is a signal that the next regulatory battles in crypto won’t just be over Bitcoin or ETFs: they’ll be over what the industry considers acceptable to let people bet on.

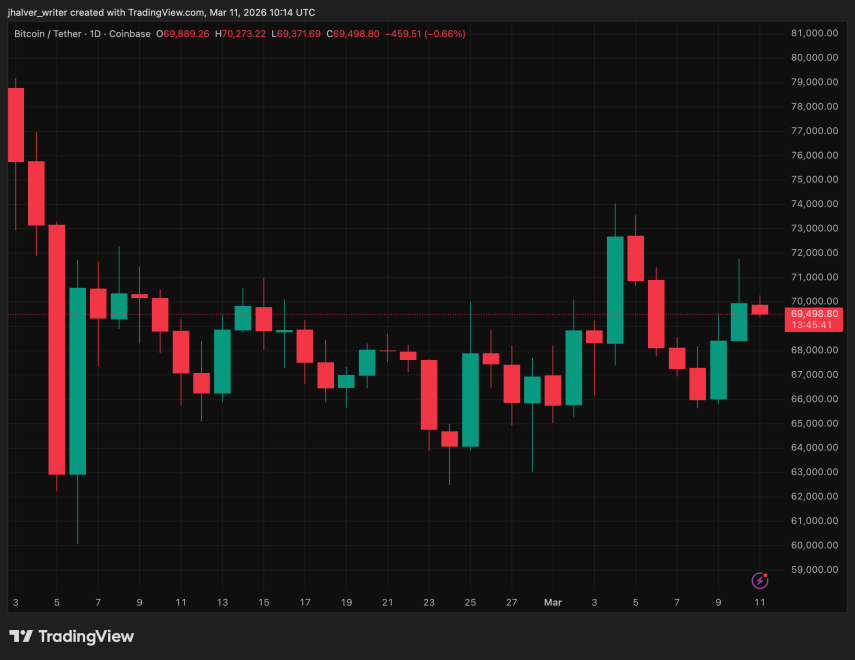

BTC’s price trends to the downside on the daily chart. Source: BTCUSDT on Tradingview

Cover image from Perplexity, BTCUSDT chart from Tradingview